Every participant in CAP (Minters, Operators, and Restakers) unlocks new earning opportunities by contributing value.

Author: DeFi Dave

Compiled by: Deep Tide TechFlow

The rise of the online platform economy has helped many small startups grow into today's tech giants, all based on a seemingly counterintuitive phenomenon: they do not own any assets required for their core business. The classic examples are that Uber does not own any vehicles in its fleet, and Airbnb does not own any rooms on its platform. These companies leverage the power of the market to precisely match service seekers with providers, whether for short trips in the city or temporary accommodations. Compared to traditional businesses that need to handle complex logistics like vehicle maintenance and licensing approvals, these platforms can focus on optimizing technology, enhancing user experience, and improving efficiency, thus achieving limitless business expansion.

A similar dynamic exists in the on-chain world. **On one side are users seeking returns, and on the other are protocols and participants providing returns, which promote high *annual percentage yields (APY)* through various strategies. However, whether through leveraging collateralized debt positions (CDPs), interest from Treasury bills (T-Bills), or market strategies like basis trading, a single strategy will encounter bottlenecks when achieving large-scale delivery.

The Story of Two (Limited) Designs

Traditional projects often rely on endogenous designs, with their returns stemming from platform usage demand. For example, lending markets and perpetual contracts depend on users' willingness to leverage, while the token flywheel effect requires new investors to continuously purchase governance tokens. However, if the platform lacks demand (whether for leverage or token purchases), liquidity supply will not yield returns. This design is similar to Ouroboros, unable to transcend itself to achieve sustainability.

For newer exogenous strategies, protocols often pose the wrong question: which strategy can achieve maximum scalability? In fact, no strategy can scale infinitely. When alpha is exhausted, all strategies will eventually become outdated, forcing developers to return to the design phase.

So, what should stablecoins focus on? As the core hub of capital formation, stablecoins need to consider how to efficiently allocate capital and ensure the safety of users' funds. To achieve true success, the blockchain ecosystem requires a flexible and secure stablecoin solution.

Entering CAP

CAP is the first stablecoin protocol that programmatically outsources yield generation while providing comprehensive safeguards.

Who Makes Up CAP?

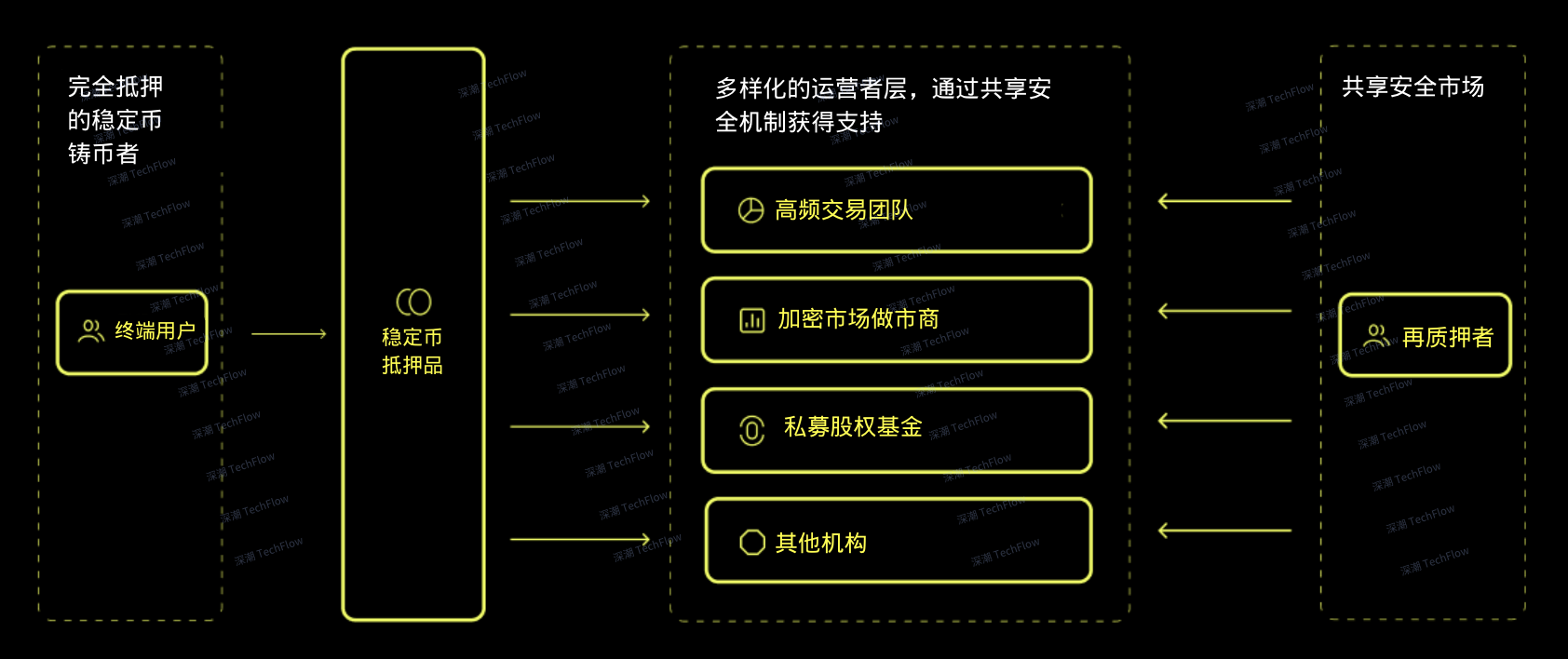

The core of the CAP system consists of three types of participants: Minters, Operators, and Restakers.

Minters: Minters are stablecoin users holding cUSD. cUSD can always be exchanged at a 1:1 ratio for its underlying collateral assets, USDC or USDT.

Operators: Operators are institutions capable of executing large-scale yield generation strategies, including banks, high-frequency trading (HFT) firms, private equity firms, real-world asset protocols (RWA protocols), decentralized finance protocols (DeFi protocols), and liquidity funds.

Restakers: Restakers are capital pools that lock up funds, providing security for stablecoin users by backing the activities of operators, and thus gain the right to use their restaked ETH.

(Original image from DeFi Dave, compiled by Deep Tide TechFlow)

How CAP Works

CAP's smart contracts clearly define the operational rules for all participants, including fixed requirements, penalty mechanisms, and reward mechanisms.

Stablecoin users deposit USDC or USDT to mint cUSD at a 1:1 ratio. Users can choose to stake cUSD to earn yields or use it directly as a stablecoin pegged to the US dollar. cUSD can always be fully redeemed.

An institution (e.g., a high-frequency trading firm with a 40% threshold yield) chooses to join the CAP operator pool and plans to obtain loans through CAP for its yield strategies.

To become an operator, the institution must first pass CAP's whitelist review and persuade restakers to delegate funds to them. The total amount of delegated funds determines the capital limit the operator can access. Once the institution obtains sufficient "coverage" through delegation, it can withdraw USDC from the collateral pool to execute its exclusive strategy.

At the end of the loan period, the institution allocates returns to stablecoin users based on CAP's benchmark yield while paying a premium to restakers. For example, if the benchmark yield is 13% and the premium is 2%, the institution can retain the remaining yield (in this case, 25%).

Users who stake cUSD accumulate interest through the activities of operators, which can be withdrawn at any time.

Motivations of Each Participant

To understand how CAP operates, it is not enough to know the behaviors of participants; it is more important to understand their motivations for participating.

Stablecoin Holders

Stable returns without frequent switching: CAP's market-set interest rates allow users to earn returns continuously without frequently changing protocols, even if market conditions change or protocols become outdated.

Security assurance: Compared to CeFi and DeFi applications that promise high returns but lead to user fund losses, CAP offers higher security. Users' principal is protected by the immutability of smart contracts and sufficient collateral, rather than relying on trust.

Operators

- Zero-cost access to additional capital: The capital provided by CAP does not require a cost basis, allowing yield market makers to achieve higher returns compared to traditional LP models, while increasing the total value locked (TVL) in DeFi protocols, the assets under management (AUM) of private credit funds, and creating more opportunities for cross-domain arbitrage.

Restakers

New uses for locked ETH: Since ETH is often locked on L1, its use cases are limited. By restaking ETH, users can delegate it to operators, thus participating in active validation services (AVS) like CAP.

Yield paid in blue-chip assets: CAP allows restakers to independently determine premiums to compensate for the risks they undertake. These premiums are paid in blue-chip assets like ETH or USD, rather than inflationary governance tokens or off-chain point programs. Therefore, the earnings of restakers are not limited by project market caps and have unlimited growth potential.

Existing Risks

Any new opportunity comes with risks, so it is particularly important to understand the potential risks of CAP:

Risks of shared security markets: CAP is based on shared security markets like EigenLayer, and thus may be affected by the risks of these platforms.

Price volatility of underlying assets: If USDC or USDT depegs, users will face the risk of price volatility. However, this risk exists even without CAP.

Risks of third-party cross-chain bridges: When users use cUSD on other chains through cross-chain bridges, they may face risks associated with third-party bridging. However, CAP itself is not directly exposed to these risks.

Smart contract risks: CAP does not rely on custodians or human oversight but protects users through the rules of smart contracts. However, users must bear the risks that may exist in the logic of smart contracts, even if the code has been audited.

Conclusion

Every participant in CAP (Minters, Operators, and Restakers) unlocks new earning opportunities by contributing value: depositors gain guaranteed stable returns, operators access capital at zero cost, and restakers earn high-quality asset returns through delegation.

To achieve large-scale adoption of yield-bearing stablecoins, we need to rely on the power of efficient markets, rather than centralized teams. Just like markets in other industries, competitive mechanisms bring the best outcomes for all participants.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。