Author: AIMan@Golden Finance

On April 25, 2025, Citi Institute, a subsidiary of Citibank, released a research report on the "Digital Dollar." Key points from the report include:

2025 is expected to be the "ChatGPT moment" for blockchain applications in the financial and public sectors, driven by regulatory changes.

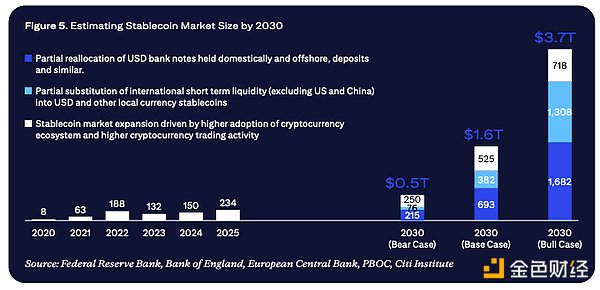

Citi predicts that by 2030, the total circulating supply of stablecoins could grow to $1.6 trillion under a baseline scenario; in an optimistic scenario, it could reach $3.7 trillion, while in a pessimistic scenario, it may be around $500 billion.

It is expected that the supply of stablecoins will primarily be denominated in U.S. dollars (about 90%), while non-U.S. countries will promote the development of their own CBDCs.

The regulatory framework for stablecoins in the U.S. may drive new net demand for U.S. Treasury securities, with stablecoin issuers potentially becoming one of the largest holders of U.S. Treasuries by 2030.

Stablecoins pose a certain threat to the traditional banking ecosystem by substituting deposits. However, they may also provide opportunities for banks and financial institutions to offer new services.

As suggested by the report's title "Digital Dollar," Citi is highly optimistic about stablecoins, dedicating a chapter to explain that "the ChatGPT moment for stablecoins is coming." Golden Finance's AIMan has specially translated the chapter "Stablecoins: A ChatGPT Moment?" as follows:

How Do Stablecoins Work?

Stablecoins are a type of cryptocurrency designed to maintain a stable value by pegging market prices to reference assets. These reference assets can include fiat currencies like the U.S. dollar, commodities like gold, or a basket of financial instruments. Key components of the stablecoin system include:

Stablecoin Issuers: Entities that issue stablecoins, responsible for maintaining the price peg by holding underlying assets equivalent to the circulating supply of stablecoins.

Blockchain Ledger: After issuance, transaction records are maintained on a blockchain ledger. This ledger provides transparency and security by tracking the ownership and circulation of stablecoins among users.

Reserves and Collateral: Reserves ensure that each token can be redeemed at its pegged value. For fiat-collateralized stablecoins, these reserves typically include cash, short-term government securities, and other liquid assets.

Digital Wallet Providers: These provide digital wallets, which can be mobile applications, hardware devices, or software interfaces, allowing stablecoin holders to store, send, and receive their tokens.

How Do Stablecoins Maintain Their Pegged Value?

Stablecoins rely on different mechanisms to ensure their value aligns with the underlying assets. Fiat-backed stablecoins maintain their peg by guaranteeing that each issued token can be exchanged for an equivalent amount of fiat currency.

Major Stablecoins

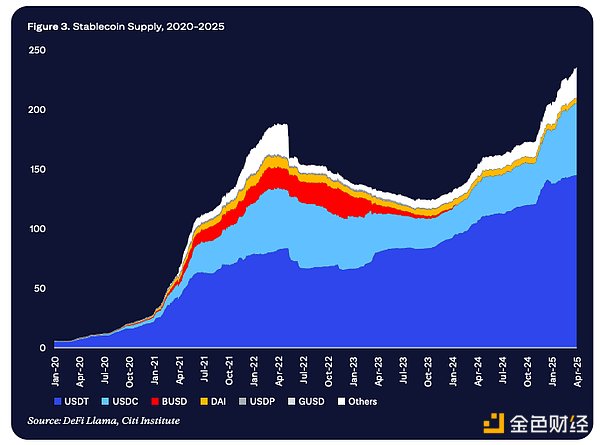

As of April 2025, the total circulating supply of stablecoins has exceeded $230 billion, growing by 54% since April 2024. The top two stablecoins dominate this ecosystem, accounting for over 90% of the market share in terms of value and transaction volume, with USDT leading and USDC following.

Figure 3 Stablecoin Supply from 2020 to 2025

In recent years, the trading volume of stablecoins has surged. Adjusted for inflation, the monthly trading volume of stablecoins in Q1 2025 ranged between $650 billion and $700 billion, approximately double the levels seen from the second half of 2021 to the first half of 2024. Supporting the crypto ecosystem is the primary application scenario for stablecoins.

The largest stablecoin, USDT, was launched in 2014 on the Bitcoin blockchain and expanded to the Ethereum blockchain in 2017, enabling its use in DeFi. In 2019, it further expanded to the Tron network, which is widely used in Asia, due to faster speeds and lower costs. USDT largely operates offshore, but times are changing.

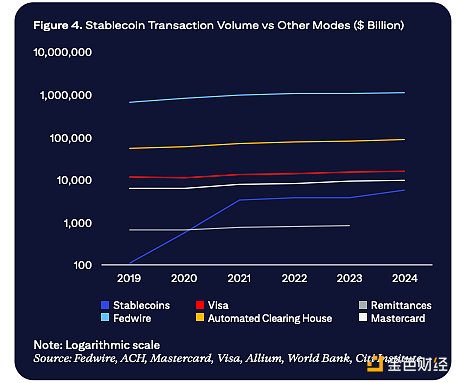

Figure 4 Comparison of Stablecoin Trading Volume with Other Payment Methods (in billions of dollars)

We will certainly see more participants (especially banks and traditional institutions) entering the market. Dollar-backed stablecoins will continue to dominate. Ultimately, the number of participants will depend on the variety of products needed to cover major application scenarios, and the number of participants in this market may exceed that of card networks. — Matt Blumenfeld, Global and U.S. Digital Assets Leader at KPMG

What Are the Driving Factors for the Adoption of Stablecoins in the U.S. and Globally?

Erin McCune, Founder of Forte FinTech:

Practical advantages (speed, low cost, availability around the clock): Demand has been created in developed economies (especially in countries where instant payments are not yet widespread, small and medium-sized enterprises are not adequately served by existing institutions, and multinational companies seek easier global fund transfers) and emerging economies (where cross-border transaction costs are high, banking technology is underdeveloped, and/or financial inclusion is lagging).

Macroeconomic demand (hedging against inflation, financial inclusion): In some regions, stablecoins have become a "lifeline" for people. In countries like Argentina, Turkey, Nigeria, Kenya, and Venezuela, where currencies are highly volatile, consumers use stablecoins to protect their funds. Nowadays, an increasing number of remittances are conducted in stablecoin form, allowing consumers without bank accounts to use digital dollars.

Support and integration from existing banks and payment providers: This is key to the legitimization of stablecoins (especially for institutional and corporate users) and can quickly expand their usage and practicality. Mature, large-scale payment networks and core processors can provide transparency and facilitate integration with familiar solutions relied upon by businesses and merchants. Establishing clearing mechanisms between different stablecoins and between banks and non-bank institutions is also crucial for scaling. Technological improvements aimed at consumers (user-friendly wallets) and merchants (integrating stablecoin payment functions into acquiring platforms via APIs) are eliminating barriers that previously confined stablecoins to the fringes of crypto.

Long-awaited regulatory clarity: This enables banks and the broader financial services industry to adopt stablecoins in retail and wholesale operations. Transparency (audit requirements) and consistent liquidity management (reliable parity) will also simplify operational integration.

Matt Blumenfeld, Global and U.S. Digital Assets Leader at KPMG:

User experience: The global payment landscape is increasingly shifting towards real-time digital transactions. However, every new payment method faces challenges during promotion regarding customer experience — whether it is intuitive, whether the application scenarios are visible, and whether the value is clear. Any institution that successfully enhances customer experience, whether targeting retail or institutional users, will stand out in their respective fields. Integration with current payment methods will drive the next wave of payment method adoption. On the retail side, this manifests as integration with card payments or penetration in the mobile wallet space; on the institutional side, it is reflected in simpler, more flexible, and cost-effective settlement methods.

Regulatory clarity: With the introduction of new stablecoin regulatory policies, we can see how much regulatory uncertainty has previously stifled innovation and promotion globally. The launch of the EU's Markets in Crypto-Assets Regulation (MiCA), clear regulations in Hong Kong, and the advancement of stablecoin legislation in the U.S. have sparked a wave of activities focused on simplifying the flow of funds for institutions and consumers.

Innovation and efficiency: Institutions must view stablecoins as a means to achieve more flexible product development, which is not easy in the current environment. This means providing a more convenient, creative, and attractive medium to enhance the functionality of traditional bank deposits, such as generating yields, programmability, and composability.

Potential Market Size for Stablecoins

As noted by Erin McCune, founder of Forte Fintech, any prediction regarding the potential market size of stablecoins should be approached with caution. There are many variable factors, and our scenario analysis shows a wide range of predictions.

We have constructed a range of forecasts based on the following factors driving the growth of stablecoin demand:

A portion of overseas and domestic U.S. dollars shifting from cash to stablecoins: Overseas-held U.S. dollar cash is often a safe haven against local market volatility, and stablecoins provide a more convenient way to obtain this hedge. Domestically, stablecoins can be used for certain payment functions to some extent, and are held for that purpose.

Households and businesses in the U.S. and internationally reallocating some dollar short-term liquidity to stablecoins: This is due to the convenience of using stablecoins (such as enabling round-the-clock cross-border transactions), which aids in cash management and payment operations. If regulations allow, stablecoins may also partially replace yield-generating assets.

Additionally, we assume that the short-term liquidity of euros/pounds held by U.S. households and businesses will also experience a similar trend of reallocation as with dollar short-term liquidity, although on a much smaller scale. Our overall baseline and optimistic scenario predictions for 2030 assume that the stablecoin market will still be dominated by the U.S. dollar (approximately 90% market share).

Growth of the public cryptocurrency market: Stablecoins are used as settlement tools or channels for inflows and outflows. This is partly driven by institutional adoption of public crypto assets and the widespread application of blockchain technology. In our baseline scenario, we assume that the issuance growth trend of stablecoins from 2021 to 2024 continues.

Citi Institute expects the baseline scenario for the stablecoin market size in 2030 to be $1.6 trillion, the optimistic scenario to be $3.7 trillion, and the pessimistic scenario to be $0.5 trillion.

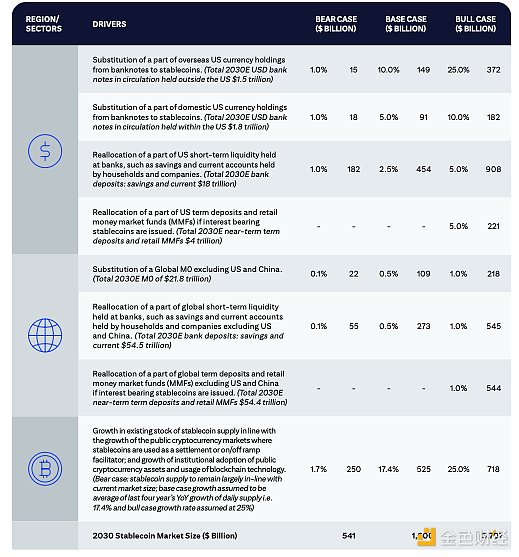

Figure 5 Forecast of Stablecoin Market Size in 2030

Figure 6 Stablecoin Market Size in 2030

Note: The total money supply in 2030 (circulating cash, M0, M1, and M2) is calculated based on nominal GDP growth. The Eurozone and the UK may issue and adopt local stablecoins. China may adopt a sovereign central bank digital currency but is unlikely to adopt foreign privately issued stablecoins. It is expected that the size of non-dollar stablecoins in bear, baseline, and bull markets in 2030 will be $21 billion, $103 billion, and $298 billion, respectively.

Outlook for the Stablecoin Market

Erin McCune, Founder of Forte Fintech

Question: What are your thoughts on the recent optimistic and cautious outlook for the stablecoin market size, as well as the potential factors driving its development trajectory?

Predicting the growth of the global stablecoin market requires immense confidence (or perhaps overconfidence), as there are still many unknowns. With that caution in mind, here is my scenario analysis for bull and bear markets:

The most optimistic prediction is that as stablecoins become the everyday medium for global instant, low-cost, and low-friction transactions, the market will expand 5 to 10 times. In a bull market scenario, the value of stablecoins will grow exponentially from the current approximately $200 billion to between $1.5 trillion and $2.0 trillion by 2030, penetrating global trade payments, person-to-person remittances, and mainstream banking. This optimistic expectation is based on several key assumptions:

Favorable Regulation in Key Regions: This includes not only Europe and North America but also markets with the highest demand for alternative local fiat currencies, such as sub-Saharan Africa and Latin America.

Real Trust Between Existing Banks and New Entrants: Along with widespread consumer and business confidence in the integrity of stablecoin reserves (e.g., 1 dollar stablecoin = 1 dollar equivalent fiat currency).

Intentional Distribution of Income (and Savings) Along the Value Chain: To promote collaboration.

Widespread Adoption of Technologies That Connect New and Old Infrastructures: To facilitate structural efficiency and scale. For example, merchant acquiring institutions have already begun using stablecoins. For wholesale payment applications, corporate finance and accounts payable solutions, as well as financial executives, will need to adjust. Commercial banks will also need to deploy tokenization and smart contracts.

In a bear market scenario, the use of stablecoins will be limited to the crypto ecosystem and specific cross-border use cases (mainly in markets with insufficient currency liquidity, which currently account for a small proportion of global GDP). Geopolitical factors, resistance to digital dollarization, and the widespread adoption of central bank digital currencies (CBDCs) will further hinder the growth of stablecoins. In this case, the market capitalization of stablecoins may stagnate at $300 billion to $500 billion, with limited relevance in mainstream economies. The following factors will lead to a more pessimistic scenario:

If one or more major stablecoins experience reserve failures or decoupling events: This would significantly undermine trust among retail investors and businesses.

Friction and costs associated with using stablecoins for everyday purchases: For example, remittance recipients may be unable to use their funds to buy groceries, pay tuition, and rent, and businesses may struggle to easily allocate funds for wages, inventory, etc.

Retail CBDCs have not yet gained traction: However, in regions where digital cash alternatives provided by the public sector achieve scale, the relevance of stablecoins may diminish.

In regions where stablecoin development further weakens the relevance of local fiat currencies: Central banks may respond by tightening regulations.

If the scale of fully reserve-backed stablecoins grows too large: This could "lock in" a significant amount of safe assets as support, potentially limiting credit in the economy.

Question: What are the current and future application scenarios for stablecoins?

Like any other form of payment, the relevance and potential growth of stablecoins must be considered in the context of specific application scenarios. Some application scenarios have already garnered attention, while others remain theoretical or clearly impractical. Here are currently (or soon-to-be) meaningful stablecoin application scenarios, ranked by their contribution to the total addressable market (TAM) for stablecoins from largest to smallest:

Cryptocurrency Trading: Currently, the largest application scenario for stablecoins is individuals and institutions using them to trade digital assets, accounting for 90-95% of stablecoin trading volume. This activity is largely driven by algorithmic trading and arbitrage. Given the ongoing growth of the cryptocurrency market and reliance on stablecoin liquidity, in a mature phase, trading (retail + decentralized finance activities) may still account for about 50% of stablecoin usage by value.

Business-to-Business Payments (Corporate Payments): According to data from SWIFT, the vast majority of traditional correspondent banking transaction values can reach their destinations within minutes via the SWIFT Global Payments Innovation platform. However, this mainly occurs between liquidity-rich currencies among central banks during banking hours. There are still many inefficiencies and unpredictabilities, especially when doing business with low- and middle-income countries. Businesses using stablecoins to pay overseas suppliers and manage cash operations could capture a significant share of the stablecoin market. The global flow of funds between businesses amounts to trillions of dollars, and even a small shift to stablecoins could account for about 20-25% of the total addressable market for stablecoins in the long run.

Consumer Remittances: Although payment methods are steadily shifting from cash to digital payments, and despite regulatory pressure and efforts from new entrants, the cost of remittances from overseas workers to domestic friends and family remains high (averaging 5% for a $200 transaction, five times the G20 target). With lower fees and faster speeds, stablecoins are expected to capture a significant share of the approximately $1 trillion remittance market. If promised instant transfers and significant cost reductions can be achieved, this could account for 10-20% of the market under high adoption rates.

Institutional Trading and Capital Markets: The application scenarios for stablecoins in the settlement of transactions for professional investors or tokenized securities are continuously expanding. Large-scale fund flows (foreign exchange, securities settlement) may begin to use stablecoins to accelerate settlement speeds. Stablecoins can also simplify the fundraising process for retail stock and bond purchases, which is currently typically handled through batch automated clearinghouses. Large asset management firms have already piloted the use of stablecoins for fund settlements, laying the groundwork for widespread application in capital markets. Given the substantial payment flows between financial institutions, even with low adoption rates, this application scenario could account for about 10-15% of the stablecoin market.

Interbank Liquidity and Cash Management: Banks and financial institutions using stablecoins for internal or interbank settlements, while relatively small (possibly less than 10% of the total market), could have a significant impact. Industry-leading firms have launched blockchain projects with daily transaction volumes exceeding $1 billion, indicating their potential, although regulatory clarity remains uncertain. This area may see significant growth, although it may overlap with the aforementioned institutional use cases.

Stablecoins: Credit Cards, Central Bank Digital Currencies, and Strategic Autonomy

We believe that the usage of stablecoins may grow, creating space for new entrants. The current dual-monopoly issuance structure may persist in offshore markets, but new participants may emerge in each country's onshore market. Just as the credit card market has evolved over the past 10-15 years, the stablecoin market will also undergo changes.

Stablecoins share some similarities with the credit card industry or cross-border banking. All these areas exhibit high network or platform effects and have strong reinforcing cycles. More merchants accepting a trusted brand (such as Visa, Mastercard, etc.) will attract more cardholders to choose that card. Stablecoins also have a similar usage cycle.

In larger jurisdictions, stablecoins are generally outside financial regulation, but this situation is changing with the EU (the 2024 Markets in Crypto-Assets Regulation) and the U.S. (where relevant regulations are advancing). The demand for stricter financial regulation, along with high costs for partners, may lead to the centralization of stablecoin issuers, similar to what we see in credit card networks.

Fundamentally, having a few stablecoin issuers can be beneficial for a broader ecosystem. While one or two major players may appear concentrated, an excess of stablecoins can lead to fragmentation and non-interchangeability of currency forms. Stablecoins can only thrive when they have scale and liquidity. — Raj Dhamodharan, Executive Vice President of Blockchain and Digital Assets at Mastercard

However, the evolving political and technological landscape is increasing the differentiation of the credit card market, especially outside the U.S. Will we see a similar situation in the stablecoin space? Many countries have developed their own national card schemes, such as Brazil's Elo card (launched in 2011) and India's RuPay card (launched in 2012).

Many of these national card schemes were launched out of considerations of national sovereignty and have been driven by local regulatory changes and political encouragement for domestic financial institutions. They have also facilitated integration with new national real-time payment systems, such as Brazil's Pix system and India's Unified Payments Interface (UPI).

In recent years, while international card schemes have continued to grow, their market share has declined in many non-U.S. markets. In many markets, technological changes have led to the rise of digital wallets, account-to-account payments, and super apps, all of which have eroded their market share.

Just as we have seen the proliferation of national schemes in the credit card market, we are likely to see jurisdictions outside the U.S. continue to focus on developing their own central bank digital currencies (CBDCs) as a tool for national strategic autonomy, particularly in wholesale and corporate payment sectors.

A survey by the Official Monetary and Financial Institutions Forum (OMFIF) of 34 central banks shows that 75% of central banks still plan to issue CBDCs. The proportion of respondents planning to issue CBDCs in the next three to five years increased from 26% in 2023 to 34% in 2024. Meanwhile, some practical implementation issues are becoming increasingly apparent, with 31% of central banks delaying issuance due to legislative issues and a desire to explore broader solutions.

CBDCs began in 2014 when the People's Bank of China started researching the digital yuan. Coincidentally, this was also the year Tether was born. In recent years, stablecoins have rapidly developed, driven by private market forces.

In contrast, central bank digital currencies largely remain in the official pilot project stage. A few smaller economies that have launched national CBDC projects have not seen large numbers of users spontaneously adopt them. However, the recent escalation of geopolitical tensions may trigger more attention to CBDC projects.

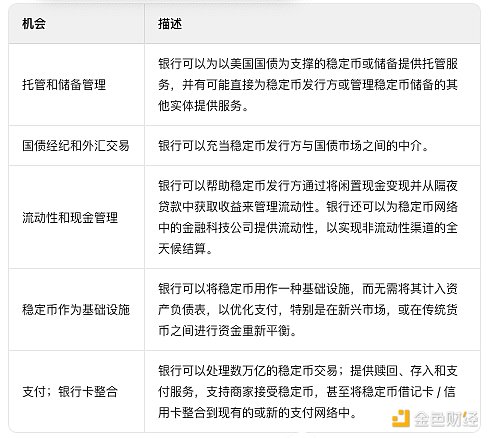

Stablecoins and Banks: Opportunities and Risks

The adoption of stablecoins and digital assets presents new business opportunities for some banks and financial institutions to drive revenue growth.

The Role of Banks in the Stablecoin Ecosystem

Matt Blumenfeld, Global and U.S. Digital Assets Leader at PwC

Banks have many opportunities to participate in the stablecoin space. This can be directly as stablecoin issuers, or indirectly as part of payment solutions, building structured products around stablecoins, or providing general liquidity support. Banks will find ways to continue being intermediaries for the flow of funds.

As users seek more attractive products and better experiences, we see deposits flowing out of the banking system. With stablecoin technology, banks have the opportunity to create better products and experiences while keeping deposits within the banking system (users generally prefer their deposits to be secured within the banking system), albeit through new channels.

Figure 7: Banks and Stablecoins: Revenue and Business Opportunities

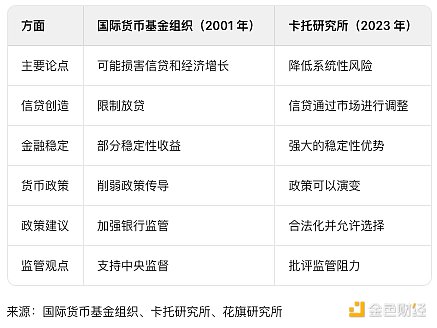

At the system level, stablecoins may have effects similar to those of "narrow banks," which have long been debated in policy circles regarding their pros and cons. The shift of bank deposits to stablecoins may impact banks' lending capabilities. This decline in lending capacity may suppress economic growth during the transition period of system adjustment.

Traditional economic policy opposes narrow banks, as summarized in a 2001 report by the International Monetary Fund, due to concerns about credit creation and economic growth. The Cato Institute presented a contrary view in 2023, arguing that "narrow banks" could reduce systemic risk, with credit and other fund flows adjusting accordingly.

Figure 8: Different Perspectives on Narrow Banks

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。