How to Hold Quality Assets Long-Term and Adjust Mindset After Selling?

Editor: Wu Says Blockchain

This issue features an AMA hosted by E2M Research on Twitter Space, with guests including Shen Yu (Twitter @bitfish1), Odyssey (Twitter @OdysseyETH), Zhen Dong (Twitter @zhendong2020), and Peicai Li (Twitter @pcfli). This AMA delves into two key questions in the Web3 cryptocurrency space: how to hold quality assets long-term and how to adjust mindset and re-invest after selling.

The guests shared various operational methods and strategies based on real cases: allocating assets through the "Four Wallet" rule to avoid emotional decision-making; using a staggered buying and cold wallet locking strategy for core assets (like Bitcoin and Ethereum) to ensure long-term holding. Additionally, for experimental assets (like NFTs), a small observation position strategy is employed to explore market potential. They also shared psychological strategies for coping with market volatility, such as establishing rules to limit irrational behavior and being bold in adjusting strategies during price corrections. These practical experiences provide investors with a rational framework and long-term strategy support to face the volatility of the cryptocurrency market.

Please note: The views of the guests do not represent Wu Says' views, and Wu Says does not endorse any products or tokens. Readers are advised to strictly comply with local laws and regulations.

The audio recording was generated by GPT, so there may be some errors. Please listen to the complete podcast:

Xiaoyuzhou:

https://www.xiaoyuzhoufm.com/episodes/673a2ca943dc3a43875e8b0d

YouTube:

https://youtu.be/yRk-5d85eHU

Definition of Good Assets, Emotional Management, and the "Four Wallet" Rule

E2M: Hello everyone, welcome to our E2M Research AMA this Friday. Today's AMA topic is how to hold good assets long-term and how to re-invest after selling. Before we start, we want to emphasize the risks, as the recent market trend has been very positive, but during such times, we hope everyone can maintain a calm mindset and avoid FOMO. So, we want to stress that the content of the program is for sharing only and does not constitute any investment advice.

Today, we are pleased to invite Shen Yu as a special guest to discuss this topic with us. I believe both Peicai and Shen Yu will have many stories to share regarding how to hold good assets long-term and how to re-establish positions after selling. We look forward to hearing their insights based on their industry experiences.

Today's topic is quite interesting. A few days ago, Shen Yu seemed to have posted on social media that Bitcoin has increased 100 times from 2021 to 2024. So, regarding how to hold good assets and the topic of long-term holding, why don't we throw it to Shen Yu first to see if he has any thoughts or experiences to share with us?

Shen Yu: OK, first, this question can be divided into two parts: the first is the definition of "good assets," and the second is "how to hold them long-term."

For the first question, the dimension of "good assets" may need to be judged based on current understanding and long-term projections. If an asset has a clear development curve, or if its potential growth trends and key inflection points are already evident, then it may enter the "good asset" category. Then, it should be compared with other assets to ultimately determine whether it is a "good asset." I won't elaborate on the judgment of good assets, as everyone will have some subjective understanding.

The core issue is, once a good asset is identified, how to hold it long-term and "hold on"? Here, I want to emphasize that the focus is not on rational aspects but on psychological aspects, specifically irrational factors. Human nature tends to lean towards the irrational, so we need to establish rules and methods when we are rational and calm to ensure that even in states of emotional loss of control or FOMO, we can maintain relative rationality. Even after making irrational decisions, these rules can help us avoid having too much impact on our overall investments.

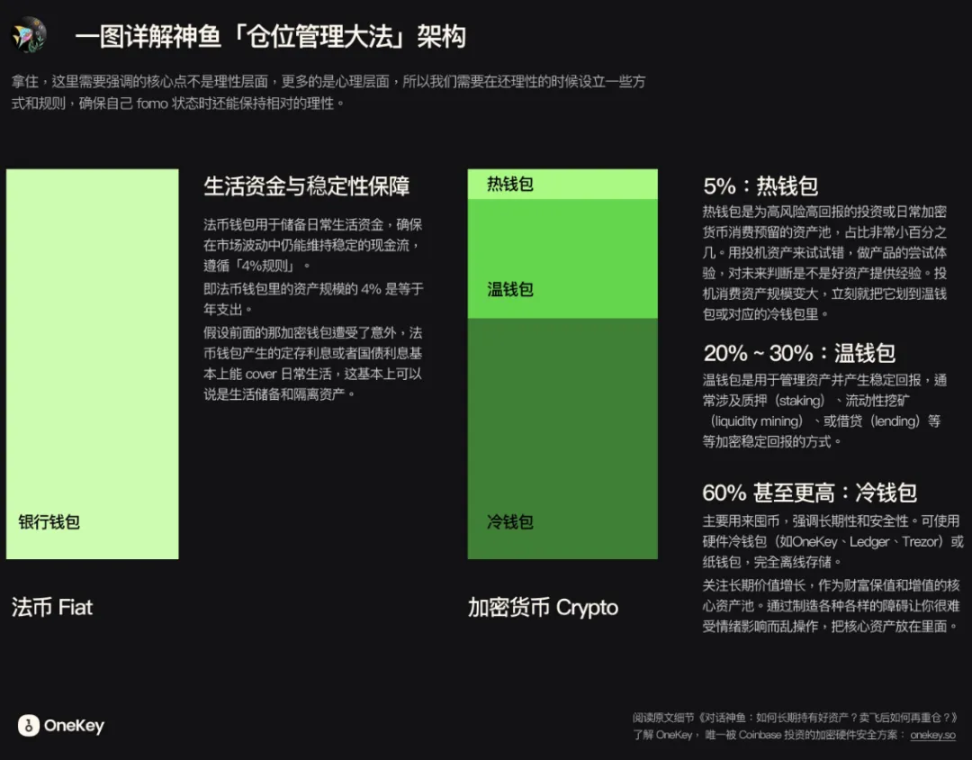

Building this framework, I believe, is a crucial system. This involves what is known as position management. When I first entered the space, an elder told me about the importance of this skill. After years of practice, I summarized a "Four Wallet" rule, dividing assets into four parts.

The first is the cold wallet, mainly used to accumulate core assets and set various operational barriers to make it difficult to access easily. When you are in a FOMO state and want to sell most of your assets, you will find that a series of operations are required to achieve this, and this time may help you calm down. Typically, this wallet accounts for more than 60% of total assets.

The second is the warm wallet, mainly used for asset management and providing stable cash flow support to maintain a stable mindset, especially in extremely pessimistic market conditions. This part of the asset accounts for about 20% to 30%.

The third is the hot wallet, mainly used for consumption and speculation, such as trying new products, buying NFTs, and other high-risk operations. This part of the asset is very small, accounting for only a small amount of funds. One characteristic of the hot wallet is that if its assets grow significantly, the profit portion should be promptly transferred to the cold wallet or warm wallet to avoid long-term risks.

Finally, there is the fiat wallet, for which I adopt a "withdraw only, no recharge" strategy. The fiat wallet is mainly used for living expenses, and I follow a "4% principle," meaning that the assets in the fiat wallet and the interest generated can cover my annual expenses. Even if the assets in other wallets incur losses, the fiat wallet can still ensure my daily living expenses, helping me maintain a state of financial independence.

Through this system, I can maintain emotional stability during short-term FOMO or irrational states. Even if the assets in the hot wallet go to zero, it is still within an acceptable range because these risks were anticipated when I was in a rational state. At the same time, for some "jealous" assets, such as meme tokens, I will try them with the hot wallet, so even if I fail, it won't affect the overall plan.

This is my core strategy and mindset management method for long-term asset holding.

Cognition and Belief Determine Whether One Can Hold Good Assets Long-Term

Peicai: I think, from my own experience, cognition is the most important. If you have no belief in an asset, when its price rises too much, to be honest, it is very hard to hold on. Especially since many times, the market fluctuates repeatedly.

I also believe that impulsiveness is a problem. Many people get distracted by engaging in cash flow businesses or ventures, which become obstacles instead. I can share two cases.

The first is about Litecoin. During the period from 2017 to 2018, we held a lot of Litecoin, which rose from 20 to over 100, but then fell back to between 20 and 80. At that time, we were very fearful, afraid of profit reversal, and ultimately sold around 80. However, six months later, Litecoin rose to about 2500 RMB. This reflects that our understanding of the asset at that time was not deep enough, not only for Litecoin but also for Bitcoin. At that time, we didn't have much money and had a great need for cash, making it hard to hold long-term.

The second case is about Bitcoin. When Bitcoin was around 6000 RMB, we sold half out of fear. At that time, Bitcoin experienced the Bitfinex loss incident, with the price dropping from 6000 to 3000, then rising back to 6000. We sold because we were worried about another drop, but later Bitcoin continued to rise.

There is also the example of Dogecoin. When Dogecoin rose from 0.002 to 0.02 USD, I impulsively sold in the middle of the night, only to find that the price doubled or even quintupled the next day. At that time, I didn't deeply understand the driving logic behind Musk and didn't anticipate that such price fluctuations would continue to rise. These experiences made me deeply realize the importance of cognition and expectations.

Now, we hold Bitcoin more steadily because we have a long-term optimistic expectation for it. For example, we believe Bitcoin could rise to 5 million or even 10 million USD each. Because of this belief, when the price rises to 100,000 or 200,000, we won't easily feel the urge to sell.

Looking back at the early days, our lack of clear understanding of assets led to many erroneous operations, such as selling Ethereum when it rose from 2 to 6 USD, missing out on further gains.

In summary, cognition is the foundation for holding good assets long-term. Without a clear judgment of the asset's ceiling and an understanding of the logic supporting its value, it is difficult to persist in long-term holding. The cold wallet strategy and the "sell half" method mentioned by Shen Yu are powerful supplements to help control impulsiveness when cognition is insufficient. But ultimately, cognition and belief are key.

How to Overcome Short-Term Trading Impulses and Achieve Long-Term Holding of Good Assets?

Zhen Dong: Actually, we can divide this topic into two parts: first, how to identify good assets; second, how to hold good assets long-term.

We have already discussed a lot about understanding good assets, such as why we consider Bitcoin and Ethereum to be good assets? Or why we think Tesla is a good asset? This requires knowledge and perspective, such as financial knowledge, understanding cash flow and traditional investment theories, and even learning about the cyclical theories of investment masters like Buffett and Munger. At the same time, in the crypto space, we also need to understand models like complex systems, nonlinear growth, and innovation diffusion, especially in the internet age, where the speed of information and knowledge dissemination is faster than ever, providing more possibilities for us to understand good assets.

The biggest enemy hindering long-term holding of good assets is the obsession with short-term trading. Many people confuse long-term holding with short-term trading, which is a cognitive misconception. For example, many people rely on short-term trading to generate cash flow to meet living expenses, but such behavior essentially interferes with long-term investment. Especially those who have just accumulated their first pot of gold are more easily influenced by short-term price fluctuations.

From my observation, many people try to profit through high-frequency trading during short-term market fluctuations, such as taking profits immediately when prices rise by 20%, or engaging in short-term operations due to favorable expectations from events like elections. Such behavior may allow them to make some money in the short term, but in the long run, this approach often misses out on greater gains from good assets.

The solution to this problem is to clearly distinguish between funds for short-term trading and long-term investment. You can allocate a portion for trading in your mental accounting, but core assets must be held long-term. It's like the founder of Nvidia; if he had retained half of his shares, or even 1/10, he would have reaped huge rewards decades later. Similarly, for crypto assets, holding Bitcoin or Ethereum long-term without trading may far exceed the benefits of frequent trading.

Regarding the issue of re-investing after selling, I believe the core lies in recognizing one's limitations and promptly correcting mistakes. For example, when you realize your views are biased, you should take immediate action to rebuild your position. This process requires a rational and humble attitude. Rationality is about continuously making investment decisions with positive expectations, while humility is about acknowledging and correcting one's mistakes.

Finally, I want to emphasize that whether it is long-term investment or re-investing after selling, continuous learning and adjustment are necessary to truly achieve the long-term value of compound growth. Mistakes are not scary; what is scary is not correcting them. Holding assets is similar to interpersonal relationships; when misunderstandings arise, apologizing and repairing the relationship may be the best choice. Sincerity and honesty are always the cornerstones of success.

How to Hold and Re-invest in Good Assets Long-Term Based on Cognition and Monopoly Advantage?

Odyssey: Regarding long-term holding of good assets, I believe there are two key points: cognition and longevity.

On the aspect of cognition, it can be divided into two parts: rational understanding and emotional understanding. I agree with Peicai's view that "buying and selling are symmetrical." When you buy impulsively, you usually sell impulsively as well. If you conduct careful research and thoughtful consideration when buying, you will also be more rational when selling, rather than acting on impulse. This symmetry in buying and selling often reflects the combination of cognition and emotion.

Building an understanding of good assets requires a process. Many people mistakenly believe that they should fully understand the potential of an asset from the beginning, such as the value of Bitcoin or Ethereum when their prices were very low in the early days. However, the world's information gradually reveals itself as uncertainty decreases over time. The construction of understanding requires continuous updating of judgments and validations, such as observing whether the asset reaches certain monopoly thresholds or demonstrates network effects.

Take ChatGPT as an example; it has a strong technological advantage but has not demonstrated bilateral network effects and strong monopoly characteristics. Therefore, when investing, one needs to wait for certain critical points to appear rather than concluding based solely on short-term user growth or technological strength. Understanding assets through monopoly advantages allows investors to transcend price fluctuations and only sell when monopoly diminishes or stronger competitors emerge.

Regarding long-term holding, I believe there are two layers of benefits: one is the cognitive benefit, which means the asset has reached your product roadmap expectations; the other is the cognitive external benefit, which refers to non-linear growth that exceeds expectations. This exceeding cognitive benefit requires investors to have an open mindset, acknowledging that the potential of good assets may be greater than their own imagination.

How to re-invest after selling? This is a psychological challenge. Many people experience strong psychological barriers after selling, especially when it involves face or self-validation desires. This psychological pressure can hinder rational decision-making. My advice is that making mistakes is not scary; the key is how to respond to those mistakes. If you can view correcting mistakes as an achievement, then re-investing after selling is no longer an act of "losing face," but a correct choice based on new understanding.

In terms of specific operations, I tend to gradually increase my positions as the asset's product roadmap is realized, while also looking for opportunities during short-term market adjustments and favorable news. For example, some recent policy changes regarding Tesla may temporarily impact profits but can enhance long-term competitive advantages, making such opportunities good times to increase holdings.

In summary, the core of investing lies in continuously updating cognition, acknowledging mistakes, and adjusting strategies to ultimately maximize long-term value.

From Others' Lessons to Self-Growth: How to Establish Long-Term Investment Strategies Amid Uncertainty

Odyssey: I want to ask Shen Yu a question. Earlier, you mentioned that you didn't understand the position management and mental accounting mentioned by your seniors when you first entered the space. What experiences led you to build this system now? Was it a significant lesson that prompted this change?

Shen Yu: In fact, I have seen many lessons from others, especially some cases that left a deep impression on me. Let me give two examples to illustrate.

The first example is a story about selling too early. In 2012, there was a person in the Chinese Bitcoin community with a traditional finance background named Lao Duan Hongbian. He initiated a fund that raised 3 million RMB. At that time, Bitcoin was priced between 30 and 50 RMB, and he used these funds to accumulate a large amount of Bitcoin, some of which he bought from me. However, when Bitcoin's price rose from a few dozen RMB to several dozen USD, he liquidated the fund. Subsequently, Bitcoin soared to 1000 USD, but he became an opponent of Bitcoin. This is a typical case of failing to adjust after selling too early.

The second example occurred on December 8, 2013. At that time, the People's Bank of China issued a policy related to Bitcoin, causing its price to drop from 8000 to 2000 RMB. I witnessed a friend on the Bitcoin China platform "sell all" his holdings, directly crashing the price to 2000. These individuals, due to psychological trauma, never returned to the Bitcoin market.

I have also experienced similar lessons, such as selling Litecoin and Dogecoin too early. Through these experiences, I gradually realized a fact: everyone is irrational. We need to be honest about our emotions and behaviors. Although many mistakes seem absurd in hindsight, if the situation were to repeat itself, it is highly likely that similar choices would be made.

I have also tracked my trading decision success rate, which is only about 40% to 43%, never exceeding 45%. Therefore, I started writing a "decision log" to record the background, emotions, and future predictions of significant decisions, and then regularly review these decisions to analyze whether I regret them and if there are areas for improvement. This made me realize that the world is full of uncertainties; even if you think a certain technology is excellent, the market may not agree. Therefore, we need to face this complex world with an open mindset.

Mistakes are essentially feedback from the world, and the most painful mistakes are often the keys to growth. When we gain real and effective information from mistakes, it is important not to get caught up in emotions but to improve ourselves through reflection. I have witnessed many people rise from scratch to experience ups and downs, and I have found that those who can survive long-term in the crypto space, regardless of their background, share a common trait: they maintain an open mindset and a growth-oriented thinking.

In summary, these experiences have made me realize that I am not good at trading, but through observation, learning, and reflection, I have gradually built a position management system that suits me. This system helps me better manage emotions and assets in uncertain environments, achieving long-term investment goals.

How to Avoid Investment Traps Through Hierarchical Management?

Odyssey: I have another question, which can be divided into two layers: the first layer is how to recognize mistakes, and the second layer is how to conduct effective reflection and attribution. Some people, for example, after selling meme coins, reflect that they should have held onto such assets and not sold them. But this kind of reflection may lead to another problem, such as ultimately causing the asset to go to zero. How do you ensure that your reflection is correct and not fall into a new pit? For instance, some people hold onto zero-value coins but continue to allocate them using conventional position management methods, resulting in exacerbated losses.

Shen Yu: Of course, there are zero-value coins, and I have held quite a few. But my position management has a major premise: the allocation of assets is primarily managed according to market value or certain proportions, rather than simply averaging. Therefore, different assets have clear emphases in my system.

Many assets in my position management system do not even meet the threshold for the cold wallet. They mostly exist in entertainment-type positions, and to be promoted to the core asset level of the cold wallet, they need to undergo long-term observation and in-depth thinking. This is a lengthy process, and typically, assets that have not gone through one or two complete market cycles find it difficult to enter higher allocation levels.

This hierarchical management approach helps me more effectively filter and manage assets, thereby avoiding falling into new investment traps due to erroneous reflections.

How to Judge Turning Points and Re-invest in Core Assets After Selling?

Odyssey: Have you ever experienced selling and then buying back? For example, re-investing heavily in core assets that you previously sold? I know that most of Peicai's Bitcoin and Ethereum were obtained through mining, and he doesn't have the experience of directly buying back large positions, so I want to ask you this question.

Shen Yu: Yes, for example, Ethereum. In the early days, when Ethereum was priced at two RMB, I bought a lot. Later, when it rose to 20 RMB, I sold a significant portion of my holdings. When Ethereum rose to 140 RMB and stabilized for a while, I again gradually liquidated most of my position, leaving about 1/4 as an observation position.

At that time, there was a key event: Ethereum's hard fork rollback, which actually challenged the core logic of POW. This weakened my confidence in Ethereum, and I basically liquidated my holdings. Later, with the rise of the DeFi wave, Ethereum began to exhibit some new characteristics and the embryonic form of its ecosystem. When these characteristics gradually emerged and reached a turning point, I re-invested heavily in Ethereum.

I believe this turning point is crucial. It allowed Ethereum to gradually possess a certain monopoly, even though I may not have fully realized it at the time. As a front-line observer, I accumulated knowledge and judged that it had become a core asset worth heavy investment. So, this is a typical case of me selling and then buying back.

How to Filter and Discard Assets Unsuitable for Long-Term Holding?

Odyssey: Some people might think that you can easily buy back assets because you have enough redundancy and don't have to worry too much about whether the assets you buy back will go to zero. But conversely, if you find it easy to buy back assets, how do you choose to discard them when you realize that certain assets are not suitable? For example, regarding the BAYC NFTs we discussed about a year ago, do you plan to hold them until they go to zero, or do you have other plans?

Shen Yu: Regarding NFTs like BAYC, I did not allocate heavily; instead, I kept them in an observation position. That batch of NFTs was essentially allocated with a consumer mindset, feeling that they had certain potential but might not take off. In my overall asset allocation, I did not allow the NFT position to exceed a critical value, so they were mostly placed in hot wallets or consumption wallets, with only a few NFTs of rare value or emotional significance transferred to the cold wallet.

My basic approach is that for an asset to warrant heavy investment, it needs to undergo long-term observation and in-depth thinking. It must meet many conditions and cross a certain important turning point that I deem significant before being included in the core asset category. Before that, such assets are more about the process of building understanding, allocated with consumer or gambling-type funds in small amounts. For assets that do not meet the conditions for heavy investment, I maintain a certain level of flexibility rather than blindly holding them until they go to zero.

Which is More Difficult: Discovering Good Assets or Re-investing Heavily After Selling? Why?

Shen Yu: I have a question for everyone: where do you think the difficulties lie in discovering good assets and re-investing heavily after selling? Because in my view, discovering good assets is not difficult; good assets are often visible to everyone. The key is whether you dare to invest heavily.

Odyssey: I also think the difficulty lies in re-investing heavily after selling. The ability required for re-investing heavily after selling is essentially no different from that needed for heavy investment itself; both require very strong psychological preparation. It involves several core abilities, such as the ability to gradually increase positions as the asset's monopoly grows, and the ability to calmly correct mistakes after facing errors. This means you not only need to judge the value of the asset but also be able to exit promptly when you make a wrong judgment, and even re-enter at a higher price.

Peicai: My view is similar. I believe the challenge of heavy investment is far greater than discovering good assets. Many people have held Bitcoin, but most of them cash out after the price rises, and very few can hold long-term or even buy back heavily. Even among my relatives and friends, very few have sold Bitcoin and then bought it back, let alone invest heavily.

The difficulty of heavy investment lies in human nature's natural discomfort with large transactions. For example, when I bought Tesla, even though I had done extensive research, I was still limited by psychological barriers. When the absolute value of the chips increases, even if it does not account for a high proportion of the overall assets, the sheer amount can create psychological pressure. This phenomenon is similar to how we make decisions in small daily expenses versus high-value real estate transactions, where the decision-making logic is completely different.

At the same time, the difficulty of re-investing heavily after selling lies in the attitude towards facing mistakes. Acknowledging mistakes requires not only courage but also the need to overturn existing logic and reconstruct the cognitive system. This is an extremely energy-intensive process, and many people prefer to cover up their mistakes with simple assumptions rather than engage in thorough reflection. Incorrect attribution and obsession with image further exacerbate this difficulty.

From a philosophical perspective, for example, Popper's philosophy of science emphasizes that the advancement of human knowledge essentially relies on conjectures and refutations. Making mistakes and correcting them is the only way to discover new knowledge. This understanding may help us face mistakes more calmly, but in actual investment, emotional pressure and psychological anchors remain significant obstacles.

For instance, my perception of Bitcoin's price has been influenced by early experiences. Although I understand the long-term logic of Bitcoin, historical price anchors make me uncomfortable with buying at high prices. A similar phenomenon occurs with Tesla; I feel more comfortable making purchases within a certain price range, but when the price deviates from that range, regardless of whether it rises or falls, it becomes very difficult to take action.

In summary, the difficulty of discovering good assets is far less than that of heavy investment, and re-investing heavily after selling is even more challenging. It involves not only asset judgment but also facing challenges related to one's own psychology and cognition, which are not on the same difficulty level at all.

Can Not Aiming to Make Money Actually Lead to Earning More?

Shen Yu: I want to ask Odyssey another question. I have noticed that aside from arbitrage, which has certain returns, when your purpose in doing something is not directly to make money, you often find it easier to earn big money. Conversely, if the goal is directly aimed at making money, the difficulty of making money seems to increase exponentially. What do you think about this phenomenon?

Odyssey: Haha, I completely agree with your view. I think this relates to the difference between process-oriented and result-oriented approaches. When the goal is entirely focused on the result of "making money," the volatility of money itself can lead to a decline in decision quality. For example, Tesla's stock is priced at over $300, but the value of cash itself is very difficult to measure. If you keep your eyes fixed on these fluctuating results, your judgment and decision-making will be constrained by them, ultimately making it difficult to make stable choices.

Rational investing requires us to transcend current fluctuations and see the long-term consequences. The essence of investing is to make future decisions based on past information, so it is necessary to combine rationality, insights into the future, and a process-oriented approach. If one solely focuses on the constantly changing metric of money, it is easy to get caught up in short-term fluctuations, leading to chaotic decision-making.

Overall, I completely agree with your point; this shift in mindset is indeed a crucial aspect of investing.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。