Author: 0xCousin

In the history of Wall Street, there has never been a shortage of legendary stories, but the strategic transformation journey of MicroStrategy's Bitcoin Treasury Company is destined to become a unique new legend.

A Bitcoin Strategy That Captivated Global Attention

In 2020, the COVID-19 pandemic triggered a global liquidity crisis, prompting countries to adopt loose monetary policies to stimulate the economy, which led to currency devaluation and increased inflation risks.

During the pandemic, Michael Saylor reassessed the value of Bitcoin. He believed that when the money supply grows at a rate of 15% per year, people need a hedge asset that is not tied to fiat cash flows. Therefore, he chose a Bitcoin strategy for MicroStrategy.

Compared to BTC ETFs or other Spot Bitcoin ETPs launched by companies like BlackRock, MicroStrategy's Bitcoin strategy is more aggressive. It uses the company's idle funds, issues convertible bonds, and increases share issuance to purchase Bitcoin, allowing the company to gain potential profits from Bitcoin's rise while also bearing the potential risks of Bitcoin's decline, whereas ETFs/ETPs focus more on price tracking.

MicroStrategy's Funding Sources and Bitcoin Purchase Journey

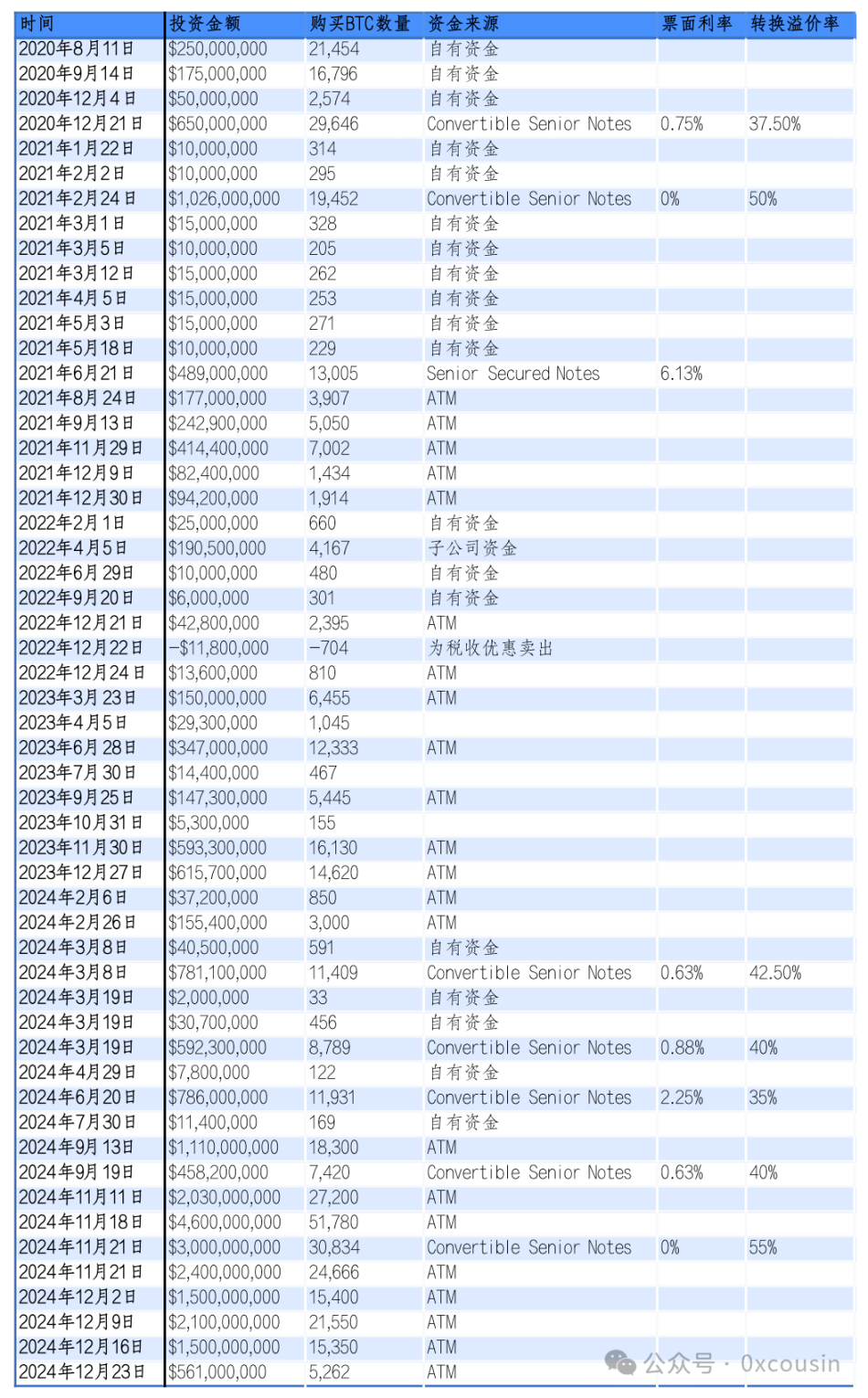

MicroStrategy primarily raised funds to purchase Bitcoin through four methods.

1. Using Own Funds for Purchases

In the initial three investments, MicroStrategy used its idle funds for purchases. In August 2020, MicroStrategy spent $250 million to buy 21,400 Bitcoins; in September, it invested $175 million to purchase 16,796 Bitcoins; and in December, it invested $50 million to buy 2,574 Bitcoins.

2. Issuing Convertible Senior Notes

To purchase more Bitcoin, MicroStrategy began to finance its purchases by issuing convertible bonds.

Convertible senior notes are a financial instrument that allows investors to convert the bonds into company stock under specific conditions. These bonds typically have low or even zero interest rates, with a conversion price set above the current stock price. Investors are willing to buy such bonds mainly because they provide downside protection (i.e., the principal and interest can be recovered at maturity) and potential gains when the stock price rises. The interest rates on several convertible bonds issued by MicroStrategy mostly range from 0% to 0.75%, indicating that investors are confident in the rise of MSTR's stock price, hoping to convert the bonds into stock for greater returns.

3. Issuing Senior Secured Notes

In addition to convertible senior notes, MicroStrategy also issued a $489 million senior secured note with a 6.125% interest rate maturing in 2028.

Senior secured notes are a type of secured bond with lower risk than convertible senior notes, but these bonds only offer fixed interest income. MicroStrategy has chosen to repay this batch of senior secured notes early.

4. At-the-Market Equity Offerings

As MicroStrategy's Bitcoin strategy began to show results, MSTR's stock price continued to rise, prompting MicroStrategy to adopt more at-the-market equity offerings for financing. This method carries lower risk because it is not debt, has no repayment pressure, and does not have a foreseeable repayment date.

MicroStrategy has signed public market sales agreements with agents such as Jefferies, Cowen and Company LLC, and BTIG LLC. According to these agreements, MicroStrategy can periodically issue and sell Class A common stock through these agents. This is known in the industry as ATM.

At-the-market equity offerings are more flexible, allowing MicroStrategy to choose the timing of selling new shares based on secondary market conditions. Although issuing stock dilutes existing shareholders' equity, the correlation with Bitcoin prices and the increase in the amount of Bitcoin per share of MSTR lead to a complex market reaction, resulting in a higher overall volatility in MSTR's stock price.

The journey of MicroStrategy purchasing Bitcoin through the above four methods is as follows:

Produced by: IOBC Capital

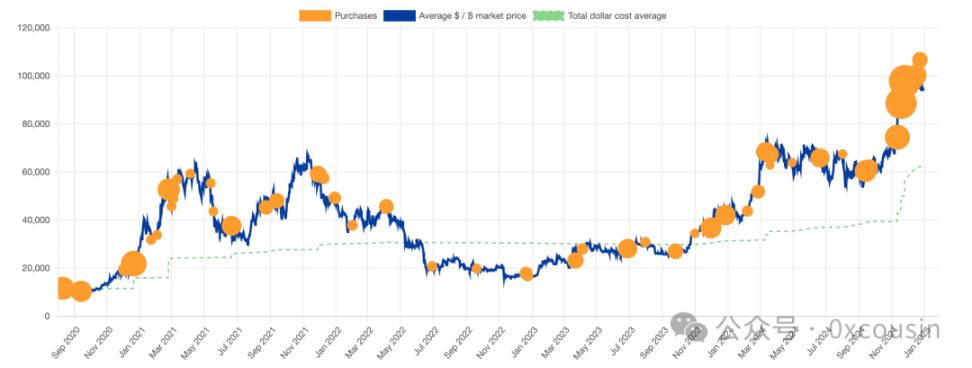

Corresponding to the BTC price chart, MicroStrategy's specific purchase history is shown in the following image:

Source: bitcointreasuries.net

As of December 30, 2024, MicroStrategy has invested approximately $27.7 billion, purchasing 444,262 Bitcoins at an average holding price of $62,257 per coin.

Key Questions About MicroStrategy's "Intelligent Leverage" Bitcoin Purchase Strategy

There is considerable debate in the market regarding MicroStrategy's "Intelligent Leverage" strategy for purchasing Bitcoin. Here are my thoughts on several key questions that are hotly discussed in the market:

1. Is MSTR's Leverage Risk High?

To conclude, it is not very high.

According to information disclosed during MSTR's Q3 2024 earnings call, MSTR's total assets were approximately $8.344 billion, with the carrying value of Bitcoin in this earnings report being only $6.85 billion (at that time, it held only 252,220 coins, calculated at a price of $27,160). Total debt was approximately $4.57 billion, resulting in a debt-to-equity ratio of 1.21.

We will not discuss accounting standards here, but only consider the data at the time of actual sale, which reflects the latest market price. If we calculate using the latest market price of Bitcoin as of September 30, 2024 ($63,560), the actual market value of the Bitcoin held by MSTR would be $16.03 billion, resulting in a debt-to-equity ratio of only 0.35.

Now, let's look at the data as of December 30, 2024.

As of December 30, 2024, MicroStrategy's total outstanding liabilities were $7.27385 billion, as follows:

Produced by: IOBC Capital

As of December 30, 2024, MicroStrategy held 444,262 Bitcoins valued at $42.25 billion. If MicroStrategy's other assets remain unchanged (i.e., $1.49 billion), then MSTR's total assets would be $43.74 billion, with liabilities of $7.27385 billion, resulting in a debt-to-equity ratio of only 0.208.

Let's compare this with the debt-to-equity ratios of leading publicly listed companies in the U.S.—Alphabet 0.05, Twitter 0.7, Meta 0.1, The Goldman Sachs Group 2.5, JPMorgan Chase & Co. 1.5.

MicroStrategy is a company transitioning from the software industry to the financial industry, and this debt-to-equity ratio is still healthy.

2. Under What Circumstances Could These Convertible Bonds Become an Unbearable Burden in the Future?

To conclude, if MicroStrategy does not continue to issue convertible bonds in the future, then Bitcoin would need to fall below $16,364 for the value of the 444,262 Bitcoins held by MicroStrategy to be less than the total amount of its convertible bonds of $7.27 billion. If MicroStrategy only uses ATM financing and idle funds to buy Bitcoin in the future, as the number of Bitcoins held by MicroStrategy increases, this "insolvency" price line could become even lower.

If MicroStrategy continues to issue convertible bonds to purchase Bitcoin at high prices and Bitcoin enters a bear market, a decline in Bitcoin prices could lead to the value of the Bitcoins held by MicroStrategy falling below the total amount of its convertible bonds, which would also cause MSTR's stock price to languish, thereby affecting its refinancing ability and debt repayment capacity, making the convertible bonds an unbearable burden.

MicroStrategy's convertible bonds allow bondholders to convert their bonds into MSTR stock, divided into two phases: Phase One—if the trading price of the bonds falls by more than 2%, creditors can exercise their rights to convert the bonds into MSTR shares and sell them to recover their investment; if the trading price of the bonds is stable or even rises, creditors can sell the bonds in the secondary market to recover their investment. Phase Two—when the bonds are nearing maturity, the 2% rule no longer applies, and bondholders can either take cash and walk away or directly convert the bonds into MSTR stock.

Since the convertible bonds issued by MicroStrategy are low-interest or even zero-interest bonds, it is clear that what creditors actually want is the conversion premium. If, at the repayment date, MSTR's stock price has increased compared to the price at the time of financing, creditors are more likely to consider converting to stock. If MSTR's stock price has decreased compared to the price at the time of financing, creditors will consider wanting the principal and interest.

If creditors do not choose to convert to MSTR stock and repayment to creditors is ultimately required, MicroStrategy has several options:

- Continue issuing new shares to raise funds for repayment;

- Continue issuing new debt to pay off old debt; (this has already been done in September 2024)

- Sell some Bitcoin to make repayments.

Therefore, at present, the likelihood of MicroStrategy falling into an "insolvency" situation is low.

3. Why Are Investors Starting to Care About MSTR's Bitcoin Per Share?

To conclude, the Bitcoin per share will determine MSTR's net asset value per share.

Whether issuing convertible bonds or using ATM, both methods achieve financing through equity dilution. The purpose of financing is to increase Bitcoin reserves. For MSTR's shareholders, equity dilution is a negative factor, traditionally seen as a bad thing. The story that MicroStrategy's management tells MSTR shareholders is—BTC Yield KPI.

Essentially, it is stated that as long as MSTR's market value is higher than the total value of the BTC it holds, there is a market value premium. Therefore, diluting MSTR's equity to buy BTC can increase the Bitcoin per share of MSTR. An increase in MSTR's Bitcoin per share means that MSTR's net asset value per share is growing, making it worthwhile for shareholders to dilute equity to finance Bitcoin purchases.

Currently, MicroStrategy holds 444,262 BTC, with a total holding value of approximately $42.256 billion. With MSTR's current market capitalization at $80.37 billion, MSTR's market value is 1.902 times the value of its Bitcoin holdings, indicating a current premium rate of 90.2%. MSTR's total share capital is 244 million shares, with each share corresponding to approximately 0.0018 BTC.

This is the core of the so-called "intelligent leverage," transforming the difference between the company's market value and the market value of Bitcoin holdings into a capital operation advantage.

4. Why Has MicroStrategy Been More Aggressive in Buying Bitcoin in the Last Two Months?

To conclude, it may be because MSTR's stock price is very high.

MicroStrategy has significantly increased the scale of its financing to buy Bitcoin in the last two months. In November and December 2024, MicroStrategy invested a total of $17.69 billion (accounting for 63.8% of the total investment) through ATM and issuing convertible bonds, purchasing 192,042 Bitcoins (accounting for 43.2% of the total purchase). Of this, only $3 billion was from convertible bonds, while the remaining $14.69 billion was financed through ATM.

Overall, the entire process of MicroStrategy's strategic allocation of Bitcoin has characteristics of regular investment over time; however, in terms of quantity and amount, it seems to be more aggressive in buying during a bull market than in a bear market.

I cannot fully understand this characteristic and can only boldly speculate that it may be because MSTR's stock price has increased more during the bull market. In August 2024, after a stock split, MSTR's stock price tripled, and the stock price increased more than fourfold over the year, while Bitcoin's increase this year was only 2.2 times.

MicroStrategy's CEO mentioned a beautiful "42B Plan" during the Q3 2024 earnings call.

British author Douglas Adams mentioned in "The Hitchhiker's Guide to the Galaxy" that the supercomputer "Deep Thought" provided the answer to "the ultimate question of life, the universe, and everything" as 42.

MicroStrategy believes this is a magical number, thus proposing the 42B financing plan. The number 21 is also magical, as the maximum total supply of Bitcoin is 21M. Therefore, MicroStrategy plans to issue $21 billion in ATM + $21 billion in Fixed Income over the next three years to continue increasing its Bitcoin holdings.

Assuming MicroStrategy ultimately raises $42 billion through issuing new shares, and assuming a share price of $330 for the new issuance, the total share capital would become 371.3 million shares. If MicroStrategy buys Bitcoin at an average price of $100,000, the company could increase its holdings by 420,000 Bitcoins, bringing MicroStrategy's total holdings to 864,262 Bitcoins. At that time, the Bitcoin per share would increase to 0.00233, representing a growth of approximately 29.4%. At this point, MSTR's total market value would be $122.53 billion, and the total value of the BTC holdings would be $86.4 billion. In this case, the market value premium would still exist.

5. After MicroStrategy, What Other Catalysts Are There for Bitcoin's Price Increase?

To conclude, aside from publicly listed companies influenced by MicroStrategy to buy Bitcoin, the only other thought is more national strategic reserves, but I do not hold high expectations for this bull market.

The current cycle of Bitcoin's price increase is mainly driven by the following major buyers:

1. Long Term Holders with Strong Consensus on Bitcoin

The long-term rise of Bitcoin does not require justification; it is as natural to BTCers as monkeys climbing trees and mice digging holes, because it is digital gold.

After Bitcoin fell below $16,000, the most mainstream Antminer S17 series miners were at shutdown price levels. Other miners like the Shenua M30S, Hippo H2, and Antminer T19 had also fallen into shutdown price ranges. Even if nothing happens, a rebound in this price range will occur. The transition from bull to bear is like a basketball falling freely from a height; after hitting the ground, it will bounce back multiple times with decreasing intensity.

Source: glassnode

As seen in the above chart, by the end of 2022, Long Term Holders were continuously increasing their positions.

After more than a decade of development, Bitcoin's consensus has become strong enough, with on-site investors and Long Term Holders sharing a consensus near the shutdown price of mainstream miners.

2. ETFs Bringing Incremental Funds from Traditional Financial Markets

Since the introduction of BTC ETFs, a total of 528,600 BTC has flowed in, bringing nearly $36 billion in incremental buying power to Bitcoin during this bull market, and $2.6 billion to ETH.

Source: coinglass.com

Additionally, the approval of BTC ETFs (and ETH ETFs) will create a ripple effect, leading more traditional financial institutions to pay attention to and invest in the crypto space.

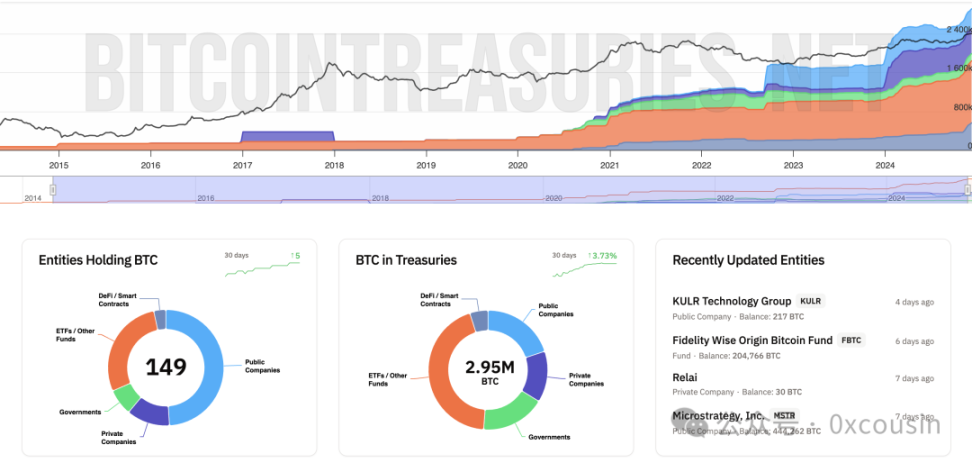

3. MicroStrategy's Continued Purchases, Imitated by Several Public Companies, Davis Double-Click

According to data from Bitcointreasuries, as of December 30, 2024, there are 149 entities holding a total of over 2.95 million Bitcoins. This number has been rapidly increasing recently.

Source: bitcointreasuries.net

Among these entities holding Bitcoin, 73 are public companies, 18 are private companies, 11 are countries, 42 are ETFs or funds, and 5 are DeFi protocols.

MicroStrategy is the first public company to adopt the "Bitcoin Treasury Company" strategy, but it is not the only one. Companies like Marathon Digital Holdings, Riot Platforms, and Boyaa Interactive International Limited have also implemented this strategy, but MicroStrategy's influence remains the largest.

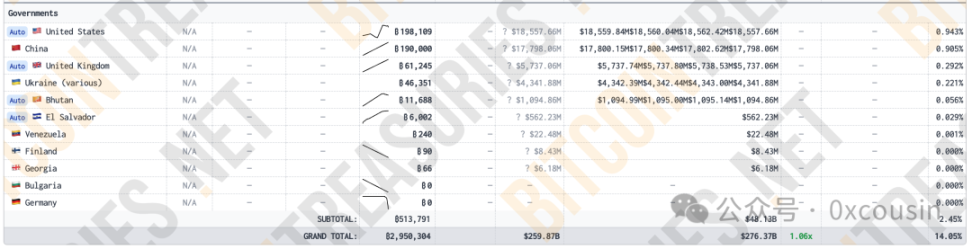

4. National Strategic Reserves

Some governments currently hold Bitcoin. The specific details are shown in the following image:

Source: bitcointreasuries.net

Although these countries hold Bitcoin, most of it was seized by law enforcement during enforcement actions. They have not sold it temporarily, so they do not qualify as stable holders.

Among these countries, only El Salvador is likely a true BTC holder. El Salvador has been buying Bitcoin since 2021, purchasing 1 Bitcoin daily, and currently holds 6,002 BTC, valued at over $560 million.

Additionally, Bhutan holds 11,688 BTC through Bitcoin mining. However, Bhutan does not qualify as a BTC holder, as it has reduced its holdings in the last two months.

During his campaign, U.S. President Trump stated that if elected, he would establish a Bitcoin strategic reserve.

If there is anything that could further drive Bitcoin's price increase after MicroStrategy, it would be Trump's administration promoting a Bitcoin strategic reserve for the U.S. government, which could lead to more countries establishing strategic reserves of Bitcoin.

Conclusion

MicroStrategy's Bitcoin strategy is not just a corporate transformation experiment; it is also a significant innovation in financial history. Through sophisticated capital operations, intelligent leverage, and profound insights into Bitcoin's value, it has not only achieved remarkable growth in its market value but has also brought Bitcoin more deeply into the view of traditional finance, breaking down barriers between crypto assets and mainstream capital markets.

MicroStrategy's bold attempt may just be the prelude to the Bitcoin legend, a small step in the true rise of Bitcoin, yet it could represent a significant leap into a new financial era.

References:

https://www.hope.com/for-corporations

https://bitcointreasuries.net/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。