This article is from: DeFi Cheetah

Compiled by: Odaily Planet Daily (@OdailyChina)

Translator: Azuma (@azuma_eth)

Berachain has officially launched its Proof of Liquidity (PoL) mechanism today. This article aims to provide the most comprehensive analysis of PoL and its potential impact on the ecosystem, particularly on the BERA price. We will start with the basic mechanism, emission schedule, and token economic model, gradually unfolding the analysis.

The PoL mechanism of Berachain aims to address the incentive misalignment issues present in PoS blockchains. In traditional PoS mechanisms, users need to lock assets to earn staking rewards, which distorts the incentive mechanism—because DeFi projects built on these blockchains also require assets and liquidity, resulting in a situation where assets directly compete with the PoS mechanism. PoL successfully reconstructs the incentive mechanism, shifting the focus from asset locking to DeFi activities while enhancing the network's security and decentralization.

Basic Mechanism

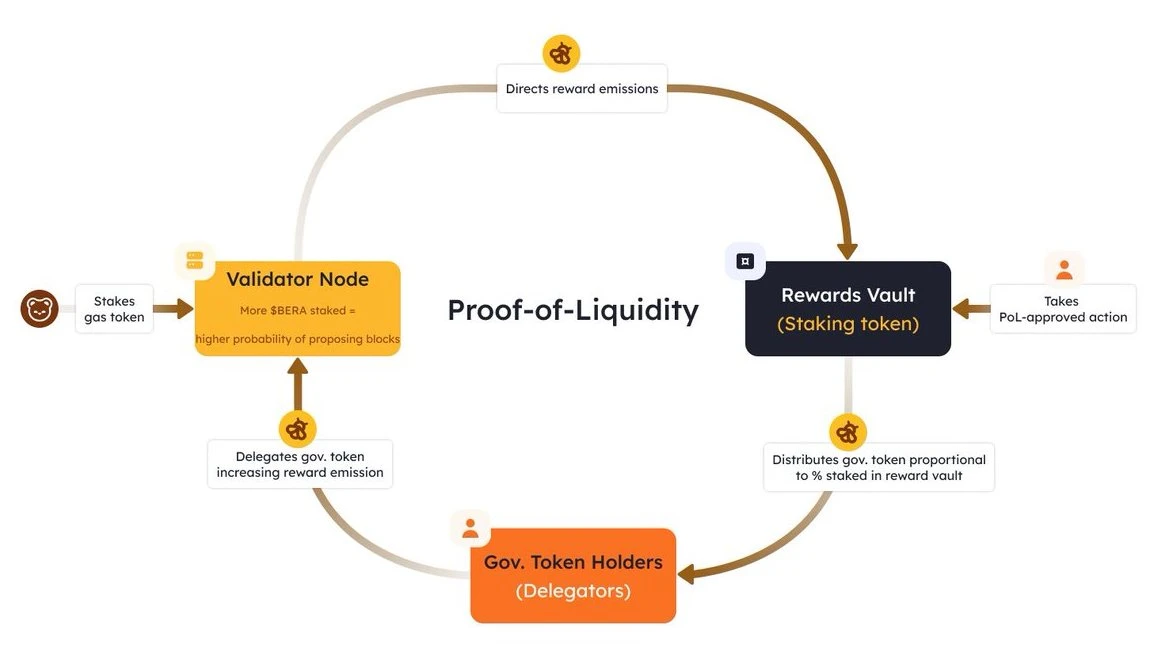

Berachain has two core native assets: BERA and BGT:

BERA is the gas token and staking token, primarily responsible for validator selection (specific mechanisms will be detailed later);

BGT is the governance token (non-transferable but can be exchanged 1:1 for BERA), with its core function being to regulate the distribution of economic incentives and determine the scale of the reward pool (Reward Vaults) allocated to whitelisted DApps.

BGT can be exchanged (or burned) 1:1 for BERA, but BERA cannot be converted back to BGT.

- Note: Whether a validator can obtain block production eligibility depends entirely on the amount of BERA they stake; the rewards a validator can earn from block production are positively correlated with the amount of BGT they hold.

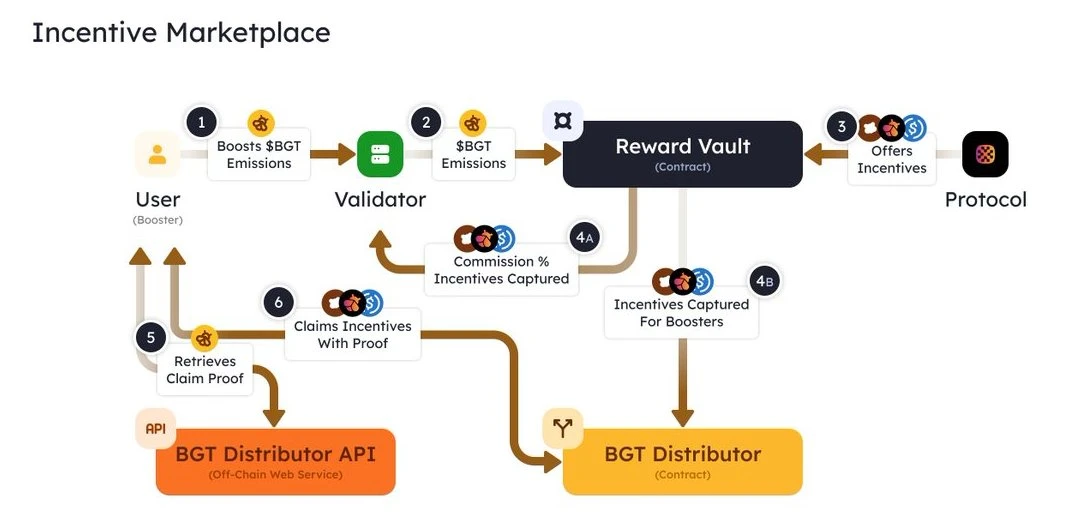

Unlike traditional PoS, in traditional PoS chains, validators can directly earn inflation rewards by executing transaction validations, while delegators can earn a portion of the total rewards based on their staking amount. In Berachain, validators can earn BGT (by receiving BGT from the BlockRewardController contract through the Distributor smart contract—the latter is the only entity that can mint BGT), but they must immediately allocate most of the BGT to the reward pools of whitelisted DApps.

In these reward pools, relevant protocols can bribe validators (for example, "1 BGT = xxx certain token") to exchange for BGT emissions. The more attractive the bribe, the more likely validators are to allocate their BGT to the DApp reward pool with the strongest incentives.

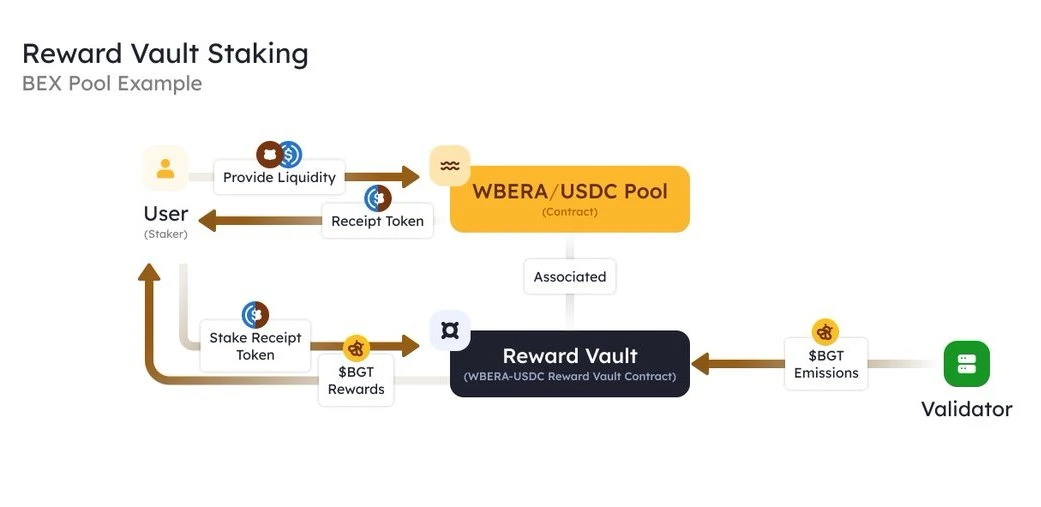

For example, users can provide liquidity to certain liquidity pools of the native DEX to earn LP fees; afterward, users can earn additional BGT release rewards by depositing LP tokens into the reward pool of that specific trading pair on the DEX, on top of the LP fees; after receiving BGT rewards, users can choose to delegate these BGT to validators or directly stake BGT—it's worth noting that the amount of BGT released to validators will increase as the amount of BGT delegated to them by users grows.

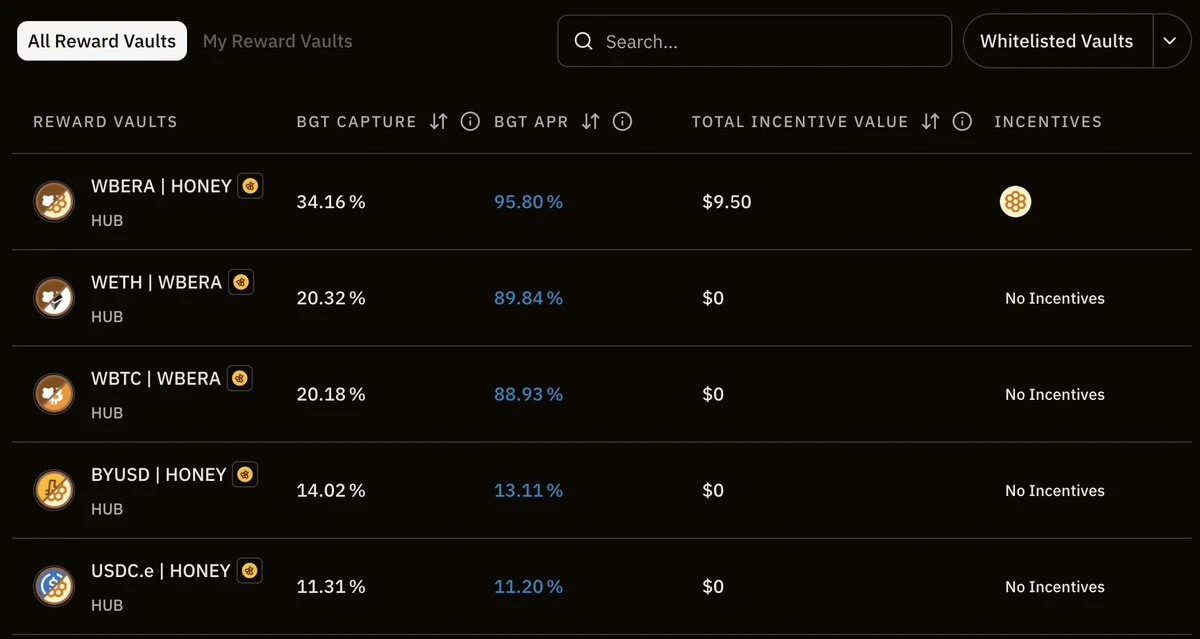

Note: With the official launch of the PoL mechanism, more whitelisted reward pools are now open (see official announcement).

Regarding BGT allocation, validators can actively or passively decide which reward pools to allocate their BGT to based on the bribe amounts provided by DApps. Users as delegators can choose validators that align more with their interests based on the validators' strategies and the expected bribe earnings for delegators—therefore, validators that can bring the most value to delegators may receive more BGT delegation.

As for BERA staking, stakers will proportionally share the BGT and BERA earnings obtained by the validator node by increasing their own staking amount in the validator node.

Block Production and BGT Emission

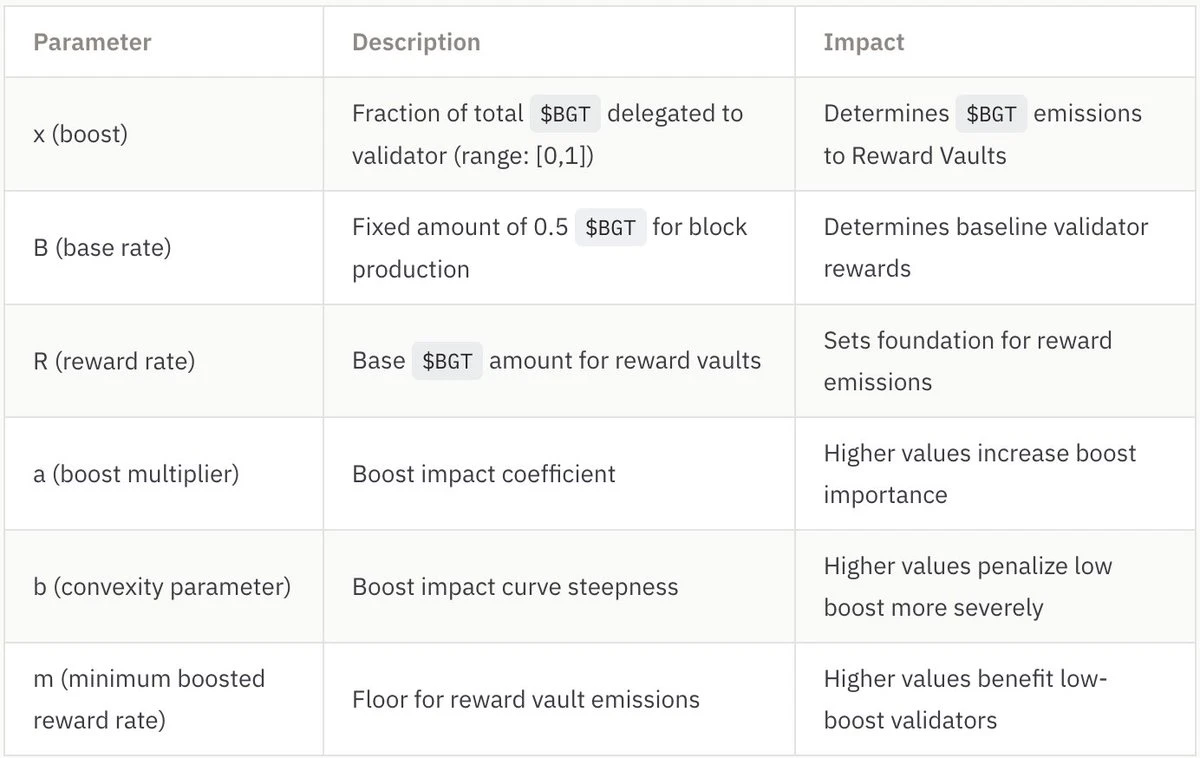

Validator selection criteria: Only the top 69 validators ranked by BERA staking amount are eligible for block production (minimum 250,000 BERA, maximum 10,000,000 BERA). The probability of proposing a block is proportional to the amount of staked BERA, but this does not affect the emission amount allocated to the reward pools.

BGT emission per block: This part is very important, and the specific emission amount depends on how the formula is designed.

BGT emissions are divided into two parts: Base Emission and Reward Vault Emission. Base Emission is always a fixed amount (currently 0.5 BGT), directly paid to the validators producing the block; Reward Vault Emission largely depends on the "boost" factor, which is the proportion of BGT delegated to the validator relative to the total BGT delegated in the network. Parameters a and b will both affect the role of the "boost" factor on the final reward pool emission, meaning that the larger the values of a and b, the greater the impact of the "boost" factor on reward pool emissions. In other words, the reward pool emission amount is proportional to the weights configured in the validator reward distribution formula.

In other words, the more BERA staked, the higher the probability that the validator will be selected to produce the next block; the more delegated BGT, the more BGT the validator can mint from the BlockRewardController smart contract, and the more BGT can be allocated to different reward pools, leading to more bribery incentives obtained by the validator from the protocol.

To summarize, the top 69 validators ranked by BERA staking amount are eligible for block production. They can direct the BGT emissions to specific reward pools in exchange for a certain proportion of bribery incentives, while the remaining bribery incentives will be allocated to delegators. The BGT in the reward pools will then be distributed to users providing liquidity for the corresponding pools. Once these users receive non-transferable BGT, they can choose to delegate it to validators and act as delegators, enjoying bribery earnings from other protocols, or irreversibly exchange it for BERA to cash out.

PoL Launch Scale Analysis

During the Berapalooza 2 event, over $500,000 in bribes was committed within the first 24 hours of the RFRV proposal submission. If this momentum continues and doubles before the official launch of PoL, we may see a bribery scale of $1 million per week—huge incentive funds are flowing into the Berachain ecosystem.

At the same time, Berachain emits 54.52 million BGT annually (approximately 1.05 million BGT per week). Since 1 BGT can be destroyed in exchange for 1 BERA, and the current trading price of BERA is $8.43 (note: price at the time of the original author's writing), this means that Berachain can allocate incentives worth $8.8 million weekly. Of this, only 16% of the emissions go directly to validator nodes, while the remaining $7.4 million will be allocated to reward pools—therefore, if the protocol pays only $1 million in bribes weekly, it could potentially receive $7.4 million in BGT incentives, resulting in an extremely attractive return on investment.

Bribery Mechanism Enhances Capital Efficiency

For the protocol, this system is disruptive. Instead of spending huge amounts to attract liquidity, it is better to improve incentive efficiency through this bribery model.

For users, this means that there will be extremely high annualized returns in the early stages of PoL launch. As protocols compete to attract liquidity, they will offer higher BGT rewards, creating excellent mining opportunities. If you want to maximize your returns, now is the time to prepare, calculate precisely, and get ready for the wave of incentives brought by Berachain PoL.

Flywheel Effect

The positive feedback loop mechanism of Berachain is as follows:

The more BGT users delegate; the more BGT incentives available to guide liquidity for trading pairs; the more liquidity the pools attract; the lower the slippage due to increased liquidity, leading to greater trading volume facilitated by the pools; the higher the fees, which in turn attract more BGT emissions directed to the corresponding pools.

This mechanism can form a self-reinforcing closed loop:

Increased liquidity → Users earn more rewards;

Increased BGT delegation → Validators receive more incentives;

Enhanced validator incentives → Improved network security and synchronized growth with DeFi.

PoL creates a "positive-sum economy." Unlike traditional staking, PoL can sustainably expand Berachain's economic activities while enhancing capital efficiency:

Users provide liquidity → Earn BGT → Delegate to validators;

Validators guide emissions → Incentivize DeFi protocol development;

Increased liquidity → Attract more users → Generate more rewards → Cycle continues…

Why is this important?

Because the enhancement of liquidity means improved trading conditions, reduced slippage, and expanded borrowing scales, while developers are often more inclined to build applications on blockchains with stable liquidity growth. Under this flywheel model, as more liquidity enters the ecosystem, it will attract more users, developers, and funds, thereby enhancing the long-term sustainability and security of the network.

The Token Economic Magic of Berachain

No matter how the team packages it, the core design of the token economic model ultimately boils down to one point—maximizing the reduction of selling pressure and smoothing the launch process.

This can be analyzed from two dimensions:

Sources of inflation: Only a portion of BGT can be exchanged for BERA (only "partially," as it will receive incentive tokens from other protocols in the Bera ecosystem as subsidies).

Deflationary mechanism: Staking BERA grants block production eligibility and increases block production probability; delegating BGT to validators can yield more rewards; the irreversible nature of BGT exchanges creates a certain deterrent (especially considering that BGT cannot be obtained from the secondary market); higher trading volumes generate more fees (benefiting from the liquidity growth expectations brought by PoL).

In traditional PoS staking scenarios, the choice and gains of validators are determined by the amount of native tokens staked and the total amount of all staked tokens. Berachain has a clever design here: by separating functions such as gas and staking from governance and economic incentives, it allocates the function used to guide economic incentives to a token with lower liquidity, thereby raising the threshold for obtaining economic incentives (i.e., people cannot directly purchase it on the secondary market), to prevent holders from selling off in large quantities.

This is similar to Curve's veCRV governance model, but Berachain goes a step further—veCRV can be converted from CRV, which can be purchased on the secondary market, while BGT cannot be purchased on the secondary market nor converted from BERA. This creates a greater deterrent effect for BGT holders; if they exchange a large amount of BGT for BERA and sell it, they will face a high barrier to re-obtain ecosystem project incentives—they can only acquire them by providing liquidity for certain whitelisted reward pools.

Additionally, the dual-token PoS model is worth mentioning: validators must stake BERA, but this only means they are eligible for block production, so they need to stake more BERA to increase the probability of producing the next block. At the same time, validators must earn more incentive tokens from the protocol for BGT delegators to attract more BGT delegation. This dynamic mechanism can create powerful deflationary forces to absorb the significant selling pressure caused by the initially high BGT inflation. This is because validators need to stake more BERA to achieve a higher block production probability, while users need to hold and delegate BGT to earn high returns.

One fatal risk I can currently think of is that if the intrinsic value of BERA exceeds the returns from BGT, BGT holders may queue up to exchange and sell BERA. The realization of this risk depends on a game dynamic where BGT holders need to assess whether the profit from holding BGT for returns is greater than the profit from directly exchanging and selling BERA. This depends on how prosperous the Bera DeFi ecosystem can develop— the more competitive the incentive market, the higher the returns for BGT delegators.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。