Compared to the fragmented power structure of Ethereum, the Solana ecosystem is smaller but more agile. After the collapse of FTX, Solana has risen from the ashes, relying on high performance, strong marketing, and various hardware products to successfully rebound.

Specifically, high performance refers to the Firedancer upgrade, strong marketing is represented by Meme Season, and hardware includes various Web3 phones. However, these are not enough. The PayFi concept proposed by Solana Foundation Chair Lily Liu has also become a hot topic. Although discussing the hot topics of July in October may seem outdated, from a long-term perspective, the entire Web3 industry is shifting towards off-chain and real consumption scenarios.

"A long time ago, you had me, and I had you."

This article is not a song made for Solana, but rather a melody composed for exploring the way out for Web3.

The Unresolved Dilemma of Crypto Wallets: The Prelude to PayFi

Before presenting Lily Liu's definition of PayFi, let's first discuss Web3 wallets. From 2022 to 2023, with the rise of smart contract wallets, account abstraction (AA), and the traffic anxiety of exchanges, a number of Web3 wallets have welcomed a second peak following the dog coin era of 2017-2021.

From the perspective of exchanges, wallets are the main entry point for people to interact with the blockchain, and subsequent traffic will flow in and out from there, even having the potential to replace CEXs. Furthermore, in the increasingly heated competition among Ethereum L2s, multi-chain wallets are bound to be the main battlefield for aggregating liquidity.

However, the wallet ecosystem in 2024 is not particularly impressive. OKX's built-in Web3 wallet is already a standout, but in many cases, it has not become an independent product. One important reason is that Web3 wallets have traffic but lack a closed-loop transaction mechanism, meaning wallets cannot solve the profitability issue. If they charge fees, users will simply open desktop products, as why not save on fees?

From a more "path-dependent" perspective, the problem with crypto wallets lies in the excessive pursuit of transaction characteristics. Note that this does not conflict with the aforementioned profitability issue. The core product feature of crypto wallets is to provide users with richer on-chain transaction characteristics, from connecting to more chains to having a more competitive dApp recommendation mechanism.

Moreover, users' funds are not like those in Alipay, which are stored within the crypto wallet. The non-custodial mechanism may provide peace of mind, but it does not earn users' loyalty. In short, crypto wallets have no relevance to Web2 wallets; they neither manage money nor provide financial services.

All these factors make it impossible for crypto wallets to establish their own closed-loop payment systems like PayPal or WeChat/Alipay. From a broader commercial perspective, Web3 wallets only have users, without support from the merchant side. If dApps are considered merchants, then there are only a small number of on-chain merchants.

However, wallets do have a large amount of traffic, and the gains or losses from DeFi on-chain can indeed be converted into off-chain consumption possibilities, although losses are also possible, depending on whether it is ETH-based, stablecoin-based, or fiat-based.

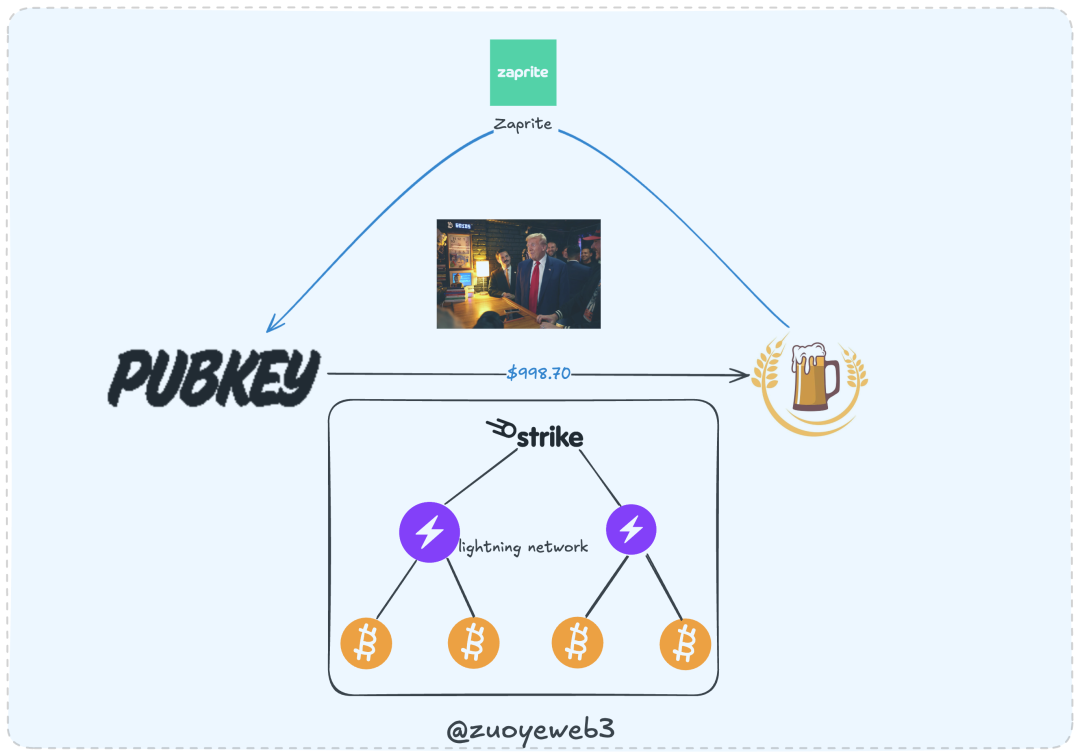

A normal payment system requires support from both the merchant side and the user side, but this is precisely the current industry's shortcoming. To illustrate this issue, we can refer to the prominent entrepreneur Chuan Bao. On September 19, 2024, Chuan Bao visited the PubKey bar in New York and bought a beer for only $998 to treat his supporters. Chuan Bao used Strike to initiate the payment, while the merchant used Zaprite to receive the payment.

In this case, the merchant and Chuan Bao did not use the same payment system, which would be hard to imagine in the Web2 era. It is akin to Chuan Bao paying with Alipay while the merchant receives payment via WeChat. However, in Web3, this makes sense because both parties use the Bitcoin network as the settlement layer. Let's outline the workflow:

- Chuan Bao initiates a payment request using Strike, which calls the Lightning Network to start the payment process. After confirmation through the Bitcoin network, the transaction is initiated.

- The merchant PubKey uses Zaprite to receive payment, and Zaprite uses the Lightning Network to confirm the payment status. After confirmation through the Bitcoin network, the transaction is completed.

In this process, Zaprite only has a subscription fee of $25; aside from that, the merchant only needs to deduct miner processing fees, and the rest is their income. We can compare this to Visa/MasterCard/AE, which require around 1.95%-2% in fees, while the average miner processing fee for Bitcoin is around $1.46 recently, and accepting Bitcoin incurs no fees at all.

Continuing this line of thought, Web2 Payments generally follow a logic similar to Chuan Bao buying beer, but there are quite a few intermediaries involved, which is a drawback of Web2. The opportunities for Web3 Payments and PayFi lie within this.

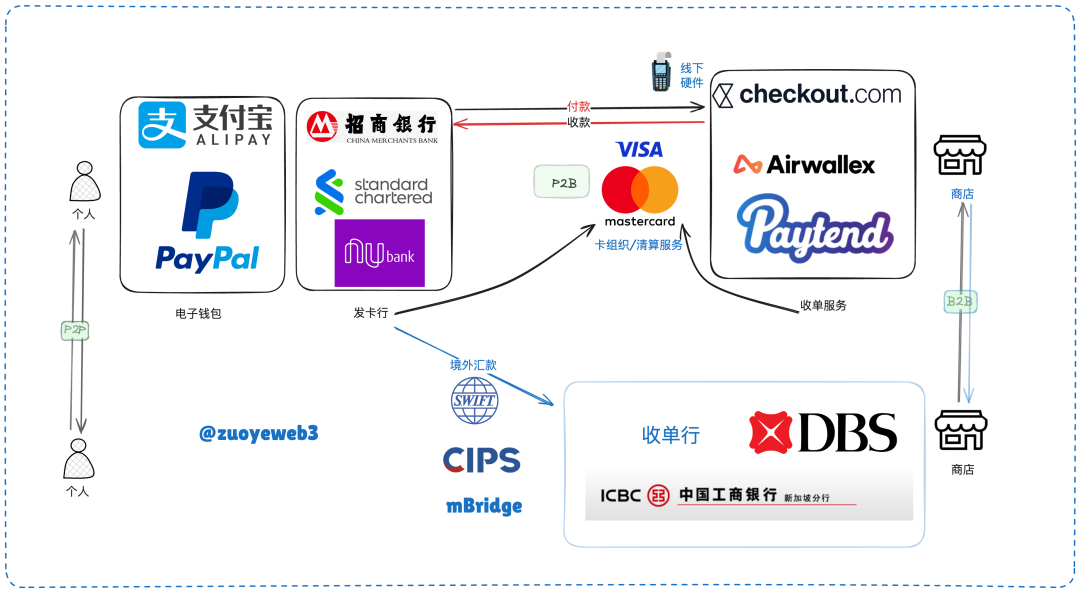

In terms of concept and product replacement, the products we commonly use, such as Alipay, WeChat Pay, and PayPal, belong to electronic wallets aimed at the consumer side, while the corresponding systems are the merchant acquiring systems on the business side. As long as a funding clearing network similar to the Lightning Network is established, the simplest P2B (personal and business) interaction system can be built. Generally, the intermediary clearing network requires card organizations and payment protocols to work together.

In the above diagram, the Web2 payment system can be divided into P2P transactions between individuals, P2B and B2B transactions between individuals and businesses, as well as payment behaviors between merchants. Interbank transactions can also occur through interbank trading systems like SWIFT or CIPS, or through cross-border CBDC trading systems like mBridge.

However, it is important to note that the act of payment strictly occurs between individuals and businesses, and we include P2P and interbank transactions here for the sake of comparison with Web3 payment behaviors. In Web3, the primary payment scenarios are actually between individuals, such as Bitcoin being a peer-to-peer electronic cash payment system.

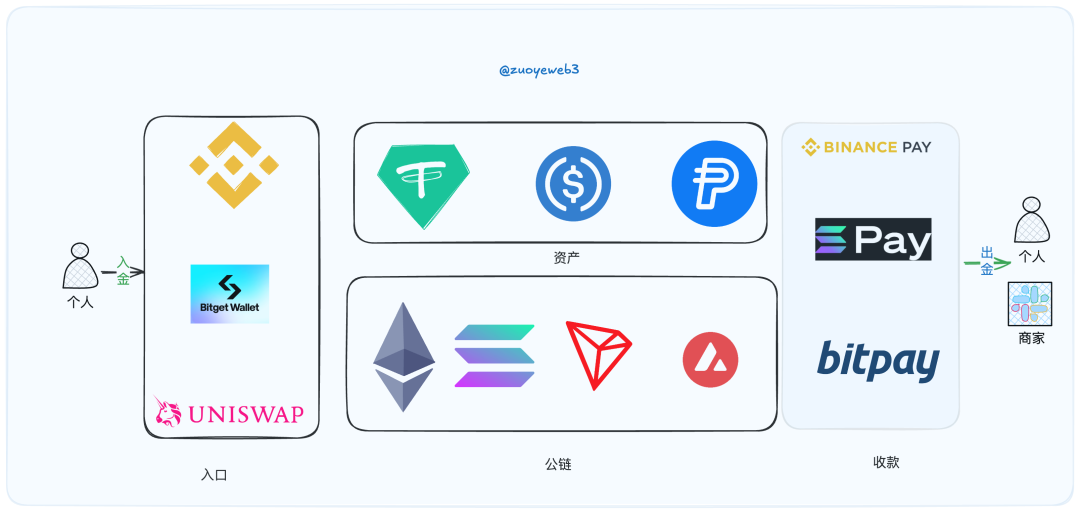

If we refer to the Web2 payment system, then the Web3 payment system is actually very simple. Of course, the theoretical simplicity does not mask the fragmentation of the ecosystem. A notable characteristic is that traditional payment systems have many banks but few card organizations, thus possessing strong network effects. In contrast, Web3 has many public chains/L2s, but the main assets are only stablecoins, with only a few products like USDT/USDC.

Even with the most optimistic estimates, there are only about 30,000 merchants worldwide that support Bitcoin. Although some regions include major brands like Starbucks, the acceptance level still cannot be compared to traditional card organizations or electronic wallets.

Merchants accepting Binance Pay/Solana Pay are more concentrated among online merchants, such as Travala and other travel OTA platforms. There is still a significant distance to go before expanding to the scale of hundreds of millions of merchants like card organizations.

We will elaborate on the content of payment systems in the following sections, and now it is time to introduce the concept of PayFi.

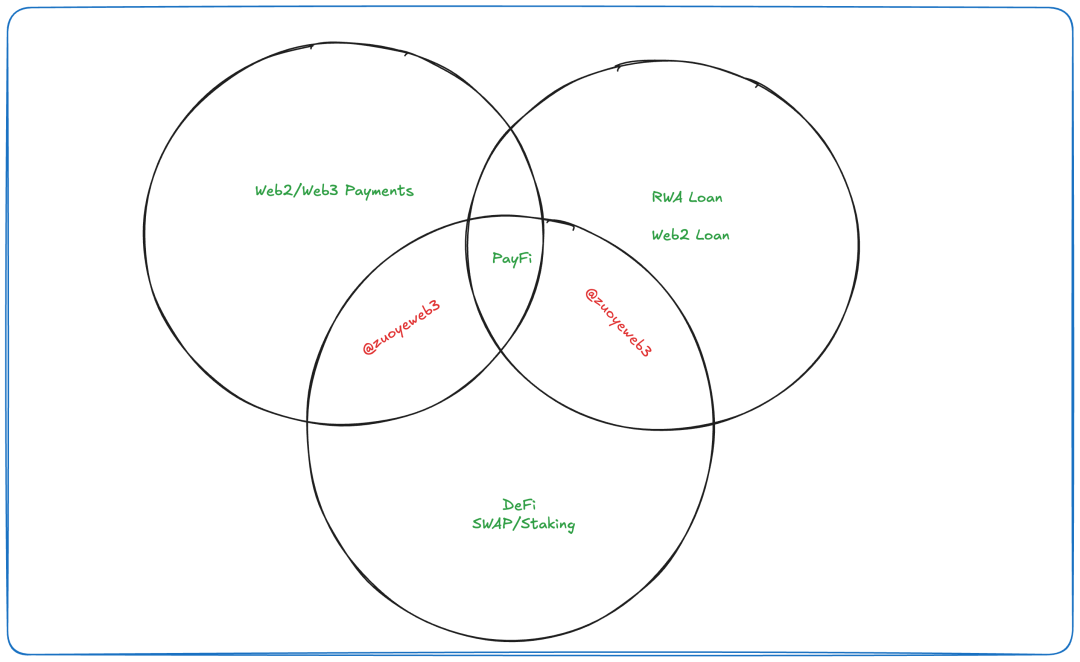

PayFi Stack: The Intersection of DeFi, RWA, and Payments

The reason for adopting a narrative structure that discusses Payments before introducing PayFi is that the differences between the two are quite significant. Overall, PayFi resembles DeFi + stablecoins + payment systems, and its relationship with Web2 Payments is not very strong, as mentioned earlier.

Let’s start with an explanation from Lily Liu: PayFi utilizes the time value of money (TVM). For example, earning profits from funds in DeFi is an application of TVM. However, the issue is that this may require time, such as staking tokens to earn rewards, which usually involves a lock-up period. But as long as there are tokens, there is potential for appreciation. In past operations, after obtaining profits, they could be reinvested in DeFi, creating a cycle of continuously seeking profit opportunities.

Now, this portion of profits can be directed elsewhere, such as using expected earnings for current consumption. For example:

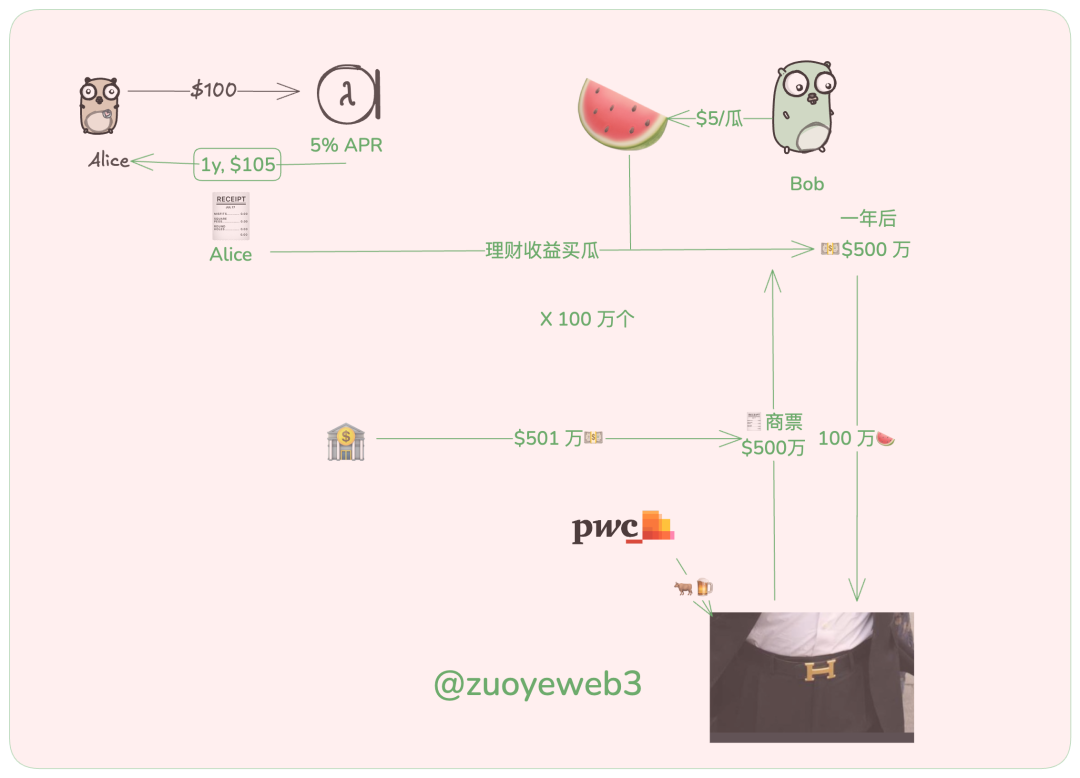

- Alice invests $100 in a financial product with an annual percentage rate (APR) of 5%, and after one year, she can receive $105 in principal and interest.

- Bob, who runs a watermelon stand, allows Alice to use her financial proof to buy a $5 watermelon. A year later, Bob can redeem the $5 from the financial product with the ticket.

This example is very simple, so simple that it cannot withstand scrutiny. For instance, how do Alice and Bob ensure the smooth execution of the contract? What if Alice's financial income decreases? However, without considering these issues, Alice can enjoy the watermelon without any cost, and Bob receives a $5 receivable.

A year later, a bull market arrives, and Bob receives many $5 payments, preparing to enter the large enterprise supplier market. After some selection, he sees that Evergrande is looking for watermelon sellers, and he places an order for $5 million. Bob is very happy, but Evergrande gives him a commercial bill. Having had experience with Alice, Bob happily accepts the commercial bill, and both parties agree to exchange cash for the bill a year later; if not, Bob can take the house as collateral.

However, six months later, Bob prepares to enter the stock market and needs to cash in the commercial bill. After a rating by PwC, the Evergrande commercial bill is rated AAA, a high-quality asset. Banks, non-financial institutions, and even individuals are eager to acquire it, all scrambling for it because Evergrande's real estate has quality assurance and great appreciation potential.

Bob successfully sells the commercial bill for an excess price of $5.01 million. The bank receives the bill, Evergrande gets a free ride, and Bob enjoys stock market dividends. Everyone has a bright future. (Generally, cashing in a commercial bill requires discounts and fees; this is just to illustrate the workflow, and the Evergrande commercial bill was already around 7/8 of its face value before its collapse.)

Another layer of meaning for TVM is the monetization of non-circulating assets, and even non-circulating assets themselves can be currency or its equivalents. This has certain similarities with the logic of restaking, which can be further explored in the article "Alternative Perspectives on Restaking: Triangular Debt or Mild Inflation."

In the context of Web3, the monetization of non-circulating assets can only occur through DeFi. Therefore, PayFi is a natural extension of DeFi, merely extracting a portion of liquidity from the on-chain Lego to improve off-chain living.

The relationship between PayFi and Payments lies in the fact that payments are the simplest and most convenient way to satisfy the need for funds to go off-chain. PayFi and RWA intersect, but traditional RWA emphasizes "on-chain" more, such as the so-called tokenization process, which requires securities, gold, or real estate to be tokenized to enable on-chain circulation. Many familiar consortium chains in China are doing this, such as blockchain electronic invoices or Gongxinbao.

It is difficult to say that PayFi is a subset of RWA; a significant portion of PayFi's activities are "off-chain." Whether there are on-chain components is not the focus of the PayFi concept; rather, its activities need to involve interactions with off-chain elements.

However, there is no need for everyone to get tangled up in this. Many concepts in Web3 lack large-scale products and user groups; they are more about speculating on concepts and selling tokens. Roughly categorizing, products related to PayFi/Payments and RWA can be divided in the following chronological order:

- Old Era: Ripple, BTC (Lightning Network, BTCFi, WBTC), Stellar

- 2022 RWA Concept Triumvirate: Ondo/Centrifuge/Goldfinch

- New Era - 2024 PayFi: Huma (already established, rebounded in 2024), Arf

In fact, from the historical development of the aforementioned products, it is reasonable to say that PayFi is a continuation of RWA. The traditional narrative, especially the business model of lending on-chain funds to off-chain entities, is precisely what 2024's PayFi represents, while in 2022, they were all referred to as RWA.

One could even boldly argue that the lending within RWA, similar to Ripple's cross-border settlement, combined with off-chain consumption of stablecoins, constitutes several aspects of current PayFi. At its core, these are the only contents.

It can be said that the construction of Web3 hardware and software is based on the material and ideological foundations of Web2, and Web3 PayFi is no exception. Its similarities with Payments actually outweigh the differences, and lending products are more about the flow of funds. If off-chain products can generate more returns, then these returns can also be used for payment activities.

Being misunderstood is the fate of the expresser. Whether Lily Liu agrees with this interpretation, I do not know, but I believe that only by laying it out this way can the logic be smooth. As long as on-chain earnings are used for off-chain consumption scenarios, it aligns with the PayFi concept. Therefore, the market's focus moving forward will be on Web3 Payments, RWA Loans, and stablecoins, which can often be incorporated into a cyclical process.

For example, RWA corporate lending, priced in U, allows individuals to enter the RWA on-chain lending pool through DeFi protocols. After evaluation, the RWA lending protocol disburses loans to real enterprises. Upon recovering accounts receivable, LPs receive profit shares from the protocol, and funds are withdrawn using a Mastercard U card, perfectly closing the loop as the merchant supports Binance Pay.

History belongs to the pioneers, not the summarizers. How PayFi is defined is not important; the urgent task is to explore real returns beyond the internal competition of DeFi on-chain. The demand from billions of people off-chain will bring richer liquidity and higher leveraged valuation support to on-chain, and those who can run the process will define the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。