What is Private Equity Financing?

Private equity financing is a broad and complex field, but simply put, its essence is a financial transaction. In traditional private equity financing, private equity financing is a financial transaction that involves exchanging fiat currency for equity.

Although private equity financing is just a financial transaction, it involves a lot of complex and specialized work and collaboration.

From the investment perspective, an investment typically goes through four stages: fundraising, investment, post-investment management, and exit. During this process, the work of institutions or fund managers involves entity registration, onboarding and managing investors, financial management, due diligence, and a large number of agreements, legal work, auditing, and more. As an investor, one needs to identify investment institutions and fund managers and review very complex fund recruitment documents. From the financing perspective, startups often need to undertake a lot of complex work to complete financing, including entity registration, financing planning and management, equity structure management, financial management, and so on.

These tasks often exceed the professional capabilities of the participants. Founders of startups usually lack financing experience and relevant professional skills, and many investors may feel confused by the large number of contracts (such as fund recruitment documents) and complex onboarding processes. Moreover, creating and operating a private fund is an enormous undertaking. To complete these tasks, they need to incur additional costs in terms of funds, time, human resources, and learning, and introduce more collaboration, such as hiring lawyers and financial managers. Therefore, private equity financing is a business with a high barrier to entry.

What is AngelList?

In the previous chapter, we mentioned that private equity financing involves a lot of complex and specialized work and collaboration, which not only makes participation difficult but also leads to high costs, low efficiency, and limitations on business boundaries.

AngelList is an online toolkit that serves the private equity financing field. Simply put, it abstracts the complex and specialized work involved in various stages of private equity financing transactions into various components and programs (different components and programs can be combined into different business flows, such as investor onboarding) and then uses internet technology to run it online, allowing people from around the world to efficiently participate in these business flows with just a simple click, without worrying about the specialized and complex specific tasks involved. For example:

Investment Institutions and Fund Managers: Investment institutions or fund managers can easily create an online operational framework through the tools provided by AngelList, such as Rolling Funds, Venture Funds, Syndicates, and Scout Funds. With these online tools, investment institutions and fund managers can conveniently and efficiently implement fundraising, investment, and other related tasks. Through the fund management tools provided by AngelList, investment institutions can easily create or link multiple bank accounts globally and use them as fundraising and investment accounts while ensuring asset security (e.g., sweep accounts feature). Additionally, AngelList provides tools to facilitate tasks such as agreement signing, tier sharing, notifications, and public announcements.

Investors: Investors can easily find excellent investment institutions through AngelList and conveniently contact and join them using the tools provided by AngelList (investor onboarding). Once investors join one or more investment institutions, they can easily view and track the operational status of the investment institutions using the tools provided by AngelList.

Startups: Startups can quickly initiate and manage financing using the financing tools provided by AngelList. Additionally, AngelList offers a series of management tools for startups, such as Cap tables and legal entity establishment. Furthermore, startups can manage funds through AngelList by linking their bank accounts for tasks such as transfers and taxes.

Two keywords: program, online.

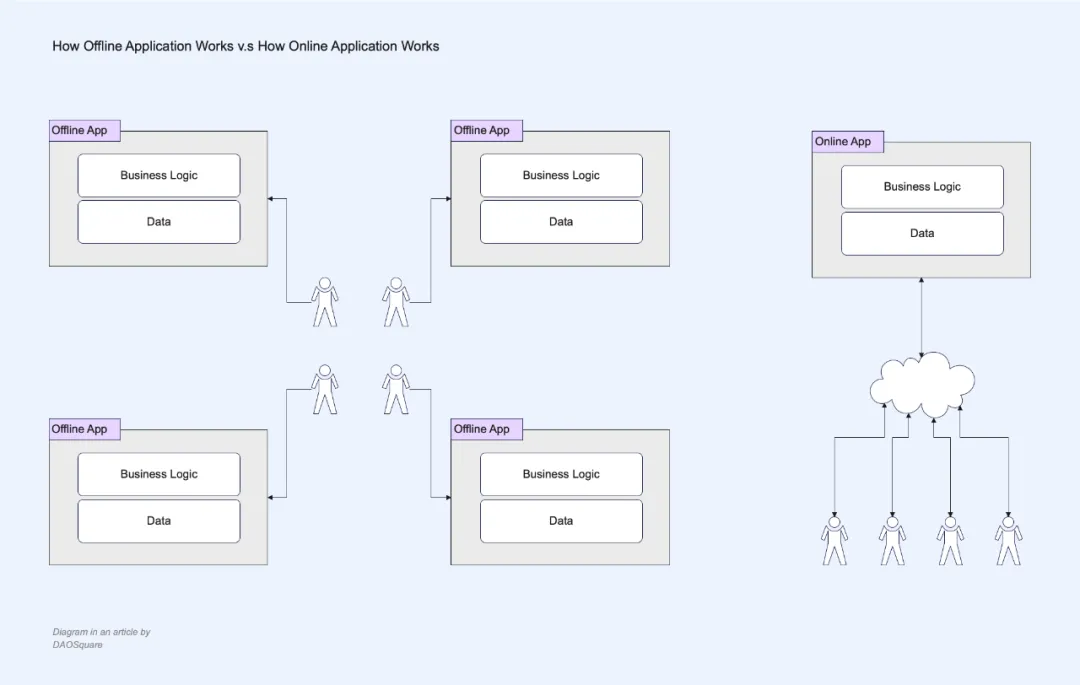

Online

Before the Online wave, applications were typically offline native applications, such as early financial management and text processing tools. From a technical perspective, simply put, the business logic and data of these applications were stored on the client side, not relying on a network environment. In contrast, Online deploys and runs the business logic and data of applications on cloud services and interacts with users via the internet. We can refer to such applications as online applications (a typical representative being web applications).

For example, before Google Docs was released in 2006, word processing applications like Word were offline native applications. If I wanted to invite others to co-edit a document, I could only export my document as a .doc file and send it to others (e.g., via email). They would import the file into Word to edit it, then export the edited document back as a .doc file and send it to me. I would need to open everyone's documents one by one, compile all the edits, and ultimately create the final version. This process often required many repetitions and was a disaster. Google Docs ushered us into a new era, where, as you see today, we can not only edit and modify in real-time with multiple people, comment and discuss in real-time, but also call any supported third-party applications in Google Docs, such as inserting a Google Sheet or a YouTube video. This is the significant change brought about by being online.

The work involved in private equity financing is much more complex than document collaboration. For instance, in a startup's financing, the startup needs to prepare financing materials and contact investors through different channels, then discuss and sign investment agreements with all interested investors, and subsequently manage the financing funds, establish an employee option pool, manage equity distribution, and more. Before the emergence of online tools represented by AngelList, these processes were completely disconnected, and we could only use some simple tools to manually complete these tasks. As the rounds of financing increased, these tasks became increasingly complex. Online tools made everything simpler. For example, using the financing tools provided by AngelList (Raise), startups can complete all processes in the financing process in a one-stop manner online, and due to the modular nature of the tools, the entire fundraising process can achieve a high degree of automation. For instance, when a fundraising round is completed, Raise automatically helps the startup update the equity structure table.

As you can see, Online has significant advantages: improving efficiency, expanding boundaries, and reducing financial and time costs.

Improving Efficiency: By moving workflows online, the efficiency of investor onboarding, investment processes, startup fundraising, legal agreement signing, and other tasks is greatly enhanced.

Expanding Boundaries: Online allows us to break through traditional social circles, giving investors more opportunities to participate in venture capital, enabling venture capital institutions to raise funds from more investors, connecting startups with more venture capital institutions, and allowing venture capital institutions to access more investment targets.

Reducing Costs: While improving efficiency and expanding business boundaries, the rich online tools also significantly reduce the financial and time costs of private equity financing tasks. For example, in Cap table management, as AngelList states:

AngelList's equity structure table eliminates the hassle of managing the startup's largest asset (equity). By leveraging unparalleled automation while maintaining compliance, better decisions can be made.

This is the paradigm shift brought about by technological change in specific industries.

New Challenges Brought by Crypto

Crypto private equity financing has one significant difference from traditional private equity financing: the investment currency in crypto private equity financing is usually cryptocurrency (e.g., USDT, USDC, ETH, etc.). Due to the inability to use private equity financing tools like AngelList, most crypto private equity financing currently employs simple management methods, such as managing fundraising assets through multi-signature wallets, completing fundraising and investment through manual transfers, and using traditional financial management software to record and manage funds and portfolios. This rough operational and management model not only causes efficiency and complexity issues but, more importantly, brings numerous risks.

Funding Risks

Typically, after a crypto investment institution completes fundraising, the investors' money is managed by the investment institution (using multi-signature wallets or even personal wallets), and the relevant personnel of the investment institution hold the management rights over the funds, while investors (such as LPs of the fund) do not have substantial guarantees. Therefore, technically, they can misappropriate these funds or even run away with the money. As you can see, such incidents have already occurred. Since the crypto private equity financing industry is still far from being regulated, and most jurisdictions' support for crypto is still inadequate, it is challenging to protect the rights and interests of investment institutions and investors through legal means.

Default Risks

Currently, all transaction links in crypto financing rely on paper contracts to bind both parties. For example, investment institutions raise funds from investors, investment institutions invest in startups, and startups release tokens to investment institutions. This reliance on traditional trust mechanisms is effective in traditional equity private equity financing, but its binding force is limited in crypto, as most jurisdictions' support for crypto is still inadequate. Especially since crypto financing is often cross-jurisdictional, the difficulty is further amplified.

Chaos in Venture Capital

In the field of crypto private investment, there are many organizations and individuals that are essentially cryptocurrency speculation groups and second-hand dealers masquerading as VCs. They obtain investment shares in startups under the guise of being VCs, then use social means to exaggerate and promote to temporarily inflate the token price before selling, or they sell the shares at a premium to other institutions and individuals after acquiring them. Such institutions not only fail to provide actual help to startups but also create numerous troubles, obstacles, and even harm to startups, which is extremely detrimental to their development. Startups often find it challenging to effectively identify these speculation groups and second-hand dealers.

The above only discusses the core interest issues of the various participants in the crypto financing field. There are many other issues, but without a doubt, asset-related issues are particularly concerning. So, in a situation where traditional trust mechanisms (such as the judicial system) cannot effectively protect the rights and interests of crypto financing participants, is there a way to address these risks?

New Opportunities Brought by Crypto

Cryptocurrency presents new challenges for private equity financing, but on the flip side, cryptocurrency also brings new opportunities for private equity financing.

In the section "What is Private Equity Financing," we discussed that traditional private equity financing can be viewed as a financial transaction that exchanges fiat currency for equity. Since these two transaction objects exist in different accounting systems (currency and equity structure), the transaction can only proceed asynchronously, that is, 1) payment of the investment amount and 2) allocation of equity. Therefore, to ensure the performance of both parties in the transaction, a third party must be introduced, namely traditional trust mechanisms (such as the judicial system) to bind both parties. In contrast, the investment currency in crypto private equity financing is usually cryptocurrency, and startups often use cryptocurrency to represent their enterprise value (such as ETH, CRV, RICE, etc.).

This means that we can view crypto private equity financing as a form of currency-to-currency transaction, and it is a currency-to-currency transaction within the same accounting system (blockchain).

Compared to traditional private equity financing, this currency-to-currency transaction not only simplifies various financing stages such as fundraising, investment, management, and exit, but also, thanks to the many technical characteristics of cryptocurrencies, allows these transactions to be constrained from a technical perspective without relying on traditional trust mechanisms such as the judiciary, insurance, or arbitration to protect the rights and interests of both parties, thereby addressing many of the risks mentioned above.

Let’s briefly understand cryptocurrencies through several technical concepts (smart contracts, programmable money, data availability) and how they can solve the aforementioned risk issues, thus bringing new opportunities to private equity financing.

Smart Contracts

In the context of blockchain, a smart contract is a program deployed and stored on the blockchain that receives user instructions and executes results according to programmed logic (internal or external). It is similar to a vending machine; when a user selects a bottle of cola and pays the amount set by the program (for example, 1 USD), the vending machine will automatically "dispense" a bottle of cola.

Unlike a vending machine, once a smart contract is deployed on the blockchain, it is typically irreversible and immutable. This means that no one can alter it. In other words, we cannot modify the programming logic of this "vending machine" after it starts running to make it dispense 10 bottles of cola when a user selects one bottle and pays 1 USD. It will always operate according to the logic of 1 USD for 1 bottle of cola. Of course, you might say that a hacker attack could do this, but that is another topic.

Additionally, due to the permissionless nature of smart contracts, no one can prevent users from using them.

Programmable Money

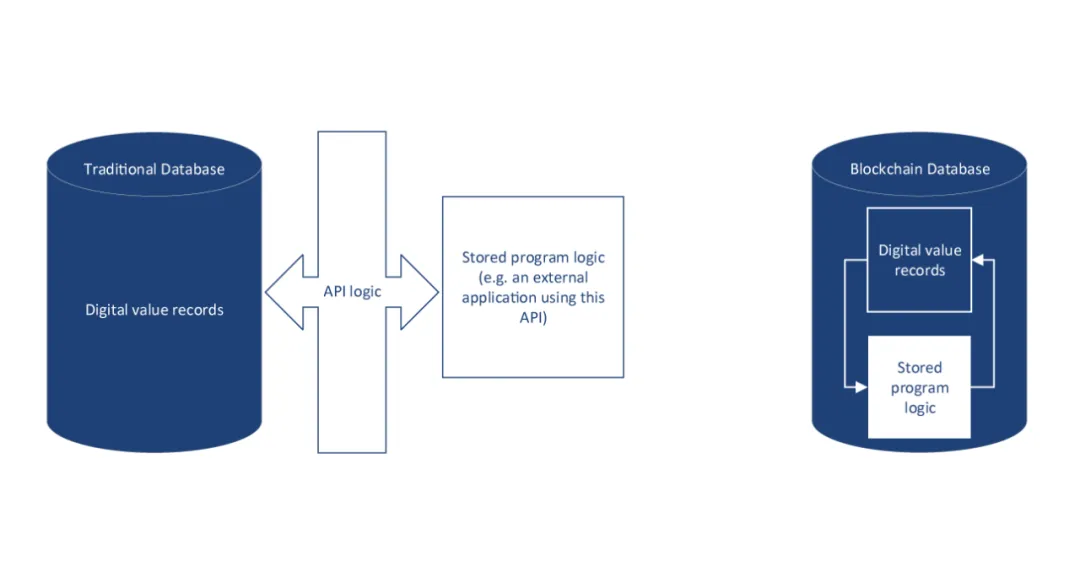

Whether in traditional financial systems or on the blockchain, digital currency is realized through "digital value records," and they can both be referred to as digital currencies. In traditional internet financial systems, digital currency is a set of digital records representing tradable value stored in an online database, which allows external programming logic (such as online banking apps) to adjust the digital value records in the database through APIs.

In contrast, on the blockchain, digital currency is a smart contract (such as ERC20) specifically designed for monetizable assets, deployed and stored in the blockchain database. It also contains digital records representing tradable value, but the adjustments to its digital records are:

Constrained by its own programming logic. Just like the vending machine example mentioned above.

Allowing other smart contracts' programming logic within the blockchain database to adjust its digital value records, provided they comply with its own programming logic. This is akin to a vending machine connected to a lucky wheel, where users can choose not to select cola when inserting 1 USD but instead authorize the vending machine to use the lucky wheel to determine which drink it dispenses. You know, the lucky wheel might have cola, a car, or it could just say "Thank you."

Due to its programmable nature, this type of digital currency operating on the blockchain is also referred to as programmable money, but we usually call it cryptocurrency.

Data Availability

The blockchain is not only an open network (anyone can access and use it) but also possesses the characteristic of data availability. This means we can access any user's blockchain account to verify any transaction that user has made on the blockchain. Therefore, it can help us:

Verify the investment history of investment institutions.

Verify the investment preferences of investment institutions.

Verify the investment strategies of investment institutions (long-termism or speculation).

Monitor and track the flow of funds in investment institutions. For example, if an institution shows signs of misappropriating funds, we can take timely action to stop it or assist relevant institutions (such as judicial bodies) in handling the situation.

As you know, in traditional finance, these are simply fanciful ideas.

Now, let’s see how we can utilize these technical characteristics to address the three types of risks mentioned above.

Fund Security

For example, we can deploy a fund management contract on the blockchain for investment institutions, allowing them to invite investors to deposit funds (such as USDT) into this contract to complete fundraising. The control of the funds in this contract account is constrained by the programming logic of the contract. The investment institution can set up a management team during the contract deployment to control the funds through a voting mechanism (fund model), or it can give control of the funds to all investors (investment club). This can technically prevent internal personnel of the investment institution from misappropriating funds.

We can also deploy a redemption contract to enhance the security of the fund management contract. We can set a fixed redemption period, just like traditional open-end funds, for example, every 30 days. This way, investors can decide every 30 days whether to continue keeping their funds with the investment institution or withdraw them based on their assessment of the institution's performance. Alternatively, we can set the redemption period to occur after each investment transaction is initiated, allowing investors to decide whether to participate in a specific investment based on their agreement with it. Due to the permissionless nature of smart contracts, the act of investors redeeming to protect their fund security cannot be blocked by any party.

Performance Security

Take a SAFT investment agreement as an example. We know that while we can view crypto private equity financing as a currency-to-currency transaction, it is usually not as simple as a swap where payment and delivery occur simultaneously. Instead, there is typically a Vesting Schedule, meaning that after receiving the investment amount, the investee will start releasing the payback currency to the investors at a future time according to certain release rules. Therefore, the Vesting Schedule is usually the most important part of the SAFT investment agreement and also the part most prone to defaults and disputes.

We can deploy an investment agreement contract on the blockchain to implement the trading rules in the SAFT agreement through programming logic, including investment currency, payback currency, price, Vesting Schedule, etc. When the investment institution and the investee create an investment transaction through this smart contract (agreeing on various parameters, such as the Vesting Schedule) and "sign" the transaction, at the same time the investment institution pays the investment amount, the investee's payback currency will be held in escrow by the smart contract, allowing investors to autonomously claim the payback token from the smart contract according to the timeline set in the Vesting Schedule (no one can stop them). For instance:

Investor Bob uses the investment agreement smart contract to create a SAFT investment transaction with entrepreneur Lisa, with the transaction details as follows:

Investment Currency: USDT

Investment Amount: 100,000

Investor: 0x1Bfe1F47a3566Ee904d5C592ab9268B931516B56 (Bob's wallet address)

Investment Fund Receiver: 0xEF72177cb6CE54f17a75c174C7032BF7703689b4 (Lisa's wallet address)

Payback Currency: RICE

Payback Amount: 100,000

Vesting Start: 10/01/2025

Vesting End: 10/01/2028

Claim Interval: 30 Days

When Bob and Lisa "sign" this transaction on the chain, 100,000 USDT from Bob's wallet will be transferred to Lisa's wallet address, while 100,000 RICE from Lisa's wallet will be transferred to the escrow contract. Starting from October 1, 2025, Bob can claim RICE from the escrow contract every 30 days, with each claim being one thirty-sixth of the total amount, until October 1, 2028, when he can claim a total of 100,000 RICE. Moreover,

Bob will definitely be able to claim RICE from this smart contract starting from October 1, 2025, without needing anyone's permission.

Lisa cannot prevent the execution of this agreement after the investment transaction is successful.

Lisa cannot withdraw RICE from the escrow contract.

No one can stop Bob from using this contract to claim RICE.

Venture Capital Screening

Due to the openness and data availability of the blockchain, we can access the fund management accounts of investment institutions on the blockchain at any time and analyze their historical transactions to verify whether the institution's claimed investment performance and philosophy are true. For example, if Bob claims to be very optimistic about Lisa's project and intends to hold RICE long-term, but his transaction records show that he immediately sells all RICE after each claim, then you should be cautious when Bob approaches you expressing a desire to invest in your project. Alternatively, if Bob immediately transfers large amounts to a group of people after each claim, it is highly likely that Bob is a second-hand dealer.

In addition, we can summarize the investment preferences of investment institutions, such as investment fields, by analyzing these historical transactions, which can also significantly save the time cost for startups in seeking investment institutions and communicating with them.

Onchain

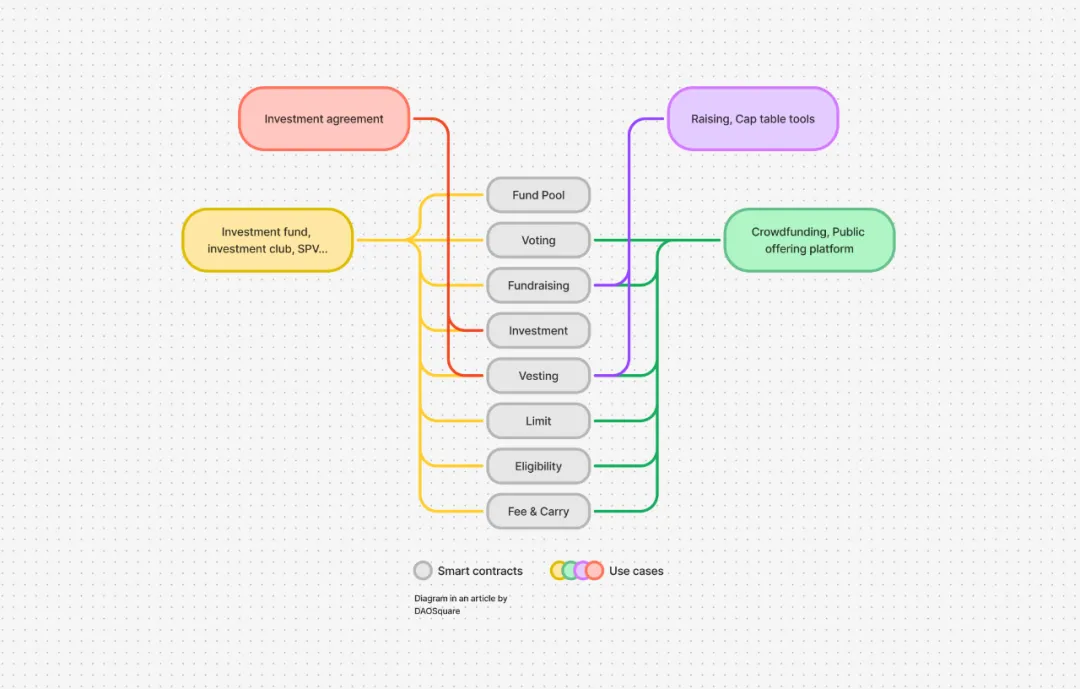

Above, we briefly introduced how to bring crypto investment and financing transactions on-chain to highlight its advantages in asset security, as well as how to leverage the technical characteristics of blockchain data availability to help us better identify investment institutions. As you know, crypto investment and financing also involve a large number of other transaction and management processes. If we bring all these transaction and management processes on-chain, that is, by building a corresponding smart contract for each transaction process and allowing these contracts to be freely combined and called upon each other, we can create an on-chain investment and financing toolkit, essentially an on-chain AngelList.

The above image lists some basic smart contracts, such as the Fundraising contract for fundraising, the Limit contract to restrict the number of participants in fundraising, the Fund Pool for holding funds, the Voting contract to control the fund pool, the Investment contract for investments, the Vesting contract for releasing project tokens, the Eligibility contract to restrict the qualifications of fundraising participants or fund managers, and the Fee & Carry contract to help investment institutions generate returns.

We can freely combine these contracts to achieve different functions, just like LEGO. As shown in the image, we can use a combination of the Investment and Vesting contracts to form a simple on-chain investment agreement. Once both parties confirm, it will automatically execute the transaction according to the agreement, which cannot be blocked or altered, and does not require the intervention of any third-party trust mechanism.

Startups can use a combination of the Fundraising and Vesting contracts to build an on-chain enterprise management tool for managing fundraising and the cap table.

Furthermore, we can use a combination of the Fundraising, Vesting, Limit, Eligibility, and Voting contracts to create an on-chain crowdfunding platform or launchpad, which will be truly decentralized, permissionless, and community-driven, without the asset risks associated with centralized control.

We can also use all the contracts listed in the image to build more complex businesses, such as running a private equity fund, investment club, SPV, etc. With more functional modules, we can meet more complex business needs, such as setting redemption periods and redemption fees for funds, or implementing a GP + LP fund operating structure, and so on.

These contracts not only provide us with trustless transaction guarantees, but they also standardize the transaction process of private equity financing, allowing us to easily complete professional tasks without needing to master relevant professional knowledge and skills. Therefore, it possesses all the advantages of being online (efficiency, boundaries, cost), while technically ensuring the transaction security and performance issues of private equity financing.

This represents a new paradigm shift brought by blockchain technology to private equity financing.

Today & Future

Since the birth of The DAO in 2016, a large number of developers and builders have been working towards the vision of "Onchain Ventures," including Moloch, DAOhaus, TheLAO, Nouns, Juice Box, PartyDAO, Gnosis Auction, Superfluid, Syndicate, Furo, Kali, DAOSquare, and others. These builders, based on their understanding of Onchain Ventures, have constructed solutions in their respective focused areas. Many have given up midway, but more continue to iterate and improve these solutions.

As a founder of DAOSquare, I am also honored to be a promoter and builder of this vision. My efforts with DAOSquare are directed towards building an on-chain AngelList, providing a complete toolkit for crypto private equity financing, technically ensuring the asset security and performance issues of all parties involved in transactions, while improving investment and financing efficiency, expanding business boundaries, and reducing the financial and time costs for all parties involved.

Like all other solution builders, I believe in the importance of Onchain Ventures for crypto private equity financing and the overall development of crypto. I also believe in the future prospects of Onchain Ventures, as capital will always be a crucial driving force for industry development, whether in traditional fields or crypto. Therefore, I believe that in the near future, as the crypto private equity financing industry continues to improve and standardize, these products serving crypto investment and financing will shine brightly. Let us wait and see.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。