The biggest challenge is not in the issuance, but in the design of the application scenarios.

Authors: Sun Wei, Aiying

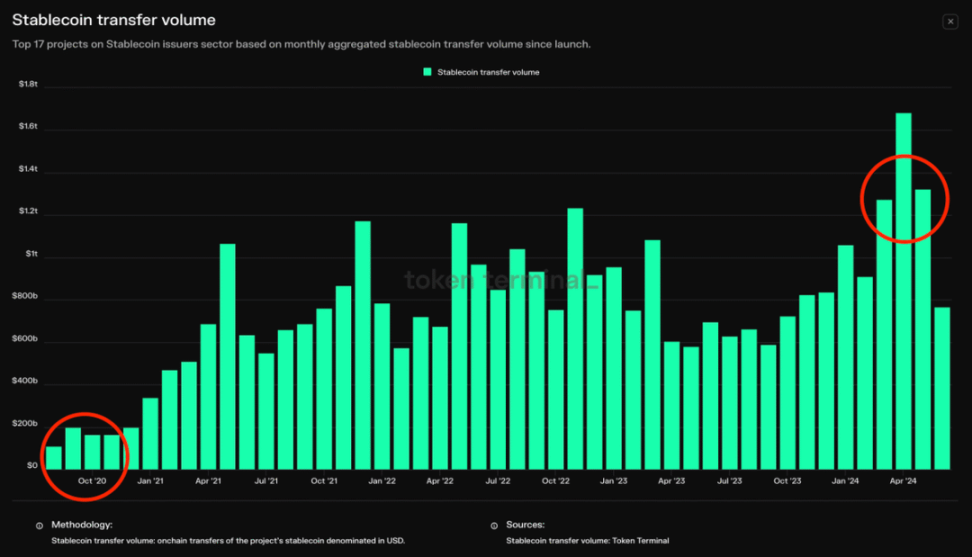

According to data from Token Terminal, the monthly stablecoin transfer volume has increased tenfold over the past four years, from $100 billion per month to $1 trillion on June 20, 2024. On that day, the total trading volume of the entire cryptocurrency market was $74.391 billion, with stablecoins accounting for 60.13%, approximately $44.71 billion. Among them, USDT (Tether) is the most widely used, with a market value of $112.24 billion, accounting for 69.5% of the total value of all stablecoins. On June 20, the trading volume of USDT reached $34.84 billion, accounting for 46.85% of the total daily trading volume.

Stablecoins, as an important presence in the cryptocurrency market, are fundamentally defined as cryptocurrencies pegged to fiat currencies or other assets to achieve value stability. The Bank of International Settlements defines stablecoins as "cryptocurrencies pegged to fiat currencies or other assets." This design aims to enable stablecoins to maintain a stable value relative to the pegged specific assets or a basket of assets, thereby achieving stable value storage and exchange medium. This mechanism is very similar to the gold standard system, but because it is issued on the blockchain, it also has the characteristics of decentralized, peer-to-peer transactions, no need for central bank clearing, and immutability of encrypted assets.

This report by Aiying will delve into the definition of stablecoins and their main models, analyze the overall market and competitive situation, focus on the operating principles, advantages and disadvantages of fiat collateral, encrypted asset collateral, and algorithmic stablecoins, as well as the performance and future development prospects of different types of stablecoins in the market.

I. Definition and Main Models of Stablecoins

1. Basic Definition: Anchoring Fiat Currency, Value Stability

Stablecoins, as the name suggests, are cryptocurrencies with stable value. The Bank of International Settlements defines stablecoins as cryptocurrencies pegged to fiat currencies or other assets. Furthermore, the main purpose of stablecoins is to maintain a stable value relative to the pegged specific assets or a basket of assets, in order to achieve stable value storage and exchange medium. In this respect, it is very similar to the gold standard system. Because it is issued on the blockchain, it also has the characteristics of decentralized, peer-to-peer transactions, no need for central bank clearing, and immutability of encrypted assets.

The main difference between the value stability of stablecoins and the pursuit of fiat currency value stability by traditional central banks is that stablecoins pursue a relative exchange rate parity with fiat currencies, while fiat currencies pursue stable purchasing power across periods. In simpler terms, stablecoins essentially aim to anchor the fiat currency system to achieve stable token value.

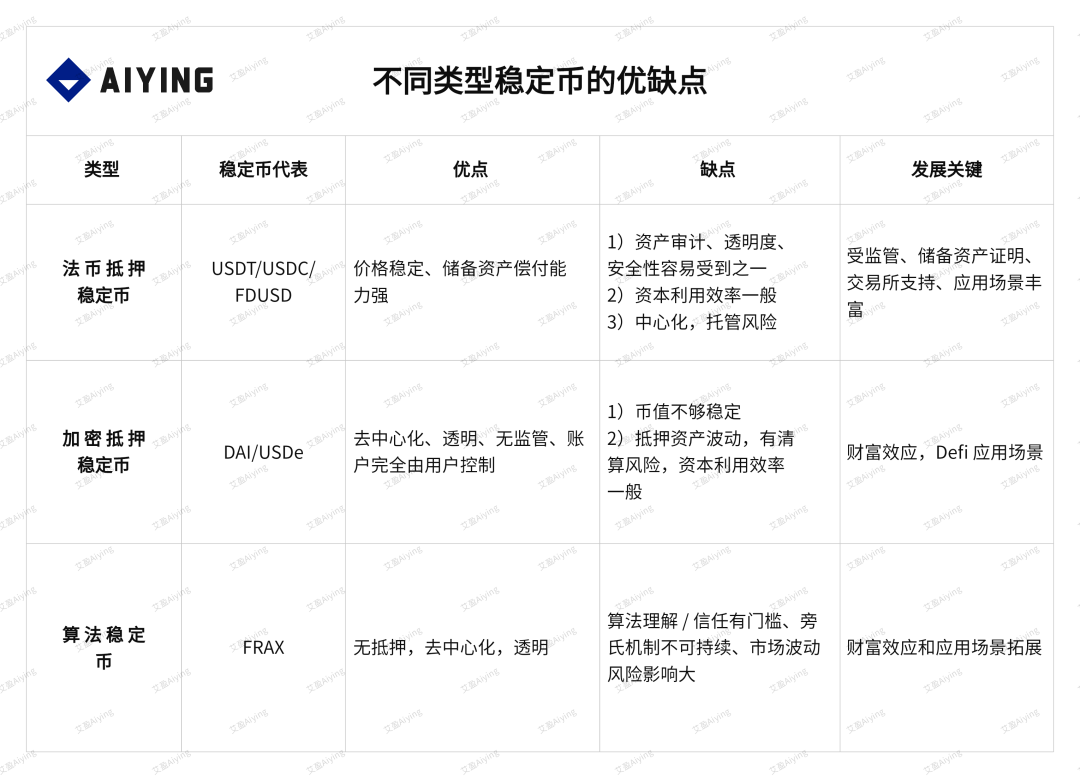

2. Main Models: Collateral Assets and Degree of Centralization as the Main Differentiation

For stablecoins, in order to ensure the anchoring of the fiat currency system, based on the endorsement of underlying assets, they are divided into collateralized and uncollateralized types, and further divided into centralized and decentralized types in terms of issuance. For value stability, using real-world valuable assets as collateral to issue stablecoins to achieve anchoring with fiat currencies is the easiest and relatively safe way to do so. A higher collateralization ratio means sufficient solvency. According to the classification of collateral, it can be further refined into fiat collateral, encrypted asset collateral, and other supported asset collateral.

Specifically, it can be further subdivided as follows:

From the above table, it can be seen that in terms of the basic operating mode, the value stability of stablecoins mainly depends on the collateral assets or the method of algorithmic regulation to keep the stablecoin price stable within a controllable fiat exchange range. The key is not the price fluctuation, but how to reasonably correct this fluctuation to operate within a stable range.

II. Overview and Competitive Situation of the Stablecoin Market

1. From the Perspective of Anchoring Fiat Currency: The US Dollar Almost Dominates the Entire Market

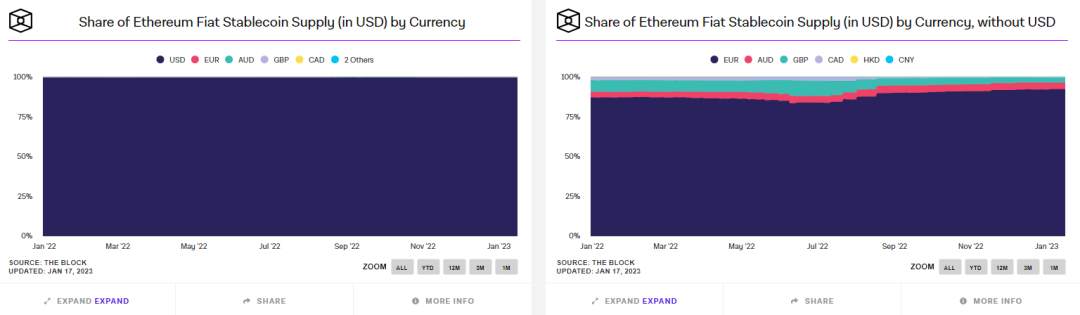

In terms of anchoring prices, apart from PAXG and other stablecoins anchored to the price of gold, 99% of stablecoins are pegged 1:1 to the US dollar. There are also stablecoins pegged to other fiat currencies, such as EURT pegged to the euro, with a market value of $38 million, GYEN pegged to the Japanese yen, currently with a market value of only $14 million, and IDRT pegged to the Indonesian rupiah, with a market value of $11 million. The overall market value is very small.

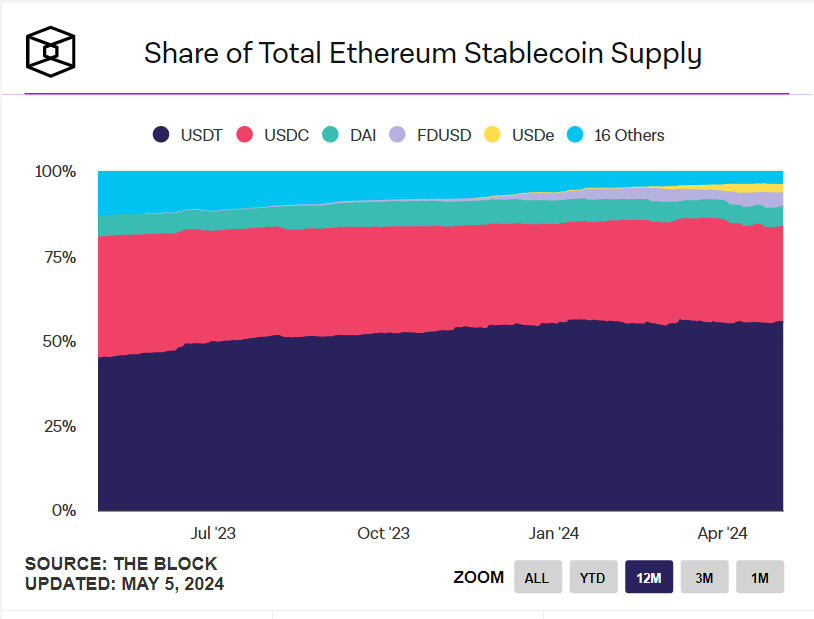

Stablecoins pegged to the US dollar currently maintain a market share of around 99.3%, with the remaining mainly consisting of the euro, Australian dollar, British pound, Canadian dollar, Hong Kong dollar, and Chinese yuan, among others.

Market share of stablecoins pegged to fiat currencies Source: The Block

2. From Market Share and Market Value: USDT is Absolutely Dominant, USDC is Catching Up

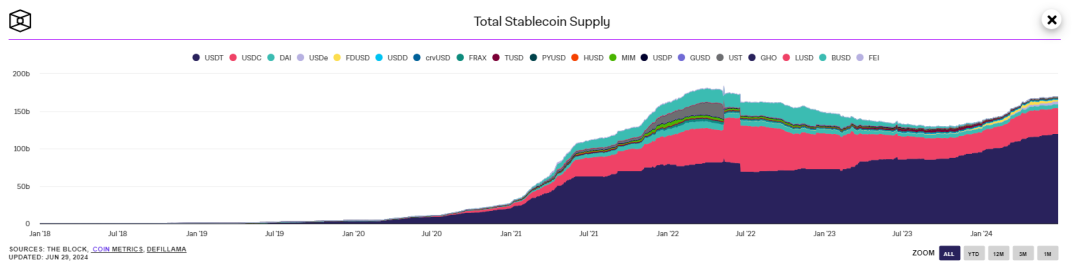

The issuance volume of stablecoins is closely related to the market situation. Monitoring data shows that overall issuance volume has continued to grow, but there was a slight decline during the last bull-to-bear period (March 2022), and it is currently in a phase of marginal issuance growth, which also indicates the current bull market.

Chart 3: Historical issuance of stablecoins (Source: The Block)

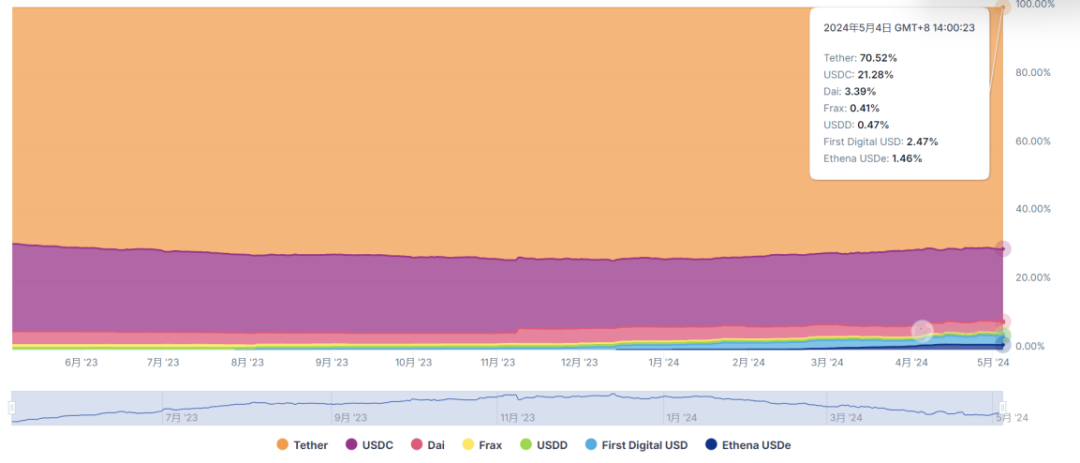

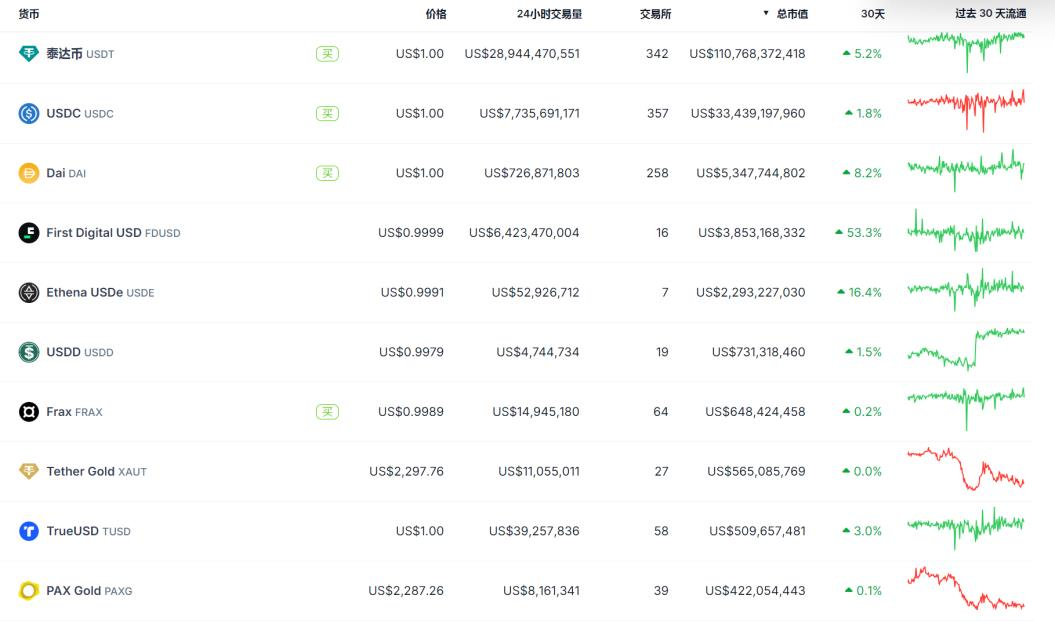

According to the latest data from Coingecko, as of May 4, in the stablecoin race, USDT has a market share of 70.5%, followed by USDC at 21.3%, DAI at 3.39%, FDUSD at 2.5%, and FRAX at 0.41%.

Chart 4: Market share of stablecoin race Source: Coingecko

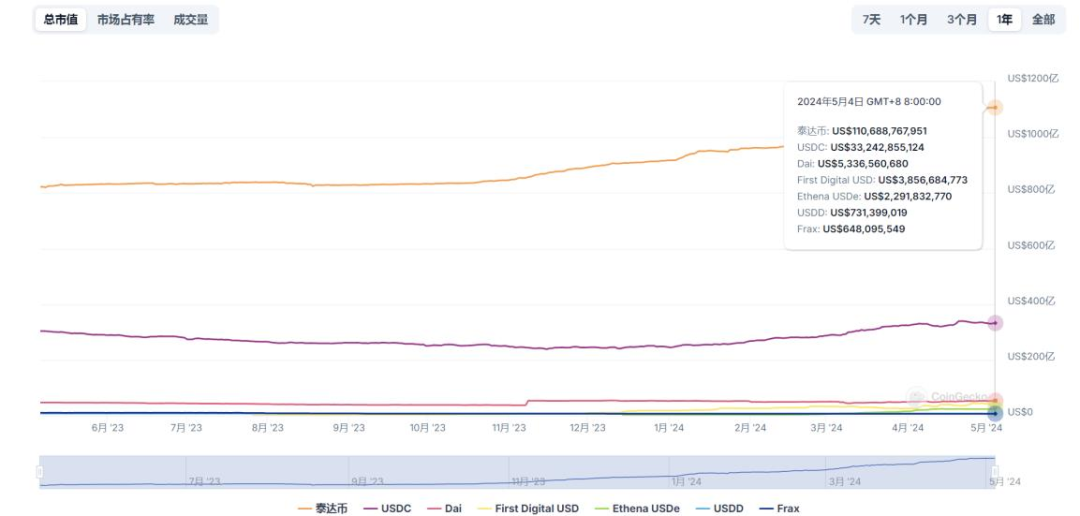

In addition, in terms of market value, the total market value of all stablecoins is over $160 billion, with USDT in a commanding lead and stable growth, currently with a market value of over $110 billion. The market value of USDC is steadily rising, at over $33 billion, but still lags behind USDT, while other stablecoins are basically stable.

Chart 5: Market value of mainstream stablecoins Source: Coingecko

3. From the Top Ten Market Value: Fiat Collateral Stablecoins Occupy the Absolute Leading Position, Covering Various Types of Stablecoins

Looking at the current top ten mainstream stablecoins, centralized US dollar collateral stablecoins mainly have a broad collateralization ratio of over 100%, while DAI is a decentralized encrypted asset collateral stablecoin; USDe is a synthetic dollar with encrypted assets as collateral; FRAX is an algorithmic stablecoin, and PAXG is a gold-backed stablecoin.

Chart 6: Market value of mainstream stablecoins Source: Coingecko

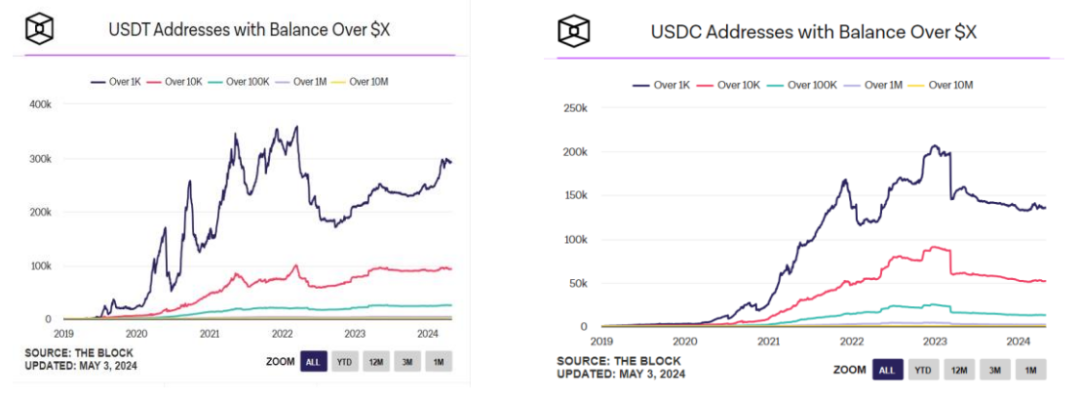

4. From the Perspective of Holding Addresses: USDT Overall Stable, USDC Showing Recent Weakness

From the changes in the holding addresses of the two, it is evident that the sharp decline in the holding addresses of both is due to the decoupling from the US dollar. On March 11, 2023, USDC was affected by the SVB bankruptcy event, causing it to decouple from the US dollar, dropping to around 0.88 at one point, leading to a rapid decrease in the holding addresses. Although it later recovered, the holding addresses were once again surpassed by USDT.

Chart 7: Changes in USDT vs USDC Holding Addresses Source: The Block

From the above chart, it can be seen that after the decoupling event, the addresses of USDC decreased significantly from over 1,000 to over 10 million. The decrease from the peak is about 30%, corresponding to the steady increase in USDT.

III. How do mainstream stablecoins operate, and what are their advantages and disadvantages?

Continuing from the analysis, the current mainstream stablecoins are mainly differentiated based on the type of collateral assets and the degree of centralization in issuance. Generally, stablecoins collateralized by fiat currencies are mostly centrally issued and currently dominate the market. Stablecoins collateralized by encrypted assets or algorithmic stablecoins are mostly decentralized, with each category having its leader. Each stablecoin's design framework has its own advantages and disadvantages.

1. Fiat Collateral Stablecoins (USDT\USDC)

1) Main Operating Principles of USDT

- Basic Introduction:

In 2014, Tether, a company under iFinex, created the stablecoin USDT. The company also owns the cryptocurrency exchange Bitfinex, both registered in the British Virgin Islands, with headquarters in Hong Kong. Tether is headquartered in Singapore. The current CEO is Paolo Ardoino (the company's former CTO), an Italian who initially developed trading systems for hedge funds. He joined Bitfinex as an executive in 2014 and joined Tether in 2017, currently owning 20% of Tether's shares.

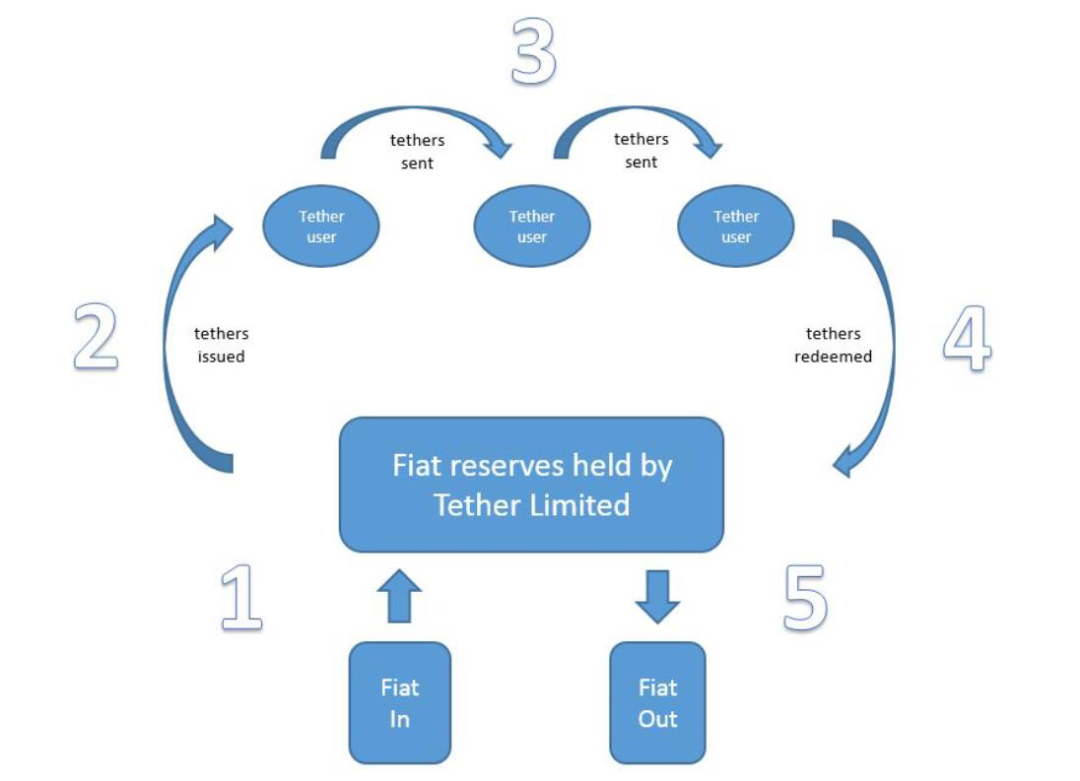

- Issuance and Circulation:

It mainly consists of five steps. The first step is for users to deposit US dollars into Tether's bank account. The second step is for Tether to create a corresponding Tether account for the user and mint the corresponding value of USDT into their account. The third step is the circulation of transactions between accounts. The fourth step is the redemption stage, where if a user wants to redeem US dollars, they need to give the USDT to Tether, and the fifth step is for Tether to destroy the corresponding value of USDT and return the US dollars to the user's bank account.

Chart 8: Full Process of USDT Issuance, Trading, Circulation, and Redemption Source: Tether Whitepaper

Technical Implementation:

The issuance of USDT by Tether requires the embedding of blockchain technology to achieve the above process. The overall technical architecture is not complex and mainly consists of three layers.

The first layer is the blockchain mainnet, initially mainly the Bitcoin blockchain, but now expanded to over 200 public chains. The USDT transaction ledger is embedded in the blockchain through the Omni layer protocol.

The second layer is the Omni Layer Protocol, which primarily serves the Bitcoin blockchain for minting, trading, and storing USDT. Since 2019, the minting of USDT has gradually shifted to the Tron and Ethereum blockchains, mainly using the TRC-20 and ERC-20 protocols.

The third layer is Tether, mainly responsible for issuance, collateral asset management, auditing, etc.

Chart 9: USDT Technical Implementation Architecture (Using the Bitcoin Network as an Example) Source: Tether Whitepaper

The fundamental aspect of the issuance and technical implementation mentioned above is the Proof of Reserves mechanism operated by Tether. Specifically, for every USDT minted, Tether must increase its reserves by $1, meaning that for every USDT issued, the corresponding collateral must also increase by $1, ensuring 100% equivalent collateral.

Asset (collateral) reserve situation:

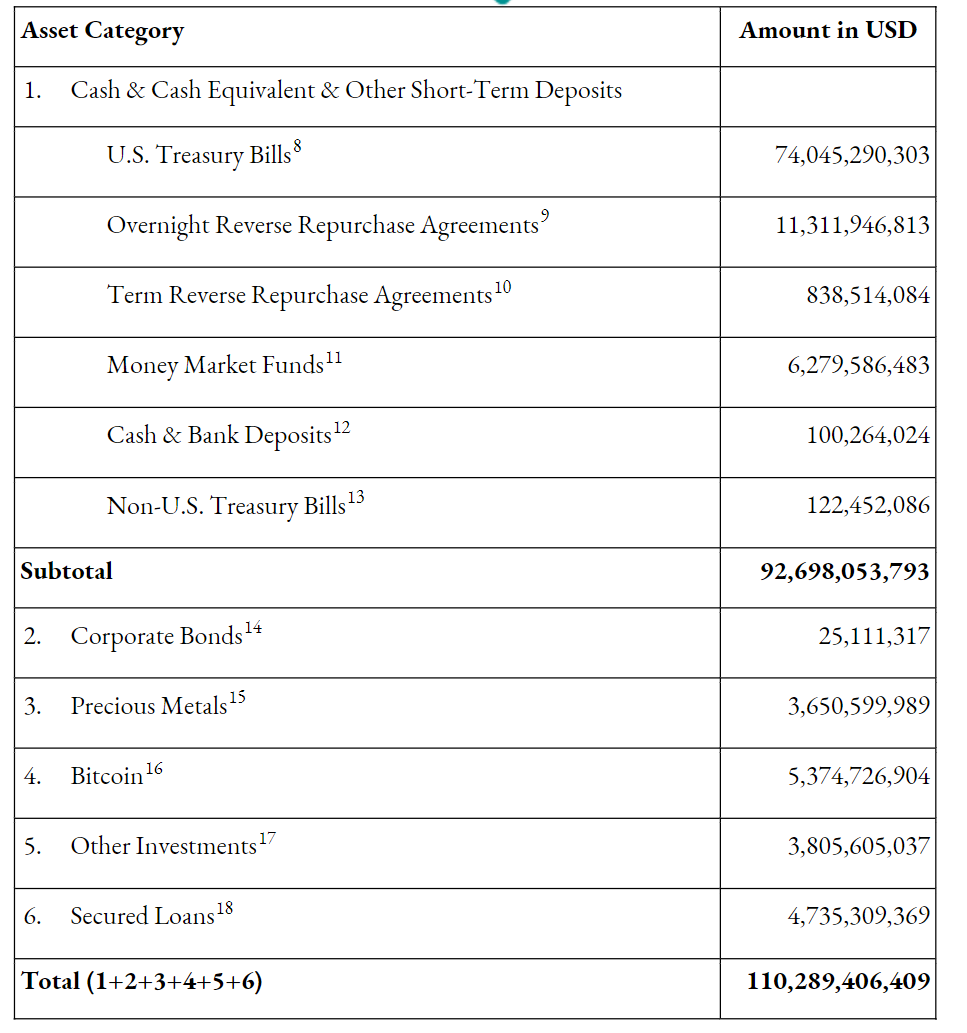

The total asset reserve is over $110 billion, consistent with its current market value. In terms of asset reserve categories, cash and cash equivalents account for 83%, while others account for 17%.

In detail, within cash and cash equivalents, short-term US Treasury bonds account for approximately 80%, followed by overnight reverse repurchase agreements at nearly 12%, with the remainder consisting of money market funds, cash and bank deposits, term repurchase agreements, and non-US Treasury bonds. In the other asset category, it mainly consists of Bitcoin, high-grade corporate bonds, precious metals, and collateralized loans, with Bitcoin and collateralized loans accounting for a large proportion.

Chart 10: Composition of Tether's Asset Reserves (Data as of Q1 2024) Source: Tether Official Website

In addition, based on audit reports from the past three years, Tether has closely followed the external macro environment in its asset reserves, with an increasing proportion of US short-term Treasury bonds and money market funds, while reducing corporate bonds, cash, and bank deposits. Furthermore, due to the different maturities of its assets, this is the most likely scenario for shorting USDT. The audit report reveals that the US Treasury bonds and term repurchase agreements it holds are all ultra-short-term, less than 90 days, with the only longer-term ones being corporate bonds and non-US Treasury bonds, with maturities of within 150 days and 250 days.

This allocation of reserve assets indirectly increases its asset operation income and further reduces its risk coefficient, enhancing asset security, especially with shortened maturities, which helps prevent shorting due to maturity mismatch.

Profit model:

Cost side: Very few technical and operations personnel, with very low marginal costs.

Revenue side: Service fees after KYC registration ($150 per person), deposit and withdrawal fees (approximately 0.1%), interest income (such as the 4-5% yield on short-term US Treasury bonds, with zero cost, and other loan interest income), custody fees (fees for institutions custodied in Tether). In Q1 2024, Tether announced a net profit of $4.5 billion, a historical high, with only around 100 employees, while Goldman Sachs and JPMorgan, with similar profits, have over 50,000 employees. The profitability efficiency is very rare.

2) Main Operating Principles of USDC

Similar to USDT, the main issuance, circulation, and technical implementation of USDC are similar, pegging 1 USDC to 1 US dollar. It is a stablecoin created by Coinbase and Circle in 2018, later than USDT, but with some differences in specific operational details:

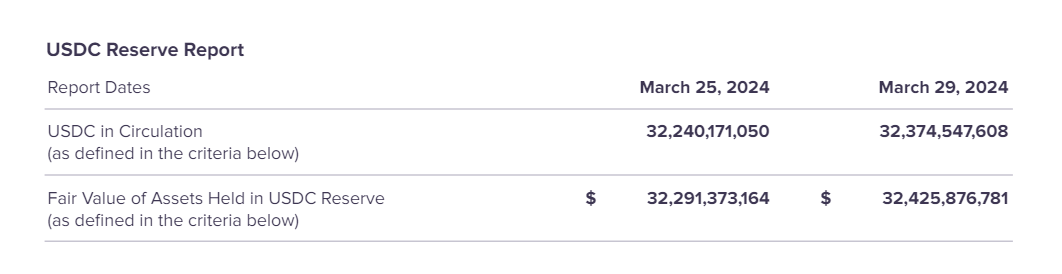

- Higher transparency of asset reserves: Compared to USDT, which discloses asset reserves quarterly, USDC discloses its asset situation monthly. Third-party audit firms conduct annual audits of asset reserves, initially mainly by Grant Thornton, changing to Deloitte in 2023. As of March 2024, the circulating USDC is $32.2 billion, with Circle's equivalent assets at around $32.2 billion, remaining roughly equal.

Chart 11: Full Process of USDT Issuance, Trading, Circulation, and Redemption

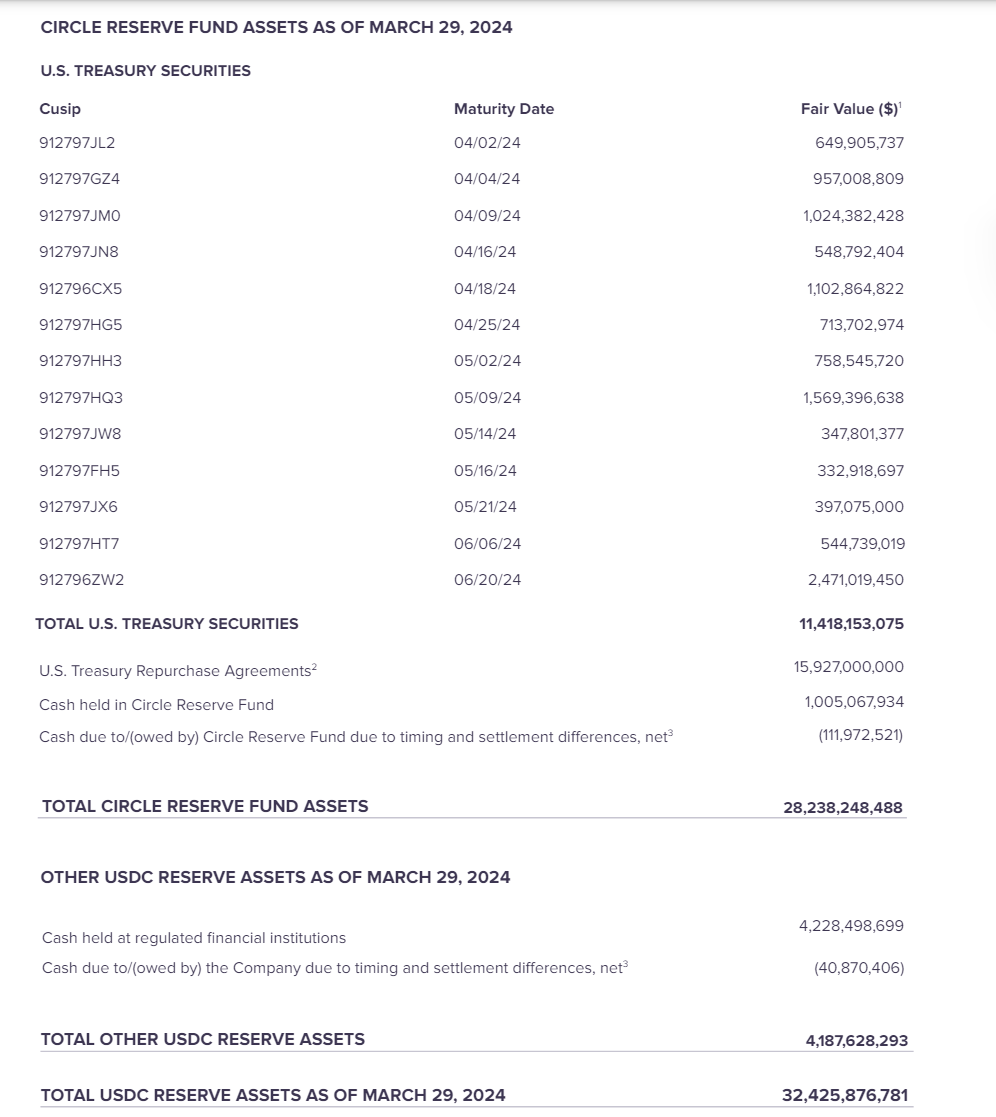

Asset reserves are mostly short-term Treasury bonds and cash, with shorter maturities, providing higher liquidity compared to USDT: Unlike USDT, which only discloses the overall maturity of Treasury bonds, USDC publishes the maturity dates of its main Treasury bond assets. According to data disclosed in March, the maturities are all within 3 months, with the latest short-term bonds maturing in June, with a total scale of $11.4 billion. Additionally, there are mainly repurchase agreements and cash reserves, totaling $28.2 billion. Furthermore, there is an additional $4.2 billion in cash, all held in the Circle Reserve Fund (CRF) registered with the SEC by BlackRock. Approximately 95% of the assets are under SEC regulation. Additionally, due to the higher proportion of cash assets, the liquidity for redemptions is higher than that of USDT.

Chart 12: USDC Reserve Assets (As of March 2024) Source: Circle Official Website

The establishment of USDC is carried out within the regulatory framework of the United States, giving it a higher legal status: Circle is registered as a money services business with the Financial Crimes Enforcement Network (FinCEN) under the U.S. Department of the Treasury and operates in accordance with the laws of each state regarding money transmission. It is generally regulated as a form of prepaid payment. Compared to USDT, the reserve assets of USDC are independent. In the event of Circle's bankruptcy, these reserve assets will be protected under New York banking law and federal bankruptcy law.

USDC does not directly exchange with individuals: For amounts over $100,000, USDT can be exchanged directly with Tether by paying a registration fee. However, Circle operates based on customer levels. Only its partners or Class A users (exchanges, financial institutions, etc.) are eligible to exchange with Circle. Regular individual users (Class B) need to go through third-party channels (such as Coinbase). Additionally, in terms of profit sources, USDC is basically the same as USDT, but due to the fact that USDC's assets are mainly short-term Treasury bonds and cash, its risk exposure is lower than that of USDT, resulting in relatively lower yields.

3) Main Operating Principles of FDUSD

After the New York Department of Financial Services ordered the cryptocurrency company Paxos to stop issuing new BUSD, the world's largest exchange, Binance, also stopped supporting BUSD products on December 15, 2023, and announced that BUSD balances would be automatically converted to FDUSD. Since then, the market value of FDUSD has been rising, occupying the third position in the fiat-collateralized stablecoin market.

- Basic Introduction:

FDUSD is a USD-pegged stablecoin launched by FD121 (First Digital Labs) in June 2023. Its parent company, First Digital Trust, is a qualified custodian and trust company based in Hong Kong, mainly engaged in digital asset-related businesses. It was established by Legacy Trust in 2017 and officially became an independent public trust company in 2019. Legacy Trust is a well-established public trust company founded in 1992.

- Operating Mode:

The basic operation of FDUSD is not significantly different from that of USDT\USDC. Users deposit US dollars, and the issuer mints the corresponding amount of FDUSD. Similarly, if US dollars are withdrawn, the corresponding amount of FDUSD is destroyed. FDUSD is audited by Prescient Assurance (an accounting firm based in New York, a CREST-certified global top 20 security testing and auditing organization), and contract auditing is conducted by Pionex.

- Asset Disclosure and Reserve Situation:

Similar to USDC, FDUSD also discloses its assets monthly. Its reserve assets are mainly managed by a public trust company in Hong Kong, without disclosing the specific names of the financial institutions where the reserve assets are held. However, it is clear that these financial institutions all have a credit rating of A-2 under Standard & Poor's. As of March 2024, the issued and circulating FDUSD is $2.5 billion, corresponding to reserve assets of $2.5 billion. In terms of reserve asset classification, $1.86 billion is in short-term Treasury bonds, with the latest maturity date being May 21, fixed deposits amount to $265 million with a maturity of 1 month, and other cash assets amount to $170 million. Overall, these are all ultra-short-term assets, with very high liquidity and immediate payment effects.

4) Summary of Fiat-Collateralized Stablecoin Track

When reviewing the top three fiat-collateralized stablecoins, USDT, USDC, and FDUSD, it is clear that they have taken different paths to success. A brief summary is as follows:

USDT: 1) The biggest advantage is the first-mover advantage, but its rise is mainly due to the support of exchanges and market surges. During the early days of cryptocurrency, from the early Bitcoin blockchain to the later Ethereum ecosystem, USDT was a worthy pioneer and also accurately predicted the market's explosive growth. Looking at its holding addresses and market value, although it was established in 2014, its true rise began in 2017. That year, in addition to the bull market, USDT began massive issuance, which was criticized for manipulating the price of Bitcoin. However, in hindsight, this was a case of reverse causality. What is easily overlooked is that China closed virtual currency that year, and more importantly, USDT was simultaneously listed on the top three exchanges. 2) Despite being attacked by risk events, USDT responded promptly and effectively, quickly regaining market confidence. Tether's affiliated exchange, Bitfinex, was once considered a company and faced hacking attacks and fines from the U.S. government from 2014 to 2016. Tether was also cut off from international wire transfers by banks such as Fubon Bank and banks in Taiwan. It even decoupled from the U.S. dollar at one point. Tether's main response was to quickly disclose its asset reserves, including its excess reserves and undistributed profits, to regain market confidence based on the health of its financial condition. Regardless of whether its data was falsified, it did provide a very strong response to market concerns. Through its first-mover advantage and multiple market public relations efforts, USDT has formed a strong consumer habit, and it is still the preferred stablecoin for deposits and withdrawals, covering the widest range of trading pairs on exchanges.

USDC: 1) Rose during the USDT crisis, transparent, regulated, and more liquid asset reserves won customer favor. Looking back at the rise of USDC, the significant increase in its holding addresses usually corresponds to a decline in USDT holdings, often occurring during USDT's risk events. This is especially true because it was the only stablecoin trading pair on the compliant exchange Coinbase in the early days, which brought great benefits to the early market expansion of USDC due to the regulated support. This was a major competitive advantage in challenging USDT's top position. 2) Due to compliance, Defi protocols favor USDC, and liquidity mining has rapidly increased the on-chain dominance of USDC. After Maker introduced the regulated stablecoin USDC in 2020, USDC became the preferred choice for major Defi protocols. Currently, MakerDAO, Compound, and Aave are the main supporters of USDC in the Defi space. In addition to the regulatory advantages, the more important factor is that as collateral for Defi protocols, USDC has lower volatility compared to USDT. The victory of USDC can be summarized as a victory for compliance. However, it is worth noting that as a compliant collateral, in August 2023, Circle froze Tornado Cash's USDC (money laundering allegations) in accordance with the U.S. Department of the Treasury's instructions, which has sown discord over whether decentralized Defi protocols should overly rely on centralized stablecoins.

FDUSD: 1) The support of top exchanges and implicit regulatory compliance are the main reasons for the rise of FDUSD. The decision by the top cryptocurrency exchange Binance to abandon BUSD in 2023 and support FDUSD as the only designated stablecoin for its Launchpad and Launchpool liquidity mining resulted in rapid market value growth for FDUSD, quickly propelling it to the top three in the stablecoin market. The rise of FDUSD can be directly attributed to Binance's support, and more crucially, the market does not lack regulated stablecoins (USDC). Binance's choice took into account the regulatory environment in Hong Kong and the U.S.'s attitude towards Binance, making FDUSD, born in Hong Kong, the best choice. 2) Scenario-based and wealth effects determine its growth rate and ceiling. If FDUSD is adopted by exchanges without suitable use cases, it would be difficult to achieve its rise. After being listed on Binance, FDUSD became one of the only two cryptocurrencies for mining on Launchpool and Launchpad (the other being BNB). Since its listing, the average annualized mining yield through FDUSD mining has been close to 70%, providing significantly high returns for short-term miners, quickly boosting the usage rate of FDUSD.

Overall, for fiat-collateralized stablecoins, their success depends on several important factors:

Whether they operate within a regulatory framework, which helps gain early user trust. This is true for USDC, FDUSD, and others.

Advantages in reserve proof auditing, security, and transparency. (For example, TUSD introduced real-time auditing in 2023, including using Chainlink to ensure coin minting security, revitalizing this older stablecoin; and the rise of USDC is also due to this factor).

Support from exchanges and extensive partnerships determine the lower limit of development. The rise of USDT, USDC, and FDUSD all depended on support from exchanges. Only with the massive liquidity support from these exchanges could stablecoins achieve a smooth start.

Use cases and wealth effects determine the development speed and ceiling. A typical example is FDUSD, as mentioned earlier, as well as USDC and PYUSD (launched by PayPal and parasitic on the PayPal wallet). The rapid development of these stablecoins is due to the strong wealth effects in a specific niche scenario or convenient services, which in turn increases user adoption.

2. Crypto Asset-Collateralized Stablecoins (DAI/USDe)

Due to the significant volatility of crypto assets, their credit basis is weaker compared to risk-free assets in U.S. dollars (such as Treasury bonds and USD deposits), so they generally require over-collateralization. However, synthetic dollars created through derivative hedging models can achieve close to 100% collateralization. However, due to the use of crypto assets, they typically have decentralized characteristics.

1) Main Operating Principles of DAI

- Basic Introduction:

DAI is the flagship decentralized stablecoin issued and managed by MakerDAO since 2017. MakerDAO is a decentralized finance (DeFi) project headquartered in San Francisco, USA, founded by Rune Christensen. Project investors include A16z, Paradigm, Polychain Capital, and other well-known crypto industry investment institutions. In the early stages, it was mainly operated by the Maker Foundation, and it is currently managed by its community through a decentralized autonomous organization (DAO) (holding MKR tokens).

- Main Operating Mechanism:

DAI is also pegged 1:1 to the U.S. dollar. The Maker protocol introduced collateralized DAI in 2017, allowing users to mint DAI by pledging ETH. In 2019, it introduced multi-collateral DAI, accepting collateral other than ETH. In addition to changes in collateral, it also introduced DAI savings interest, supporting stablecoin interest, and renamed the collateral vault to the Vault, while stablecoins generated from single collateral were renamed SAI.

The creation process is as follows.

Step 1: Create a vault through the Oasis Borrow portal or interfaces created by the community such as Instadapp, Zerion, MyEtherWallet, etc., and lock in a specific type and quantity of collateral to generate DAI (the Maker protocol also supports using RWA assets as collateral, such as real estate mortgages and accounts receivable).

Step 2: Initiate and confirm transactions through a crypto wallet, while generating DAI (equivalent to collateralized borrowing).

Step 3: To redeem the collateral, users need to repay the corresponding amount of DAI (equivalent to repaying the debt) and pay stability fees (equivalent to risk compensation, or can be considered as a risk parameter to adjust supply and demand, maintaining the 1:1 peg to the U.S. dollar. In a bull market, stability fees can be as high as 15% or more). In the fourth step, the Maker protocol will automatically destroy DAI and return the collateral to the user.

Mechanism for stabilizing the price of DAI. Compared to fiat-collateralized stablecoins, the collateral assets of DAI have risk-free characteristics and high liquidity, making them a hard peg, allowing the price range to be quickly stabilized through reserve assets. For decentralized stablecoins collateralized by crypto assets, the volatility and trading in the crypto market can lead to price differentials, so a price stabilization mechanism is needed. This is mainly achieved through interest rate adjustments and liquidation. In terms of interest rates, it mainly involves stability fee rates and DAI Savings Rate (DSR). The stability fee rate is based on the risk coefficient of continuously pegging to the U.S. dollar, equivalent to loan interest; DSR is equivalent to the basic yield of earning DAI or the deposit interest rate. This stabilization logic is similar to traditional banking. If the income from loans (stability fee income) is lower than the DSR income (interest paid on DAI deposits), the protocol as a whole will have bad debts. To make up for the bad debts, additional MKR (governance tokens) need to be issued, shifting the burden to MKR holders. This mechanism also ensures fairness and reasonableness in stability fee voting.

Mechanism for liquidation of DAI. Similar to traditional credit, if the value of the collateral significantly decreases and the debt cannot be covered, it will face forced liquidation by the bank. DAI also has a similar mechanism, using a Dutch auction (decreasing price tiers, bid equals transaction) to determine the main auction initiation mode based on the collateral value-to-debt ratio (liquidation ratio), which varies for different vaults created by different users. For example, if the collateral is ETH with a collateralization ratio of 75% and a market price of 3000U, the user can receive a maximum of 2250U of DAI. If the user only takes 2000U of DAI for insurance, the collateral coverage ratio is 1.5, with an exposure of 66.7%. Generally, it faces liquidation when the exposure usage rate exceeds the collateralization ratio, meaning that when ETH falls to 2666U, it faces liquidation risk. Anchoring and stabilizing protocol for DAI. It is difficult to understand literally, but if expressed in traditional financial terms, it is a currency swap agreement. The simple operation is that DAI can be exchanged for other stablecoin assets such as USDC at a 1:1 exchange rate. Additionally, through stablecoin swaps, the protocol converts the reserve pool of USDC and other fiat stablecoins into U.S. dollars for short-term U.S. bond investments, further increasing its returns and enhancing its DSR income, attracting users.

Profit analysis of DAI. It mainly comes from stability fee income (loan interest), similar to the funding rate for USDT deposits and withdrawals. It also includes liquidation penalty income, stablecoin swap transaction fees, and investment income from collateralized RWAs. In 2023, the protocol's revenue was $96 million.

2) Main Operating Principles of USDe

Basic Introduction:

USDe is a decentralized on-chain stablecoin created by Ethena Labs. Its early concept was proposed by the well-known crypto influencer Arthur Hayes, and the project also received investments from BitMEX founder Arthur Hayes and his family fund, as well as several major funds including Deribit, Bybit, OKX, Gemini, and others. After its launch on February 19, 2024, its supply skyrocketed, entering the top five in the stablecoin supply industry, second only to FDUSD.

Operating principles of USDe: Application of neutral hedging strategies in the cryptocurrency market

USDe from Ethena Labs is a synthetic dollar protocol. In the cryptocurrency market, a synthetic dollar protocol uses a series of crypto derivatives to stabilize the issued stablecoin to the U.S. dollar.

In specific operations, USDe uses a delta-neutral strategy. In traditional finance, delta refers to the change in option price divided by the change in the underlying asset price. Delta-neutral generally refers to a portfolio's value not being affected by small changes in asset prices, often referred to as delta-neutral (delta equals 0).

Ethena's neutral strategy operates as follows. When a user mints 1USDe, Ethena simultaneously deposits ETH worth 1 U.S. dollar on a derivatives exchange and establishes a short position in the perpetual contract for 1ETHUSD. If ETH falls by 10 times, the contract will earn a profit of 9ETH. Therefore, the total position of ENA is 10 ETH, and since the price has also fallen by 10 times, the total value of the position remains unchanged. The same applies in the case of price increases, ensuring the stability of the minted stablecoin. If a user chooses to redeem USDe, Ethena will quickly close the short position.

The rapid rise of USDe: Similar to the Pareto mechanism, but more than Pareto, it is essentially a term hedge

Financial products.

For users who mint USDe, they can quickly pledge it in Ethena and earn pledge rewards. This is in contrast to other stablecoins like USDT, where users do not receive any dividends. In traditional finance terms, any currency issuance would incur a seigniorage tax, and existing stablecoins like USDT do not share this. USDe immediately takes out the seigniorage income. This alone is enough to attract large institutions to participate. After all, when MakerDAO achieved a yield of 8%, the market took off directly, not to mention that the yield of sUSDe (pledged USDe certificate) once exceeded 30%.

For $ENA, it is the platform governance token of the project. While the project earns basic income from pledging USDe, it also rewards ENA tokens. Conversely, if you hold ENA, you can also participate in pledging and increase the rewards for pledging USDe.

Fundamentally, USDe has built a stablecoin architecture entirely based on ETH as the underlying asset. Its core anchor is to maintain the value of collateral through derivative futures contracts, serving as a key model. To attract users, the investment portfolio's earnings are fed back to the users who mint stablecoins, allowing users to not only enjoy the stability of the stablecoin's price but also the dividends of seigniorage. Additionally, the issuance of the platform token ENA allows users to earn ENA by pledging USDe, and conversely, increase the rewards for pledging stablecoins. It has Pareto properties, but it is not a simple Pareto, as its core profit model is a term arbitrage. As an individual, you can also use this method. ENA simply aggregates everyone's funds to achieve greater collective returns.

Profit model of USDe:

The minting of USDe itself requires the user's stETH, combined with short positions in perpetual contracts. There are two parts to the earnings: stETH staking rewards (APY 3%-4%) and funding rates from short positions in perpetual contracts. The funding rate mechanism for perpetual contracts is simple, aiming to flatten the contract and spot prices. In a bull market, the funding rate for long positions is generally relatively high (APY 25%), to attract counterparties. This is the project's main source of profit. It's worth noting that the stETH is not stored on a regular CEX but on custodial platforms like Cobo and CEFFU to prevent misappropriation or CEX defaults.

Core risks of USDe:

As a stablecoin collateralized by crypto assets, the basic model of USDe is term arbitrage, where the value of the collateral is essentially spot ETH and the corresponding short position. In a bull market, it is basically 100% fully collateralized, not to mention the circulating market value of ENA itself, meaning that there is currently no risk of default. However, there is an exception, which is the decoupling of ETH's LST collateral (stETH) from ETH itself. The biggest risk is the issue of scale limits. If the short position ratio on a single exchange is too large, it may face a lack of counterparties, leading to a decrease in funding rate income. Based on the current market situation, the safe minting limit is approximately $10 billion. Another risk is the sustainability of staking rewards, which is a clear and obvious issue. There is also the custodial model of ENA, which theoretically carries the risk of misconduct or even bankruptcy, leading to a series of leveraged liquidations. Finally, the biggest risk is the risk of the project team running away with the funds.

3) Summary of the Stablecoin Race for Crypto Asset Collateral

Compared to fiat-collateralized stablecoins, crypto asset-collateralized stablecoins do not depend on specific scenarios or centralized exchanges. Both DAI and USDe have followed a highly consistent path to success, driven by wealth effects and transparent management. Both DAI and USDe were born in a bull market and grew rapidly. Thanks to the bull market growth, stemming from the DAI lending protocol, it has given retail investors the opportunity to leverage and earn higher returns. Additionally, compared to fiat-collateralized stablecoins, crypto asset-collateralized stablecoins generally offer basic deposit returns, serving as an anchor to attract customers and can be considered as interest-bearing assets. The wealth effect brought about by high returns is the main reason why crypto collateralized stablecoins can thrive and spiral upwards. In contrast to USDT and USDC, which do not offer interest dividends for holding and may also suffer from asset depreciation due to changes in the USD exchange rate or inflation.

3. Unsecured/Algorithmic Stablecoin (FRAX)

The last peak of algorithmic stablecoins was UST, an algorithmic stablecoin created by LUNA, which ultimately collapsed due to its Pareto mechanism. As of now, there has not been a popular algorithmic stablecoin in the market, and projects like FRAX are currently lukewarm. Algorithmic stablecoins come in two modes: single-token and multi-token. The former was the main mode in the early days of algorithmic stability, such as AMPL and ESD. The latter is mainly represented by FRAX (a hybrid algorithmic stablecoin). The biggest drawback of single-token pure algorithmic stablecoins is that unless designed as a Pareto model (high yield), they can hardly form a good scenario for growth, and due to the extreme volatility of the crypto market, it is difficult to instill confidence in the algorithm itself. Based on this, FRAX has developed a model of hybrid algorithmic stablecoins.

FRAX has designed a relatively complex hybrid stablecoin model based on collateral and algorithms. The main collateral consists of USDC and FXS (the project's governance token). Its core focus is based on arbitrage trading.

The main operating logic is:

When the protocol first launched, minting 1 FRAX required 1 USDC. As market demand for FRAX increased, the USDC collateral ratio decreased, adjusted to 90%, meaning that minting 1 FRAX only required 0.9 USDC, while burning 0.1 FXS token. Similarly, redemption would return 0.9 USDC and 0.1 FXS. This stable model fundamentally relies on arbitrage trading. If FRAX is less than $1, arbitrage trading will buy FRAX and then redeem USDC and FXS, simultaneously selling FXS for profit. As demand for FRAX in arbitrage trading increases, the exchange rate can be restored. The latest second version of the project has introduced an algorithmic market controller (AMO). The main improvement is that, under the premise of a 1:1 peg to the U.S. dollar, the protocol's collateral is placed in other DeFi protocols to earn revenue.

Main profit models: Fees for stablecoin minting and burning, revenue from various DeFi protocols under the AMO mechanism, and FRAX lending. Additionally, assets such as staked ETH can be used for collateral nodes to earn returns. The current total market value exceeds $600 million. Core bottleneck: Compared to USDC/USDT and DAI, even though FRAX has increased security through semi-collateralization, its upper limit is currently limited due to scenario restrictions (arbitrage within the ecosystem). This is the main bottleneck for algorithmic stability, and how to expand its application scenarios in the cryptocurrency ecosystem.

4. Outlook on the Stablecoin Race and Thoughts on Hong Kong Stablecoins

1. Advantages and Disadvantages of Different Types of Stablecoins

Whether fiat-collateralized, crypto-collateralized, or unsecured algorithmic stablecoins, they each have their own advantages and disadvantages in terms of decentralization, capital efficiency, and price stability, as well as their key developments.

2. Summary of the Stablecoin Race

A review of the stablecoin race shows that whether fiat-collateralized, crypto-collateralized, or algorithmic stablecoins, they all rely on support from application scenarios. They either have sufficient convenience and credit endorsements, or the use of their stablecoins within the scenario can earn returns for users. The rise of USDC proves the importance of regulatory endorsement, while the rise of FDUSD demonstrates the importance of scenario-driven traffic from exchanges. The rapid eruption of USDe once again proves that the most powerful driving force for cryptocurrency projects is the wealth effect.

Based on the above analysis, for a stablecoin project to seek market recognition, its path is relatively clear in the current market landscape.

1) For fiat-collateralized stablecoins: Two essential conditions for success are regulatory compliance and trust, and scenario endorsement brought by exchanges/payment institutions. Both are indispensable.

2) For crypto-collateralized and algorithmic stability: Two essential conditions for success are basic yield/high yield to address users' demands for efficient turnover of crypto assets, and continuous expansion of DeFi/payment application scenarios. If a stablecoin project has the above two points, it has the initial potential for success. In addition, the project team always needs to seek a balance between capital efficiency, value stability, and decentralization.

3. Thoughts on Hong Kong Stablecoins

For Hong Kong, aside from pegging to the US dollar, there are remaining options to peg to the Hong Kong dollar and offshore RMB. Apart from the rigid regulatory issues, purely from the stablecoin minting perspective, there are almost no difficulties at the practical level. However, the more challenging aspect is the application scenario after minting (or the circulation issue). If it cannot be used for large-scale real-world payments or cross-border exchanges, even with cooperation from major exchanges, there are still significant obstacles, given the stronger credit and circulation of the US dollar. From a regulatory perspective, the regulatory framework for stablecoins in Hong Kong will sooner or later be introduced, especially after the implementation of the virtual asset framework in 2023, making the trend of stablecoin regulation relatively clear. If pegged to the Hong Kong dollar, it can be expanded in the following areas:

1) Introducing the interest-bearing effect of crypto assets into fiat collateral. That is, using the returns from the collateralized assets in Hong Kong dollars to distribute dividends to users, gaining early trust from users.

2) Hong Kong dollar stablecoin payments. Expanding it into a payment tool rather than just a trading medium, including cross-border trade settlements in Hong Kong dollars. Additionally, since the Hong Kong dollar is pegged to the US dollar, if it is not a profitable financial product/payment tool, its necessity and attractiveness are almost minimal. In addition to the Hong Kong dollar, Hong Kong also has over 10 trillion offshore RMB and RMB assets (including offshore RMB bonds), with offshore deposits of nearly 1.5 trillion, mainly concentrated in Hong Kong, Singapore, and other places. In fact, offshore RMB stablecoins are not new, such as TCHN launched by Tron, CNHT launched by Tether, and CNHC issued by CNHC Group (the project was arrested in mainland China in 2023, but not because of the stablecoin project). The main reasons for their lack of growth are, on the one hand, the uncertainty of the regulatory framework in Hong Kong, and on the other hand, the lack of a suitable entry point. For offshore RMB, the key points are as follows:

1) Offshore RMB is not subject to domestic and foreign exchange controls, but the issue of asset ownership is still a barrier. Starting from the People's Bank of China, the most important thing is the legal status of the RMB. If it is only pegged to offshore RMB, it is beneficial for the internationalization of the RMB, and more importantly, it is beneficial for activating the vast offshore RMB assets. The biggest bottleneck at present is that most holders of offshore RMB are mainland Chinese, which still poses significant operational challenges and obstacles.

2) Endorsement by institutions such as Bank of China Hong Kong. Bank of China Hong Kong is the clearing bank for offshore RMB. If an offshore stablecoin is issued, subsequent clearing and custody tied to Bank of China Hong Kong can solve its core trust foundation.

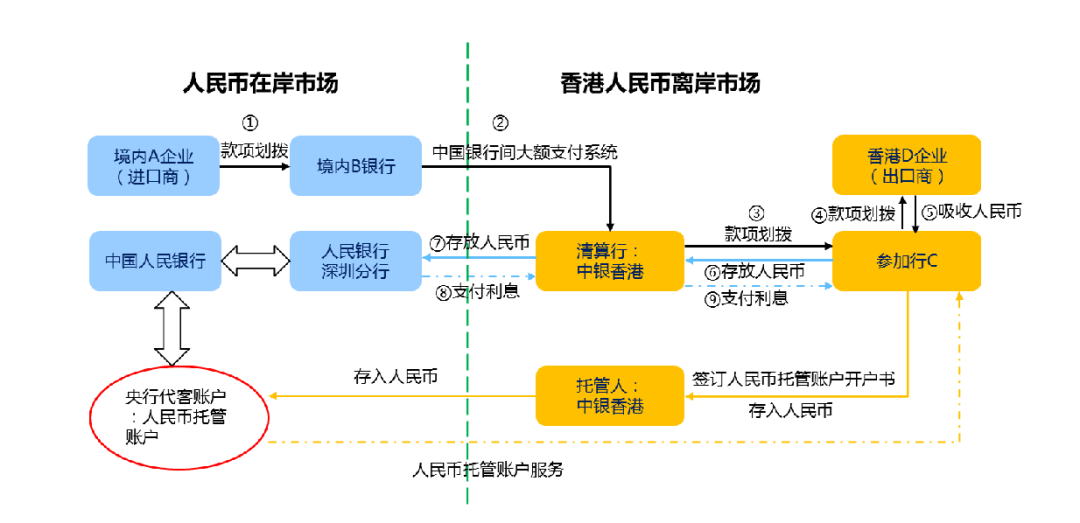

Chart 15: Cross-border trade flow of onshore and offshore RMB

3) Expanding the payment and procurement scenarios under cross-border trade will be the core application of offshore RMB. Currently, offshore RMB (CNH) mainly comes from cross-border trade, procurement, and payments, which then accumulate in Hong Kong/Singapore, especially in countries along the Belt and Road. From the perspective of global offshore US dollars, most countries are very short of US dollars, and combined with the instability of many countries' currencies, trade with China will result in the accumulation of RMB. By trading pairs of offshore RMB stablecoins/USDC, the channels for the exchange of RMB to USD in Belt and Road countries will be significantly improved. In addition, in terms of payments under trade, cooperation with cross-border payment institutions can explore payment scenarios for e-commerce, gaming, and commodity trading.

4) It can attempt to build a unique income model for offshore RMB. In addition to traditional minting and redemption fees, the key is how to return users' expected earnings. It can also attempt to mix RMB collateral with USD collateral to achieve exchange rate neutrality, achieve higher stability, and obtain two-way short-term financial returns on assets, serving as the basic income for stablecoins. In addition, it can consider issuing tokenized offshore bonds for domestic high-grade credit entities (RWA) overseas, as another anchoring direction for stablecoin income (similar to DAI), including the offshore RMB foreign exchange derivatives market. In addition, the issuance of offshore bonds, as high as 300 billion yuan per year, can also be tokenized.

In summary, currently, the biggest challenge for both Hong Kong dollar stablecoins and offshore RMB stablecoins is not in issuance, but in the design of application scenarios. Looking at future trends, offshore RMB has a more extensive application space and scenarios compared to the Hong Kong dollar. If it is strongly anchored to the RMB and regulated within the Hong Kong framework, it will not directly conflict with the legal status of the RMB. On the positive side, it can expand the convenience of offshore RMB payments (no need to open a bank account, pay anytime, anywhere), while also enriching the global issuance of domestic RMB assets and greatly expanding the global flow of domestic RMB assets. In the current period of tightening foreign exchange controls and economic downturn, it has a certain policy space and acceptance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。