Author: Armonio, AC capital, Twitter: @armonio_liang

Abstract

In this article, we propose two interrelated theoretical logical clues: the first clue traces the evolutionary process of DeFi liquidity technology, while the second describes the transformative impact of on-chain barter from the perspective of economic development history. The original intention of this article is to confirm that a profound DeFi revolution is imminent: just a little more patience is needed. Those visionary builders who can persist in idealism will eventually receive market rewards.

We carefully track the development of the decentralized exchange (DEX) market to illustrate that the emergence of on-chain barter trading is not accidental, and on-chain barter trading is a true game-changer. It represents an important chapter in the history of Web3 builders. Achieving its function requires a lot of innovation and improvement, not only within DEX, but also at the underlying infrastructure level.

If on-chain barter becomes a significant milestone in history, we believe that all relevant efforts and contributions should be appropriately commemorated.

01 Have we lost control of the rhythm of the cryptocurrency industry?

Since January 2023, driven by ETF approval and new quantitative easing expectations, Bitcoin has fallen to a low and rebounded to a new high. However, the prices of most altcoins did not perform as strongly as before, showing stronger upward momentum after Bitcoin created room for imagination. Some investors, due to the high valuation and low liquidity of VC tokens, mocked real innovation and viewed the crypto world as a criminal domain. At certain industry conferences, individual industry leaders even bluntly referred to the entire industry as similar to a casino. Many crypto enthusiasts are intoxicated by the excitement of PvP (player versus player). The overall market performance shows that memecoins are sought after in the early stages of a bull market, while value tokens are overlooked, absent from the entire bull market cycle.

In this bull market, many veterans feel that this time is indeed different, even surpassing the industry chill of 2018-2019. Some developers are confused, starting to question the original intention of entering the industry: can cryptocurrency really change the real world? Since last year, with the rise of AI, many people have shifted their focus to artificial intelligence, while many others remain hesitant.

Why is this cryptocurrency market different this time?

We cannot ignore the influence of venture capital, team greed, misaligned interests, unethical behavior, and short-term thinking in the market. The market has long been in the dark forest. Apart from the code, there are not many rules to regulate participants. Although these issues have existed for a long time, they are not enough to explain the weakness of this bull market.

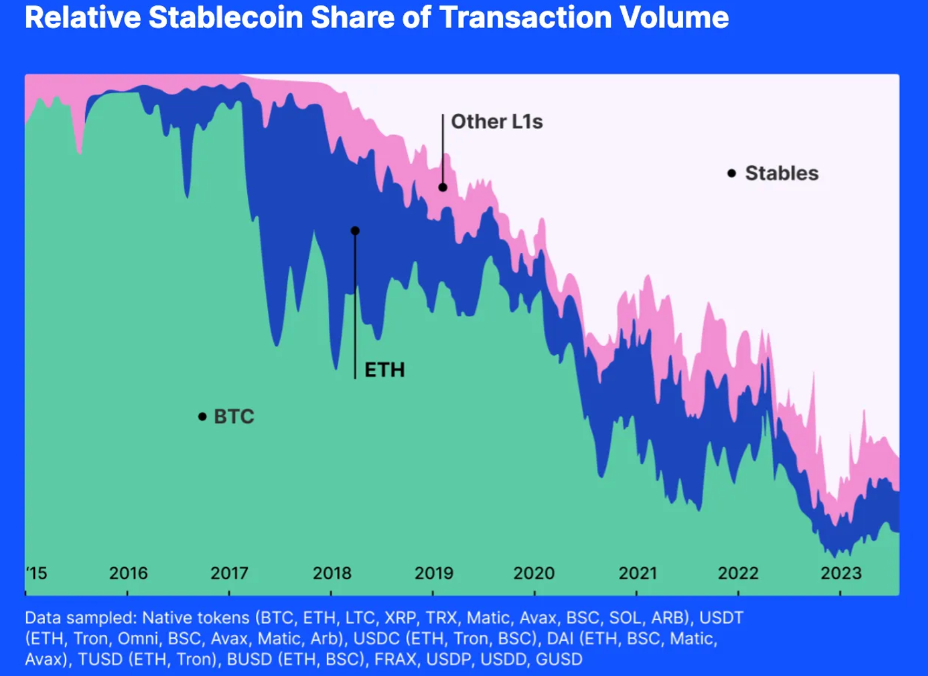

Therefore, we propose an additional reason: the self-inflation within the crypto market is no longer sufficient to provide the necessary liquidity for our crypto ecosystem. Please refer to the following chart:

(Resource: https://www.fixing.finance/report/the-future-of-stablecoin-design)

The chart shows the activity of various crypto equivalents. It can be seen from the chart that since 2018, non-stablecoins have continuously declined in market share. In terms of trading volume share, in the past one or two years, the vast majority of trades have been provided by USD stablecoins. If the market value of USD stablecoins cannot continue to expand, liquidity pools will be drained as new coins continue to be issued.

In the past, Bitcoin and Ethereum were to a large extent the general equivalents in the market. Bitcoin and Ethereum could serve as liquidity for others, and during the bull market phase, altcoins and mainstream coins serving as liquidity would spiral upward, mutually promoting each other. In such a market structure dominated by tokens themselves providing liquidity, altcoins rarely lacked liquidity. Now, most trading pairs are pegged to USD stablecoins. Even with the explosive growth in the value of Bitcoin or Ethereum, the status of stablecoins makes it difficult for BTC and ETH to inject liquidity into other tokens.

The pricing power of cryptocurrencies falls into the hands of Wall Street

All USD-pegged stablecoins and other compliant financial instruments are bait. Cryptocurrencies follow the Wall Street clock.

In October 2014, Tether began offering a stable digital currency to bridge the gap between cryptocurrencies and fiat currencies, providing the stability of traditional currencies and the flexibility of digital currencies. Now it has become the third largest token by market value. In addition, USDT has the most trading pairs in the index, ten times that of Ethereum or wBTC.

In September 2018, Circle partnered with Coinbase to launch USD Coin (USDC) under the Centre Consortium. It is pegged to the US dollar, with each USDC token pegged to the US dollar reserve at a 1:1 ratio. As an ERC-20 token, USDC can seamlessly trade and integrate with various decentralized applications.

On December 10, 2017, the Chicago Board Options Exchange (CBOE) pioneered Bitcoin futures, which, even if settled in USD, can still impact the spot price of Bitcoin, especially since Bitcoin's open interest now accounts for 28% of the global market.

Wall Street not only physically influences the crypto market, but also psychologically affects the liquidity in the crypto market. Do you remember when we started paying attention to the attitude of the Federal Reserve, Grayscale's trust write-downs, the "dot plot" of the FOMC, and the cash flow of BTC-ETF? All this information psychologically affects our behavior.

Stablecoins are the bait thrown by the US government. Since we accepted stablecoins pegged to the USD as a means of providing liquidity, it has begun to accumulate consensus, replacing the liquidity role of native crypto tokens, competing with and weakening the credit of other tokens, and gradually dominating the general equivalent market.

As a result, we have lost our market rhythm.

I am not blaming stablecoins pegged to the USD. On the contrary, this is the natural result of fair competition and market choice. Tether and Circle help investors directly invest in USD-pegged assets on-chain, allowing them to bear the risk equivalent to the USD, and providing investors with more choices.

The market is struggling for liquidity! Losing control of liquidity means losing control of the rhythm of the cryptocurrency industry.

02 The Millennium War of Liquidity

Liquidity has always been a real demand

Liquidity is a fundamental feature of the market, and any innovation that can improve market liquidity is a significant historical progress.

According to organizational theory, the market is defined as a structured environment for the exchange of goods, services, and information between buyers and sellers. This environment is guided by established rules, norms, and institutions to facilitate coordination, reduce transaction costs, and support efficient economic interactions.

Liquidity is crucial for market organization because it directly affects the efficiency, stability, and attractiveness of the market. High liquidity reduces transaction costs by minimizing slippage and increasing trading volume. Markets with high liquidity also exhibit greater price elasticity, better prices, attract more participants, and help find more accurate price information. Information economics emphasizes the role of the market in information discovery. In an ideal market, information flows freely, enabling participants to make wise decisions, optimize resource allocation, and achieve equilibrium prices. A market with high liquidity will generate reliable information, helping to allocate resources more effectively.

Whether it is price discovery efficiency, price stability and resilience, or lower transaction costs, these features enhance the ability of the market to attract participants. Market attractiveness further enhances market liquidity, improving the efficiency of all aspects of the market. Therefore, improving liquidity is essential for any market.

Currency is an innovation to alleviate liquidity problems

Academically, there are two mainstream theories about the origin of money. One view is that money is a convenient medium of exchange, accepted by the general public and scholars; the other comes from David Graeber's "Debt: The First 5000 Years," in which he believes that money originates from debt relationships, but also acknowledges the universal equivalent role of money.

In addition to Green Davis's "The History of Money: From Ancient Times to the Present" and Karl Marx's "Capital: Volume I," there are other sources that hold similar views on the origin and evolution of money.

For example, in "The Ascent of Money: A Financial History of the World," Niall Ferguson points out that the development of money also originated from the society's need for an efficient exchange system, starting from barter and gradually evolving into a more complex system using items with intrinsic value.

Similarly, in Felix Martin's "Money: The Unauthorized Biography," the author also discusses money as a concept of social technology, developed out of the need for a more efficient exchange system. Like Marx, Martin believes that money is a universal equivalent, originating from a common commodity in the barter era.

Finally, David Graeber's "Debt: The First 5000 Years" presents a unique perspective, suggesting that money evolved from systems of debt and obligation, which appeared before the invention of money itself. However, Graeber's viewpoint still aligns with the core idea that money was created as a universal equivalent to facilitate the exchange of goods and services.

These resources further emphasize the role of money as a medium of exchange, echoing the views of Davis and Marx.

In summary, the academic consensus on money is that its function after its birth is as a general equivalent, a product of solving market liquidity. The disagreement lies in whether the starting point of the carrier of money is commodities or debt.

Money was the ancient elites' answer to the problem of market liquidity before the emergence of the value internet, and it was a means to increase liquidity.

The old forces that equated money with liquidity rarely attempted to improve the organizational structure of the market to achieve better liquidity conditions. They never considered how to build market liquidity without money. Perhaps it's because they, like fleas trapped in a covered box, have been there for too long and forgotten how high they can jump.

DEX: The Power of Change

The primary goal of any market is to provide the most accurate prices and the most efficient allocation of resources. Every component, mechanism, and structure is designed to achieve this goal. Throughout history, humans have continuously created new methods to improve market efficiency.

Over the centuries, the market has undergone significant changes. The price discovery mechanism has undergone multiple upgrades. To meet different economic needs, the market has developed various settlement procedures, such as dealer markets, order-driven markets, broker markets, and dark pools.

With the emergence of blockchain technology, we have encountered new constraints and touched on new opportunities to solve the liquidity problem. Here, we can create innovative methods to address exchange demands and provide liquidity for tokens.

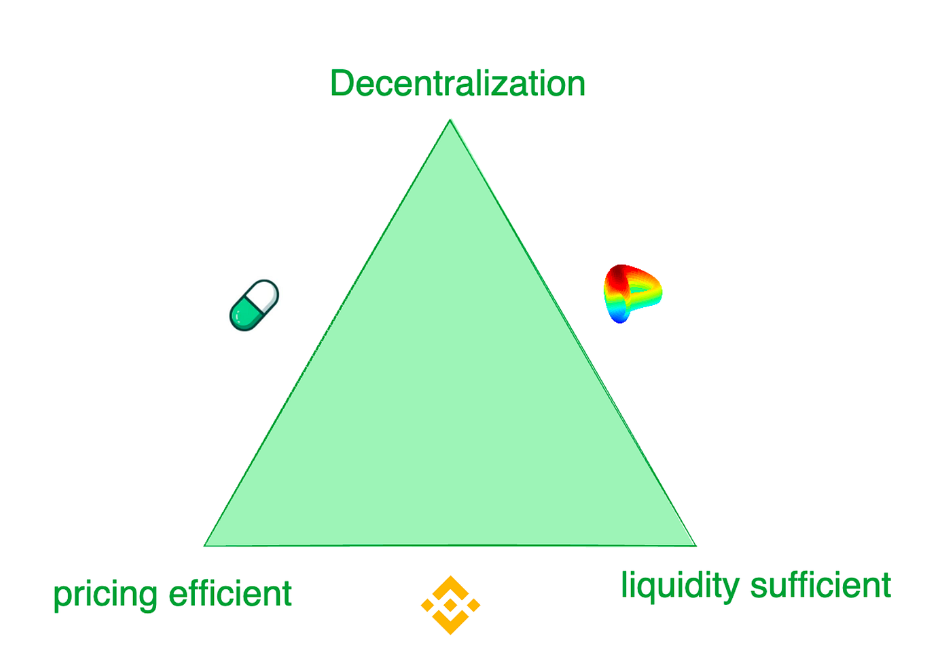

In summary, contemporary token exchanges face a trilemma: 1) adequate liquidity, 2) effective pricing, 3) decentralization.

The trilemma of exchange

While centralized exchanges represented by Binance provide the best trading experience, their users are also plagued by fraud risks and monopolistic exploitation. Even the former world's second-largest exchange FTX is currently undergoing bankruptcy liquidation due to misappropriation of user assets. However, exchanges with slightly better liquidity have to pay hefty listing fees to the project party, as well as other stringent terms. In contrast, decentralized exchanges are more flexible, designing different mechanisms to cater to different demand scenarios. For example, Pionex is known for providing an extremely sensitive token supply curve, while Curve provides the best liquidity in most cases, rather than price discovery sensitivity. These exchanges adopt various models to meet the trading preferences of their target customers. It is undeniable that each has its own focus and sacrifices.

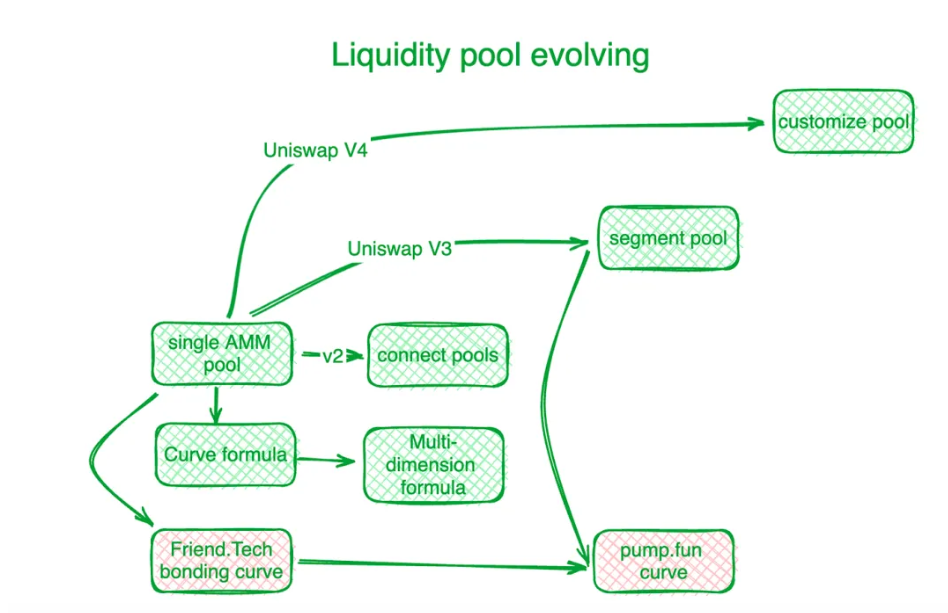

Attempts to Create On-Chain Liquidity

Decentralized exchanges have made significant progress in solving this trilemma and other on-chain trading challenges through innovation. The first step in the long march is to establish on-chain liquidity. Here is a simple industry overview: Uniswap is the benchmark in this segment. The innovation of Curve Protocol marks the beginning of a new era. Before Uniswap's "X*Y=C" curve, decentralized exchanges used order books to settle on-chain trading demands. The subsequent Automated Market Makers (AMMs) followed Uniswap's exploration direction, creating liquidity pools. In Uniswap V2, the liquidity in different trading pairs' pools is connected through algorithms. Uniswap V3 introduced segmented liquidity pools, allowing users to define price ranges where they want to provide liquidity. Uniswap V4 further advances this by providing customized solutions for liquidity pools.

For assets with relatively stable trading prices, the market demands more concentrated liquidity supply. Curve Protocol, which focuses on stablecoin trading, developed its own supply liquidity curve to provide more token liquidity near predetermined balance points. To address the challenges of joint liquidity pools, Curve Protocol invented a multi-dimensional formula that allows users to place more than two tokens in a liquidity pool, thereby sharing liquidity among all tokens in the pool. In practice, centralized exchanges (CEX) demonstrate better liquidity and pricing efficiency. On-chain pricing systems typically lag behind off-chain CEX. Hashflow, with the help of oracles, has established a Professional Market Maker (PMM) pool to connect on-chain and off-chain liquidity.

However, for small-scale tokens, traditional joint curves are costly, and the contradiction of liquidity fund costs is more prominent. Friend.tech designed steeper joint curves to accommodate small investors who prefer price increases over sufficient liquidity. As the value scale of tokens increases, investors' preferences shift towards liquidity. Inspired by this, Pump.fun uses steep curves when the token value is low, but as the value increases, the curve changes to different slopes or even different curves.

Evolution of liquidity pools

MEV, the Race for On-Chain Liquidity

MEV is another arena for decentralized exchanges.

Maximal Extractable Value (MEV) refers to the profit that miners or validators gain from their ability to include, exclude, or reorder transactions in the blocks they generate. It can be seen as a liquidity cost. In liquidity pools, each exchangeable token (liquidity) is distributed along a price scale, and the liquidity for each price span is limited. Those who can interact with liquidity pool contracts earlier gain an advantage by obtaining better prices. Thus, MEV is inherently linked to the liquidity problem.

The form of MEV in decentralized exchanges is to gain advantageous liquidity by sorting transactions. This competition improves the efficiency of on-chain transactions but also harms the interests of all parties. To retain as much trading value as possible in decentralized exchanges and return it more completely to participants, developers have built algorithms and mechanisms at the application layer to intercept MEV generated by transactions.

Flashbots, as a veteran in the MEV management field, focuses on the distribution of node profits. To ensure transparent and efficient MEV distribution, they have established a MEV auction system at the node level. Eden Network pursues similar goals. KeeperDAO combines MEV extraction and staking, allowing participants to benefit from MEV while protecting users from its negative impact. Jito Labs, a liquidity staking project on the Solana network, also addresses this issue.

Cow Protocol, as a leading project, including UniswapX, 1inch Protocol Fusion, etc., uses auction interaction rights to retain MEV within the trading process, rather than allowing this value to flow to the node accounting level. Intercepting MEV protects active traders and AMM liquidity pools, eliminating the dilemma of MEV loss due to DEX bribing nodes.

Decentralized Liquidity Calls for AGENT to Solve the Problem

As mentioned earlier, token liquidity is dispersed in various customized pools controlled by different protocols on different blockchains or Layer 2 solutions. Polygon has proposed an aggregation layer concept to collect liquidity from different layers. Initially, some decentralized exchanges (DEX) aggregators emerged to integrate liquidity from these different pools. However, after accumulating enough traffic, a more effective approach is to create platforms that facilitate competition, such as 1inch and Cow Protocol.

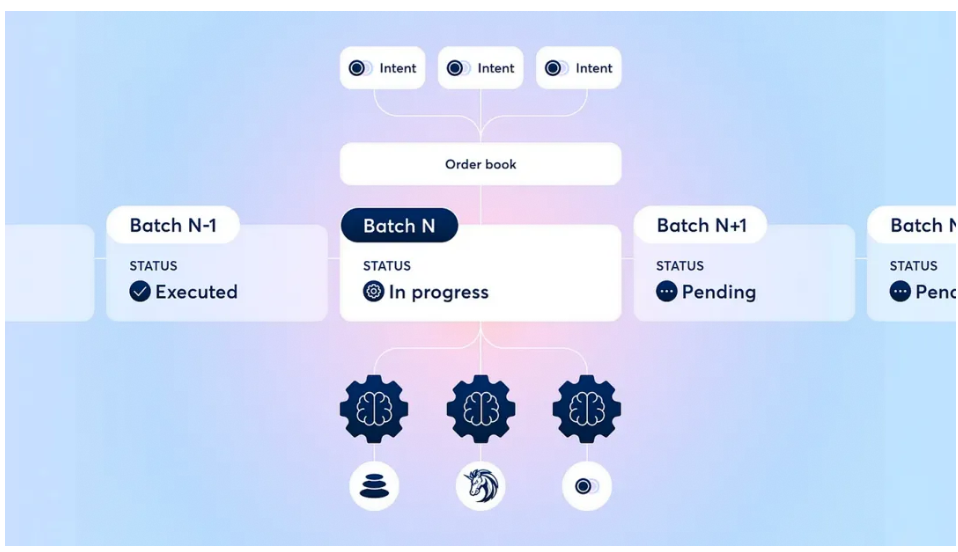

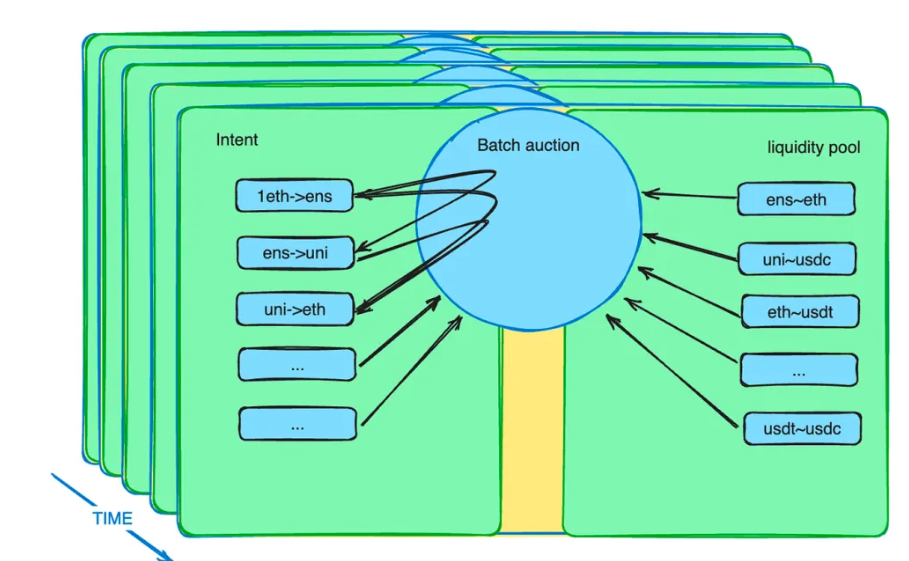

Furthermore, batch auction mechanisms enhance the role of agents. It introduces a new market mechanism to alleviate liquidity constraints. In practice, traders can place orders at a limited price within a specified period. Batch auction smart contracts collect these orders and bundle them into a batch. Then, the smart contract allows agents to bid on these batches. The agent offering the best price will win the opportunity to settle all potential trades within that batch.

Explanation of Cow Protocol's Batch Auction Mechanism

Draft of the batch auction from Cow Protocol

Batch Auction: The Culmination of DEX Development

After years of DEX development, the industry has embraced methods such as batching, auctions, and order matching to optimize trading outcomes for all participants. The specific implementation of auction mechanisms varies, but in general, they transfer the complexity of optimizing exchange outcomes to professional participants and redistribute the remaining portion to relatively inexperienced traders.

Illustration of batch auction

This type of auction can address many challenges faced by DEX from multiple perspectives.

In addition to the MEV redistribution mentioned earlier, batch auctions can do much more. Traders send intentions to smart contracts rather than instructions. These intentions can last for several minutes. These intentions are packaged into a batch and proposed to a group of competing specific trading agents. We know that there are a massive number of intentions, and liquidity pools come in various forms, making optimization a challenge. By entrusting professionals with professional tasks, system efficiency can be improved.

Batch auctions maximize value efficiency by sacrificing time efficiency (each trade intention defaults to lasting several minutes), differentiating from CEX. Batch auctions can retain MEV in exchanges, benefiting all trading participants. Furthermore, batch auctions break down liquidity barriers between chains and between on-chain and off-chain by relaxing time constraints.

Moreover, barter is back on stage!

03 Barter Trade Returns to the Stage

As the ancestor of all cryptocurrencies, Bitcoin defines itself as a currency. Decentralized markets are a nascent field with no clear consensus constraints. Barter is a native trading mode for cryptocurrencies, naturally requiring no education for users.

Decentralized exchanges (DEX) are often referred to as "exchange" platforms. In their trading model, there is no predetermined universal equivalent role. Traders do not need to use fiat currency or stablecoins as intermediaries. At the liquidity pool level, any trading pair is allowed. Traders can use any tokens they like to exchange for other tokens and bear the cost of low liquidity efficiency.

However, relying solely on liquidity pools for barter trading has significant limitations. For all types of barter trading, there are not enough pairs. Due to the structure of liquidity pools, liquidity deployment takes a long time, making it difficult to find equilibrium prices. Therefore, liquidity must be deployed across a wider price range, leading to scarcity compared to the limited-time demand of intentions. This is where intentions and batch auctions come into play.

Assuming multiple potential trade intentions can meet each other's needs and are supplemented by liquidity from the pool. In this case, barter trading will return to the market in a more efficient state. With the improved scalability of web3 infrastructure and more commodities and financial instruments joining web3, batch auction smart contracts will capture thousands or even millions of trade intentions per second. Any token can serve as a means of settling other tokens. We will break free from the liquidity constraints imposed by the US dollar in a universal context.

Batch Auction: Key to On-Chain Barter

The revival of barter represents a renaissance. Its revival is not a creation out of nothing, but a response to market demand.

Historically, when money was invented, traders found it difficult to find direct barter opportunities to meet their immediate needs. Therefore, they exchanged commodities for a universal equivalent (money) and then bought what they truly needed in another transaction. Once this exchange mode was widely accepted, it forced genuine barter demand to be divided into at least two steps, and the direct barter market was completely replaced.

Today, on-chain barter demand exists in the form of short-term intentions. Batch auction smart contracts collect these intentions. Anyone, whether human or AI agents, can meet the entire trading demand by offering the best bid. If intentions match, stablecoins pegged to the US dollar are not needed. Tokens retain their utility and share liquidity as before. This matching of barter demand is based on a global market and stronger information matching capabilities, extending from the tradition of cryptocurrency barter culture.

In the short term, the existence of intention time spans allows arbitrageurs to transfer liquidity across chains and from off-chain to on-chain. For example, an algorithm that discovers price differences between different chains or between DEX and CEX can buy at a lower price and sell at a higher price within a specified time. It may require using financial instruments to hedge market risks to achieve a risk-free state. However, in the future, when on-chain, off-chain, and cross-chain transactions can be synchronized, all transactions can be executed simultaneously. This can eliminate the cost of risk and provide the best experience for traders.

Why is it said that Barter under BATCH AUCTION is a Milestone of the DEX Era?

The reason is simple. If we look back at the history of money, the right to coin money was initially private. According to "Debt: The First 5000 Years," debt could be personal. Even in modern times, as detailed in "A Monetary History of the United States, 1867-1960," private individuals could mint silver coins. However, today, all credit is issued by the Federal Reserve. Even Bitcoin is priced in dollars, which is unfortunate for the times. The dollar has overshadowed the brilliance of cryptocurrencies. Barter trading provides an opportunity to reclaim this status, highlighting the importance of the revival of barter.

The development of decentralized exchanges (DEX) gives us confidence that we can eventually surpass centralized exchanges (CEX). In the last DeFi summer, it was widely believed that DEX would eventually surpass CEX at the right time. How many people still hold this belief today? If we study the development of DEX, the introduction of batch auctions is not a coincidence. It is a deliberate step towards solving the liquidity problem, a phased achievement of continuous technological iteration for DEX. DEX has evolved from merely having liquidity pools to becoming a comprehensive liquidity system with different participant roles, specialized components, and permissionless composability. This progress has been achieved through the efforts of predecessors. Relaxing time constraints and creating differentiated conditions from centralized exchanges show us more possibilities. It even restores my confidence in DEX surpassing CEX.

A business cycle has passed, and although the appearance of DeFi giants remains unchanged, there has been a transformation internally. Batch auctions are an important milestone, as important as the invention of liquidity pools. I believe they can realize the dream of DEX surpassing CEX. When barter trading becomes the primary trading mode again, we can regain control of our market rhythm.

04 Afterword

In discussions about the future with many industry leaders, I found a general sense of confusion in the market, with a lack of emphasis on technology leading to a lack of confidence among many.

I still remember the end of 2018 and the beginning of 2019, when I was having hotpot in Chengdu with a friend, talking about the bright future of DeFi and Ethereum. He talked enthusiastically about the future of DeFi and Ethereum, even though the price of ETH was less than $90 at the time, his eyes were shining with excitement.

Think about it, when did the industry fall to the point where it needed speculators' wallets to define it?

Decentralized exchanges (DEX) are just a small part of the vast DeFi industry. If we look closely, we will find significant and exciting progress in DeFi, and even in other fields. As long as technology continues to advance and develop without stopping, what do we have to worry about? Dreams will definitely come true.

For all the industry builders who are forging ahead, I have only one line of ancient Chinese poetry to offer: "Do not worry that the road ahead has no companions, for who in the world does not recognize you?"

Thanks to the help of @Jialin, and the encouragement from @NewMingshiS and @0xNought, the Observer has completed the final observation record of the trip to Amed Beach in Bali.

References:

1. Debt: The First 5000 Years

2. Money: The Unauthorized Biography

3. The Ascent of Money: A Financial History of the World

4. A History of Money: From Ancient Times to Present Day

5. Das Kapital

6. The Future of Stablecoin Design

https://www.fixing.finance/report/the-future-of-stablecoin-design

7. Uniswap Labs and Across Propose Standard for Cross-chain Intents

https://blog.uniswap.org/uniswap-labs-and-across-propose-standard-for-cross-chain-intents

8. Understanding Batch Auctions

https://blog.cow.fi/understanding-batch-auctions-89f0f85e6c49#:~:text=A batch auction is a,rules that prevent MEV attacks.

9. Uniswap v2 Overview

https://blog.uniswap.org/uniswap-v2

10. Introducing Uniswap v3

https://blog.uniswap.org/uniswap-v3

11. Aggregated Blockchains: A New Thesis

https://polygon.technology/blog/aggregated-blockchains-a-new-thesis

12. A deep dive into 1inch Fusion

https://blog.1inch.io/a-deep-dive-into-1inch-fusion/

13. Priority Is All You Need

https://www.paradigm.xyz/2024/06/priority-is-all-you-need

14. Quantifying Price Improvement in Order Flow Auctions

https://blog.uniswap.org/UniswapX_PI.pdf

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。