Original Title: Stablecoins: Better, Faster, Cheaper—Why They Matter

Original Author: @proofofnathan

Original Translation: zhouzhou, BlockBeats

Editor's Note: Stablecoins break the traditional payment trilemma with "better, faster, cheaper," providing global users with an open payment network that operates around the clock, at low cost, and without permission. They are evolving from intermediary tools to mainstream value carriers. Although they still face bottlenecks such as fiat currency exchange, stablecoins are expected to reshape the global financial landscape as network effects expand.

The following is the original content (reorganized for readability):

These three characteristics make stablecoins different from traditional payment systems and break an old rule: you cannot have all three at once. Any upgrade comes with costs. Improving quality slows down delivery speed; speeding up production increases costs; lowering costs diminishes excellence. Builders typically choose to optimize one dimension—better, faster, or cheaper.

Historically, innovators could usually only solve two of the three problems at a time, unable to address all simultaneously. Stablecoins have solved this innovation trilemma.

This is very important for retail users. Now, they can access an open payment network that operates around the clock, completing settlements in seconds, with fees of just a few cents rather than a percentage.

Stablecoins are better. They represent the obvious next step in the transfer of funds. As the world gradually becomes fully digital, it is natural for value itself to enter a fundamentally digital form. Stablecoins facilitate this evolution. They operate on an open network around the clock, storing and exchanging value more simply than fiat currency. Anyone can access them, and as I have written before, they are programmable.

Stablecoins are faster. Settlement speed depends on the blockchain, but even the slowest networks far exceed traditional payment systems. Ethereum transactions are completed in about 12 seconds, Tron in about 3 seconds, and Plasma aims for millisecond confirmations. Traditional payment systems can take anywhere from a few hours to several business days. Faster settlements reduce opportunity costs, minimize currency risk, and in emergencies, can quickly transfer funds to those who need them at critical moments without delay.

Stablecoins are cheaper. Regardless of which blockchain they exist on, their cost structure is lighter. Fixed fees for global transfers are almost always more economical than the percentage fees included in card networks or international bank transfers. On Plasma, USD₮ transfers incur no gas fees, bringing marginal costs close to zero and opening up the realm of true on-chain micropayments.

Better, faster, cheaper. Stablecoins solve the aforementioned innovation trilemma. But why is this important, and who will benefit?

Why is this important?

Stablecoins have attracted a lot of attention, but the "why" is often overlooked. The answer is simple: because they are better, faster, and cheaper, they directly serve retail users globally.

So far, we have analyzed stablecoins through the lens of the innovation trilemma. Now, let’s look at the issue from a different perspective.

Mikey Kremer succinctly summarized the importance of cryptocurrencies in the digital world:

"The crypto ecosystem did not invent a new financial system; it invented a new venue. By transferring familiar services—payments, lending, market-making—into ostensibly 'permissionless' code, projects have exploited the gaps left by the over-regulatory framework post-2008."

Stablecoins operate in an open field where anyone can connect—this is their greatest unlock for retail users.

In a sense, stablecoins are merely a tokenized form of the dollar, not particularly radical. But as Mikey pointed out, "The real innovation is not the service itself, but the ability to achieve the service without permission."

This is where the advantage of stablecoins lies: they break the "trilemma" while remaining completely open and permissionless. Throughout history, true breakthroughs often come from changes in how humans collaborate, and money, as a core collaborative tool, has evolved alongside society for centuries.

However, each upgrade in currency has also brought value transfer closer to the state. Today's payment systems are regulated, owned, and maintained by government-related agencies.

One of the core ideas of Bitcoin is libertarianism. As more people around the world seek to detach themselves from state control, they are turning to Bitcoin.

Today, this pursuit of freedom is also guiding them toward stablecoins.

For retail users, the simplest reason stablecoins are superior is that they exist for everyone. In this sense, the blockchain that stablecoins rely on is essentially a permissionless payment system. People around the world can connect and freely transfer funds in a better, faster, and cheaper way.

But stablecoins are not a perfect solution

Bottleneck Issues

It is overly idealistic to think that a new system has no flaws. Stablecoins certainly have their shortcomings. The most critical bottlenecks focus on the "last mile"—the final settlement stage between stablecoins and fiat currency. Major obstacles include but are not limited to:

- Liquidity and settlement issues: Converting large amounts of stablecoins to fiat, or vice versa, still heavily relies on decentralized banking channels and partnerships;

- Withdrawal and actual consumption issues: Using stablecoins conveniently for daily consumption or converting to fiat still involves many frictions, making it less convenient compared to fiat;

- Local regulation and capital controls: Many countries have yet to establish clear rules for stablecoins, and strict capital controls in some countries directly limit citizens' access to dollars.

Since the "last mile" still relies on traditional financial systems, global capital flows at this stage are inevitably constrained by the old framework.

I believe that stablecoins will ultimately become the default medium for transferring value. As that day approaches, these frictions will gradually disappear, and consumers will genuinely enjoy all the benefits that stablecoins bring.

To achieve such a future, the network effects of stablecoins must continue to amplify.

Network Effects

Stablecoins thrive on network effects. Tom Blomfield, co-founder of Monzo, explained the essence of network effects: "Network effects are different from other forms of growth—the product itself becomes better as more people join your network. Whatsapp and Skype are good examples; the more friends you have, the easier and cheaper it is to contact them."

This mechanism is very applicable to stablecoins. As the number of users increases, more merchants accept them, and more businesses begin to integrate, the entire system's trust foundation accumulates.

Adoption typically occurs in two stages: initially, people accept stablecoins while still using cash as a mental anchor; but over time, they choose to use stablecoins because they are indeed better, faster, and cheaper. At this point, the network effects fully kick in.

As the network effects of stablecoins continue to expand, they naturally become more suitable for a broader range of retail users. Although the barriers to using stablecoins are relatively low and most networks are permissionless, global adoption is still progressing gradually. The two key forces driving adoption are:

- Organic diffusion of network effects

- Innovative ways to make stablecoins more applicable in daily life

The future of stablecoins is slowly but surely unfolding.

Shhhigurh accurately depicted the current state of this transformation in "The Stablecoin Paradox":

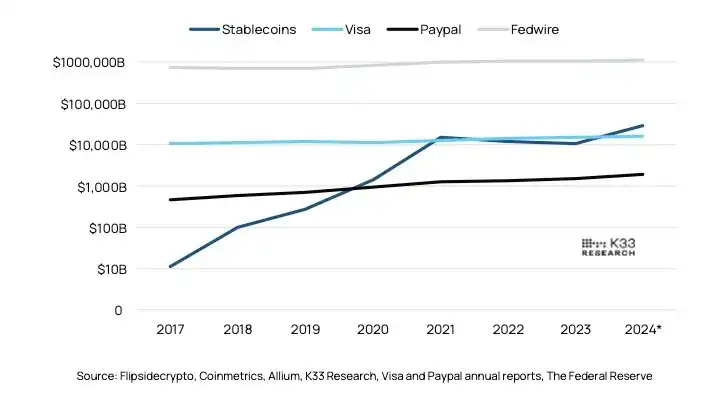

"The transaction volume handled by the stablecoin ecosystem is less than that of Visa or PayPal, but the average transaction amount is much larger. In 2023, Visa processed 276 billion payments, averaging $54 each; PayPal processed 25 billion, averaging $61. Fedwire, on the other hand, only processed 193 million transactions, but each was as high as $5.6 million. In comparison, stablecoins processed 2.6 billion transactions in 2023, with an average amount of $4,200, sitting right in the middle between retail and institutional transactions."

This passage reveals a key trend: stablecoins are currently still in the "mid-tier"—between everyday retail card swipes and institutional-level large transfers. They have not yet become the default track for processing small, high-frequency payments—Visa card swipes and PayPal clicks still dominate this level.

However, due to the clear advantages of stablecoins in terms of cost, speed, and openness, it is only a matter of time before they further penetrate everyday consumer payment scenarios.

A World Where Stablecoins Are Fully Adopted

I have long contemplated and written about how the future stack structure of a "stablecoin-based payment network" will be built.

If stablecoins truly become mainstream payment tools, we may see a completely new paradigm of financial interaction:

- Wallet = Account, no need to open a bank account; global users only need a wallet address to send and receive payments;

- Smart Contracts = Routers, fund allocation, payment splitting, supply chain settlement, and automatic execution of financial products will all be completed on-chain;

- On-chain Identity = Trust Layer, social graphs, credit systems, and payment systems will be interconnected; identity equals credit;

- Open API = Application Interface, any product can directly integrate stablecoin payments without the need for intermediary permission;

- Micropayments will activate long-tail scenarios, from content tipping and creator income to real-time salary payments and IoT device settlements, all becoming normalized.

In other words, stablecoins are not just "digital dollars," but the key to unlocking a permissionless, real-time settlement, globally interconnected financial new world.

From the current "average transaction amount of $4,200" to the future "content tipping of $0.42," this distance is slowly pieced together by infrastructure, regulation, experience, and network effects.

We are witnessing the construction of an era. Are you ready?

However, what I rarely delve into is the most ideal ultimate vision.

If retail adoption continues to grow exponentially, we will eventually reach a situation where:

Stablecoins no longer need "seamless conversion to cash" as support but directly become the default form of currency. Everyone will use stablecoins as the underlying payment layer, replacing fiat currency for daily settlements.

In this future world:

Value naturally flows on-chain,

People will be accustomed to using stablecoins for transfers, payments, salary disbursements, and shopping,

Merchants, businesses, and even governments will use stablecoins as their primary currency,

Traditional fiat currency will become "off-chain assets," while stablecoins will become the mainstream "money" in real life.

In such an "ideal utopia," stablecoins have completely triumphed. This is not just a transformation of currency form but a vision of a decentralized, cross-border, real-time programmable financial infrastructure fully replacing the old financial system.

Of course, we have not yet reached that future. But you can feel the direction of the trend:

From fringe players to mainstream adoption, stablecoins are rewriting the ancient question of "what is money."

I have clearly thought a bit too far ahead. That ideal future is still a long way from our current world. The existing fiat currency system still feels "safe and reliable," even though it has long fallen behind in terms of cost, speed, and accessibility. The key to achieving that future lies in whether the network effects can continue to expand.

Traditional network effects usually occur in "walled gardens," such as Facebook, Instagram, Monzo, and Revolut— the more users there are, the better the experience, but the platforms are closed.

Stablecoins disrupt this model: they operate on open, permissionless blockchains rather than closed systems.

Even so, as more and more people use stablecoins for payments, the overall user experience will continue to improve: more merchants, higher acceptance; faster transfers, lower fees; wallets, infrastructure, and user interfaces becoming more user-friendly; trust and liquidity continuously accumulating.

Imagine: if every person in the world could access a borderless, permissionless, low-cost payment network at any time, then "fast and cheap remittances" would no longer be a privilege but a basic human right.

Final Thoughts:

All of this is happening because stablecoins genuinely bring benefits to ordinary users around the world: they are easier to use, faster to transfer, cheaper, and most importantly: anyone can use them without permission.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。