Original Title: Interest Rate Perpetuals: DeFi's missing piece

Original Author: @defiance_cr

Original Translation: zhouzhou, BlockBeats

Editor's Note: The lack of interest rate perpetual contract tools similar to CME in DeFi has led to significant interest rate fluctuations and an inability to hedge risks. Introducing interest rate perps can help both borrowers and lenders lock in rates, achieve arbitrage and risk management, and promote the integration of DeFi and TradFi, enhancing market efficiency and stability.

The following is the original content (reorganized for better readability):

At the Chicago Mercantile Exchange (CME), the daily trading volume of interest rate futures exceeds one trillion dollars. This massive trading volume primarily comes from banks and asset managers who operate by hedging the risks between floating rates and fixed-rate loans that have been issued.

In DeFi, we have already established a thriving floating rate lending market, with a total locked value exceeding 30 billion dollars. Pendle's incentive-based order book has shown liquidity exceeding 200 million dollars in a single market, demonstrating strong demand for interest rate spot.

However, we still lack a DeFi-native tool like CME interest rate futures to hedge interest rate risks for both borrowers and lenders (IPOR swaps do not count because they are too complex).

To understand why we need this tool, we first need to understand how interest rates operate in DeFi.

Taking AAVE as an example, its interest rates are adjusted based on supply and demand dynamics. However, AAVE's supply and demand are not isolated; they are nested within the broader context of the global economy.

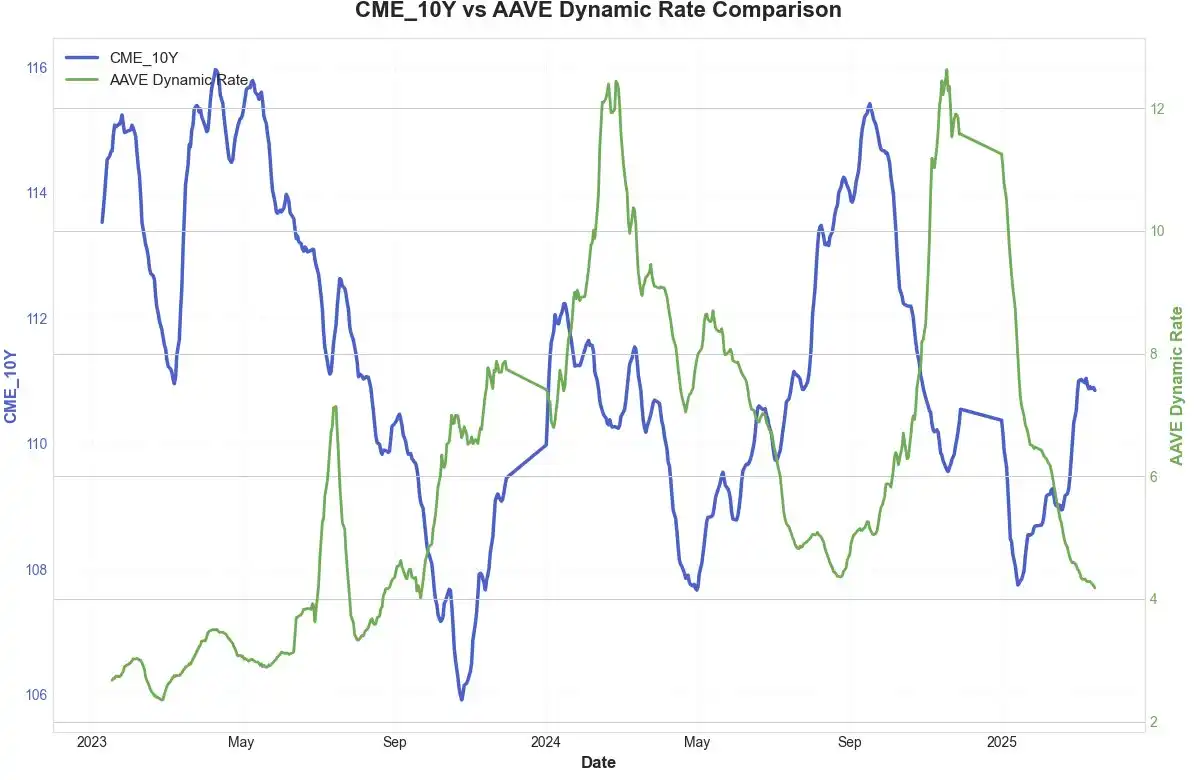

By comparing the smoothed USDC floating rate of AAVE with the CME 10-year Treasury futures prices, we can see this macroeconomic correlation:

The trend of AAVE's USDC interest rate aligns with global interest rates but exhibits a certain lag. The primary reason for this lag is the lack of an immediate linkage mechanism between global interest rates and AAVE rates.

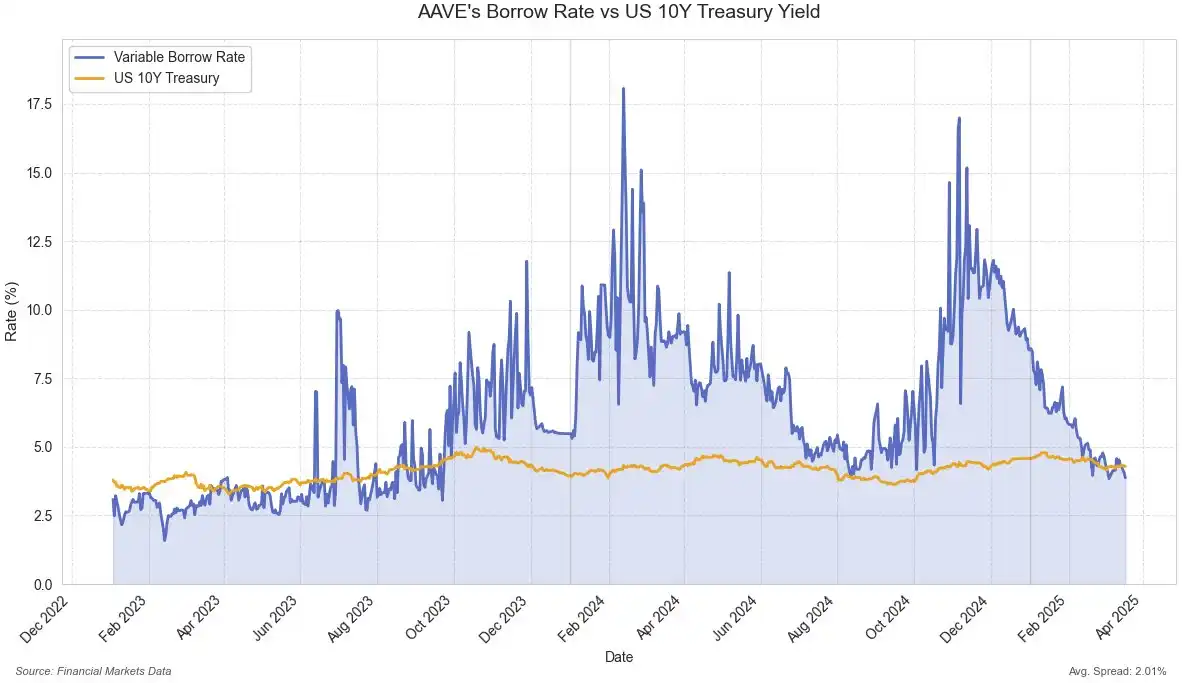

This disconnect means that the supply and demand dynamics of the crypto market play a stronger role in interest rate formation. When we remove the smoothing and directly compare AAVE's rates with global 10-year Treasury rates, this phenomenon becomes even more apparent:

AAVE's interest rate fluctuations are very volatile, and for most of the time, its rates have a significant premium compared to the US 10-year Treasury rates.

The fundamental reason for this premium is still the lack of direct correlation between these two markets. If there were a simple, two-way connection mechanism between DeFi and TradFi interest rates that could hedge or arbitrage, it would better integrate the two ecosystems.

Interest Rate Perpetual Swaps are the best way to achieve this. Perps have already been validated by the market for product-market fit (PMF), and establishing a perpetual market covering AAVE rates and US Treasury rates would bring about significant transformation.

For example:

- For borrowers, they can go long on an interest rate perpetual contract pegged to the AAVE borrowing rate. If the annual borrowing rate spikes from 5% to 10%, the price of this perpetual contract will rise, thus hedging the risk of rising costs.

Conversely, if interest rates fall, borrowing becomes cheaper, but the perpetual position incurs losses, akin to paying an "insurance premium." In this way, borrowers effectively lock in an effective fixed rate through borrowing + going long on the perpetual contract.

- For stablecoin lenders, they can short an interest rate perpetual contract based on the stablecoin lending rate. If lending yields decline, the short position on the perpetual contract profits, offsetting the losses from reduced loan yields; if yields rise, the short incurs losses, but interest income increases, creating a hedge.

Moreover, these contracts can also use high leverage. In the CME interest rate market, 10x leverage is a common configuration.

Having a liquid interest rate market can also reduce cascading reactions during market stress. If market participants hedge in advance, they will not be forced to withdraw or liquidate on a large scale due to interest rate fluctuations.

More importantly, this also opens the door to truly long-term fixed-rate loans—if this interest rate perpetual contract is fully DeFi-native, it can be used by various protocols for long-term interest rate hedging, thus providing users with fixed-rate loans.

In traditional finance, hedging interest rate risks is a routine operation, and most long-term loans have interest rate hedging tools behind them.

Introducing this mechanism into DeFi can not only enhance efficiency but also attract more TradFi players into this market, truly bridging the gap between DeFi and TradFi.

We can make the market more efficient, and all it takes is the emergence of an interest rate perpetual contract.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。