Author: @charlotte_zqh

This research report is supported by international crypto media and primary investor @RomeoKuok.

Pendle is undoubtedly one of the standout assets in this round, rising from $0.7 in August 2023 to $7.5 in April 2024, a strong increase of over 10 times in just six months, making it one of the best-performing altcoins. Meanwhile, Pendle's TVL has also risen, surpassing $6.6 billion at its peak. However, starting in April, Eigenlayer's announcement of an airdrop ignited the first wave of negative sentiment towards Pendle. By mid-May, PENDLE quickly fell to $3.8, a drop of over 50% in less than a month. Although it rebounded afterward, as the re-staking sector cooled down and pessimism spread across the entire Ethereum ecosystem, Pendle fell into a downturn, with the price of PENDLE dropping to $2 on August 5. This article will provide a systematic analysis of Pendle's mechanisms, examining how Pendle quickly captured market demand, directly translating fundamentals into price, and how it was negatively impacted by the cooling of the Ethereum ecosystem, leading to its decline.

1 Pendle 101: How to Achieve Separation of Principal and Yield

1.1 Separation of Yield-Generating Assets

Pendle is a decentralized finance protocol that allows users to tokenize and sell future yields. In the specific business process, the protocol first wraps yield-bearing tokens into SY tokens (Standardized Yield Tokens), which are tokens under the ERC-5115 standard that can encapsulate most yield-generating assets. Subsequently, the SY tokens are split into two parts: PT (Principal Token) and YT (Yield Token), representing the principal and yield portions of the yield-generating asset, respectively.

PT is similar to a zero-coupon bond, allowing users to purchase it at a certain discount and redeem it at face value on the maturity date. Its yield is implicit in the difference between the purchase price and the redemption price. Therefore, if a user holds PT until maturity, they will receive a fixed return. For example, if PT-cDAI is purchased at $0.9, the user will receive 1 DAI at maturity, yielding (1-0.9)/0.9=11.1%. The act of purchasing PT is a short yield behavior, indicating that the user believes the future yield of the asset will decline below the current yield of PT. This fixed yield is suitable for low-risk preference users. However, this behavior differs from actual shorting; it is more of a value preservation action.

YT holders can receive all the yields of the yield-generating asset during their holding period, corresponding to the yield rights of the principal. If the yield is settled in real-time, YT holders can claim settled yields at any time. If the yield is settled at maturity, users can only claim yields with YT after maturity. Once the corresponding yields of YT are fully claimed, the YT asset becomes invalid. The act of purchasing YT is a long yield behavior, indicating that the user believes the future yield of the yield-generating asset will rise, and the total yield obtained will exceed the current purchase price of YT. YT provides users with a yield leverage, allowing them to directly purchase yield rights without needing to buy the entire yield-generating asset. However, if the yield significantly declines, YT assets face the risk of loss, making YT a high-risk, high-reward asset compared to PT.

Pendle provides tools for both long and short yield strategies, allowing users to choose corresponding investment strategies based on their yield predictions and judgments. Therefore, yield is an important indicator for participating in this protocol, and Pendle also offers various APYs to reflect the current market situation:

Underlying APY: The actual yield of the asset, calculated as a 7-day moving average yield, to help users estimate the future yield trend of the asset.

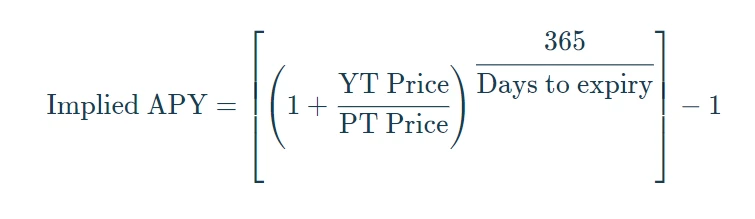

Implied APY: The market consensus on the future APY of the asset, reflected in the prices of YT and PT assets. Its calculation formula is:

Fixed APY: Specifically for PT assets, the fixed yield that can be obtained by holding PT, which is equal to the value of Implied APY.

Long Yield APY: Specifically for YT assets, the annual yield rate of purchasing YT at the current price. However, this yield rate is constantly changing because the yield of the yield-generating asset itself is changing (this value could be negative, meaning the current YT price is too high, exceeding the project's future yield). It is worth noting that many YT assets currently have potential yields from airdrops and points, making their value unquantifiable, resulting in many YT assets having a Long Yield APY of -100%.

These four yield rates are displayed simultaneously on the Pendle Market interface. When Underlying APY > Implied APY, it indicates that holding the asset will yield more than holding PT, at which point a long yield strategy can be adopted, i.e., buying YT and selling PT. When Underlying APY < Implied APY, the opposite strategy should be considered. However, it should be reiterated that these yield measurements do not account for future airdrop expectations, so the above strategies are only applicable to pure interest rate swap assets.

1.2 Pendle AMM: Facilitating Trading of Different Asset Types

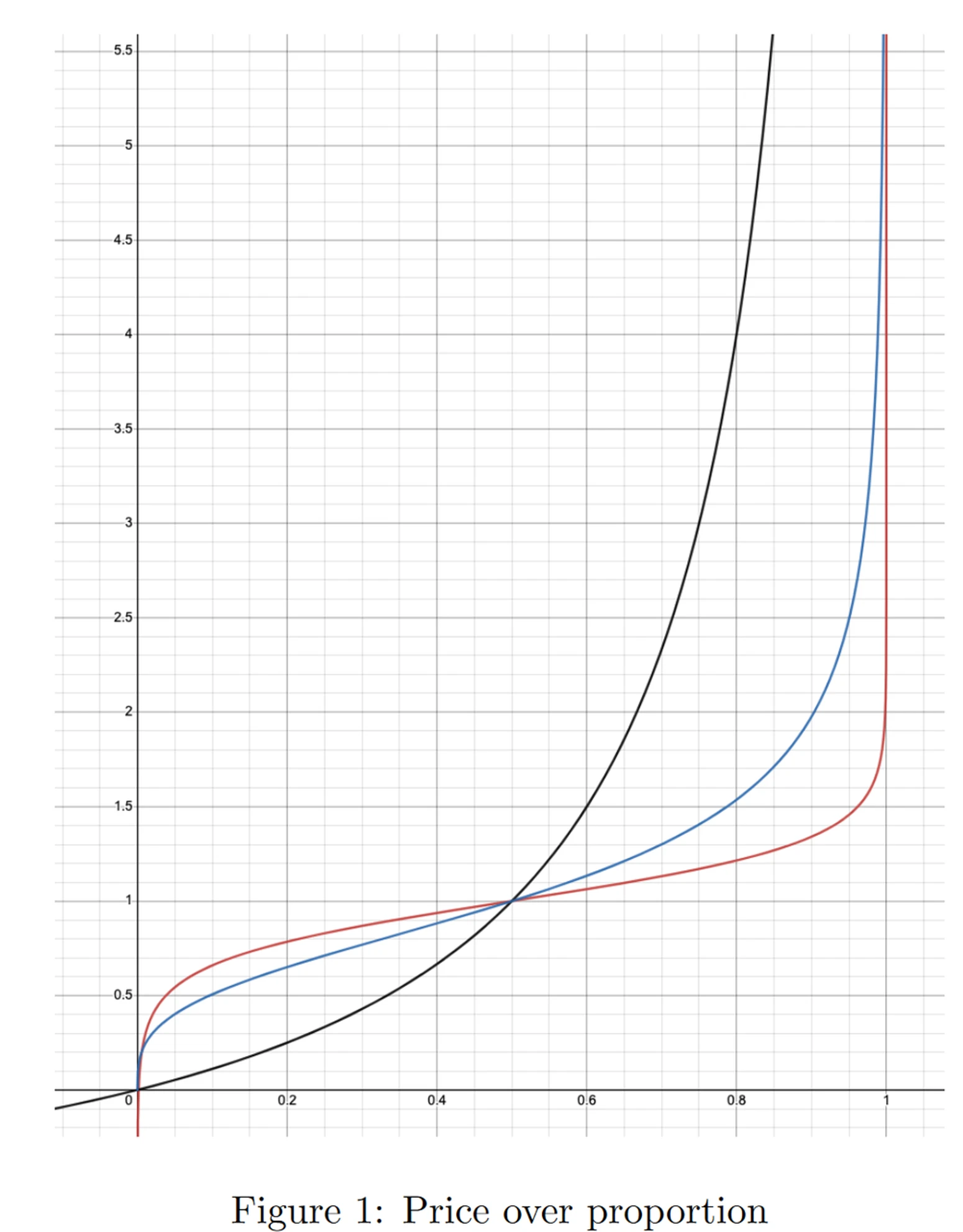

Pendle AMM is used to facilitate trading between SY, PT, and YT tokens. According to the Pendle whitepaper, in the V2 version, Pendle improved the AMM mechanism by drawing on Notional Finance's AMM model, enhancing capital efficiency and reducing slippage. The three AMM models for fixed income protocols on the market are illustrated below, where the X-axis represents the proportion of PT assets in the pool, and the Y-axis represents the Implied Interest Rate. Currently, Pendle adopts the AMM model corresponding to the red curve, while the black curve represents the V1 model, and the blue curve represents other fixed income protocols' AMM models.

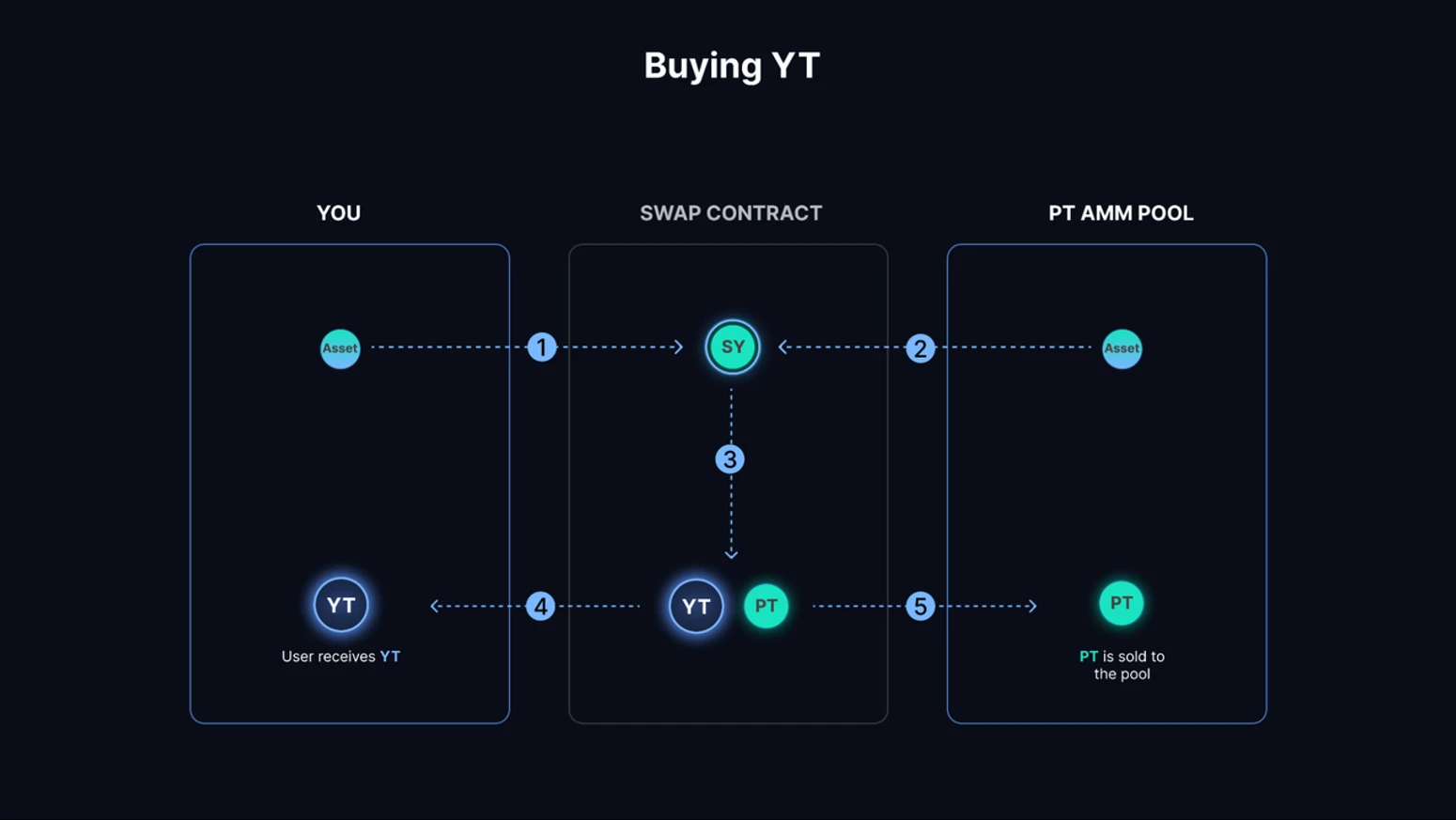

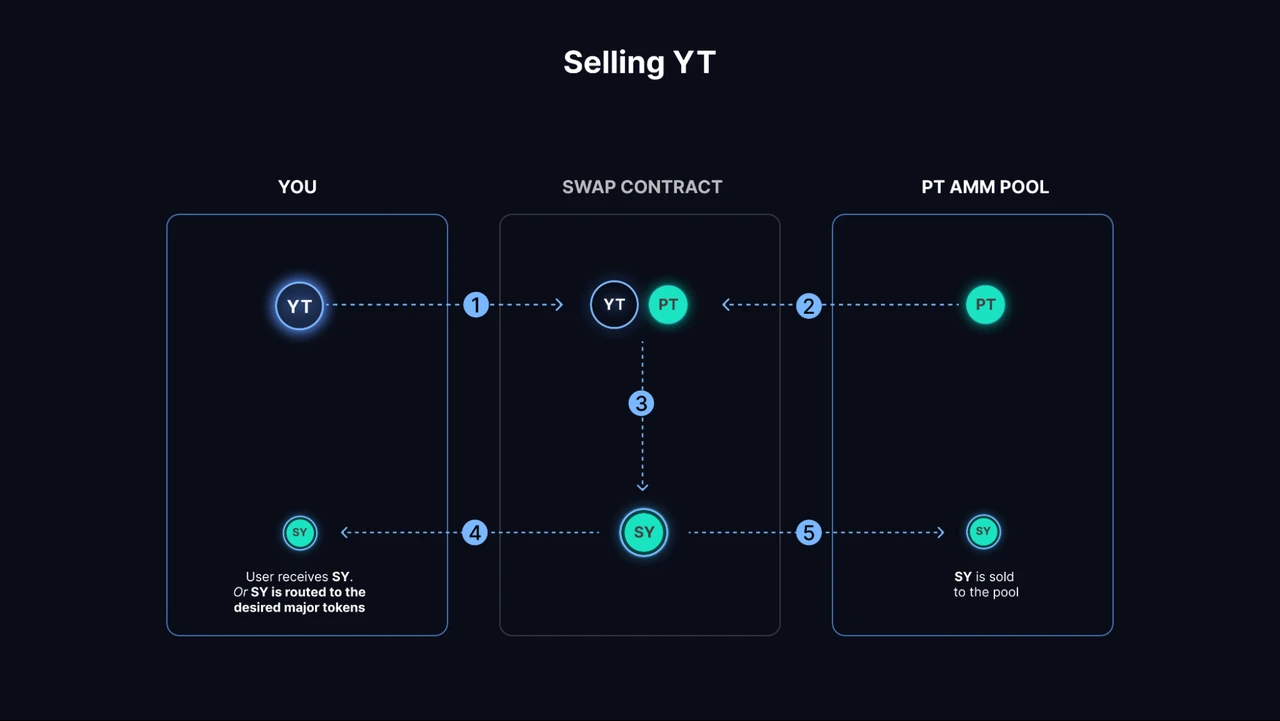

In specific pools, Pendle V2 uses PT-SY trading pairs, such as PT-stETH and SY-stETH, which can significantly reduce LP's impermanent loss (to be analyzed in detail later). Since SY = PT + YT, YT can be exchanged through Flash Swap. The specific process is as follows: if a user needs to purchase YT-stETH worth 1 ETH, they need to achieve the exchange from ETH to YT-stETH. Assuming 1 ETH = N YT-stETH, the contract will borrow N-1 SY-stETH from the pool and convert the user's ETH into SY-stETH (the specific process is to first exchange ETH for stETH through Kyberswap, then wrap it into SY-stETH within the protocol), and then split all SY-stETH (N in total) into PT and YT, giving the appropriate amount of YT (in this case, N) to the user, and returning PT (N in total) to the pool. What is actually completed in the pool is the exchange of SY-PT (N-1 SY exchanged for N PT).

The process of selling YT is the opposite. If a user wants to sell N YT (assuming the value of N YT is currently 1 SY), the contract will borrow N PT from the pool, combine them into N SY, give one SY to the user, and return N-1 SY to the pool. What is actually completed in the pool is the exchange of PT-SY (N PT exchanged for N-1 SY).

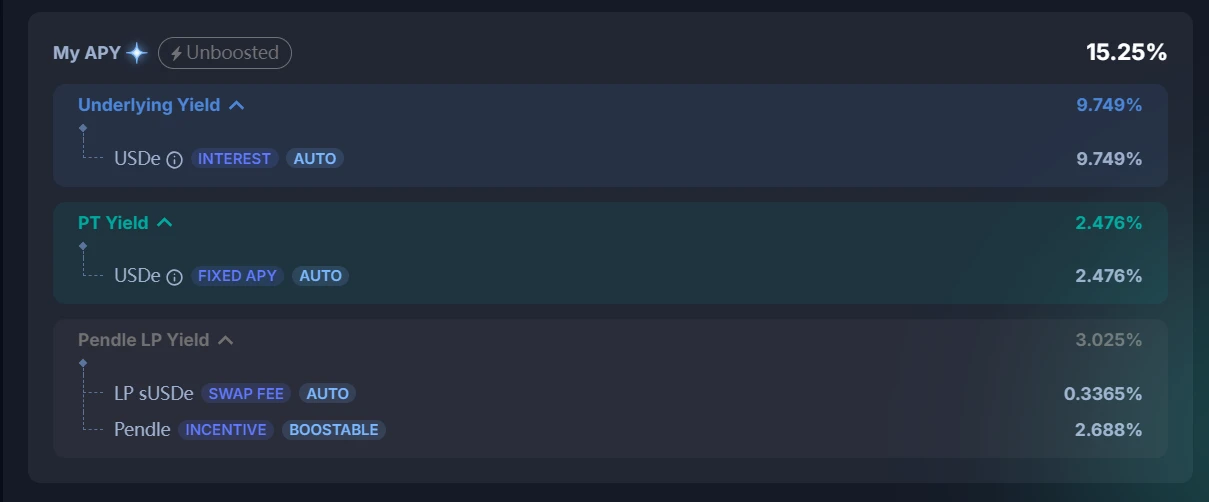

Like other AMMs, Pendle AMM also requires LPs to provide liquidity to the pool. However, since at maturity, one PT is always equal to one SY, there is no impermanent loss for LPs at maturity. When users provide liquidity, the assets provided are SY and PT assets, thus automatically capturing the native yield of these assets, in addition to transaction fees and PENDLE liquidity mining rewards, which include four sources of income:

PT fixed yield: The yield from purchasing PT itself.

Underlying yield: The yield from SY assets.

Swap fees: 20% of transaction fees.

PENDLE token incentives.

2 Token Economics: How Business Revenue Drives Price Increase?

2.1 Token Economic Mechanism: How to Achieve Economic Flywheel?

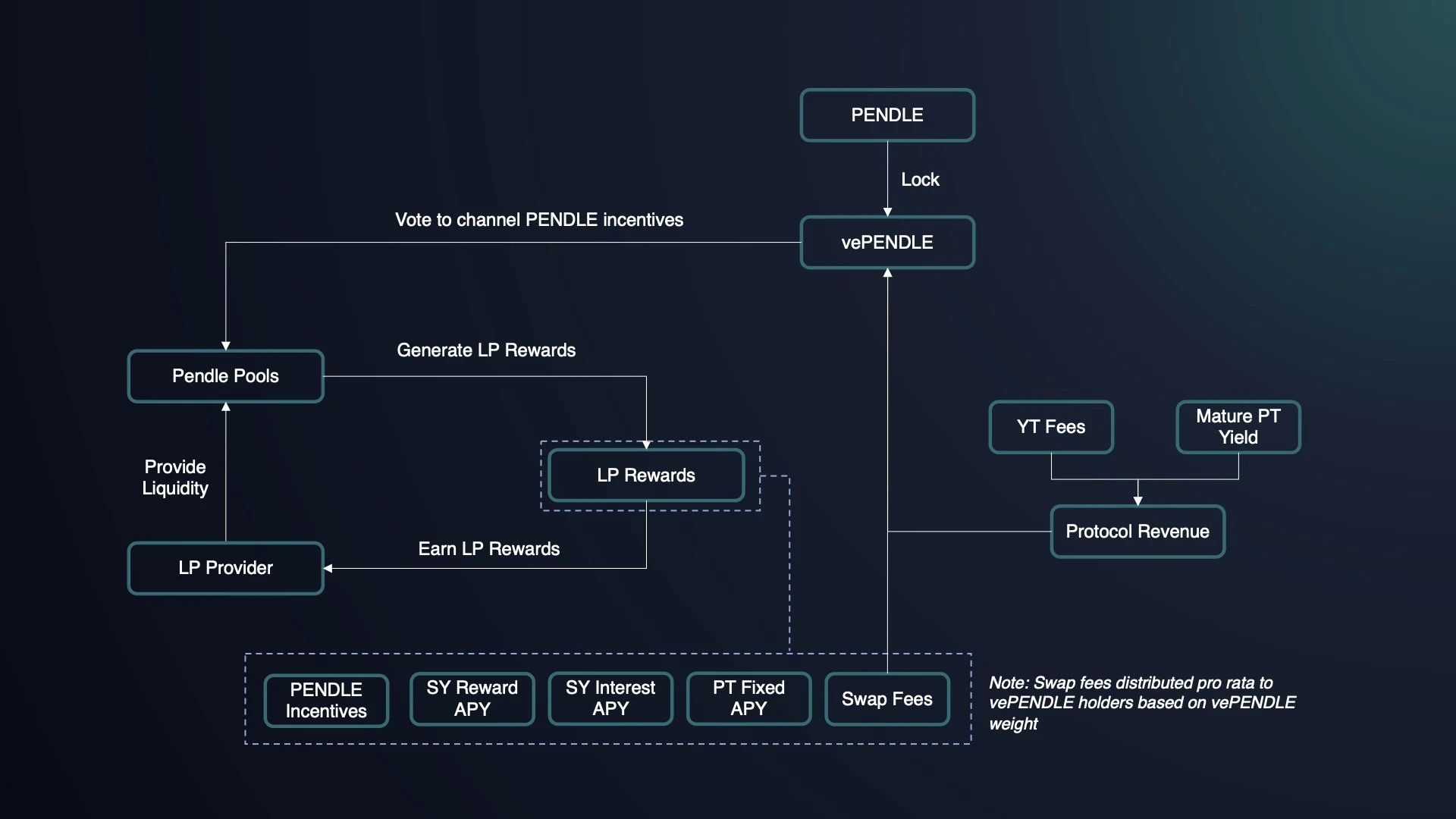

The token economic mechanism of PENDLE mainly revolves around locking up to obtain vePENDLE, which allows participation in protocol revenue sharing and governance decisions. Similar to Curve's veCRV model, users can lock PENDLE to receive vePENDLE, with longer lock-up periods yielding more vePENDLE, ranging from 1 week to 2 years.

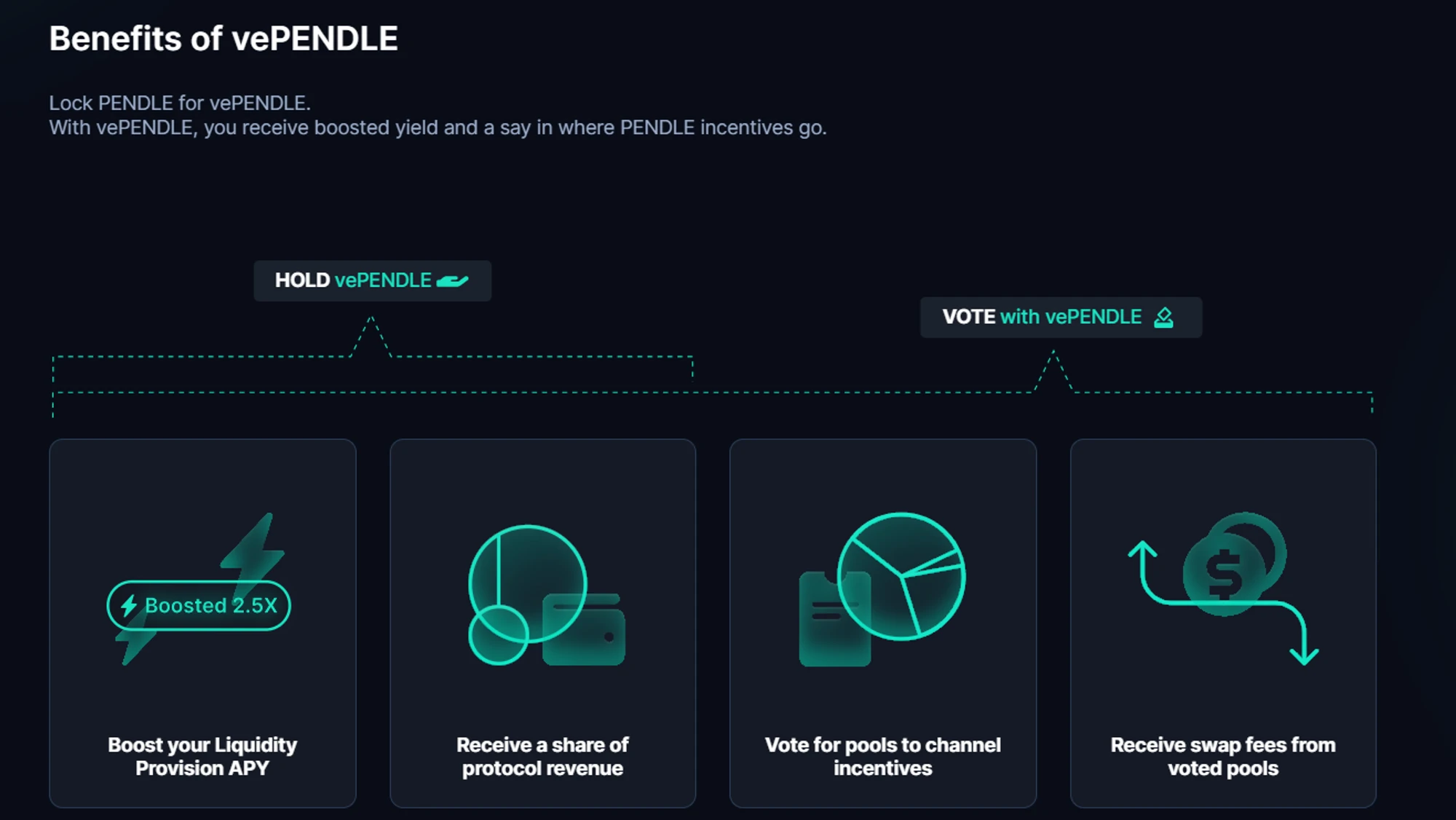

The benefits of holding vePENDLE include:

Boost Yield: Users can boost their earnings as LPs by up to 2.5 times.

Voting Rights: Users can vote on the distribution of PENDLE incentives across different pools.

Revenue Sharing: Holders of vePENDLE can receive the following benefits:

80% of the trading fee share from the voted pool: vePENDLE holders vote on the flow of PENDLE incentives, and only by completing the vote can they receive rewards from the selected trading pool.

3% of all YT earnings.

A portion of PT earnings: This portion comes from unredeemed PT. For example, if a user purchases PT assets and does not redeem them at maturity, after a period, this portion of assets is acquired by the protocol.

In terms of yield calculation, the Total APY for holding vePENDLE = Base APY + Voter’s APY, where Base APY comes from the earnings of YT and PT, and Voter’s APY comes from the trading fee share of designated pools, which is also a major component of APY—currently, the Base APY is only around 2%, while Voter’s APY can reach 30% or more.

Pendle's ve model has also facilitated the emergence of bribery platforms, with Penpie and Equilibria engaging in related businesses, similar to the business processes between Convex and Curve. However, compared to Curve, the core project parties trading assets on Pendle do not have a need for bribery. Curve, as a major trading platform for stablecoins and other pegged assets, ensures that the depth of the pool is crucial for maintaining the peg of the asset price, which drives project parties to participate in bribery to guide liquidity. However, maintaining trading depth in Pendle AMM seems to hold little significance for related project parties like LSD and LRT, so the main motivation for participating in bribery will come from LPs on Pendle. The establishment of bribery platforms primarily optimizes two issues: 1) Pendle LPs can achieve higher yields without needing to purchase and lock PENDLE; 2) PENDLE holders can obtain liquid ePENDLE/mPENDLE to gain vePENDLE incentives. Since this article focuses solely on Pendle, we will not elaborate further on the bribery ecosystem here.

2.2 Token Distribution and Supply: No Major Unlock Events Ahead

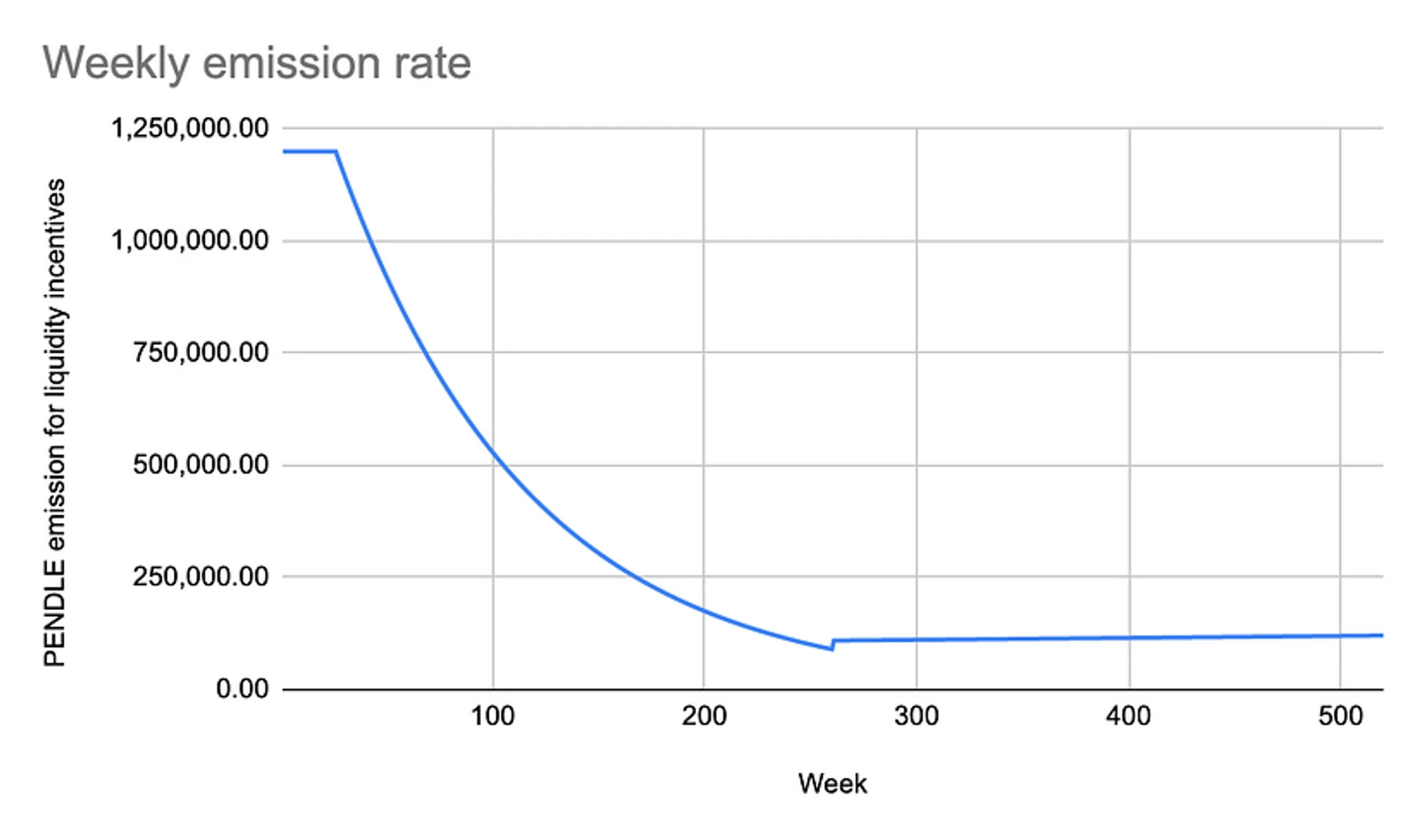

The PENDLE token was launched in April 2021, adopting a hybrid inflation model with no upper limit on token supply. It provided a stable incentive of 1.2 million PENDLE per week for the first 26 weeks, after which (from week 27 to week 260), liquidity incentives will decrease by 1% per week until week 260. After that (from week 261 onwards), the inflation rate will be 2% per year for incentives.

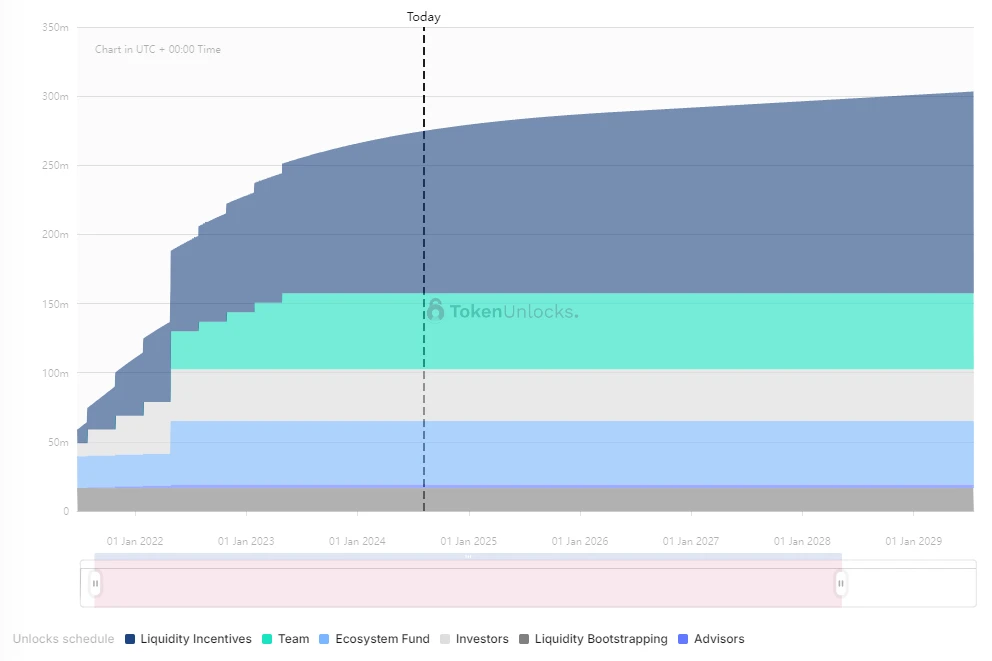

According to Token Unlock data, the initial token distribution allocated to the team, ecosystem, investors, advisors, etc., has now fully unlocked all tokens. If we do not consider OTC trading and only look at the initial distribution, PENDLE will not face significant concentrated unlocks in the future. Currently, daily inflation comes solely from liquidity mining incentives, with a daily emission of approximately 34.1k PENDLE. Based on the price on August 5 ($2), the daily unlock selling pressure is $68.2k, which is relatively small.

3 Application Scenario Development: Stable Wealth Management, Interest Rate Trading, and Points Leverage

Pendle's development can be roughly divided into three stages:

Pendle was established in 2021, during which, although it was the DeFi Summer, DeFi was in its infrastructure phase, with major projects revolving around DEXs, stablecoins, and lending. As a rate swap product, it did not receive much attention.

By the end of 2022, as Ethereum completed its transition to PoS, Ethereum staking rates became the native rates in the crypto space. A plethora of LSD assets quickly emerged, leading to: (1) interest rates becoming one of the focal points in the crypto space; (2) a large number of yield-generating assets being born, allowing Pendle to find its PMF; (3) Pendle becoming a small-cap asset in the hype of the LSD sector, with relatively few competitors in the niche market. The launch on Binance during this period further increased Pendle's valuation ceiling.

From late 2023 to early 2024, Eigenlayer initiated the re-staking narrative for Ethereum, leading to the emergence of numerous liquidity re-staking (LRT) projects. Both Eigenlayer and LRT projects announced points and airdrop plans, igniting a points war. This resulted in: (1) the birth of more yield-generating assets, effectively broadening Pendle's path to increase TVL; (2) most importantly, Pendle captured the intersection of principal-yield trading and points leverage, finding a new PMF. The following sections will elaborate on how Pendle plays a role in the points war and how it empowers the PENDLE token.

In summary, aside from becoming an LP and a holder of vePENDLE, Pendle's main use cases currently include three: stable wealth management, interest rate trading, and points leverage.

3.1 Stable Wealth Management

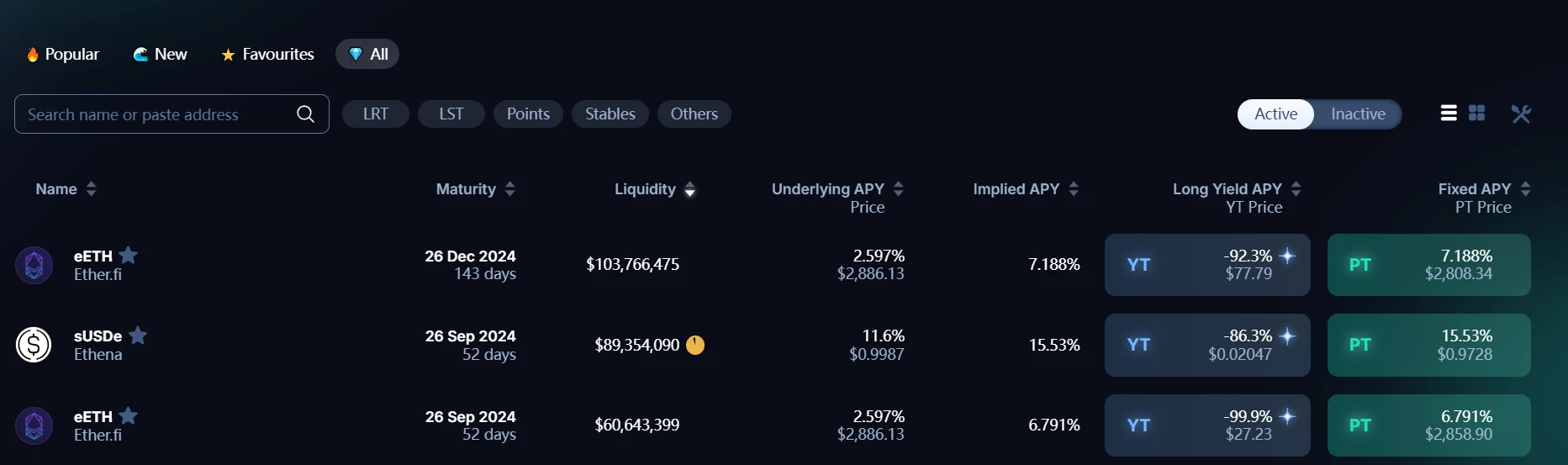

This primarily corresponds to the function of PT assets. By holding PT assets, users can receive a fixed amount of the corresponding asset at maturity, with this fixed rate determined on the purchase date, allowing users not to constantly monitor APR fluctuations. This function offers stable yields with low risk and low returns. After the launch of points trading, this function has further increased user yields: taking eETH as an example, users choose to forgo the yield from holding eETH for a higher fixed yield. As a result, the current yield of PT assets (7.189%) is significantly higher than (2.597%), providing a wealth management tool for users seeking higher fixed income in Ethereum. Some users who are not optimistic about the future token performance of LRT projects can buy PT assets at a low price when market FOMO drives up YT prices, effectively shorting LRT tokens.

3.2 Interest Rate/Yield Expectation Trading

Users can achieve long and short positions on interest rates through swing trading of YT assets. When they believe future yields will significantly increase, they buy YT assets and sell them when the price rises. This strategy is suitable for trading assets with high yield volatility, such as sUSDe, which is a staking certificate for the stablecoin issued by Ethena. The staking yield mainly comes from the funding rate for ETH; the higher the funding rate, the higher the staking yield, which depends on changes in market sentiment. Therefore, the staking yield also exhibits some volatility. By trading YT-sUSDe, users can quickly profit from swing trading. Additionally, after introducing points yield rights, trading YT assets also includes pricing changes based on airdrop expectations. For example, before the ENA token launch, early purchases of YT-USDe can be sold after market FOMO begins for the ENA airdrop, yielding high returns. However, this swing trading carries high returns and risks. For instance, the price of YT-sUSDe has recently declined repeatedly, partly due to the decreasing points earned from holding YT assets as the holding period shortens, and partly due to the continuous decline in ENA prices, leading to a decrease in market expectations for airdrop value, which may result in significant losses for early buyers.

3.3 Points Leverage and Trading

The most significant impact on Pendle in this cycle comes from the points trading function, providing users with potentially high leverage for points and airdrops. This article will focus on this function and aims to answer the following questions:

(1) Which projects are suitable for Pendle's points trading?

Points have become the primary form of airdrop distribution in this cycle, with methods to acquire points including interaction-based, volume-boosting, and deposit-based approaches, among which deposit-based methods have become the most prominent. With the emergence of various LRT protocols, BTC Layer 2, and staking protocols, the TVL battle has become a main theme this year. Some protocols directly lock related assets, such as BTC Layer 2 directly locking BTC and inscription assets, and Blast directly depositing ETH, while others return corresponding liquid assets as deposit certificates after deposits, allowing users to earn points through holding. Pendle's principal-yield separation mechanism is particularly suitable for the second type, which requires an underlying asset to serve as a medium for accumulating points.

(2) In what aspects has Pendle's points trading achieved PMF?

Pendle has achieved PMF in two main areas: first, by enabling the leverage of points, and second, by facilitating early pricing and expectation trading for airdrops. The TVL battle is a game for whales, as ordinary retail investors cannot hold enough ETH to deposit. Pendle allows users to directly obtain points yield rights by purchasing YT assets, enabling them to earn points without needing principal, achieving dozens of times leverage in projects like LRT and Ethena. Additionally, Pendle essentially provides the earliest market pricing for points, and trading YT assets also involves trading expectations for project airdrops and token prices. This can be further divided into two scenarios: ① For tokens that have not yet undergone TGE, most airdrop rules are unclear, thus encompassing both market expectations for potential tokens and early pricing for these tokens; ② For tokens that have already undergone TGE, the token price has a clear market price, while the unknown information may be how many tokens correspond to a single point airdrop. If the airdrop rules are relatively clear and it is known how many tokens can be obtained from the underlying asset at maturity, then this YT asset is equivalent to an option, with the current price reflecting expectations for the token price on the expiration date.

(3) How does points trading affect Pendle's business revenue and token price?

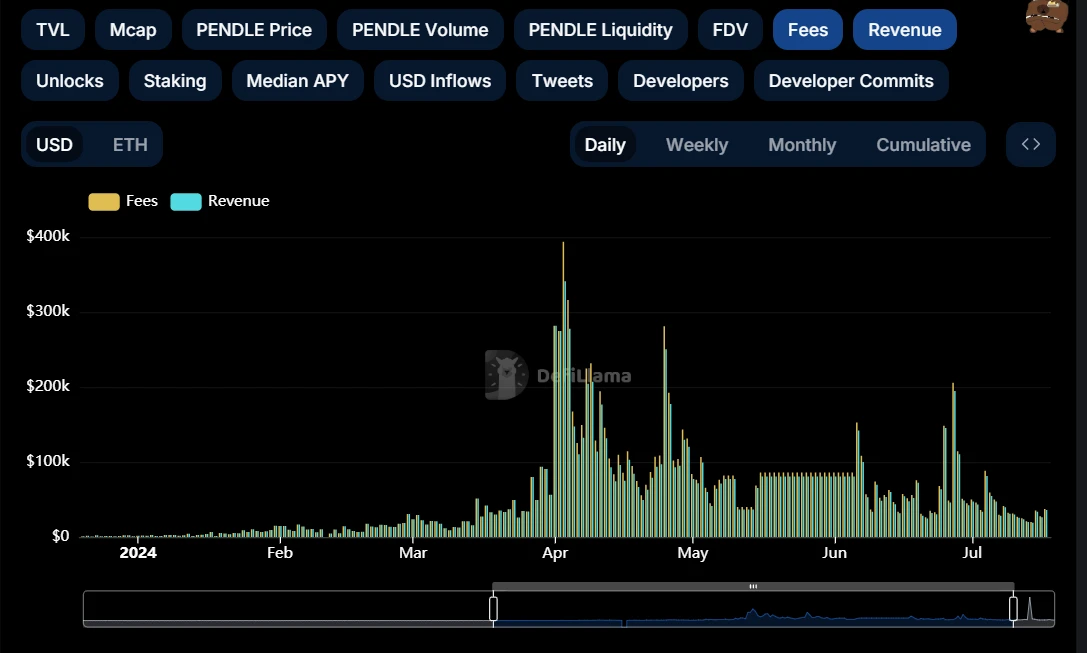

As analyzed earlier, the introduction of points trading has brought about trading expectations for future airdrops, which, compared to yield rates, change and fluctuate rapidly, leading to higher speculation and trading demand. Most directly, this has rapidly expanded Pendle's trading volume and trading fee revenue, and the diversification of asset classes has also increased Pendle's TVL.

The empowerment of PENDLE is even more evident. The income of vePENDLE holders mainly comes from the sharing of trading fees. Without sufficient volatility and speculative demand, there will not be enough trading, resulting in very low yields for vePENDLE. In July 2023, the total APY for vePENDLE was only around 2%. Therefore, although Pendle was riding the hype of the LSD sector at that time, the token price still could not benefit from the business. The introduction of points trading has changed this predicament, and currently, the APY for vePENDLE in multiple pools exceeds 15%, with some related asset pools for multiple LST assets even exceeding 30%.

(4) How do the performances of related projects affect Pendle?

The two core negative impacts surrounding Pendle include: the airdrop landing of major assets (LRT and Ethena); and the continuous decline in the prices of major project tokens. The landing of airdrops has reduced speculative demand. Although the points program will continue for multiple periods, combined with the declining token prices, market confidence and expectations for the project have significantly decreased, leading to a reduction in users choosing to deposit, and related trading volumes have also shrunk significantly. Currently, Pendle's TVL and trading volume have both seen a significant decline, and the same predicament is reflected in the token price.

4 Data Analysis: TVL and Trading Volume as Pendle's KPIs

This article believes that the business data surrounding Pendle can be mainly divided into two parts: stock and flow. Stock is primarily represented by TVL, and it is also necessary to closely monitor indicators that affect the health and sustainability of TVL, such as the composition structure of TVL, the maturity dates of asset pools, and the rollover ratio; flow is mainly represented by trading volume, including trading volume, trading fees, and the composition of trading volume. Changes in trading volume will directly impact token empowerment.

4.1 TVL and Related Indicators

The TVL denominated in ETH rapidly increased after mid-January 2024 and maintained a high correlation with the price of PENDLE. At its peak, TVL exceeded 1.8M ETH, experiencing rapid declines on June 28 and July 25, primarily due to a large number of asset pools maturing. After maturity, the demand for reinvestment was insufficient, leading to a rapid loss of TVL. Currently, Pendle's TVL is approximately 1M ETH, nearly a 50% drop from its peak, and the downward trend has not been effectively alleviated.

Specifically, on June 27, 2024, multiple LRT asset pools, including eETH from Ether.Fi, ezETH from Renzo, pufETH from Puffer, rsETH from Kelp, and rswETH from Swell, matured, and users redeemed their principal investments. Although there are still asset pools with other maturity dates, the rollover ratio among users is low, and TVL has shown no signs of recovery, which corroborates the earlier analysis that as LRT projects launched their tokens and token prices declined, users' demand for further participation in related asset management and investment has decreased. In this cycle, the lack of innovation in the Ethereum ecosystem and the market's pessimism towards ETH prices mean that if the market's investment demand for ETH weakens, it will directly impact Pendle's business revenue levels. Therefore, Pendle is strongly bound to Ethereum.

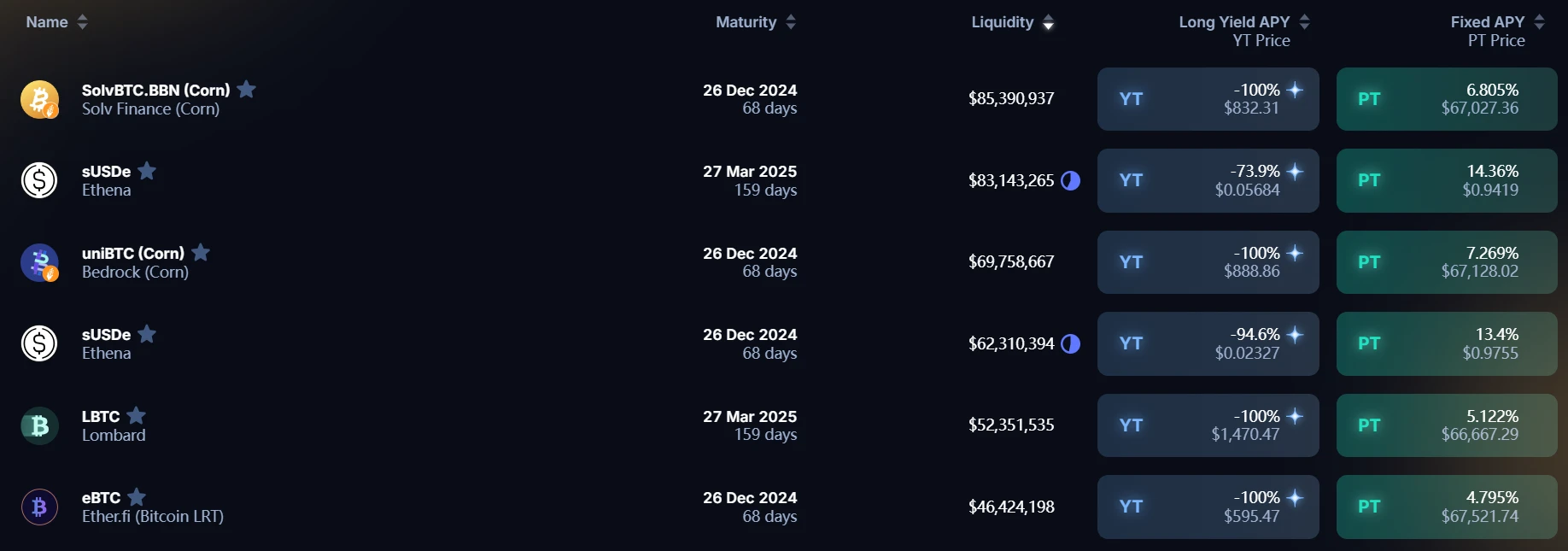

In terms of Pendle's TVL composition, the total TVL is $2.43B, with 11 asset pools having a TVL exceeding $10M. The pool with the highest TVL is SolvBTC.BBN, accounting for approximately 3.51% of the total TVL. The structure of the TVL composition is relatively healthy, with no single asset pool dominating a large portion of the TVL. Regarding the maturity of asset pools, the next significant maturity date will be December 26, 2024, and Pendle's TVL may exhibit a relatively stable trend in the near term.

After the wave of Ethereum re-staking ended, Pendle smoothly transitioned to stablecoin assets like BTCfi and USDe/USD0. Although business data and market sentiment are not as strong as in April, the TVL data has been maintained without significant declines. However, with the launch of tokens from various Ethereum LRT protocols and the entry of EIGEN into trading, the imagination for the re-staking track is diminishing, which has also compressed speculative enthusiasm for the BTC staking track, reflected in the decline of Pendle's trading volume. The next potential event that may impact Pendle could be the launch of Babylon and the BTC staking track. After the end of BTC re-staking, can Pendle find new application scenarios?

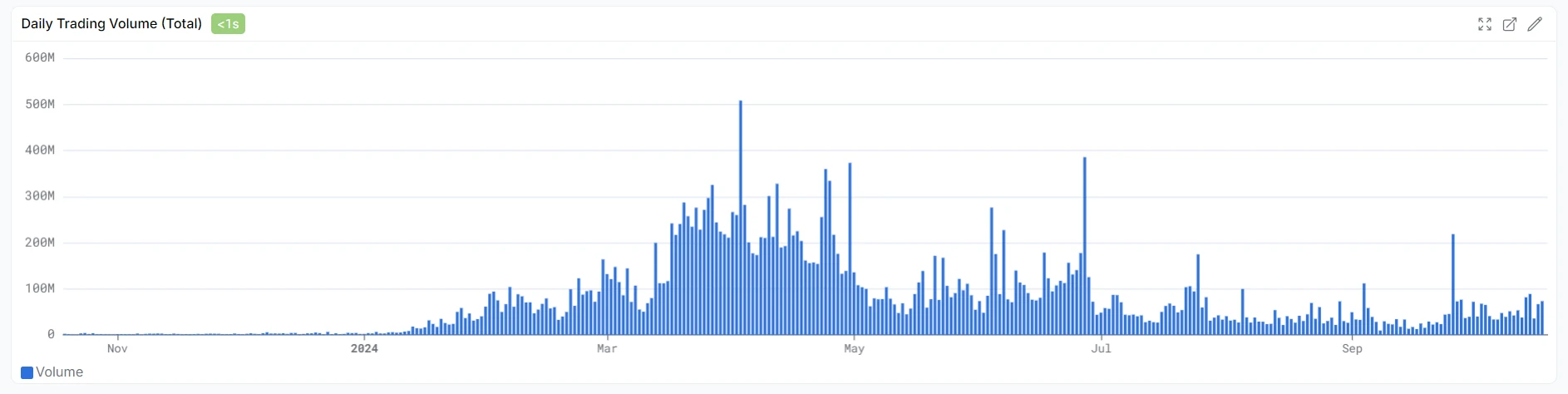

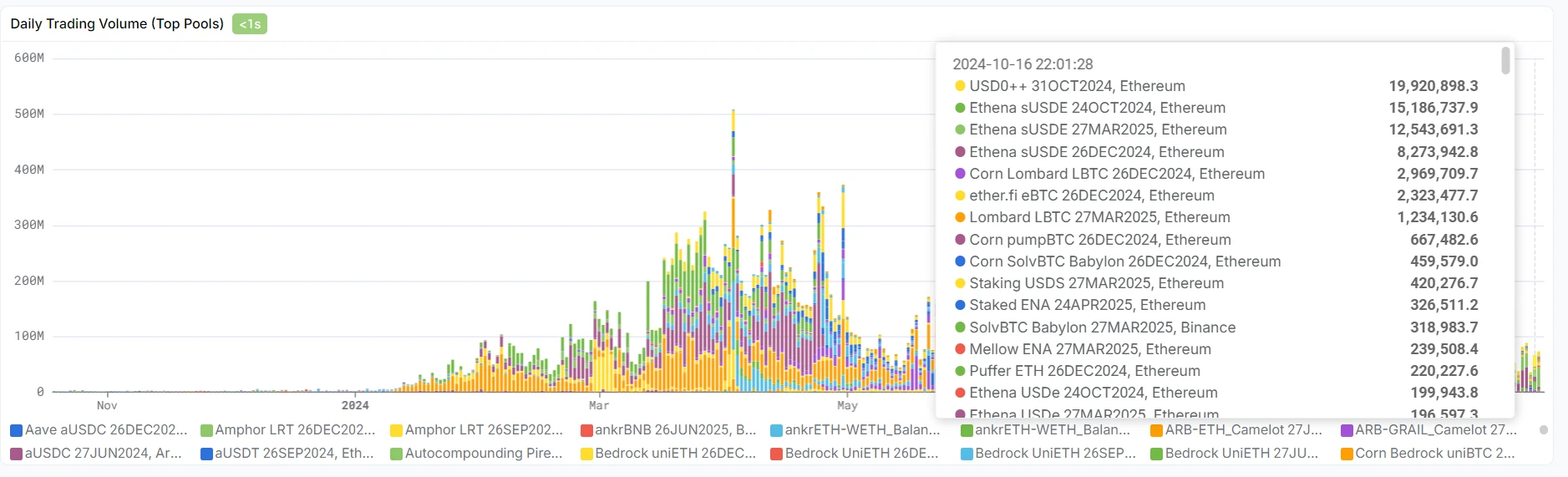

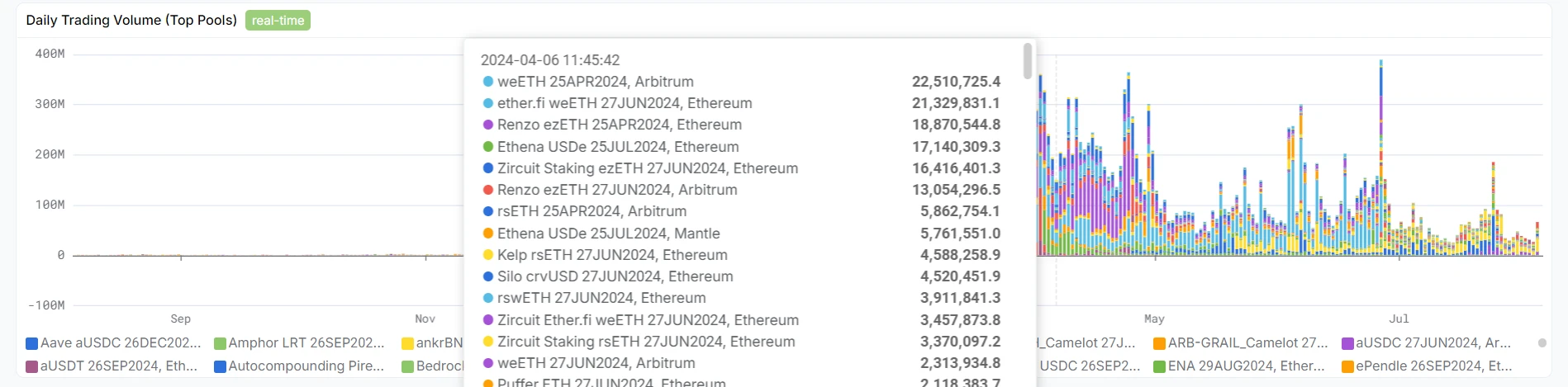

4.2 Trading Volume and Composition

The trading volume of Pendle AMM also rapidly increased after January 2024, peaking around April. After Eigenlayer announced its token launch at the end of April, accompanied by the realization of airdrop expectations for LRT projects like Ether.fi, trading volume saw a significant decline, and it has further decreased, reaching a low level since 2024.

In terms of the composition of trading volume, in the first half of 2024, trading volume was mainly composed of transactions related to Renzo and Ether.fi assets. Currently, Pendle AMM's trading volume primarily comes from the Ethena and USD0 protocols, with trading volume from BTCfi assets being relatively limited. Trading volume directly affects trading fees and the annualized returns for vePENDLE holders, making it a more direct transmission factor compared to TVL.

4.3 Token Locking Ratio

The token locking ratio directly affects the supply and demand relationship of the token. With a relatively stable daily release of tokens, the more PENDLE that is locked as vePENDLE, the more positive the stimulus effect on the token price. Changes in the amount of PENDLE locked show a similar trend to changes in business data and token prices. Since November 2023, the amount of PENDLE locked has started to rise rapidly, increasing from 38M to a peak of 55M. After reaching 54M in April 2024, the growth rate of PENDLE locked began to slow down, and there was even a net outflow of vePENDLE. This aligns with the earlier analysis of the business— as TVL and trading volume decrease, the yield for vePENDLE starts to decline, leading to a decrease in the attractiveness of locking PENDLE. Currently, there has not been a significant outflow of vePENDLE, partly due to the restrictions of the locking period, which causes this indicator to lag compared to TVL, trading volume, and token price, making it unable to show significant changes in the short term. On the other hand, top asset pools still have decent yields, which mitigates the outflow of vePENDLE. However, it should be noted that both business data and the growth data of vePENDLE reflect that Pendle is facing short-term operational pain. Pendle has yet to find new growth points after the cooling of re-staking and points to continue its previous legend.

5 Conclusion: Pendle urgently needs to find new scenarios after re-staking

Based on the analysis above, Pendle's success lies in accurately identifying PMF. More importantly, business revenue directly empowers the token, finding a direct factor for transmitting token price—packaging YT products as points trading targets, increasing AMM trading volume, and enhancing vePENDLE income.

Since starting to decline from $7.5, Pendle has not reversed its downward trend. It cannot be denied that Pendle is a great DeFi product, combining both wealth management and speculative attributes, meeting the needs of investors with different risk preferences. However, after the decline of Ethereum-based TVL, there are no signs of recovery. The poor performance of re-staking projects and Ethena has lowered market expectations for subsequent airdrops, leading to a decrease in demand for Pendle's usage. Consequently, the price of PENDLE is also searching for a new position. Pendle needs to find new product packaging or expand into new ecosystems like Solana to increase its TVL and trading volume, which may allow it to find new growth opportunities.

Another positioning for Pendle is Ethereum Beta, but it is currently undergoing a transformation: During the Ethereum re-staking era, Pendle was an important wealth management product for Ethereum and derivative assets. Even Ethena, while a stablecoin, has its USDe staking yield directly related to ETH's funding rate. If the market temporarily loses information about the Ethereum ecosystem and ETH struggles to rise, Pendle will also be powerless to change its fate. It is also important to note that Pendle differs from MEME-type Ethereum Betas like PEPE; the price of ETH has a direct transmission effect on the price of PENDLE: ETH struggles to rise → Demand for ETH-based wealth management decreases / Re-staking track performance cools → Decreased demand for Pendle usage → Decreased business revenue for Pendle → Decreased price of PENDLE. However, on Pendle, Bitcoin staking assets have already replaced Ethereum, which may weaken this transmission effect.

Finally, this article provides key points to focus on regarding the fundamentals:

Pay attention to the progress of the points programs for LRT projects and stablecoin projects like Ethena and USD0. The end of the points season may again reduce Pendle's business revenue.

Monitor changes in Pendle's TVL and trading volume. If multiple asset pools mature again, it may lead to a significant drop in TVL, at which point it may be wise to sell part of the PENDLE position in advance to hedge.

Continuously follow Pendle's product developments, including but not limited to: the launch of Pendle V3; the introduction of new asset pools and trading strategies; and the possibility of expanding into new public chain ecosystems.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。