Original | Odaily Planet Daily (@OdailyChina)

On April 11, the new lending product Lista Lending from the BNB Chain ecosystem LSDFi project Lista DAO was launched and immediately caused a "frenzy" in the market. The first phase, valued at $10 million in BNB, was fully borrowed in less than an hour. Within just four days of its launch, Lista Lending's total deposits exceeded $189 million, and the peak borrowing amount surpassed $120 million.

The product's popularity was so great that even CZ couldn't help but retweet and comment: "Lista Dao is 🔥".

As a new generation of lending product on the BNB Chain, Lista Lending has gained widespread favor among market users, including CZ, primarily because it adopts an innovative P2P model that offers users higher deposit rates and lower borrowing rates. Odaily Planet Daily will provide a straightforward introduction to Lista Lending in this article and explain why borrowing BNB on Lista Lending is a better choice.

Lista Lending Product Introduction

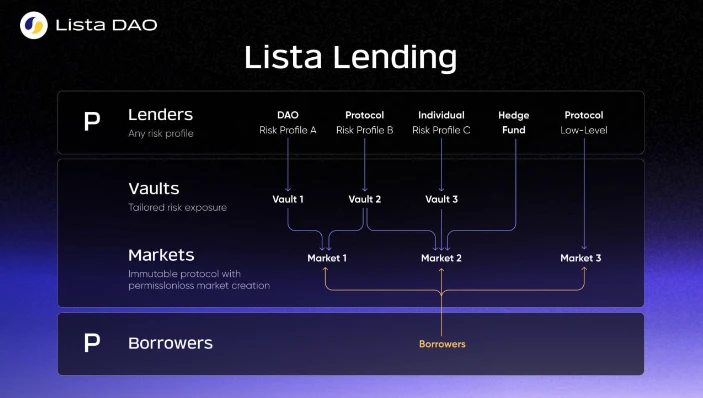

Lista Lending is a new generation decentralized lending platform launched by Lista DAO, utilizing an innovative P2P model and advanced interest algorithms to provide users with efficient financial management and lending services. The platform aims to enhance capital utilization, reduce borrowing costs, and strengthen protections for borrowers.

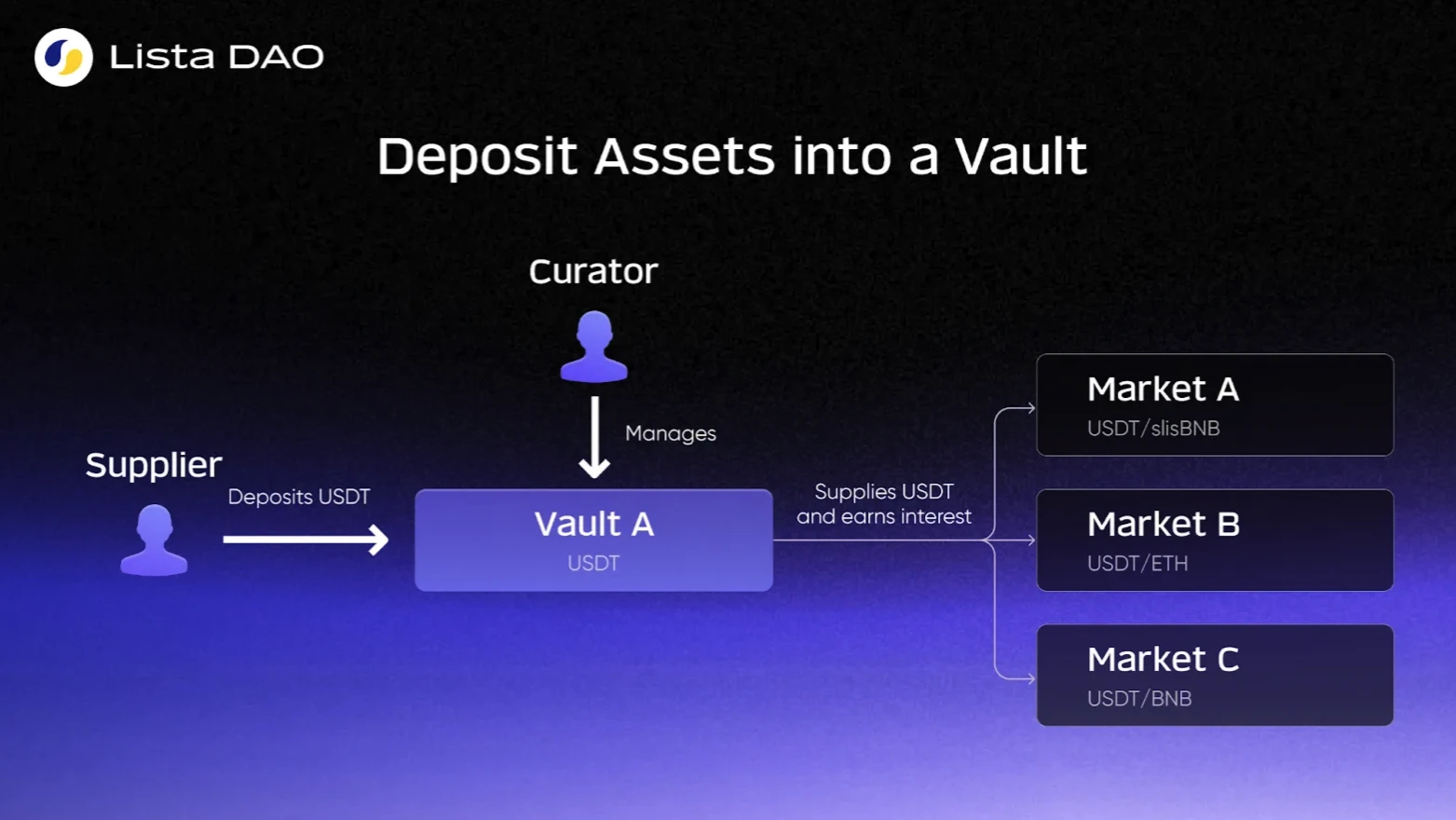

In simple terms, Lista Lending consists of multiple vaults and markets, where lenders deposit funds into vaults to earn interest, and the vaults allocate funds to different markets so that borrowers can engage in over-collateralized lending in the markets. In Lista Lending, lenders can be anyone, including individuals, protocols, DAOs, or hedge funds.

How Lista Lending Works

Currently, Lista Lending has launched the BNB vault and the USD1 vault. The BNB vault's deposits have exceeded $169 million, and users can borrow BNB by collateralizing BTCB, PT-clisBNB, and solvBTC. The USD1 vault is the first application of the Trump crypto project WLFI's stablecoin USD1 on the BNB Chain.

Here's a little knowledge nugget: some DeFi newcomers may wonder why they need to over-collateralize more funds on-chain to borrow a portion of funds, such as collateralizing more BTCB to borrow USDC worth 70 BNB. This mainly stems from users' recent demand for short-term liquidity, such as participating in Binance Launchpool or Binance wallet new listings, which are considered "sure-win trades." There is a short-term demand for BNB, and using lending to obtain BNB instead of directly purchasing it has the added benefit of avoiding profit erosion caused by short-term price fluctuations.

Is the world tired of Venus?

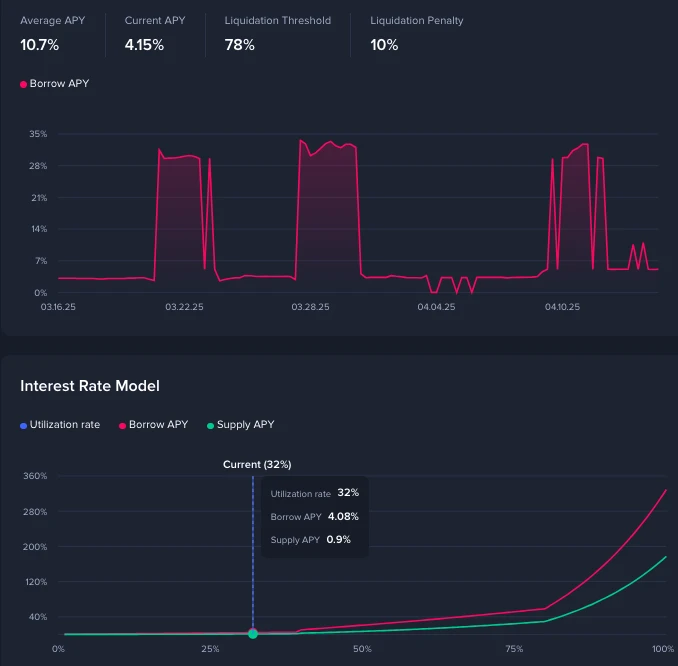

Venus is the largest lending protocol on the BNB Chain, with a TVL exceeding $1.583 billion, and is currently an important borrowing channel for users participating in Binance Launchpool and Binance wallet new listings. Although it has been growing under "Binance's feeding," Venus's lending mechanism is still not user-friendly, with a low capital utilization rate (about 32%) and an increase in borrowing rates (up to 30%) when there is high short-term demand for BNB, while deposit rates do not see a similar increase, "the money all goes into their own pockets."

Venus BNB borrowing rate changes and capital utilization rate curve

The world is tired of Venus, and users hope for new competitors to break Venus's "monopoly." This has proven to be the case; after Lista Lending launched on April 11, Venus's BNB borrowing rate plummeted to 5%. Well-known KOL Brother Lion from Australia also stated on social media that "Lista did a great thing, breaking Venus's monopoly on BNB lending over the past few years." CZ also commented in the discussion area, "The market needs competition. 😆"

Why is Lista Lending a better choice for borrowing BNB?

According to official data from Lista Lending, the current borrowing rates for BNB in different markets are as low as 0.84% and only up to 2.05%. In contrast, Venus's BNB borrowing rates range from 4% to 5%, and its rate model can spike to over 28% after exceeding a certain borrowing amount. For ordinary users, Lista Lending will be a better choice.

- P2P lending mechanism significantly reduces user costs

So, why can Lista Lending offer such low borrowing rates? This is primarily due to its innovative P2P lending mechanism.

Traditional DeFi lending protocols (like Venus) use a pool-to-pool lending model, where all liquidity is concentrated in a shared pool. The core issue of this model is the low matching of funds for lending and borrowing; the total deposit amount in the pool often far exceeds the total borrowing amount, causing the interest of deposit users to be diluted by idle funds, while borrowing users must bear the interest cost for the entire pool rather than just paying interest on the portion they actually use. The result presented to users is high borrowing rates and low deposit rates.

Lista Lending adopts a peer-to-peer lending model, allowing the funds in the vaults to be directly and effectively matched with borrowers. Through its multi-oracle system, it can implement a dynamic interest algorithm that adjusts rates in real-time based on market supply and demand. The result presented to users is lower borrowing rates, higher deposit rates, and a capital utilization rate of up to 90%.

- Freedom to create vaults and markets, enhancing lending flexibility

In the early stages of the protocol's development, Lista Lending only had the BNB vault and the USD1 vault. However, as the protocol matures, Lista Lending will open more vaults and allow users to create vaults and markets without permission. Users can create vaults and markets for any token, including assets that are not recognized by traditional DeFi platforms (like Venus) but are redeemable through smart contracts.

In contrast, traditional DeFi lending protocols typically have the platform or DAO vote to decide which lending assets or collateral to support, resulting in lower flexibility and efficiency.

- Providing stronger risk resistance for both borrowers and lenders

The core pool assets of traditional DeFi lending protocols usually share risks, and liquidation can cause a chain reaction. In Lista Lending, each vault has separate liquidation parameters, isolating risks between vaults. This user-friendly design enhances the risk resistance of both borrowers and lenders, ensuring a fairer and safer trading environment.

Lista Lending as a new growth engine for Lista DAO

Lista DAO is a DeFi project operating on the BNB Chain that combines liquid staking, CDP systems, and lending, invested by Binance (YZi Labs), and is set to launch its TGE on Binance in June 2024.

In Lista DAO, users can stake BNB to obtain liquid staking certificates slisBNB and earn POS income, while also borrowing stablecoins lisUSD by over-collateralizing native crypto assets like ETH, BNB, and liquid staking tokens like slisBNB, wstETH, and solvBTC. Additionally, if users borrow lisUSD using BNB as collateral, they can also obtain borrowing limits for clisBNB to participate in Binance Launchpool new listings.

As of now, Lista DAO has a total TVL of $1.108 billion, ranking third in the BNB Chain, only behind Venus and PancakeSwap. Among them, the collateral value exceeds $362 million, and the value of liquid staking assets is approximately $390 million.

Lista DAO is a steadfast builder on the BNB Chain, deeply engaged in BNBFi. Previously, users could only borrow the stablecoin lisUSD through Lista DAO, which not only limited the lending products available but also failed to meet users' diverse needs for BNB to participate in Binance's new listings. Additionally, the collateralized assets did not generate any returns. The emergence of Lista Lending addresses these shortcomings and has become a new growth engine for Lista DAO.

Lista Lending has already created a chemical reaction with existing Lista DAO products. In terms of token price, since the launch of Lista Lending on April 11, the price of its token LISTA has been on the rise, reaching a peak of $0.2 on April 13 after being retweeted by CZ.

At the same time, PT-clisBNB is the main collateral for Lista Lending. PT-clisBNB is the yield-bearing token of clisBNB on Pendle, with an APY of 14.86%. The introduction of Lista Lending allows users to borrow BNB while earning Pendle's annualized returns. Users can choose to participate in short-term activities like Binance's new listings or continue to engage in circular lending within Lista DAO, enhancing their DeFi yield leverage.

In summary, through the flexible lending market of Lista Lending, it is expected to synergize with Lista DAO's original products, increasing the overall TVL of the protocol and providing users with more playability, thereby revitalizing the lending ecosystem on the BNB Chain.

Lista Lending Brings BNB Chain Lending into a New Era

According to data from DeFiLlama, lending is the category with the highest TVL in DeFi, with 508 protocols engaged in lending, more than double that of the second-ranked liquid staking sector, indicating that market demand and competition remain fierce.

However, the proportion of the lending sector on the BNB Chain is relatively low. The DeFi TVL of the BNB Chain reaches $5.4 billion, with loans amounting to only $1.9 billion, accounting for about 35%, which is far below the over 50% share of lending on Ethereum.

It is undeniable that the Ethereum ecosystem, as the "big brother" of DeFi, has a more complete infrastructure in the lending field. Morpho has already improved the utilization of lending funds in the Ethereum ecosystem using a peer-to-peer lending mechanism. This visible gap needs to be addressed collectively by BNB Chain ecosystem projects. However, Venus, as the largest lending protocol on the BNB Chain, has a surprisingly low LTV (loan-to-value ratio) of only 78% for BNB, while the LTV for BTCB and ETH reaches 80%. Clearly, the liquidity of BNB on the BNB Chain is better than that of BTCB and ETH, but in terms of lending, BNB still seems "inferior." Venus, as an important lending infrastructure on the BNB Chain, should have taken proactive measures to establish an advantage for BNB, but the results have been unsatisfactory.

As the first lending product on the BNB Chain to adopt a P2P model, Lista Lending is taking on the responsibility of establishing a new generation of lending infrastructure on the BNB Chain. Not only can BNB's LTV reach up to 90%, but compared to Morpho in the Ethereum ecosystem, Lista Lending employs a multi-oracle system and upgradable smart contracts, ensuring more accurate and fair pricing while timely meeting the needs for contract upgrades.

Now, backed by low-risk opportunities like Binance Launchpool and Binance wallet new listings, the BNB Chain DeFi lending market has sufficient liquidity and a user base. Lista Lending is set to become an important catalyst, potentially ushering in a new era for BNB Chain lending.

Conclusion

In this on-chain world where liquidity is king and efficiency is life, every technological iteration and mechanism innovation can reshape the order. The birth of Lista Lending comes at a time when the BNB Chain ecosystem is gradually maturing, injecting a shot of adrenaline into the market.

It is not only a powerful challenge to traditional lending mechanisms but also brings tangible benefits and choices to users—lower borrowing rates and higher capital utilization rates. This "user-centric" design philosophy reflects the BNB Chain ecosystem's determination for self-evolution and echoes the original spirit of DeFi.

In the future, Lista Lending may not only serve as a "supply station" behind Binance's new listings but could also become the core hub of on-chain lending liquidity, supporting a more efficient, open, and fair financial order within the entire BNB Chain ecosystem.

Just as the sprouts of spring do not immediately turn into a forest, the growth of Lista Lending also requires time. However, it has already positioned itself at a promising starting point, providing a new solution for users, developers, and the entire BNB Chain DeFi ecosystem. Whether Lista Lending can shoulder this significant responsibility remains to be seen.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。