PayFi's core advantage in realizing its vision lies in leveraging Solana's high performance to break down the barriers between the real world and blockchain, while regulation and scalability pose the greatest challenges to widespread application.

Author: YBB Capital Researcher Ac-Core

TL;DR

● The concept of PayFi was introduced by Lily Liu, Chair of the Solana Foundation, during her keynote speech "The Emergence of PayFi: Realizing the Vision of Cryptocurrency" at the 7th EthCC conference;

● The core concepts of PayFi: 1. Emphasizes "instant settlement," which holds significant value, especially in speculative trading; 2. Supports a new model of "Buy Now, Pay Never," providing new pathways for creators to monetize, invoice financing, and manage payment risks;

● The core advantage of realizing PayFi's vision lies in leveraging Solana's high performance to break down the barriers between the real world and blockchain, while regulation and scalability are the biggest challenges to widespread application;

● Lily Liu provided a profound explanation of PayFi: "PayFi creates new financial markets around the time value of money. On-chain finance can achieve new financial primitives and product experiences that traditional finance and even Web2 finance cannot."

1. What is PayFi?

Image source: 7th EthCC conference

PayFi, short for Payment Finance, is an innovative paradigm that integrates payment and finance, proposed by Lily Liu, Chair of the Solana Foundation, at the EthCC conference in July 2024. Its core lies in emphasizing "instant transactions" to enhance the efficiency of speculative trading and various financial operations. According to the definition by Lily Liu, PayFi is a programmable financial structure that conducts new financial innovations on top of the settlement layer while autonomously handling payment transactions. The following summarizes the content based on Elponcho:

The Vision of PayFi

To "establish a programmable currency system within an open financial system that provides users with economic sovereignty and self-custody capabilities."

Application Scenarios of PayFi

New technologies give rise to new markets. PayFi supports the "Buy Now, Pay Never" model, utilizing on-chain finance and instant settlement capabilities to ensure that profits generated on-chain can meet immediate consumption needs in real-time. For example, a user can invest $50 on-chain to earn interest, and the instant settlement and payment of that interest can be used to buy a "free" cup of coffee.

Additionally, PayFi can support monetization based on the completion progress of creative work (e.g., a YouTuber gradually receiving ad revenue as they reach 1 million views), provide invoice financing, manage payment processing risks, and develop a global private credit pool on the Solana chain. Lily Liu believes that PayFi will surpass DeFi in the future, leading new financial trends.

Solana and PayFi

Lily Liu believes that Solana stands out in the blockchain space due to its high performance, consistently demonstrating fast transaction speeds and low costs, and holding advantages in the liquidity of capital and talent. Clearly, Solana is a strong candidate for realizing the vision of PayFi.

Three Key Elements for PayFi's Success in Blockchain

Lily Liu identifies three key factors for success in blockchain: fast and low-cost transactions, a broad user base, and a strong developer community. She stated that currently, Solana is the only ecosystem that fully possesses these three elements.

The Future of PayFi and Solana

At the end of her speech, Lily Liu shared various financial application scenarios on the Solana platform, such as supply chain finance, payday loans, credit cards, corporate credit, interbank repurchase markets, and insurance markets. These applications demonstrate the immense potential of combining Solana with PayFi to change the traditional financial system in the future.

In the article "Understanding PayFi: Solana's Next New Narrative," Lily Liu stated that the core of PayFi lies in the time value of money, illustrated by three important cases:

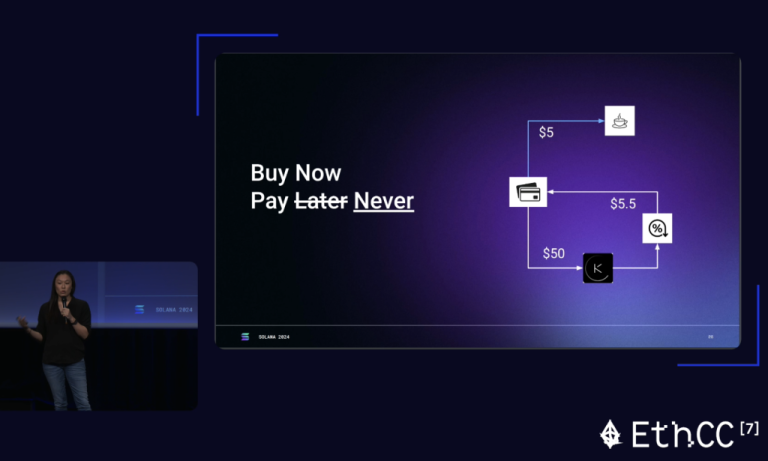

● Buy Now, Pay Never: Most people are familiar with "Buy Now, Pay Later," but "Buy Now, Pay Never" is almost the opposite. The former optimizes cash flow through installment payments, incurring some interest costs, while the latter involves investing funds in DeFi products to earn interest, which is then used to pay for consumption. Although this sacrifices cash flow, it does not require touching the principal.

For example, a user purchases a $5 coffee and can deposit $50 into a lending product. When the interest accumulates to $5, they can use that interest to pay for the coffee, and once the funds are unlocked, they return to the user's account. This process relies on the automated execution of "programmable money."

● Monetization for Creators: Many creators face cash flow issues during content creation, as it requires time and investment, while returns often lag. This period can lead to funding shortages, affecting the pace of creation. In Lily Liu's vision, PayFi can help creators accelerate monetization. For instance, if a video's expected revenue is $10,000 but it takes a month to receive, the creator can use PayFi to immediately obtain $9,000 in cash, realizing income early, even though they sacrifice some earnings, thus improving cash flow.

● Accounts Receivable: This refers to the common financial relationship between businesses and customers, indicating the amounts owed by customers to businesses. Due to accounts receivable, businesses sometimes face cash flow shortages. To address this, businesses typically mortgage accounts receivable to financing companies or sell them at a discount to obtain immediate funds and maintain stable cash flow. PayFi aims to further simplify and optimize this process. By accelerating settlement through blockchain, it improves capital turnover efficiency and lowers barriers, allowing more businesses to utilize this supply chain finance tool to accelerate capital flow.

2. How PayFi Connects to DeFi, with RWA as the Bridge to a New Narrative

Image source: Coincu

The origin of blockchain technology can be traced back to Satoshi Nakamoto's revolutionary white paper "Bitcoin: A Peer-to-Peer Electronic Cash System," published in 2008, which laid the foundation for a new era of decentralized payments, creating not only a new form of currency but also fundamentally changing the entrenched payment systems in traditional finance. PayFi utilizes blockchain technology and smart contracts to manage the flow of funds through digital assets and decentralized finance (DeFi) tools. Its core idea is to optimize the time value of funds and shorten settlement times through decentralized technology. The main operational principles include:

● Time Value of Money (TVM): PayFi emphasizes enhancing the time value of funds, helping users improve the efficiency of fund utilization. For example, users can deposit funds into a lending platform and use the generated interest to cover daily expenses. For instance, when a user buys a $5 coffee, they can lock in $50 of funds, and when the interest is sufficient to cover the coffee cost, the principal does not need to be touched;

● Smart Contract Automation: Smart contracts are central to PayFi, capable of automatically executing complex financial operations based on predetermined conditions, thereby reducing intermediary involvement, accelerating transactions, and lowering costs;

● Tokenization of Real-World Assets (RWA): PayFi tokenizes real-world assets such as real estate and accounts receivable, facilitating cross-border payments and capital flow. This not only enhances the liquidity of physical assets but also provides a new platform for global transactions.

As the demand for sustainable value assets in the crypto ecosystem rises, RWA may naturally become a popular option. In the past two years, tokenized treasury bonds with yields of 4-5% have become the preferred choice for on-chain capital, with the total value rapidly increasing to $2 billion. With the emergence of inflation and signals of central bank interest rate cuts, treasury bond yields are declining, prompting capital to seek other high-yield, low-risk assets. This presents an opportunity for PayFi's rise in the RWA sector.

Typical PayFi Scenarios May Include

Cross-Border Payment Financing: Arf is changing the traditional cross-border payment model by providing on-chain liquidity solutions for financial institutions, supporting 24/7 instant, transparent, and low-cost USDC-based settlements, eliminating the need for global pre-funded accounts. Cross-border payment financing offers high capital efficiency and scalability;

Digital Asset-Backed Corporate Cards: Rain provides Web3 teams with corporate card settlement liquidity backed by USDC. Companies pledge funds into a vault, set credit limits, and automatically repay corporate card balances through on-chain settlement of assets at the end of each settlement cycle, reshaping expense management;

Trade Financing: BSOS combines enterprise resource planning (ERP) platforms with on-chain liquidity to create real-world assets (RWA) in the supply chain, offering shorter-term financing options to meet corporate funding needs.

Real-World Assets (RWA) May Include

Instant RWA Settlement: Even highly liquid assets (such as treasury bonds or tokenized funds) typically require 2-4 days for settlement, as the underlying assets need to be cleared for redemption. However, through on-chain liquidity pools, these assets can achieve 24/7 real-time subscriptions and redemptions, ensuring transactions are fast and transparent.

DePIN Financing: With the rapid expansion of the DePIN ecosystem, many projects are based on the idea of sharing the costs of large infrastructure construction and redistributing future value. For example, TLay provides critical trust infrastructure to accelerate DePIN adoption; Peaq has customized L1 for DePIN and offers functionalities that enable machines to trade efficiently with each other or interact with humans, supporting the development of the machine economy.

At the same time, the birth of stablecoins has become a bridge connecting fiat currency and blockchain, driving the emergence of the first wave of real payment scenarios. Since 2014, stablecoins have experienced exponential growth, proving the increasing demand for blockchain innovation in the payment sector. Today, stablecoins support approximately $20 billion in organic payments annually, nearing Visa's annual payment processing volume. Although the crypto ecosystem is continuously overcoming challenges such as poor user experience, significant delays, high transaction costs, and compliance issues to unleash the unlimited potential of stablecoins, there is still room for further development. Looking back at the history of payment systems, financing mechanisms have played a crucial role in driving their development. For example:

● Credit Cards: Contributing $16 trillion annually to merchant payments, demonstrating how financing drives widespread adoption and practicality;

● Trade Financing: Providing $10 trillion annually in funding support for B2B payments, emphasizing the critical role of financing in global commerce;

● Cross-Border Payments: Supporting global remittances and settlements through pre-funded capital of $4 trillion. Today, 1 in 6 households globally relies on remittances for their livelihood.

Without payment financing, global liquidity would be significantly constrained. Similarly, without financing mechanisms, the utility and adoption of internet-native currencies would also be hindered. PayFi was born to address these limitations. Lily Liu, Chair of the Solana Foundation, proposed the concept of "PayFi," clearly articulating its vision: "PayFi is a new financial market created around the time value of money, where on-chain finance can achieve new financial primitives and experiences that traditional finance and even Web2 finance cannot provide."

3. Thoughts on PayFi

Image source: Solana official website

In terms of the hype capability of the crypto market, Solana has always been at the forefront, with various narratives continuously stimulating the activity of the speculative market. The new narrative of PayFi has its greatest advantage in returning to the inherent disruptive innovation of blockchain in traditional finance. By leveraging the attributes of decentralization and security, it reduces fraud risks and enhances transaction integrity, eliminating intermediary institutions in traditional financial payment processing and compiling the entire transaction process on-chain. This overall reduces the barriers for users to participate in finance, while from a narrative perspective, PayFi becomes the bridge linking RWA and DeFi to the real world.

Although PayFi has the potential to support large-scale applications of blockchain in the future, it still faces some challenges that may limit its widespread adoption. Foremost among these is regulatory issues; currently, global financial institutions have not fully understood or established legal frameworks regarding blockchain operations, and the first threshold for connecting to the real world is legality. Another obstacle is scalability; blockchain networks may experience congestion during peak times, affecting transaction speed and costs, and the block generation speed between different chains is difficult to coordinate. Market acceptance may be lacking; currently, enterprises and users have a relatively low acceptance of new technologies, and there is still a "fear of discussing cryptocurrencies" mentality when blockchain is mentioned. For blockchain to thoroughly open up pathways to the real world, it must continuously optimize its ability to reach more fields, and the effectiveness of breaking through barriers still requires ongoing improvement.

References:

1: PayFi: The Frontier of Blockchain Payment Finance

2: Understanding PayFi: Solana's Next New Narrative

3: PayFi - The New Frontier of RWA

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。