Author: Snow

Translator: Paine

Reviewers: KOWEI, Wayne, Elisa, Ashley, Joyce

Report Highlights

Restaking is a mechanism that enhances yield by releasing liquidity and increasing leverage, primarily based on Ethereum's security framework. While it can provide additional returns for stakers and improve capital efficiency, it also introduces a range of risks, including slashing, liquidity, centralization, contract, and smart contract risks. EigenLayer is a pioneer in this field, but with the emergence of more competitors such as Symbiotic, Karak Network, Babylon, BounceBit, and Solayer, market funds are becoming fragmented, and more challenges may arise in the future. Users should carefully consider the risks and rewards of participating in restaking protocols and implement appropriate contract monitoring to ensure asset security.

Background

Staking and Liquid Staking

Ethereum staking refers to users locking their ETH in the Ethereum network to support its operation and security. In Ethereum 2.0, this staking mechanism is part of the Proof of Stake (PoS) consensus algorithm, replacing the previous Proof of Work (PoW) mechanism. Stakers become validators by staking ETH, participating in block creation and confirmation, and in return, they can earn staking rewards.

The emergence of Liquid Staking Derivatives (LSD) aims to address the liquidity issues in traditional staking. It allows users to receive liquidity tokens (such as Lido's stETH or Rocket Pool's rETH) that represent their staked shares while staking tokens. These liquidity tokens can be traded, lent, or used for other financial activities on other platforms, enabling participation in staking for rewards while maintaining capital flexibility.

Breakdown of Trust Networks

The Bitcoin network introduced the concept of decentralized trust from its inception, designed as a peer-to-peer digital currency system based on UTXO and scripting language. However, its ability to build various applications on the network is limited. Later, Ethereum allowed developers to build permissionless decentralized applications (DApps) on its consensus layer through a highly programmable virtual machine (EVM) and modular blockchain concepts, providing trust and security for all DApps built on it. However, many protocols or middleware have not fully leveraged Ethereum's trust network.

For example, Rollup enhances Ethereum's performance by separating transaction execution from the EVM and only returning to Ethereum at the time of transaction settlement. However, these transactions are not deployed and verified on the EVM, so they cannot fully rely on Ethereum's trust network. Besides Rollup, other systems based on new consensus protocols, such as sidechains, data availability layers, new virtual machines, oracles, and cross-chain bridges, face similar challenges and need to establish their own trust layers to ensure security and prevent malicious behavior, known as Active Verification Services (AVS).

Liquidity Fragmentation

As the largest Proof of Stake (PoS) blockchain, many projects rely on staking to ensure their security, such as cross-chain bridges, oracles, data availability layers, and zero-knowledge proofs. Therefore, whenever a new project launches, users must lock a certain amount of funds, leading to competition among different projects for limited capital pools. As the staking yields offered by different projects continue to rise, the risks borne by the projects themselves also increase, creating a vicious cycle. On the other hand, users can only stake limited funds in limited projects, resulting in limited returns and low capital utilization. With the increase in public chains, applications, and various projects, liquidity becomes increasingly fragmented.

Market Demand for Staking Services

With the approval of Bitcoin spot ETFs and the successful upgrade of Ethereum in Cancun, Ethereum has regained new vitality. As of July 15, 2024, over $111 billion worth of Ether (ETH) has been staked, accounting for 28% of the total supply. The amount of staked ETH is referred to as Ethereum's "security budget," as these assets are subject to network penalties in the event of double-spending attacks and other violations of protocol rules. Users staking ETH contribute to enhancing Ethereum's security and earn rewards through protocol issuance, priority hints, and MEV. Users can easily stake ETH through liquid staking pools without sacrificing asset liquidity, leading to an increasing demand for staking.

In this context, the market's demand for shared security has emerged, necessitating a platform that can utilize users' staked assets for the security of multiple projects, which is the background for the emergence of restaking.

What is Restaking

Today, the modular expansion of blockchains has led to the birth of many new protocols and supporting middleware. However, each network needs to establish its own security mechanism, often using a variant of the Proof of Stake (PoS) consensus, but this approach results in each security pool becoming isolated entities.

Restaking is the process of utilizing the economic and computational resources of one blockchain to secure multiple blockchains. In PoS blockchains, restaking allows the staking weight and validator set of one chain to be used on any number of other chains. This involves using liquid staking tokens already staked on Ethereum for validators on other blockchains to restake, earning more rewards while enhancing the security and decentralization of the new network. The result is a more unified and efficient security system that can be shared across multiple blockchain ecosystems. This concept extends Ethereum's existing economic trust to protect other distributed systems, such as oracles, bridges, or sidechains.

The concept of restaking has existed in the industry for many years, with the Polkadot ecosystem attempting this concept in 2020. Cosmos launched a restaking model called "shared security" in May 2023; in June of the same year, Ethereum introduced a similar model through EigenLayer. The primary value of restaking protocols comes from the staked funds locked in Ethereum, making Ethereum, as a PoS blockchain, economically the most secure.

An important distinction between the restaking mechanism and liquid staking is that while both mechanisms can help ETH already staked on Ethereum earn more rewards, the restaking mechanism fully inherits the trust consensus of the staking mechanism and extends it, allowing validators to make credible commitments for more applications, infrastructure, or distributed networks, thereby enhancing the overall economic security of the Ethereum ecosystem.

How Restaking Works

The core of restaking is to use liquid staking token assets for staking with validators on other blockchains, earning more rewards while establishing a shared security pool to enhance the security and decentralization of the new network. Specifically, liquid staking tokens (LST) represent the tokenized form of staked ETH and accumulated rewards, while liquid restaked tokens (LRT) represent the tokenized form of restaked ETH and accumulated rewards. Restaking is built on Ethereum's security framework and aims to optimize the efficiency of capital utilization in the cryptocurrency ecosystem. Stakers can not only support the security of one network but also provide validation services for multiple networks, thereby earning additional rewards.

The main issue facing restaking remains liquidity. Similar to PoS staking, assets after restaking are locked in nodes, leading to limited liquidity. To address this issue, Liquid Restaked Tokens (LRT) have been introduced. LRT is a synthetic token issued for restaked ETH or other LST, used by multiple Active Verification Services (AVS) to ensure the security of applications and networks and distribute various types of additional rewards. It allows staked assets to provide security support across multiple services while bringing additional rewards and returns to stakers. Therefore, although there are some detailed risks in the restaking process, it brings significant liquidity and yield to stakers and DeFi.

Track Analysis

Competitive Projects

EigenLayer

EigenLayer is the leader in the restaking field, and there are currently no large-scale direct competitors. As an innovative concept, there are relatively few direct competitors in the market. However, EigenLayer may face the following potential competition and challenges:

Other LSD protocols may develop their own restaking features, such as Lido Finance and Rocket Pool.

Other data availability and governance service protocols may develop their own LSD features, such as The Graph and Aragon.

Other Layer 2 or cross-chain protocols may develop their own security and trust networks, such as Polygon and Cosmos.

Since EigenLayer primarily uses LSD as collateral, LSDFi projects in the market may also compete for LSD market share.

Karak Network

Karak Network operates similarly to the EigenLayer protocol, but its AVS service is called Distributed Security Service (DSS), and it has launched its own Layer 2 network, K2. Unlike EigenLayer, Karak aims to support the restaking of any asset, currently supporting restaking assets on its platform, including ETH, various LSTs, LRT assets, and stablecoins such as USDT, USDC, DAI, and USDe. Additionally, Karak has been deployed on Ethereum, Arbitrum, BSC, Blast, and Mantle, allowing users to choose restaking based on their asset distribution.

Babylon

Babylon is a restaking protocol based on Bitcoin, introducing staking functionality for Bitcoin, allowing BTC holders to stake their assets trustlessly into other protocols or services that require security and trust, earning PoS staking rewards and governance rights. Babylon covers two aspects: first, BTC holders can stake BTC to provide security and credibility for other protocols and earn rewards; second, new protocols in the PoS chain or Bitcoin ecosystem can utilize BTC stakers as validation nodes to enhance security and efficiency.

Solayer

Solayer is a restaking protocol within the Solana ecosystem that allows SOL holders to stake their assets into protocols or DApp services within the Solana ecosystem that require security and trust, in order to earn more PoS staking rewards. Solayer has completed a builder round of financing, with investors including Solana Labs co-founder Anatoly Yakovenko, Solend founder Rooter, Tensor co-founder Richard Wu, and Polygon co-founder Sandeep Nailwal. Solayer supports users depositing native SOL, mSOL, JitoSOL, and other assets. As of July 15, 2024, the total value locked (TVL) on the Solayer platform exceeds $105 million, with SOL accounting for approximately 60%.

Picasso

Picasso is a general-purpose restaking blockchain built on the Cosmos SDK. It connects to underlying chains through the IBC protocol and handles the details of deposited assets, then allocates funds to AVS. Picasso's restaking solution is similar to EigenLayer, which allows a subset of the network to join in protecting AVS weight. This architecture has been replicated across multiple underlying chains and unified under Picasso. The node operators of Picasso are elected through a governance mechanism. Currently, Picasso's restaking layer only accepts assets deposited from Solana via SOL LST and native SOL as restaking collateral. Picasso's roadmap plans to expand to Cosmos chains and other assets after launching AVS on Solana. Currently, the restaking products supported on Picasso include LST assets such as SOL, JitoSOL, mSOL, and bSOL.

Universal Restaking Protocol

Universal restaking is a system that can concentrate native assets from multiple chains for restaking. This approach is agnostic to specific assets and underlying chains, allowing for the concentration of many staked assets across multiple chains. Universal restaking relies on an additional layer located between the economic security source chain and AVS, or a series of contracts across multiple blockchains.

Overview

The restaking field is currently developing rapidly. While EigenLayer is a pioneer in this area, an increasing number of competitors and innovators are joining, continuously expanding the application scenarios and technical boundaries of restaking. Restaking not only brings new revenue models but also promotes advancements in the security and liquidity of the blockchain ecosystem.

Market Size

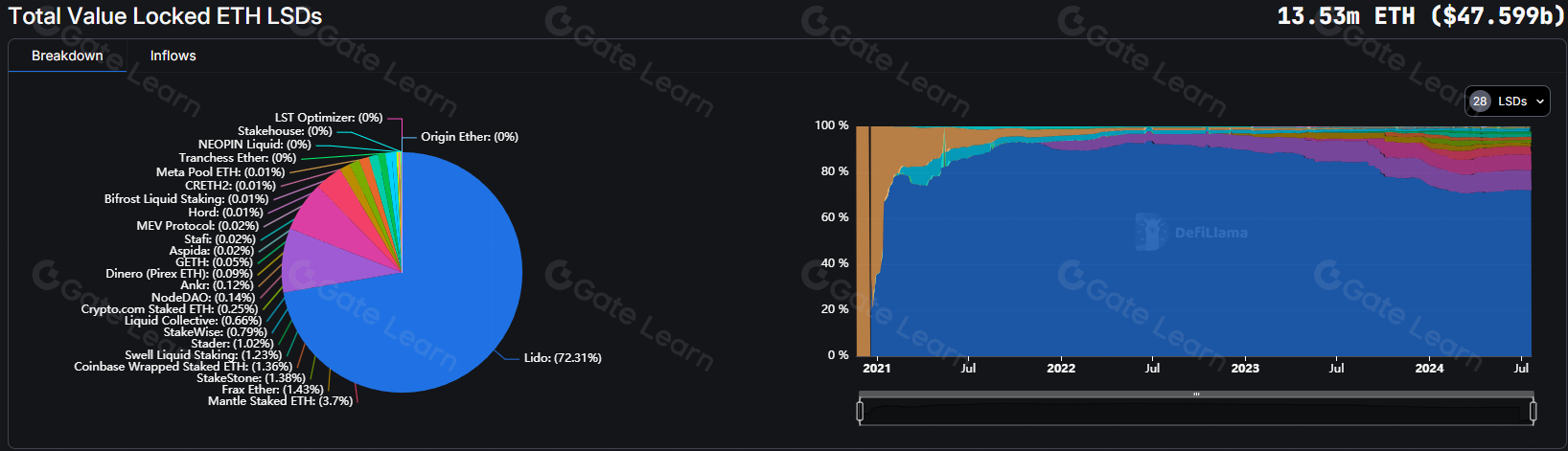

According to data from DeFiLlama, as of July 21, 2024, the total value locked in the global ETH liquid staking market is $47.599 billion. Lido is the largest participant, accounting for as much as 72.31% of the locked value. Lido provides a liquid staking solution that allows users to stake ETH into the Ethereum 2.0 network and receive equivalent stETH tokens, which can be used in the DeFi market or restaked. Major restaking protocols include EigenLayer and Tenet.

Source: https://defillama.com/lsd

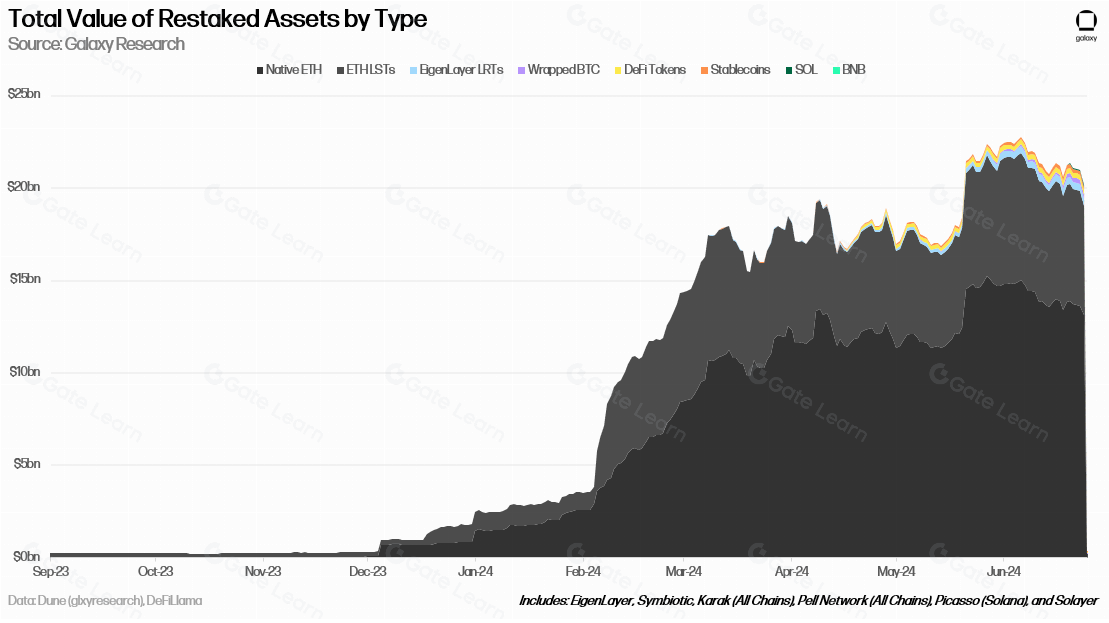

As of June 25, 2024, the total locked value of assets in the global restaking market reached $20.14 billion. Currently, most restaking protocols are deployed on the Ethereum chain, with a total locked amount of ETH and derivative assets reaching $19.4 billion; additionally, restaking protocols on the Solana chain, such as Picasso and Solayer, have staked assets worth $58.5 million; through Pell Network and Karak on various chains (including Bitlayer, Merlin, and BSC), $223.3 million of BTC has been restaked.

The chart below shows the total locked value of leading restaking solutions (EigenLayer, Karak, Symbiotic, Solayer, Picasso, and Pell Network) calculated by total locked value. Overall, the total amount of restaked assets exceeds $20 billion, with most coming from locally restaked ETH and ETH LST. The top three categories of restaked assets are centered around ETH based on TVL.

Source: https://x.com/ZackPokorny_

Core Competitive Factors

Asset Scale

Asset scale refers to the total amount staked on the staking platform. A high-quality staking platform should have a large scale of assets to demonstrate its stability and credibility. For example, EigenLayer currently has staked 5,842,593 Ethereum, with a total TVL exceeding $18 billion, making it the largest protocol in the restaking field.

Source: https://dune.com/hahahash/eigenlayer

Yield

- Restaking projects should offer higher yields than single staking to attract user participation. To achieve this, it is necessary to optimize staking strategies, allocate income and rewards reasonably, and utilize compounding effects to enhance users' capital efficiency and return rates. For instance, Eigenlayer's proposed restaking solution allows liquidity tokens to earn rewards not only from staking Ethereum but also from other cross-chain bridges, oracles, and LP staking.

- Staking Ethereum rewards, such as those obtained through liquid staking protocols like Lido that yield stETH;

- Token rewards from nodes built and validated by partner projects;

- LP rewards from staking liquidity tokens in DeFi.

Liquidity

Restaking projects need to address the liquidity issue of staked assets, allowing users to easily join or exit staking, or transfer assets to other protocols or platforms. Therefore, services such as liquid staking tokens, liquidity mining, and lending markets need to be provided to enhance users' liquidity and flexibility.

Security

Protecting user asset security is the primary goal of staking projects. Restaking projects must ensure that user assets are not compromised due to smart contract vulnerabilities, validator misconduct, or hacker attacks. Therefore, high levels of security measures and risk management mechanisms are essential, such as multi-signature, firewalls, insurance, and penalty mechanisms. For example, EigenLayer becomes a validation node by staking Ethereum-related assets and borrows security from the mainnet through a slashing mechanism.

Ecosystem

Restaking projects need to build a robust ecosystem that supports validation services for multiple PoS networks and protocols, thereby enhancing the security and decentralization of the network and providing users with more choices and opportunities. To achieve this goal, collaboration and integration with other blockchain platforms, DeFi applications, and Layer 2 protocols are necessary.

What Risks Does Restaking Bring?

Slashing Risk

In Ethereum's staking mechanism, as well as in restaking protocols, there is a 50% slashing risk. This means that users' funds may face the risk of being slashed, although this risk is distributed across multiple nodes.

Liquidity Risk

Many restaking protocols lock a large amount of liquid restaking tokens (LST). If most LST is locked in restaking pools, it may lead to increased volatility of LST relative to ETH prices. This situation increases users' risk exposure, as the security of AVS is directly related to the liquidity of LST. When a certain type of LST is overly concentrated in AVS, liquidity risk further escalates.

Centralization Risk

Centralization risk may lead to DAO hacking attacks. For example, if one-third of ETH is concentrated in a single AVS, exceeding the traditional Byzantine fault tolerance security threshold, that portion of ETH may be slashed for failing to submit fraud proofs rather than due to technical issues like double-signing. Centralization risk means increased coupling within the system, raising the overall vulnerability of the system.

Contract Risk

Participating in restaking requires interaction with the project's contracts, so users bear the risk of contracts being attacked. Project funds are ultimately stored in contracts of protocols like EigenLayer, and if that contract is attacked, users' funds will also suffer losses.

LST Risk

LST tokens may become unpegged or experience value deviations due to LST contract upgrades or attacks.

Withdrawal Risk

Currently, most mainstream restaking protocols in the market, except for EigenLayer, do not support withdrawals. If the project fails to implement the corresponding withdrawal logic through contract upgrades, users will be unable to withdraw assets and can only exit through the secondary market for liquidity.

How to Mitigate These Risks?

Restaking is an emerging concept that has not undergone the necessary time-tested evaluation at either the contract or protocol level. In addition to the risks outlined above, there may be other unknown risks, making it particularly important to reduce risks.

Capital Allocation

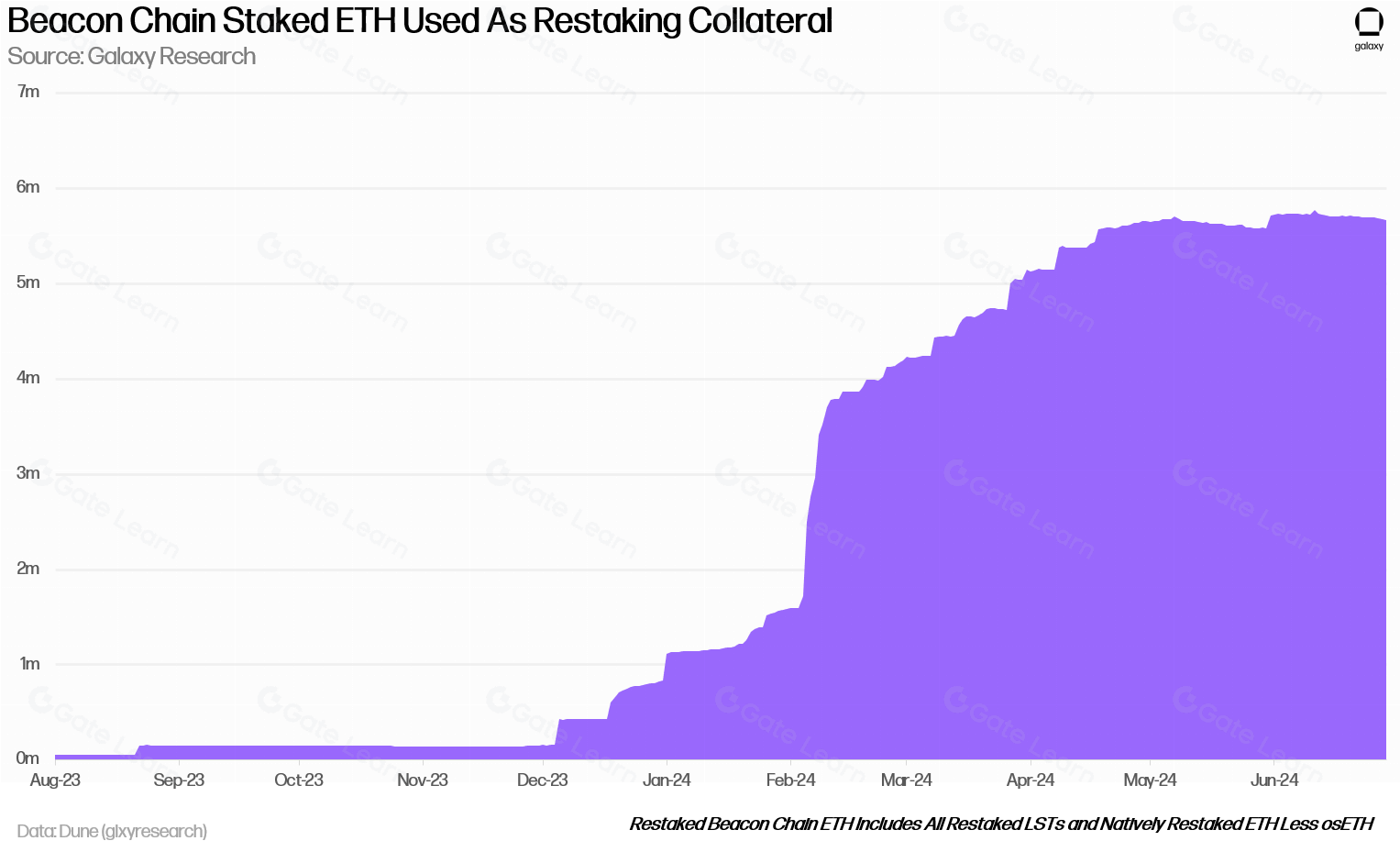

For users participating in restaking with large amounts of capital, directly participating in EigenLayer's Native ETH restaking is an ideal choice. This is because in Native ETH restaking, the ETH assets deposited by users are not stored in EigenLayer contracts but in Beacon chain contracts. Even in the worst-case scenario of a contract attack, attackers cannot immediately access users' assets.

Source: https://x.com/ZackPokorny

(Currently, 33.4 million ETH is staked on the Beacon Chain, including ETH in the entry/exit queue.)

For users who wish to participate with large amounts of capital but do not want to wait for long redemption times, a relatively safe option is to use stETH as the participating asset and invest directly in EigenLayer.

For users looking to earn additional returns, they can allocate a portion of their funds to projects built on EigenLayer, such as Puffer, KelpDAO, Eigenpie, and Renzo, according to their risk tolerance. However, it is important to note that these projects have not yet implemented the corresponding withdrawal logic, and participants should also consider withdrawal risks while paying attention to the liquidity of related LRT in the secondary market during the investment process.

Monitoring Configuration

The projects mentioned currently have the capability to upgrade contracts and pause operations, and the multi-signature wallet of the project team can execute high-risk operations. For advanced users, it is recommended to configure a corresponding contract monitoring system to monitor upgrades of relevant contracts and the execution of sensitive operations by the project team.

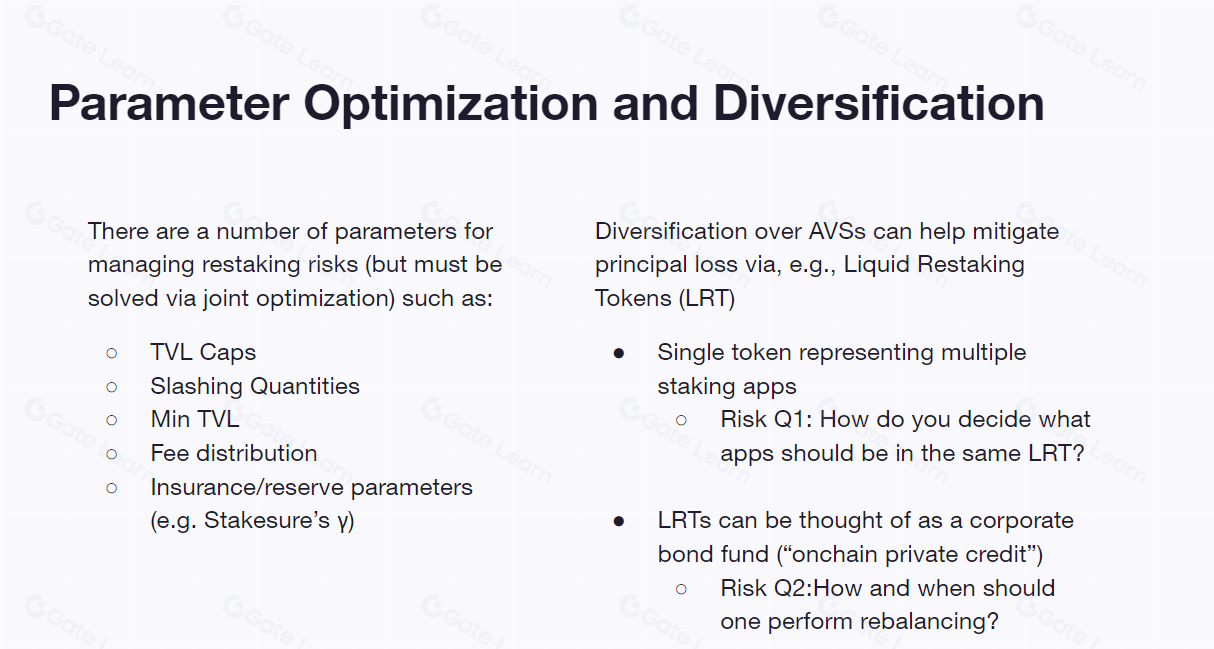

Optimizing Parameters

Optimize restaking parameters (TVL cap, reduction amount, fee distribution, minimum TVL, etc.) and ensure diversification of funds between AVS. Restaking protocols allow users to choose different risk conditions when depositing for restaking. Ideally, each user should be able to assess and choose which AVS to restake into without having to delegate this process to a DAO.

Source: https://docs.google.com/presentation/d/1iIVu6ywaCqlTwJJbbj5dX07ReSELRJlA/edit?pli=1#slide=id.p23

Challenges Faced

From the perspective of application chains, restaking applications represented by EigenLayer can meet the needs of small and medium-sized application chains to reduce node deployment costs. However, these application chains cannot fully meet their security requirements, and the sustainability of their demands is relatively weak.

From a competitive standpoint, although the restaking track has a huge amount of capital, as more restaking applications are launched, market funds will be dispersed. If the profits of restaking applications like EigenLayer decline, for example, during a bear market, will the sharp reduction in demand from application chains lead to a run on funds?

From the perspective of partners, EigenLayer initially developed 14 AVS partners. Although early AVS may be attracted by potential returns, the security risks of the restaking mechanism may affect the willingness of subsequent AVS operators to join.

From the user's perspective, users may not be able to obtain substantial Staking rewards in the short term. The uncertainty of staking yield may negatively impact the growth of the user base in the future.

Copyright belongs to Gate.io.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。