From a business strategy perspective, Ethereum's modular transformation aims to maintain its ecosystem's dominance.

Authors: Alex Pack & Alex Botte

Compiled by: Deep Tide TechFlow

Executive Summary

Ethereum's performance lags behind Bitcoin and Solana. Critics argue that this is primarily due to Ethereum's choice of a modular strategy. Is this true?

In the short term, it is indeed the case. We find that Ethereum's shift to a modular architecture has led to a decline in ETH prices due to reduced fees and a decrease in token burn.

When considering the total market capitalization of Ethereum and its modular ecosystem, the situation is different. In 2023, the value generated by Ethereum's modular infrastructure tokens was comparable to Solana's total market capitalization, around $50 billion. However, in 2024, their overall performance is expected to lag behind Solana. Additionally, the profits from these tokens primarily flow to teams and early investors rather than ETH token holders.

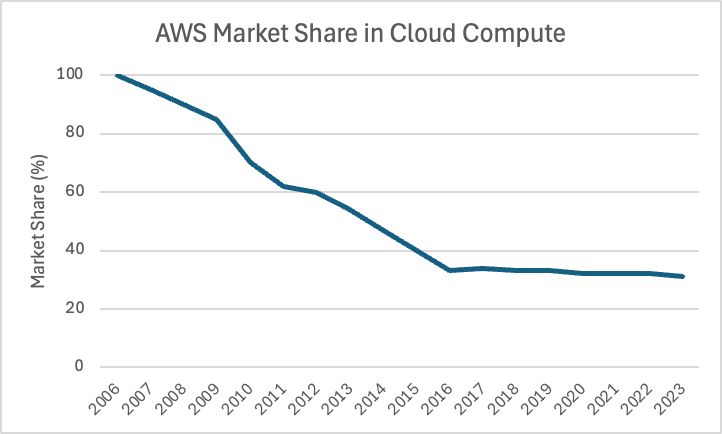

From a business strategy perspective, Ethereum's modular transformation is aimed at maintaining its ecosystem's dominance. The value of a blockchain is reflected in the scale of its ecosystem; although Ethereum's market share has decreased from 100% to 75% over the past nine years, this proportion remains quite substantial (we compare it to the leader in the Web2 cloud computing space, Amazon Web Services, whose market share has dropped from nearly 100% to 35%).

In the long run, the greatest advantage of Ethereum's modular strategy lies in enabling the network to adapt to future technological advancements to avoid obsolescence. Through its Layer 2 solutions, Ethereum successfully navigated the first major challenge of Layer 1 blockchains, laying the groundwork for its long-term resilience (despite some trade-offs).

Introduction: Where is the Problem?

In this market cycle, Ethereum's performance has not matched that of Bitcoin and Solana. Since the beginning of 2023, ETH has risen by 121%, while BTC and SOL have increased by 290% and 1452%, respectively. Why is this happening? Many viewpoints suggest that the market is irrational, the technical roadmap and user experience lag behind competitors, and Ethereum's ecosystem is losing market share to rivals like Solana. Could Ethereum become the AOL or Yahoo! of the cryptocurrency space?

The primary reason for this underperformance is a deliberate strategic decision made by Ethereum about five years ago: to shift to a modular architecture while decentralizing and deconstructing its infrastructure development roadmap.

In this article, we will explore Ethereum's modular strategy and assess its impact on ETH's short-term performance, Ethereum's market position, and its long-term prospects through data analysis.

Ethereum's Strategic Shift to a Modular Architecture: How Bold is it?

In 2020, Vitalik and the Ethereum Foundation (EF) made a bold and controversial decision to deconstruct the various components of Ethereum's infrastructure. Ethereum would no longer handle all aspects of the platform (such as execution, settlement, data availability, ordering, etc.) on its own but would encourage other projects to provide these services in a composable manner. This process began by promoting new rollup protocols as Ethereum's Layer 2 (L2) to handle execution (see Vitalik's 2020 article "A Rollup-Centric Ethereum Roadmap"), and now there are hundreds of different infrastructure protocols competing to provide what were once Layer 1 (L1) exclusive technical services.

To understand how radical this idea is, one can imagine a Web2 analogy. A similar example of Ethereum in Web2 is Amazon Web Services (AWS), a leading cloud infrastructure platform for building centralized applications. Imagine if AWS, when it launched 20 years ago, had only focused on its flagship products, such as storage (S3) and computing (EC2), rather than expanding into the dozens of different services it offers today. AWS might have missed a huge opportunity to increase customer revenue by expanding its service suite. Additionally, by providing a comprehensive product service, AWS could create a "walled garden" that makes it difficult for customers to integrate with other infrastructure providers, thereby locking in customers. This is exactly what happened. AWS now offers dozens of services, and the stickiness of its ecosystem makes it hard for customers to leave, with revenue growing from hundreds of millions in its early days to an expected annual revenue of $100 billion today.

However, the result is that AWS's market share has gradually been eroded by other cloud service providers, such as Microsoft Azure and Google Cloud, which have been steadily growing year by year. The initial market share of nearly 100% has now dropped to about 35%.

What if AWS had taken a different approach? What if it acknowledged that other teams might perform better on certain services, chose to open its API, and prioritized modularity and interoperability instead of trying to lock in users? AWS could have allowed developers and startups to build complementary infrastructure, creating more specialized services and forming a developer-friendly ecosystem that enhances the overall user experience. While this might not have increased AWS's revenue in the short term, it could have given AWS a larger market share and a more vibrant ecosystem.

Nevertheless, for Amazon, this might not have been cost-effective. As a publicly traded company, it needs to focus on current revenue rather than a "more active ecosystem." Therefore, deconstruction and modularity might not be suitable for Amazon. However, for Ethereum, this could be reasonable because Ethereum is a decentralized protocol, not a company.

Decentralized Protocols vs. Companies

Decentralized protocols, like companies, can generate usage fees and even have "revenue" to some extent. But does this mean that the value of a protocol should be measured solely based on this revenue? The answer is no. Today, this is not the measuring standard.

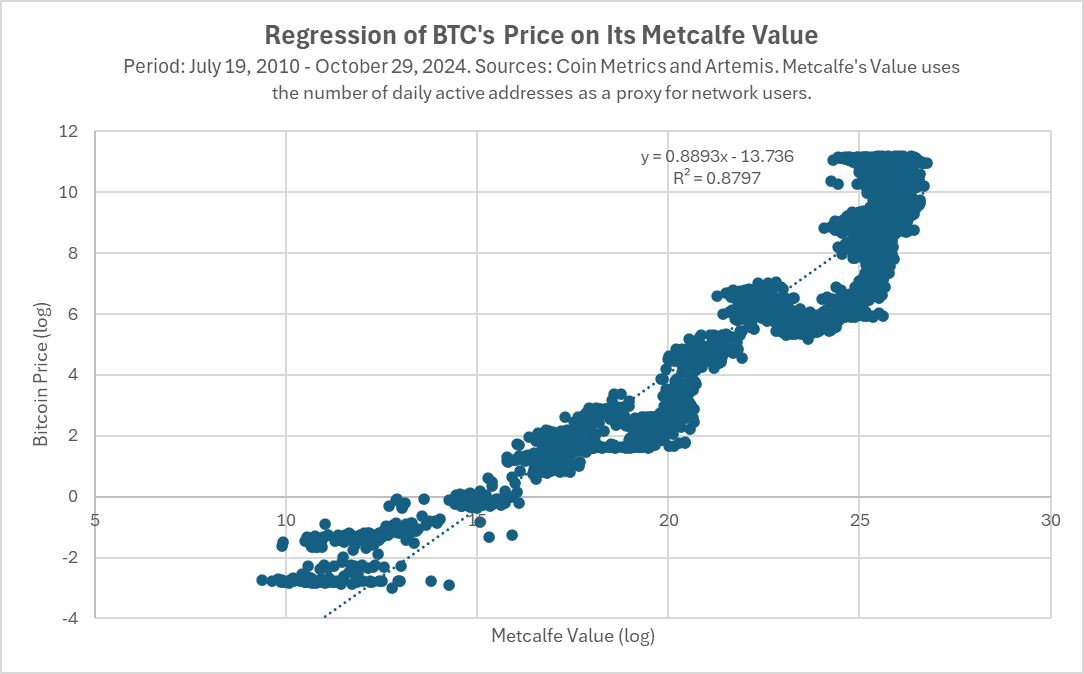

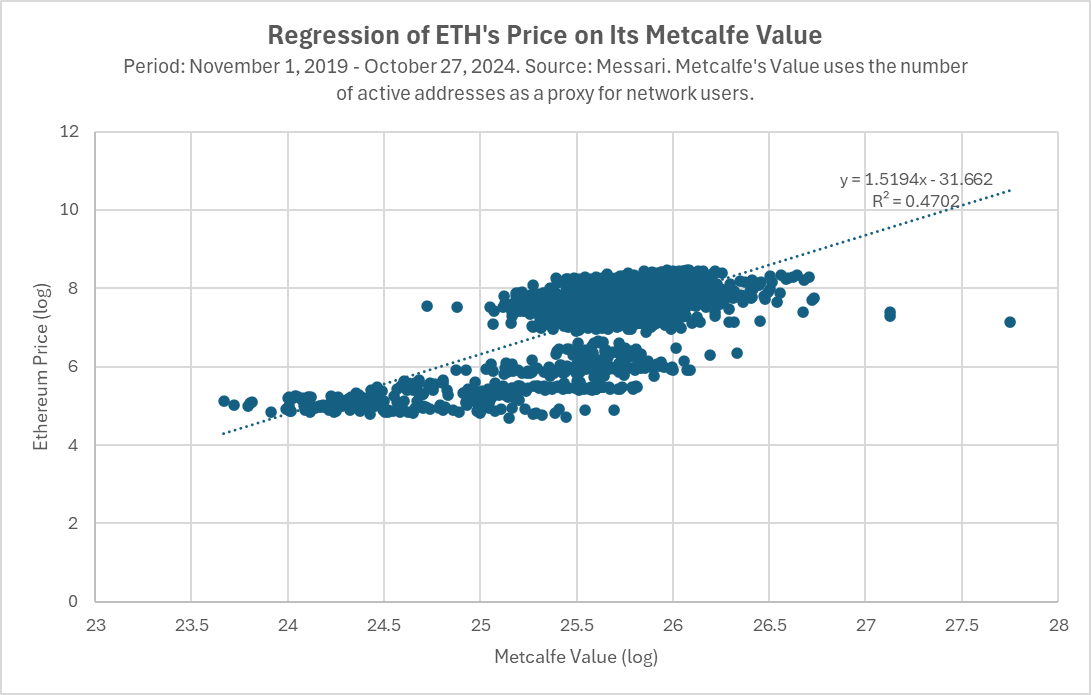

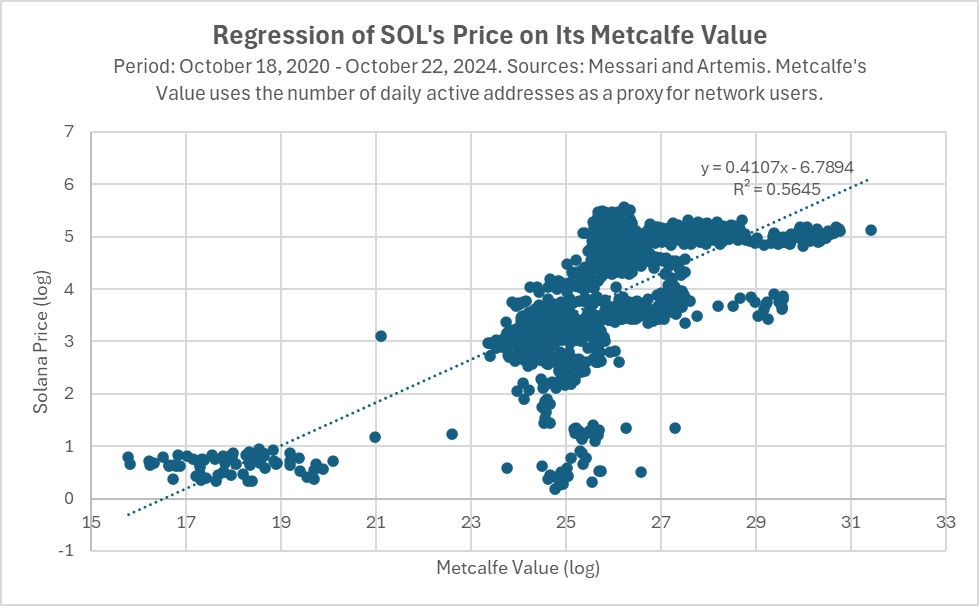

In the Web3 space, the value of a protocol is more dependent on the overall activity on its platform and whether it has the most active developer and user ecosystem. Our analysis comparing Bitcoin, Ethereum, and Solana shows a high correlation between token prices and Metcalfe's value (a measure of the number of network users), a relationship that has persisted for over a decade in the case of Bitcoin.

Why does the market place such importance on the activity of these tokens when pricing them? After all, stock pricing is typically based on growth and earnings. However, the current theories on how blockchains can appreciate their tokens are still in their infancy and have not shown strong explanatory power in the real world. Therefore, it is more reasonable to evaluate crypto networks based on network activity, including factors such as user numbers, assets, and activities.

Specifically, the price of a token should reflect the future value of its network (just as stock prices reflect a company's future value rather than its current value). This also leads to a second reason why Ethereum is considering modularity: to "future-proof" its product roadmap in order to increase the likelihood of Ethereum maintaining its dominance in the long term.

In 2020, Vitalik wrote his "Rollup-Centric Roadmap" when Ethereum was still in its 1.0 phase. As the first smart contract blockchain, Ethereum was clearly set to achieve several-fold improvements in scalability, cost, and security. For a pioneer, the greatest risk lies in failing to adapt quickly to new technological changes, thereby missing the next leap opportunity. For Ethereum, this meant transitioning from PoW to PoS and achieving 100 times greater blockchain scalability. The Ethereum Foundation (EF) needed to cultivate an ecosystem capable of scaling and achieving significant technological advancements, or it risked becoming the Yahoo or AOL of its era!

In the Web3 world, decentralized protocols have replaced traditional companies, and Ethereum believes that nurturing a strong and modular ecosystem is more valuable in the long run than fully controlling the infrastructure, even if it means relinquishing control over the infrastructure roadmap and core service revenues.

Next, we will explore the actual results of the modular decision through data.

The Impact of Ethereum's Modular Ecosystem on ETH

We analyze the impact of modularity on Ethereum from the following four aspects:

Short-term price (negative impact)

Market capitalization (beneficial for some)

Market share (outstanding performance)

Future technology roadmap (to be discussed)

1. Negative Impact: Fees and Prices

In the short term, Ethereum's modular strategy has had a noticeable negative impact on the price of ETH. Although ETH has rebounded significantly from its lows, its performance still lags behind BTC, some competitors like SOL, and even at times the Nasdaq Composite Index. This is largely due to its modular strategy.

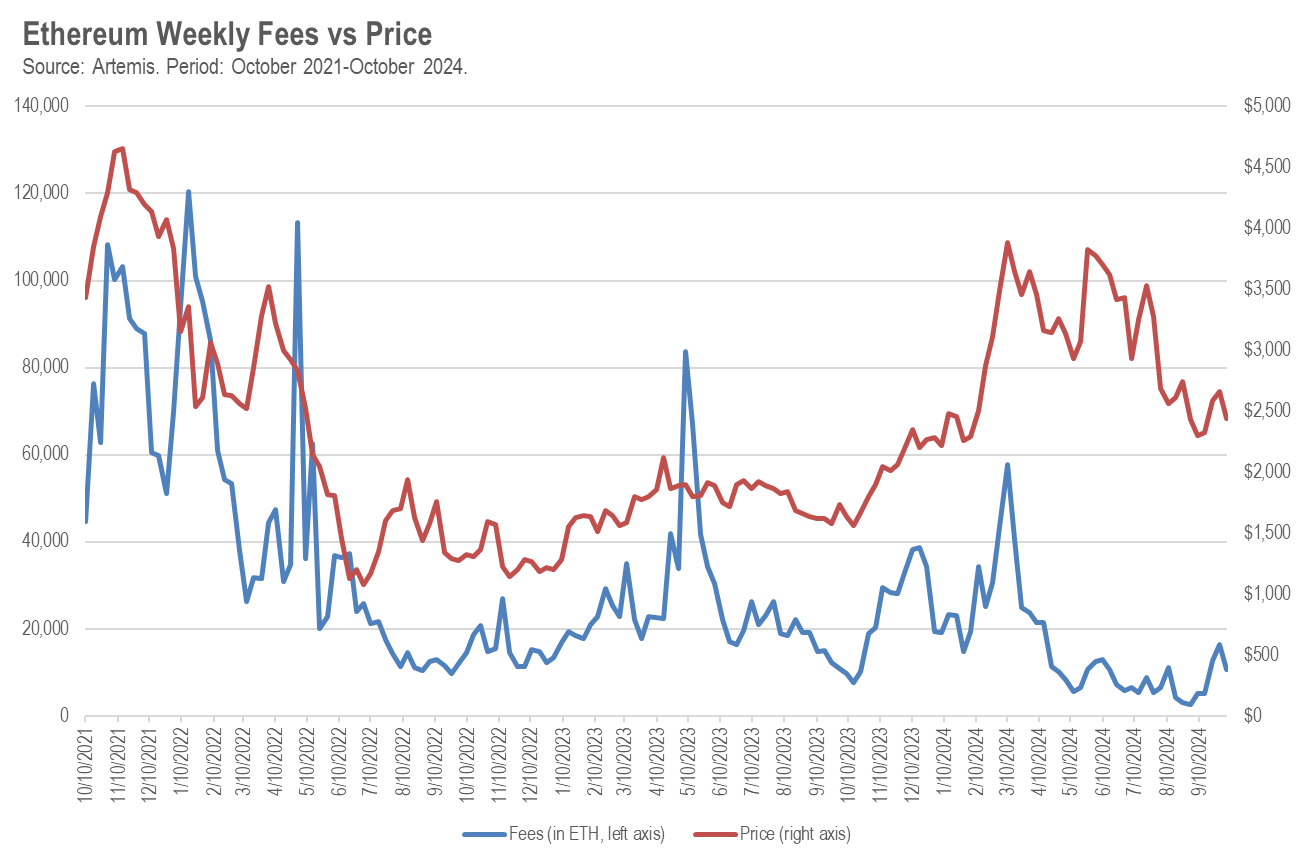

Ethereum's modular strategy first affected the price of ETH by lowering fees. In August 2021, Ethereum implemented the EIP-1559 proposal, which "burns" excess fees in the network, thereby reducing the supply of ETH. This is similar to stock buybacks in the stock market, which theoretically should have a positive impact on prices and indeed worked for a time.

However, with the launch and development of L2 execution layers and alternative data availability layers like Celestia, Ethereum's fees began to decline. As it relinquished its core revenue source, Ethereum's fees and income decreased, significantly impacting the price of ETH.

Over the past three years, there has been a significant statistical correlation between Ethereum's fees (measured in ETH) and the price of ETH, with a weekly correlation coefficient of +48%. If Ethereum's blockchain fees decrease by 1,000 ETH in a week, the price of ETH is expected to drop by an average of $17.

Thus, outsourcing execution to L2 has led to lower fees on L1, which in turn has reduced the burn of ETH, resulting in a price decline. At least in the short term, this is not good news.

However, these fees have not disappeared; they have flowed to new blockchain protocols, including L2 and DA layers. This has also led to a second potential impact of the modular strategy on the price of ETH: most of these new blockchain protocols have their own tokens. In the past, investors only needed to purchase one infrastructure token (ETH) to participate in all the growth of the Ethereum ecosystem; now they need to choose among many different tokens (there are 15 listed in the "modular" category on CoinMarketCap, with more VC-backed projects in development).

The new category of modular infrastructure tokens may have influenced the price of ETH in two ways. First, if we view blockchains as companies, then theoretically, the total market capitalization of all "modular tokens" should belong to the market capitalization of ETH. This is similar to company spin-offs in the stock market, where the market capitalization of the old company typically decreases, corresponding to the new company's market capitalization.

However, the situation may be more unfavorable for ETH. Many cryptocurrency traders are not particularly sophisticated investors, and when they need to purchase dozens of tokens to participate in "all the innovative growth on Ethereum," they may feel overwhelmed and even choose not to buy. This psychological burden, along with the transaction costs of purchasing multiple tokens instead of a single token, may negatively impact the prices of both ETH and the modular tokens.

2. The Positive Side (for Some): The Market Capitalization Story

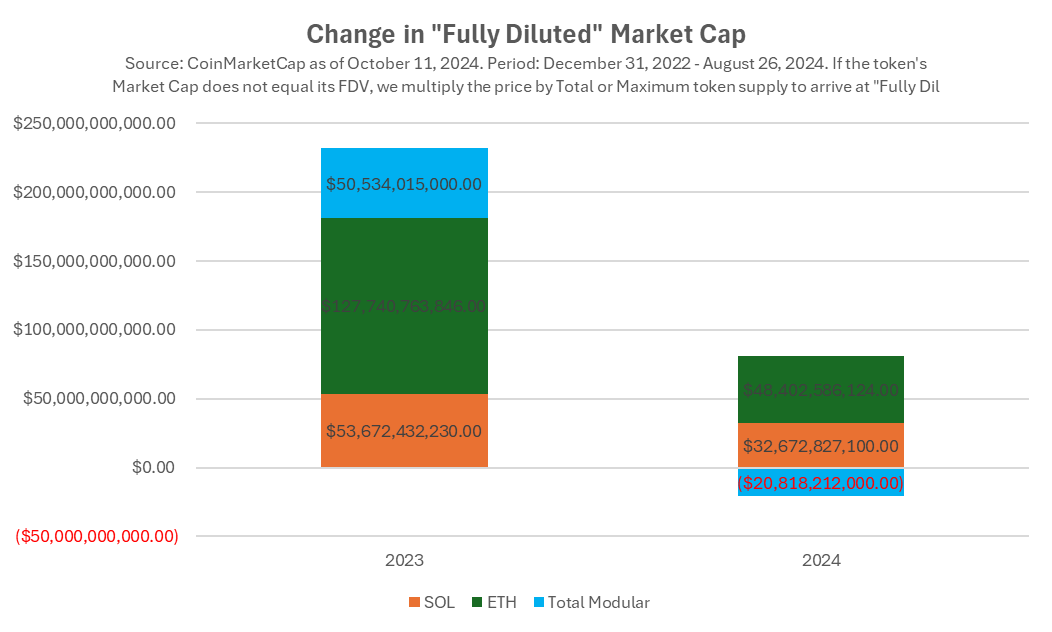

Another way to assess the impact of Ethereum's modular strategy on its success is to observe the changes in its market capitalization. In 2023, the market capitalization of ETH grew by $128 billion. In contrast, Solana's market capitalization increased by $54 billion. Although ETH's absolute growth is higher, Solana started from a lower base, resulting in a price increase of 919%, while ETH grew by 91%.

However, when considering the market capitalization of all the new "modular" tokens developed through Ethereum's modular strategy, the picture changes. In 2023, the market capitalization of these tokens increased by $51 billion, roughly on par with Solana's market capitalization growth.

What does this indicate? One interpretation is that the Ethereum Foundation (EF), through its shift to a modular strategy, has created value for the Ethereum-related modular infrastructure ecosystem comparable to that of Solana. Additionally, it has generated a market capitalization of $128 billion for itself, which is quite remarkable! Imagine how astonishing it would be for Microsoft or Apple to spend years and billions of dollars building their developer ecosystems and then see Ethereum's achievements.

However, this trend did not continue into 2024. SOL and ETH continued to grow (albeit at a slower pace), while the overall market capitalization of modular blockchains declined. This may reflect a weakening of market confidence in Ethereum's modular strategy in 2024, possibly due to the pressure of token unlocks, or the market feeling overwhelmed by the need to purchase multiple tokens when they could choose to invest in just one token to access Solana's technological ecosystem.

Let us shift from price trends and market feedback to the actual fundamentals. Perhaps the market judgment in 2024 is incorrect, while the market judgment in 2023 was correct. Has Ethereum's modular strategy helped or hindered it in becoming the leading blockchain ecosystem and mainstream cryptocurrency?

3. Outstanding Performance: The Dominance of the Ethereum Ecosystem and ETH

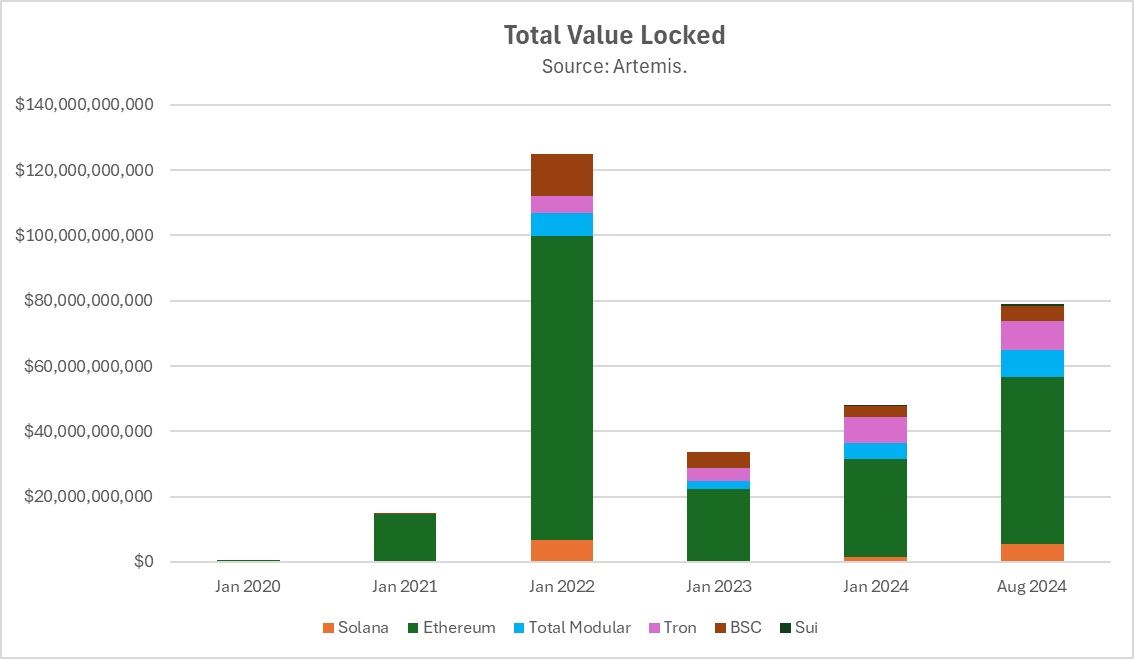

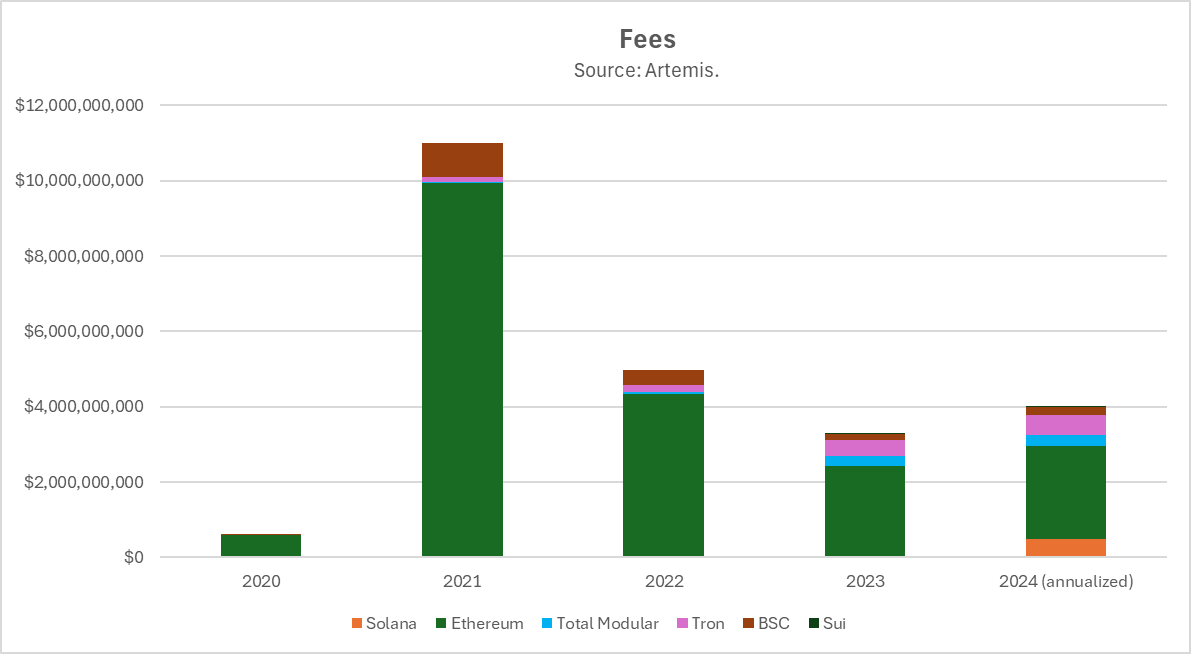

From a fundamental and usage perspective, Ethereum-related infrastructure has performed exceptionally well. Among peer projects, Ethereum and its L2 have the highest total value locked (TVL) and fees. The TVL of Ethereum and its L2 is 11.5 times that of Solana, and even when considering only L2, its TVL exceeds Solana's by 53%.

From the perspective of TVL market share:

**Since its launch in 2015, Ethereum initially held 100% of the market share. Despite facing hundreds of competing L1 projects, Ethereum and its modular ecosystem still maintain about 75% of the market share today. A decline from 100% to 75% over nine years is quite impressive! In comparison, *AWS* has seen its market share drop from 100% to about 35% over a similar timeframe.**

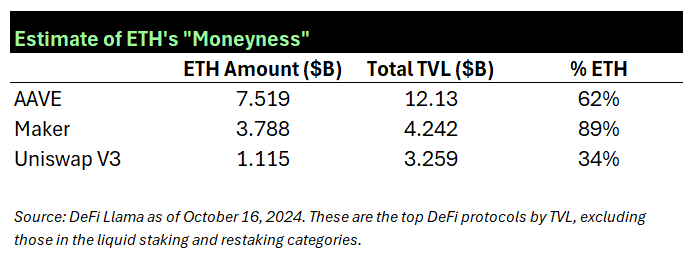

So, has ETH truly benefited from the dominance of the "Ethereum ecosystem"? Or is it the case that Ethereum and its modular components are thriving without utilizing ETH as an asset? In reality, ETH is a crucial component of the broader Ethereum ecosystem. As Ethereum expands to L2, ETH also expands in tandem. Most L2s use ETH as gas (network currency), and in the TVL of most L2s, the amount of ETH is at least 10 times that of other tokens. Please refer to the table below to see ETH's dominance in three major DeFi applications within the Ethereum ecosystem, including mainnet and L2 instances.

4. Worth Discussing: The Technology Development Story

From the perspective of the technical roadmap, Ethereum's decision to modularize the L1 chain into independent components allows projects to specialize and optimize within their specific domains. As long as these components maintain composability, decentralized application (dApp) developers can leverage the best infrastructure for building, ensuring efficiency and scalability.

Another significant advantage of modularity is that it enables the protocol to be future-proof. Imagine a game-changing technological innovation that only those protocols adopting it can survive. This scenario has been seen repeatedly in technological history: AOL's valuation plummeted from $200 billion to $4.5 billion due to its failure to transition from dial-up to high-speed broadband. Yahoo's valuation fell from $125 billion to $5 billion because it failed to timely adopt new search algorithms (like Google's PageRank) and missed the shift to mobile.

However, if your technical roadmap is modular, as L1, you do not need to chase every new wave of technological innovation yourself—your modular infrastructure partners can do that for you.

Does this strategy work? Let's take a look at the actual construction of Ethereum-related infrastructure:

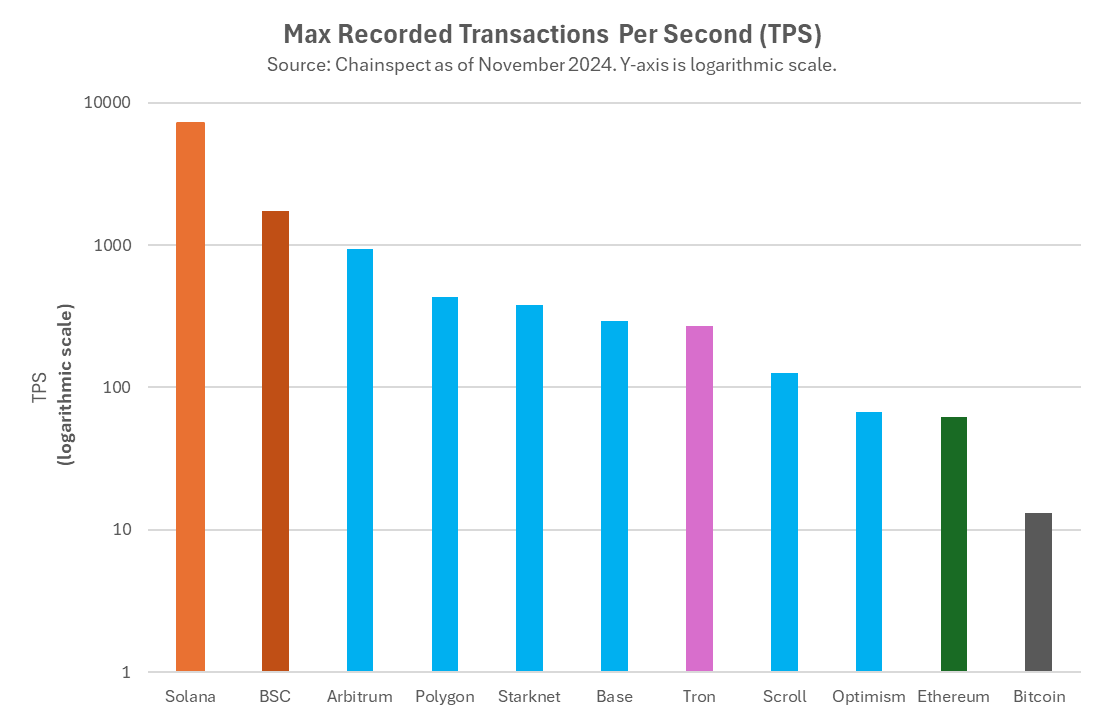

- Ethereum's L2 layers exhibit excellent scalability and execution costs. At least two innovative technologies have succeeded here: optimistic rollups, such as Arbitrum and Optimism, and zero-knowledge (zk) proof-based rollups, such as ZKSync, Scroll, Linea, and StarkNet. Additionally, there are many other high-throughput, low-cost L2s. The advancement of these two blockchain technologies has enabled Ethereum to achieve an order-of-magnitude improvement in scalability, which is no small feat. Dozens or even hundreds of L1s launched after Ethereum have yet to achieve a 2.0 version with 100 times the scalability and cost improvements. With these L2s, Ethereum successfully navigated the "first major mass extinction event" of blockchains: achieving a 100-fold increase in transactions per second (TPS).

New Blockchain Security Models. Innovations in blockchain security are crucial for the survival of protocols—just look at how every major L1 has transitioned from PoW to PoS. The "shared security" model pioneered by EigenLayer may be the next significant transformation. While there are similar shared security protocols in other ecosystems, such as Bitcoin's Babylon and Solana's Solayer, EigenLayer is the pioneer and the largest in Ethereum.

New Virtual Machines (VMs) and Programming Languages. A major criticism of Ethereum is its Ethereum Virtual Machine (EVM) and its programming language, Solidity. While writing code is relatively simple, it is a low-level programming language that is prone to errors and difficult to audit, which is one reason why Ethereum smart contracts frequently suffer attacks. For non-modular blockchains, trying multiple VMs or replacing the initial VM is nearly impossible, but Ethereum is different. A new wave of alternative VMs built as L2 allows developers to code in other languages without relying on the EVM, while still building within the Ethereum ecosystem. Examples include Movement Labs, which adopts the Move VM developed by Meta and promoted by leading L1s like Sui and Aptos; zk-VMs like RiscZero and Succinct, as well as implementations developed by A16Z's research team; and teams like Eclipse that are bringing Rust and Solana VM to Ethereum.

New Scalability Strategies. Similar to internet infrastructure or AI, significant scalability improvements are expected to emerge every few years. Even now, Solana has been waiting for years for the next major improvement developed by the Jump Trading team—Firedancer. Additionally, new ultra-scalable technologies are being developed, such as the parallel architectures of L1 teams like Monad, Sei, and Pharos. If Solana cannot keep up, these technologies may pose a survival threat, but Ethereum is different, as it can easily integrate these technological advancements through new L2s. This is also the strategy that new projects like MegaETH and Rise are attempting. These modular infrastructure partners help Ethereum incorporate significant technological innovations in the crypto space into its ecosystem, avoiding obsolescence and innovating alongside competitors.

However, this also brings trade-offs. As we mentioned earlier, as long as the various components maintain composability, the modular technical architecture can function well. As our friend "Composable Kyle" says, Ethereum increases the complexity of user experience when adopting a modular architecture. Ordinary users find it easier to get started with a single-structure chain like Solana, as they do not have to deal with issues like cross-chain bridging and interoperability.

In the Long Run

So where does all this lead us?

The modular ecosystem has sparked widespread discussion. The market's growth expectations for Ethereum-related modular infrastructure tokens in 2023 were similar to those for Solana, but the situation changed in 2024.

At least in the short term, the modular strategy has indeed had a negative impact on the price of ETH, primarily due to the resulting decrease in fees and burns.

Viewing the modular approach from a business strategy perspective reveals its rationale. Over the past nine years, Ethereum's market share has declined from 100% to 75%, while Amazon Web Services (AWS) has seen its market share drop to about 35% over the same period. In the world of decentralized protocols, the scale of the ecosystem and the dominance of tokens are more important than fees, which is good news for Ethereum.

From a long-term perspective, Ethereum's modular strategy and its future technological upgrades to avoid becoming the AOL or Yahoo! of the crypto world are also performing well. Through L2, Ethereum has successfully navigated the first "mass extinction event" of L1 blockchains.

However, this also brings trade-offs. The modular Ethereum is not as composable as a single chain, which affects user experience to some extent.

It remains unclear when the advantages of modularity will outweigh the reduced fees and the impact of competing modular Ethereum-related infrastructure tokens on the price of ETH. For early investors and teams of these new modular tokens, being able to share in the market capitalization of ETH is certainly a good thing, but the situation where modular tokens launch with unicorn valuations indicates that the distribution of these economic benefits is not balanced.*

In the long run, Ethereum may become stronger due to its investments in driving the broader ecosystem's development. Unlike AWS losing some market share in the cloud computing market, or Yahoo! and AOL nearly being wiped out in the competition for internet platforms, Ethereum is laying the groundwork to adapt, scale, and succeed in the next wave of blockchain innovation. In this industry, where success relies on network effects, Ethereum's modular strategy may be key to maintaining its dominance in the smart contract platform space.

Acknowledgments

Special thanks to Kyle Samani (Multicoin), Steven Goldfeder (Arbitrum), Smokey (Berachain), Rushi Manche (Movement Labs), Vijay Chetty (Eclipse), Sean Brown, and Chris Maree (Hack VC) for reviewing drafts, arguments, and data for this article.

Footnote

We need to state here that we may have some bias, as our venture capital firm Hack VC is an early investor in many Ethereum-related modular infrastructure tokens, as mentioned in the previous footnote. Therefore, in some cases, we are also among those profiting from Ethereum's market capitalization, which may be detrimental to ETH token holders in the short term.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。