Messari is very optimistic about the combination of AI and cryptocurrency, and also bullish on the three emerging narratives of DePIN, DeSoc, and DeSci.

Author: Messari

Translation: Deep Tide TechFlow

As scheduled, the well-known cryptocurrency data and research institution Messari has released "Messari Theses 2024." We have compiled and translated the first chapter, which covers the top ten investment trends for 2024.

In the author's view, "Web3" is a silly concept, and when people stop using this term and return to the narrative of "Crypto," the total market value of cryptocurrencies doubled.

In this year's investment trend forecast, Messari expresses strong optimism for Bitcoin, while at the same time, it is bearish on Ethereum, considering the "ultrasound money" narrative (referring to sustained deflation leading to continuous price increases) as nonsense. Compared to Solana, Ethereum does not have overwhelming advantages. Additionally, Messari is very bullish on the combination of AI and cryptocurrency. Based on the subsequent disclosure of analyst holdings, many people hold tokens such as AKT\TAO, and Messari also has high hopes for the three emerging narratives of DePIN, DeSoc, and DeSci.

Welcome to read the full article:

1.0 Investment Trends

In December of last year, I, representing everyone in the cryptocurrency field, abolished the term "Web3."

It is a nonsensical, PR-driven term that undermines everything interesting we are trying to build.

NFT PFP collections are Web3, "DeFi 2.0" is Web3, Sam Bankman-Fried is Web3…

In the crypto world, I want more things that are not entirely dependent on Ponzi schemes, such as personal wallets, transaction privacy, infrastructure progress, DeFi, DePIN, and DeSoc.

This year did not disappoint.

Since the cold-blooded murder of the word "Web3" (note: referring to the collapse of the scams representing Web3), the market value of cryptocurrencies has almost doubled. The biggest fraudsters in our industry are either in jail or on their way there.

Great products with smooth designs are being launched. And I am even more excited about the prospects for cryptocurrencies in 2024.

In short, the state of the crypto market is strong.

I realize that some newcomers may be reading this article, so I want to remind you that this is an advanced course, not an introductory course for beginners.

I assume you already have relevant knowledge, so I will be concise because time is a critical factor.

This "Investment Trends" section at the beginning is for those who want to tell their friends that they have read the entire report. I don't think it's necessary to start the victorious journey on the first three sections of my report from last year, but we see smooth performances in various market segments, and there is evidence to support the need for optimism after the long crypto winter.

We will start this article with the bull market case for Bitcoin in 2024.

1.1 BTC and Digital Gold

"Where are we now? It feels a bit like January 2015, or December 2018, more like selling a kidney to buy more Bitcoin."

The above is my view on Bitcoin in December 2022.

Although predicting Bitcoin's trading position in the short term is very difficult, its long-term attractiveness is almost indisputable.

We don't know if the Federal Reserve will further raise interest rates, or hit the emergency brakes, reverse direction, and start seriously implementing quantitative easing. We don't know if we will face a commercial real estate-driven recession, or if we will successfully achieve an "easy landing" for the economy after the post-COVID monetary and fiscal lashings. We don't know if stocks will fall or fluctuate, or if Bitcoin will prove to be related to tech stocks or gold.

On the other hand, the long-term argument for Bitcoin is straightforward. Everything is becoming digital. Governments are too indebted and spendthrift, and they will continue to print money until they fail completely. Investors can only obtain a total of 21 million Bitcoins. The most powerful MEME in the market is the upcoming Bitcoin halving in 2024, marking its quadrennial marketing event.

Sometimes you just need to keep it simple!

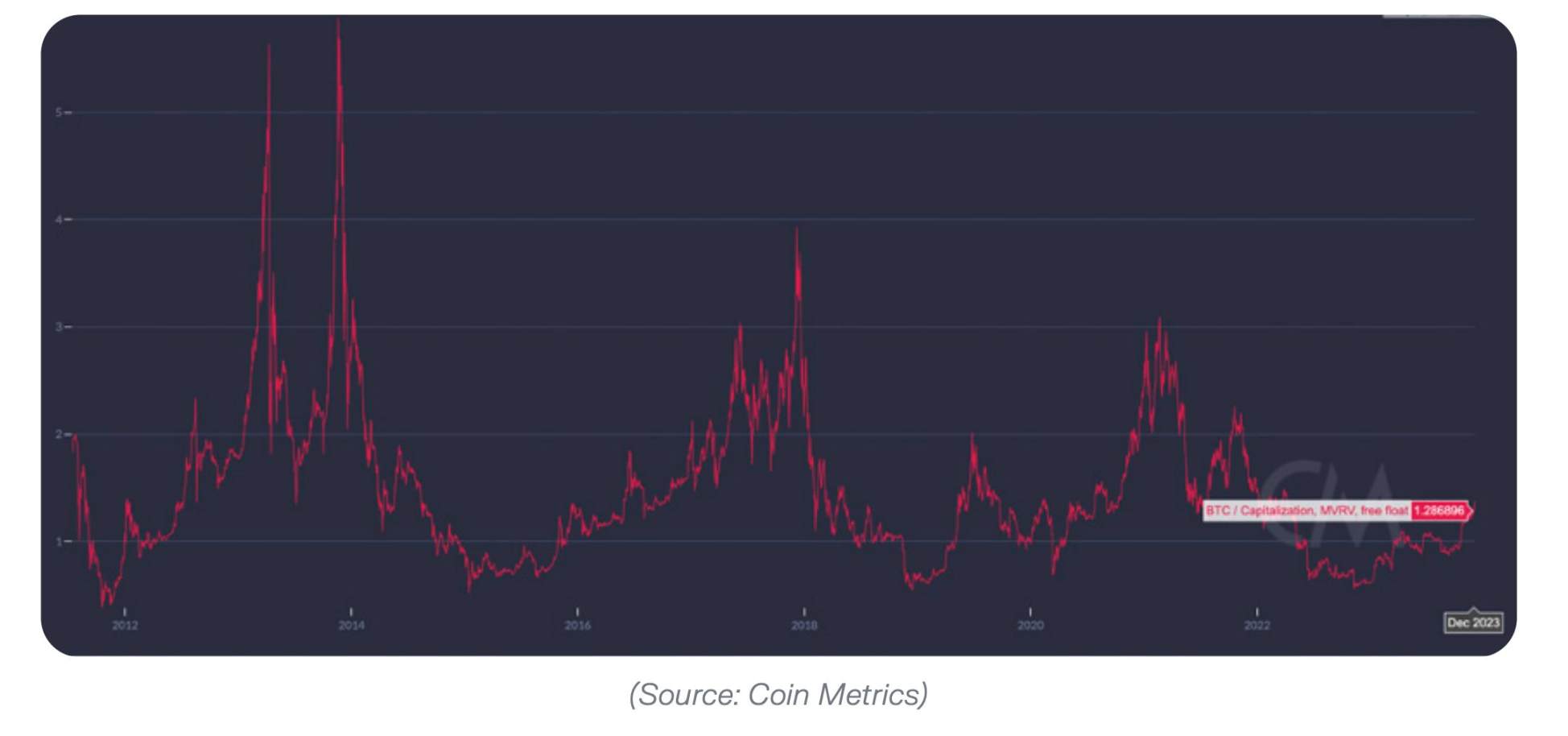

To maintain year-over-year consistency, let's revisit the MVRV chart that I wrote about last year, which made people want to sell their kidneys to buy in. Remember, the chart compares Bitcoin's current market value (MV, i.e., price * total supply) and realized market value (RV, i.e., the product of the price and the sum of the supply units moved on-chain at the last movement).

According to the theoretical calculation above, a ratio below 1 is the golden zone. Ratios above 3 always signal a peak in a cycle.

After a 150% increase this year, is Bitcoin still a good "buy" target?

The answer is somewhat affirmative.

Perhaps we are no longer in the deep value domain, but given some institutional tailwinds supporting us (ETF approvals, FASB accounting changes, new sovereign buyers, see Chapter 4.1), buying Bitcoin with an MVRV ratio of 1.3 is clearly no longer a blind leap of faith.

Please remember, as more Bitcoin is inevitably locked in ETF products, the MVRV ratio will be artificially inflated because the frequency of new buyers appearing on-chain is not as high as in trading records on the New York Stock Exchange and Nasdaq. A slightly higher than 1 MVRV ratio is just below the historical median.

You know what's more appealing if you are interested in cryptocurrencies as an asset class.

Bitcoin tends to lead the recovery. We have recently seen multi-year highs in Bitcoin dominance, but it still has not approached the highs reached at the beginning of the bull markets in 2017 and 2021. In 2017, Bitcoin's dominance shrank from 87% to 37%. In 2021, during its consolidation phase and before rising to $40,000, it regained 70% market share, then dropped to 38% at the peak of the bubble. We have just touched 54%. There is still room for consolidation.

To be honest, it's hard to see another catalyst for the cryptocurrency boom that does not start with Bitcoin's continuous surge.

DeFi faces continued regulatory resistance, which will limit growth in the short term. NFT activity is essentially dead. Other upcoming areas (stablecoins, gaming, decentralized social, and infrastructure) are more likely to rise slowly and steadily rather than sharply and suddenly.

Large fund managers also agree. Binance recently conducted some excellent research, showing that in the summer, the "Bitcoin" sentiment overwhelmingly dominated the "cryptocurrency" sentiment among asset allocators (although this sentiment may be changing with the poor performance of ETHBTC).

With this momentum, my bet is that Bitcoin's dominance will reach 60% again in the ETF-driven rally (leading the rise) or during severe macro pressures (consolidating in decline).

Even if I am wrong, we have already seen the high Bitcoin dominance of this cycle, and I think the likelihood of nominal and relative declines in Bitcoin prices is very low.

In the early stages of the cryptocurrency bull market, the play with the highest expected value has always been to bet on the leader, and this cycle is (and will continue to be) no different.

I will reiterate what I said last year: I find the argument for Ethereum as "ultrasound money" (note: referring to sustained deflation leading to price increases) completely unconvincing. If such a MEME had strength, then the liquidity data would not look like this, even after the approval of ETH futures ETFs:

We may not see another 100x increase in Bitcoin, but this asset is likely to surpass other mature asset classes again in 2024. The eventual parity with gold will push the price of each BTC to over $600,000. Remember: gold has many of the same macro bullish events, so that price may not be the limit.

If the currency crisis is severe enough, then cryptocurrencies will be worth something: 1 BTC will be worth 1 BTC.

1.2 Ethereum

In September 2022, Ethereum successfully completed the "Merge," and in April 2023, it completed the "Shapella" upgrade, both of which are among the most impressive technological upgrades in history. The "Merge" also ushered in a new era for Ethereum as a net deflationary digital asset. I like Ethereum and everything it has spawned. Without the crypto asset ecosystem built by Vitalik, Messari itself would not exist. But in the long run, the investment case for ETH is more like Visa or JPMorgan, rather than Google or Microsoft, or commodities like gold or oil. ETH is in a dilemma. Due to institutional allocators' interest in digital gold as a "pure play," BTC outperforms ETH in the cryptocurrency space, and widely available Ethereum alternatives (L0s, L1s, L2s) may perform well because of their absorption of on-chain transaction volume relative to the Ethereum main chain. I don't see ETH surpassing Bitcoin and upcoming high beta performance. That being said, nominally, I wouldn't be against ETH. It has withstood multiple technical challenges and market cycles. It has better supply dynamics than today's Bitcoin, one could argue. I agree that any ETH bridged to other Rollups may be gone forever, "won't come back to accept bids." Pessimism towards ETH is not a criticism of Ethereum, but a sober recognition that ETH has maintained a dominant position as an asset so far, making it difficult to continue holding over 60% of the market share among peers.

When I think about Ethereum and Solana, I think of Visa versus Mastercard, not Google versus Bing in terms of dominance. Even if I give ETH geeks a fair chance, I still have to point to relevant data metrics and note that ETH has a low risk-adjusted return compared to BTC.

I will discuss the technical aspects more later, but I know you're not sitting around the fireplace drooling over my views on sharding. What you want is not-so-smart bullish/bearish advice, and betting on ETH is right in the middle of the bell curve. I'm sure I'll be arguing about this with the folks at Bankless soon. (Note: Although I hate hedging, this firm view has weakened since I first drafted this section. With BTC now up about 150% and SOL up over 6x year-to-date, we are at a point where ETH needs some mean reversion, as it has been stablecoin for many months and significantly lagging.)

1.3 (Liquidity) Domain

Bitcoin (BTC), Ethereum (ETH), and USD-backed stablecoins now account for 75% of the overall cryptocurrency market of $1.6 trillion. However, this situation will not remain unchanged.

I founded a company based on the premise that the remaining 25% of the crypto market will achieve 100x growth in the next decade, requiring investors to conduct more sophisticated due diligence to analyze thousands of crypto assets, rather than just limiting themselves to two. Based on the current market size, this 100x growth in the "other domain" will slightly exceed the private capital market (20 to 25 trillion USD), accounting for about 30% to 35% of the global bond and equity capital markets.

More crucially, if you agree with my view that blockchain is essentially an accounting innovation, then eventually all assets will become "crypto" assets traded on public blockchains, rather than relying on traditional clearing and settlement systems, whether they are "utility tokens" or "equity tokens." Over time, the relationship between cryptocurrencies and traditional finance (TradFi) will become increasingly intertwined, eventually almost merging into one.

Of course, sticking to market-cap-weighted index investing in BTC and ETH also has its advantages.

First, from a historical perspective, this has been proven to be a successful strategy. If you had attended the North American Bitcoin Conference in Miami in 2014 and bought into the products recommended by Vitalik (Ethereum ICO and Bitcoin), you would have enjoyed 75% market growth over the past decade. These blue-chip assets have now become the most robust "hard investments" in the cryptocurrency market, as you don't have to worry about the risk of dilution over time.

In contrast, many other top projects have large financial reserves, and over time, these token reserves may be gradually sold off by insiders. Therefore, while their "market value" may rise, their token prices may remain unchanged or even decline.

Of course, this is not investment advice. But as a historical researcher, I understand:

A. Although BTC and ETH may be the current market leaders, they are not invincible forever;

B. Since 1926, although there are 26,000 stocks trading in the market, only 86 stocks have contributed to more than half of the value appreciation in the US market.

Many stock market leaders of the 1920s are no longer around, and the development of the cryptocurrency market will be no exception. So, what should someone like me who likes passive indexing do?

To be honest, there's not much that can be done at the moment. Existing crypto index product alternatives are not very appealing, and I doubt this situation will change in 2024.

A low-cost, auto-rebalancing index considering token oversupply and market liquidity would undoubtedly be an excellent investment tool. But to get index exposure at present, your choices are either paying high AUM (assets under management) fees (e.g., 200-250 basis points for Grayscale products), trading fees (actively managed crypto funds), or a complex methodology (implementing on-chain operations correctly involves significant regulatory and technical risks).

For investing in crypto assets ranked 3rd to 1000th, a "cheap" way is to rely on your own investment capabilities, and I can give an example.

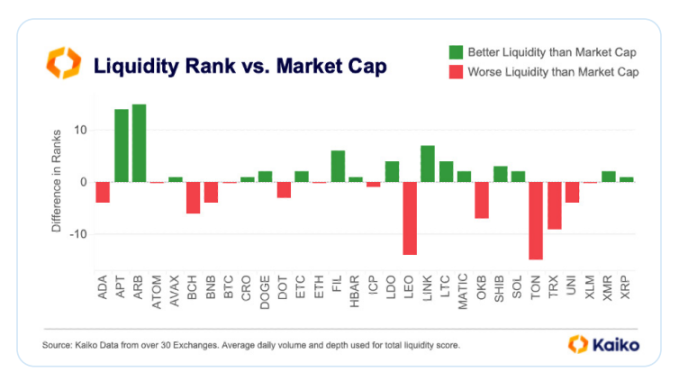

A simple at-home index investment strategy could be to monitor Kaiko's liquidity list and rebalance quarterly. If you buy green assets with liquidity rankings higher than market value rankings and sell red assets with market value rankings higher than liquidity rankings, you have essentially replicated my large asset long/short list year-to-date (of course, this is not investment advice).

Source: Kaiko

1.4 The Revival of the Private Cryptocurrency Market?

A few years ago, I wrote that the business model of crypto fund managers was nothing more than representing clients' "loss of alpha," which made them quite unhappy. It turns out I was right.

(I'm not gloating, but convincing myself that I made the right decision at the time, giving up the most profitable business model in the world, although I could have been doing the 2% management fee plus 20% profit sharing job since 2017, without having to think about the returns of Bitcoin/Ethereum.)

Many crypto investors have not only underperformed but have even exited the market. Some liquidity investors have found themselves in trouble due to bad leverage positions (such as 3AC), poor trading counterparts (such as Ikigai), or both (we discussed DCG in detail in Chapter 6). You should be familiar with these, so I won't repeat last year's crisis.

So, what will happen in 2024? The liquidity crypto market remains a jungle full of technical and counterparty risks, high trading fees, and intense competition. Adjacent to this jungle is a true "valley of death" - the private crypto venture capital market.

Overall, the VC market has been severely impacted in recent years by the shocking monetary policy of the Federal Reserve. The crypto infrastructure has been hit even harder due to fraud and widespread regulatory crackdown. New users and clients are excluded from accessing "long-tail" crypto assets until they obtain much-needed legal clarity, while old users and clients cut expenses to survive this winter as much as possible. This has led to brutal demand destruction: service revenues are declining, burn rates are increasing, budgets are further reduced, and so on.

To make matters worse, AI has become the new darling of the tech industry. Once again, we have become bystanders. (As I explained in Chapter 1.8, I believe this is a foolish MEME and a wrong choice; AI and cryptocurrencies actually go well together.)

Nevertheless, I remain optimistic about new crypto primary investors. Funds from 2023 are likely to outperform the S&P 500 in the medium to long term, with many even surpassing the benchmark performance of BTC/ETH due to exceptionally low entry prices this year. The liquid market has regained momentum, and there are signs of a revival in the venture capital market.

The funding for private venture capital (from seed rounds to Series D+) has reached its highest level since May, with over $500 million in announced transactions (which can be tracked in our funding filter):

Here are some of the crypto funds I have been following this year:

Multicoin: I wrote a trilogy about their legendary performance in 2021. However, it's unclear how their LPs are coping with the harsh reality of SOL plummeting 96% in 2022. Even if Multicoin's AUM rebounds significantly this year, I'm not sure if any fund LPs have experienced a bigger rollercoaster ride.

1confirmation: Nick Tomaino is one of the most honest crypto investors I've met. He candidly addresses the benchmark issues I mentioned earlier, the need for better accountability in crypto investments, and his role as one of the few skeptics of Sams. First SBF, then Altman. His actions have also proven his point, even sharing his fund's DPI, which is rare in the venture capital market.

There are also "bottom-up" investors whose tweets have proven to be correct in hindsight. Framework (Vance) and Placeholder (Burniske) are examples of those who have expressed specific views and are not simply perpetual bulls. (Even those who are bullish at the top may be proven to be prophets in the long run.)

a16z and Paradigm may be at a disadvantage in valuing their private investment portfolios, depending on how much capital they invested at the market top in 2021, but I don't want to bet against Chris Dixon, Matt Huang, and their team. In fact, I am somewhat glad that they may have had mediocre or temporarily losing investment performance in some years. This makes them excellent fighters in Washington, and their policy team has performed exceptionally well.

Syncracy Capital has significantly outperformed the crypto market since its inception. The team includes three former Messari analysts, including co-founder Ryan Watkins. Full disclosure, I am an LP in this fund and will proudly advocate for those who helped build Messari and continue to make money for me after leaving. They are one of the few new liquidity funds that have consistently outperformed the BTC/ETH benchmark since their inception.

1.5 IPOs and M&A

In the cryptocurrency world, three companies stand out for their positioning, team, and capital-raising capabilities: Coinbase, Circle, and Galaxy Digital.

Coinbase remains the most important company in the cryptocurrency space. As the most valuable and tightly regulated cryptocurrency exchange in the United States, Coinbase deserves special mention. It is unlikely to face major competitors in the US market next year, but one of its major partners, Circle, may go public in 2024.

Circle's CEO Jeremy Allaire shared at Mainnet that Circle's revenue in the first half of 2023 reached $800 million, with EBITDA of $200 million - a figure equivalent to the company's full-year data in 2022, and revenue may further increase in a "higher and longer" interest rate environment.

Circle may be well-positioned in the cryptocurrency market to take advantage of progress in US stablecoin policy or the prosperity of international stablecoin growth. The company's valuation depends almost entirely on the market's trust in its product and technology growth, rather than its "we earn interest from your floating income" economics (*Tether is even stronger financially, and has regained its market share since the Silicon Valley bank collapsed in March this year, but don't expect its S-1 to appear soon).

I once thought that DCG would be the first IPO candidate due to its diverse service portfolio. But DCG is under siege and may not go public for a long time. At the very least, DCG faces a daunting challenge of rebuilding its institutional reputation after the bankruptcy lawsuit of its subsidiary Genesis (a public scandal) and the rapid liquidation of its core assets in the past 12 months (GBTC, CoinDesk divestitures, etc.).

Meanwhile, another New York-based crypto financial group's stock price (both in image and in reality) is rising. Galaxy Digital's venture capital portfolio, trading division, mining operations, and research institution may help it replace DCG in the narrative of the cryptocurrency industry: Mike Novogratz's company has been listed on the Toronto Stock Exchange with a market value of $3 billion.

If they are willing, this is enough for Novogratz's team to choose an aggressive integration strategy in 2024. Under continued venture capital pressure, some major assets are bound to be in trouble, and Novogratz already has a complete investment banking advisory team.

Apart from these companies, I wouldn't hold too much hope for any other cryptocurrency company's IPO. I doubt whether other companies' IPOs will be allowed before the 2024 US election under the current regulatory regime. Therefore, the path to liquidity for cryptocurrencies is still through the token market.

1.6 Policy

(Note: This section mainly discusses the potential for the US to succeed in the global crypto market and the challenges it currently faces. The author mentions some important historical events and trends, including the crypto wars of the 90s, government regulation of digital privacy, and changes in the US's position in global competition, emphasizing that the attitudes of the younger generation towards digital privacy and personal freedom may be different from those of previous generations, which may have an impact on crypto policy. It may contain some ideological content and be a bit dry, so it can be skipped.)

We will discuss the outstanding figures of Senator Elizabeth Warren and SEC Chairman Gary Gensler in later chapters. No need to worry.

But first, we need to take a step back and look at the bigger picture. The United States has the talent, financial markets, and regulatory policies to win the global cryptocurrency market, ensuring that the US remains a financial and technological powerhouse in the 21st century. However, I believe this time we don't have enough crypto punks to save us.

The past 30 years have not only been a time of growth for our millennial generation, but they also provide clues and background for the crypto policies we might expect in the short and medium term. Among the most influential events and changes in the past few decades in the crypto world, one historical analogy and two major trends are particularly important for our attention:

- The initial crypto wars of the 90s, including the unfair struggle with the National Security Agency, legislation proposing the installation of a literal government chip in all your devices for on-demand unlocking, and a popular grassroots rebellion led by developers against government overreach. This is the origin of the term "cypherpunks write code." You should read a book about the crypto wars, or at least read this paper.

It accelerated the history of cryptography. It's a story of the underdog's comeback, although due to profound cultural changes in the US, this victory seems unlikely to be repeated in our cryptocurrency.

Complacency and Awakening Spells: Unfortunately, the X generation (born from 1964 to 1980) has aged, and since then, the X generation has done some quite terrible and unconstitutional things in collaboration with the baby boomer generation. Today, "crypto" poses a significant threat to the "surveillance and control" national order. When we look at our young protagonists, the millennial and Z generations (born from 1995 to 2009), the question is whether they may not care about the fight at all. They are accustomed to erosion of civil liberties in the post-Patriot Act and post-COVID era. After 20 years and a $7 trillion global military disaster, they have never lived in a situation where a national security apparatus looks inward. Many of them even disdain the scrutiny industrial complex of Twitter files and big tech companies. Peter Thiel and David Sacks wrote a prediction article in the early 90s about the danger of campus cultural conformity, and SBF is just reminding us of what we already knew, that this conformity may be performative, but now it's harmful.

The end of American hegemony: When you combine #1 and #2, what you really need to understand is that a large part of government officials really believe that the tech policies of the 90s were a mistake, and the miracle of the open internet and the economic growth it brought have had a net negative impact on American society. Technology has become the scapegoat.

While our concerns about hollowing out our manufacturing base and over-financializing the economy have some merit, many envy China's closed internet, only seeing "missed opportunities to curb misinformation," which is a bit scary. We are no longer the only superpower, as bureaucratic institutions of competitors like China seem to be effective in some areas, and our leaders also seek more control.

Our culture has gradually weakened, the delusions of the elderly ruling group at home are strong, and this time we have a formidable opponent. We must play a different game, focusing on "Moneyball" elections. The good news is that we will win. (Chapter 5 will discuss how this will happen more.)

(I know you may think these trends are completely irrelevant, or at most tangentially related to cryptocurrencies, but that's what they said about Pepe Sylvia. We are in a life-and-death information war.)

1.7 What Can Developers Do?

Despite the crypto market being mired in a downturn for the past two years, with declining trading volumes and heavy regulatory resistance, the activity of cryptocurrency developers this year has remained strong. Mid-year, Alchemy found that the number of smart contracts deployed on EVM chains grew by 300% quarter-over-quarter, and the installation of crypto wallets reached an all-time high.

Electric Capital found that as of October, the monthly active developers contributing to open-source projects had sharply declined year-over-year, but this is attributed to several factors: regulatory indifference to the open-source ecosystem after the Ooki DAO ruling this year, more innovation and development at the application and infrastructure layers, and a more cautious attitude towards competitive threats in a bear market.

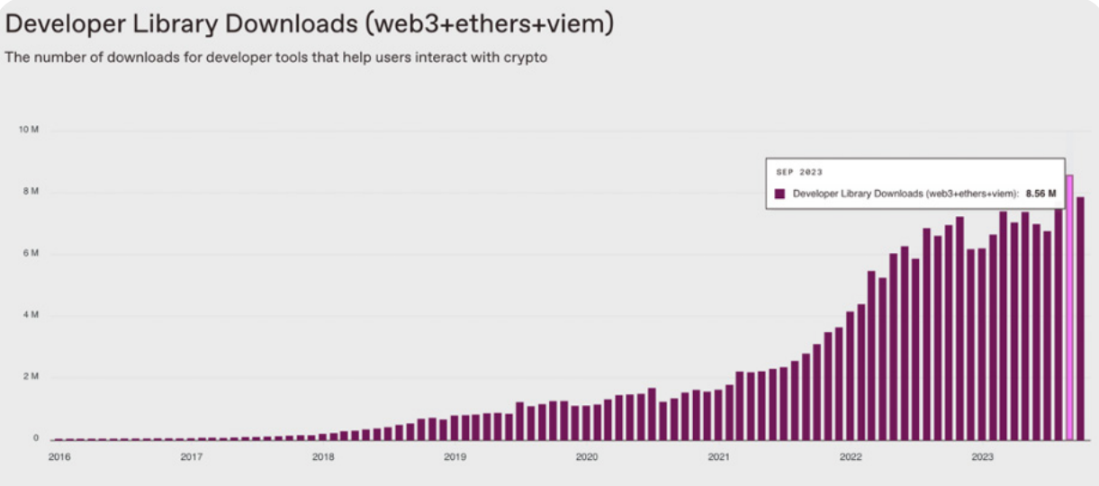

a16z's Cryptocurrency Market Status Index may be the best index to observe the overall market health. Its tracking also highlights a 30% decrease in the number of open-source developers, but it also records some positive market data: developer kit downloads hit a historical high in the third quarter, while active addresses and mobile wallet activity hit historical lows. Is this the spark that will ignite the explosion of crypto applications in 2024? If I could blindly invest in cryptocurrencies based on a single chart, it would be this one:

The real turning point in the market will come when artificial intelligence developers realize that cryptocurrencies are their next battleground.

1.8 AI & Cryptocurrencies

In this era marked by rich AIGC, providing reliable, global, mathematically guaranteed provenance and digital scarcity is crucial.

Take deepfakes, for example: cryptocurrencies are crucial in timestamping and verifying devices and data. Without cryptocurrencies, it's difficult to verify whether certain images or texts come from AI or non-AI, or from Washington or Beijing. Additionally, without the fees required by public chains, preventing generative DDOS attacks would also be a major challenge.

The rise of artificial intelligence is seen as a "threat" to cryptocurrencies, much like mobile technology was seen as a threat to the internet, which is clearly absurd. The progress of artificial intelligence will only increase the demand for cryptocurrency solutions. While we may debate whether artificial intelligence is good or bad for humans (just as we debate whether the iPhone is good or bad… but we still know it's obviously beneficial), AI is great for cryptocurrencies.

I personally welcome our machine overlords, bringing about the perfect machine currency: Bitcoin.

There's no need to overthink this, but an article by Arthur Hayes (founder of BitMEX) this summer on this topic is worth noting. For any artificial intelligence, the two most critical elements are data and computing power. Therefore, it seems reasonable that "artificial intelligence will trade a currency that maintains its purchasing power over time" perfectly describes Bitcoin.

Some criticize this view as oversimplified, especially considering two potential applications of artificial intelligence - micro-payments and smart contract execution, which have not significantly developed on Bitcoin. Some argue that AI agents would choose the blockchain with the lowest cost, not necessarily Bitcoin, as Bitcoin's POW mechanism has transaction friction.

Dustin (Messari researcher) believes that the concept of an "energy-priced currency" may be the opposite: AI agents may be more inclined to directly purchase Gas tokens (related computational resources).

1.9 DePIN, DeSoc, DeSci

I am permanently bullish on decentralized finance (DeFi), but I don't necessarily "overvalue" it, as I believe other market segments will perform better in the coming year.

I do believe that some top DeFi protocols in this field (especially in the decentralized exchange sector) will rebound after a year of stable trading volumes, but I am not sure if the unit economics of DeFi and product-market fit are sufficient to offset the impending harsh regulation.

Additionally, the types of assets driving DeFi trading volume are also a concern. This year's trading peak was mainly driven by MEME coins, rather than breakthroughs in new applications. Perhaps I have considered too many doomsday scenarios for DeFi in Washington (more on this in Chapter 8).

My focus has shifted to several key non-financial sectors in the crypto space. I like DePIN (physical infrastructure network), DeSoc (social media), and DeSci (yes, science!), because they seem to be driven less by rampant hype and more by critical solutions that go far beyond the financial sector in our industry.

Last year, Sami (a researcher at Messari) helped popularize the term DePIN, and no one is better than him at drawing the landscape of these hardware networks or explaining how these networks scale, truly competing with big tech companies.

The cloud infrastructure services industry is valued at $5 trillion in the traditional market, and DePIN accounts for only 0.1% of it. Even assuming that 1% of online services will use DePIN as their primary stack, the demand for decentralized redundancy alone could lead to a significant increase in demand. To eliminate the risk of big tech platforms, a 1% "insurance premium" could lead to a 10x increase in DePIN utilization. It doesn't take much to change the status quo, especially in the demand for GPU and computational resources driven by artificial intelligence.

There are similar opportunities in social media, where the major players in the field generated $230 billion in revenue last year (half of which came from the Meta family of companies), and only a tiny percentage of creators could earn enough money through content creation.

We have already seen this changing (YouTube's continued growth, Elon's revenue sharing), and we have also seen the potential breakthrough DeSoc applications (Farcaster, friend.tech, and Lens). This is more like the beginning of a J-curve that is almost imperceptible at first, rather than a false start.

Friend.tech shared $50 million with its creators in the first few months after launch, which is one way to attract users. I believe that DeSoc in 2024 will follow the hype of the "DeFi summer" in 2020.

Finally, there is decentralized science. 50% of the DeSci projects we track were established in the past year. One of the best OG cryptocurrency investors I know has already devoted 100% of his time to this area.

In this market, the incentive mechanism of cryptocurrencies makes sense: people's trust in our scientific institutions may be at an all-time low, and the current system is rife with bureaucratic inefficiency, flawed data methods, and poor incentive mechanisms (where only peer-reviewed papers can secure a tenured position), while cryptocurrencies have proven their ability to fund scientific experiments.

To scale up, token sales and DAOs are aimed at fundamentally changing the way we conduct research, and the interest in longevity, rare disease treatment, and space exploration is significant enough to drive the development of this field.

You can invest directly in DePIN, start using DeSoc applications now. However, I don't yet know of a lazy way to articulate the investment case for DeSci. (VitaDAO?)

Think about it, feel free to DM me anytime.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。