Author: Frank, PANews

When Bitcoin encounters a "value winter," real-world gold is being remade on the blockchain behind a curtain of value.

Recently, the volatility of the crypto market has become increasingly uncertain with changes in the international financial market, and the price trends of Bitcoin, Ethereum, SOL, and other mainstream crypto assets have also fallen into a slump. The market's enthusiasm for crypto trading seems to be shifting from optimism to a bearish outlook. In stark contrast, international gold prices have been rising, breaking through $3,240 per ounce, continuously setting new historical highs, once again validating gold as a safe-haven asset.

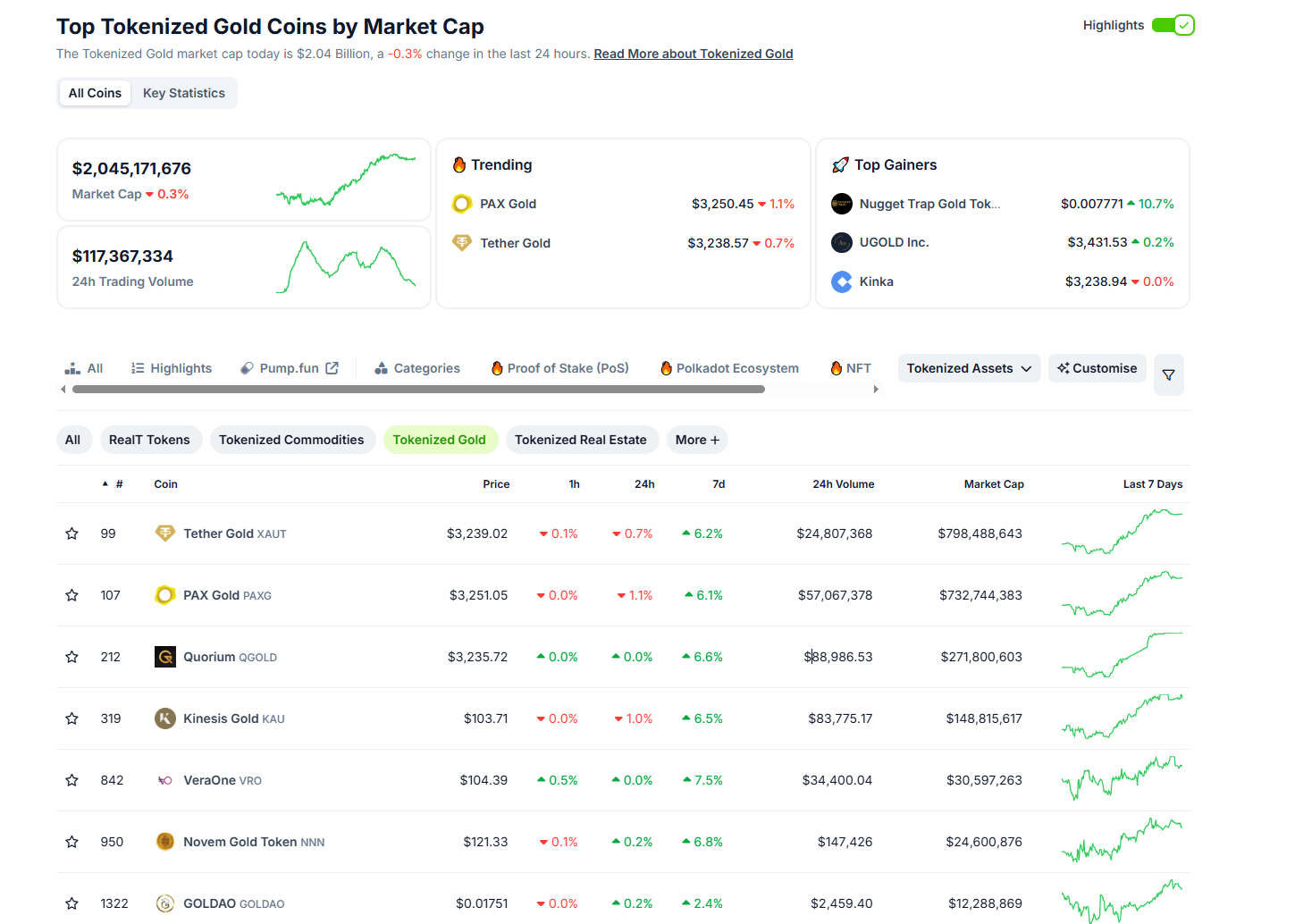

In the crypto market, the market value of assets linked to gold has also been on the rise, with the market capitalization of tokenized gold assets surpassing $2 billion on April 11. From a risk-hedging perspective, gold-related crypto assets seem to be becoming a new quality choice. PANews reviews the current mainstream gold-related trading exposures in the crypto market.

Currently, gold-related trading exposures in the crypto market are divided into tokenized gold, such as TetherGold (XAUT) or PAXGold (PAXG), which are essentially digital certificates of ownership of physical gold. There are also derivative trades using these tokenized gold assets in conjunction with stablecoins, such as spot trading pairs or contract trading pairs offered by exchanges. Additionally, some online precious metal traders support cryptocurrency as a payment method when trading physical gold. These methods of participating in gold vary in terms of risk preference and capital flexibility.

XAUT and PAXG: Leading Projects in Tokenized Gold

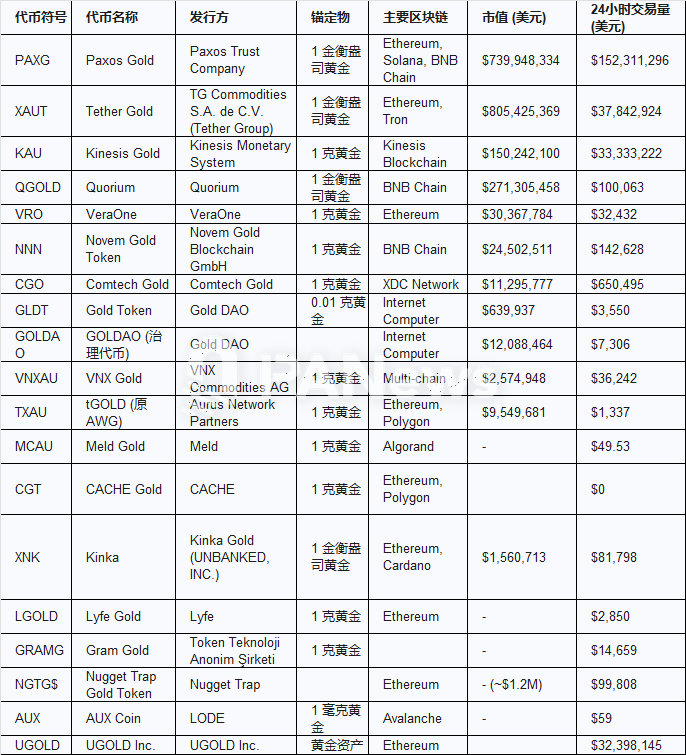

TetherGold (XAUT) and PAXGold (PAXG) are currently the two largest tokenized gold assets by market capitalization. XAUT is issued by Tether, the issuer of USDT, with 1 XAUT corresponding to the ownership of 1 troy ounce of gold from a specific LBMA (London Bullion Market Association) approved "good delivery" gold bar. The gold is designated for allocation, and holders can check the unique serial number, purity, and weight of the gold bar associated with their address through the official website. Tether claims that its reserves fully support the issued tokens, with XAUT backed by the gold portion of the reserves. As of April 12, the total support amount for XAUT was 7,667.7 kilograms of gold, distributed across 644 gold bars, with a market capitalization of approximately $797 million.

PAXG is issued by Paxos Trust Company, a trust company and custodian regulated by the New York State Department of Financial Services (NYDFS). PAXG also corresponds to the ownership of 1 troy ounce of London good delivery gold bars for each token. The monthly issuance of PAXG is reported by a third-party auditing company, and the report as of February 28 shows that the company holds 209,160 ounces of gold (approximately 5,929 kilograms).

PAXG is issued by Paxos Trust Company, a trust company and custodian regulated by the New York State Department of Financial Services (NYDFS). PAXG also corresponds to the ownership of 1 troy ounce of London good delivery gold bars for each token. The monthly issuance of PAXG is reported by a third-party auditing company, and the report as of February 28 shows that the company holds 209,160 ounces of gold (approximately 5,929 kilograms).

Compared to traditional gold ETFs or futures, both XAUT and PAXG tokenized gold have no custody fees and have a smaller minimum purchase amount.

The fee structure of PAXG differs from that of XAUT. Creating or redeeming PAXG directly through the Paxos platform incurs a tiered fee based on trading volume, while on-chain transfers incur a 0.02% Paxos fee. In contrast, XAUT claims no custody fees but charges a 0.25% fee when directly purchasing/redeeming. This means that for small users, trading PAXG on secondary exchanges may be more cost-effective than operating directly through the Paxos platform, avoiding creation or redemption fees. However, frequent on-chain transfers will incur additional costs for PAXG.

Self-Operated Mint Kinesis and Gold Mining Model Quorium

In addition, there are tokenized gold products with a market capitalization exceeding $100 million, such as Quorium (QGLOD) and KinesisGold (KAU). QGLOD has a unique business model, as the gold it holds is essentially mining reserves rather than physical gold. Furthermore, although the project claims to have regular reports on gold reserves, PANews found that these web pages are no longer accessible. Therefore, it is impossible to understand QGLOD's reserve situation. The information is vague, contradictory, and lacks key details verified by independent third parties. Particularly, the concept of "undeveloped reserves" raises unresolved questions about how it provides stable support for liquid tokens and how it is audited and valued, creating significant uncertainty and risk for investors.

Additionally, QGOLD's market data presents some warning signals. Its market capitalization (approximately $270 million) is relatively high, but its daily trading volume is abnormally low (around $100,000), concentrated in a few lesser-known exchanges. This severe mismatch between market capitalization and trading volume, along with insufficient transparency, seems to undermine the security of QGLOD.

KinesisGold's pricing method differs from PAXG or XAUT, using a model where each token represents 1 gram of gold. Its core differentiation lies in its unique revenue-sharing model; unlike PAXG and XAUT, which only track gold prices, KAU returns a portion of the platform's trading fees to holders in the form of gold (KAU). However, this revenue is neither fixed nor risk-free, as its size directly depends on the overall trading volume and fee income of the Kinesis platform. Additionally, Kinesis has launched a corresponding virtual card, allowing users to directly use KAU for daily consumption, which is another distinguishing feature of KAU. In terms of transparency, Kinesis chooses to conduct audits every six months and supports physical delivery for every 100 grams. Kinesis's official materials indicate that Kinesis operates a 5,600 square meter mint and refining facility, KinesisMint, producing high-quality gold and silver bullion products.

In terms of market circulation, XAUT and PAXG remain the two most liquid tokenized gold assets, tradable on multiple mainstream centralized exchanges and DEXs. KAU can be traded on its own KinesisExchange platform as well as on centralized exchanges like BitMart and Emirex, but its liquidity is slightly lacking.

Numerous Payment Exposures for Spot Delivery, Gold Tokens Struggle to Break the DeFi Dimension Wall

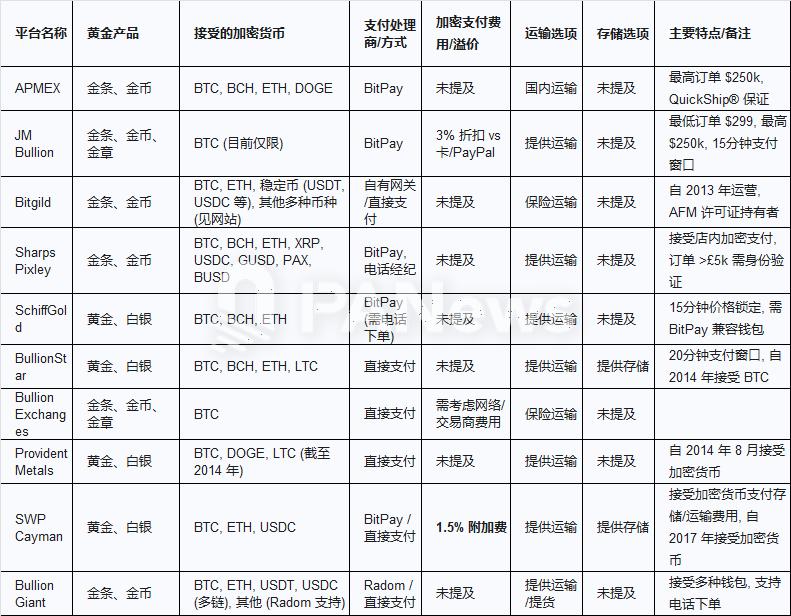

In addition to tokenized gold, many traditional precious metal traders also support payments in cryptocurrency. This gold exposure is mainly applicable to spot trading, where cryptocurrency is merely a payment method rather than a fundamental shift in the business model. Moreover, this type of trading usually requires a higher one-time investment threshold, and many platforms trade products like coins or gold medals, which means users may also need to have product identification and premium discernment abilities in addition to the intrinsic value of gold itself.

In addition to trading tokenized gold like PAXG or XAUT, some centralized exchanges offer different categories of gold trading. For example, Bybit offers gold contracts for difference (CFD), which allow traders to speculate on price movements of assets (like gold) without actually owning the asset. This type of trading is similar to index contract trading in financial markets, where users only track the price movements of gold to place contract orders but ultimately cannot deliver physical gold. Among mainstream centralized exchanges, it seems that only Bybit offers similar products, but many traditional XAU/USD CFD platforms now also accept cryptocurrency deposits, such as FP Markets, Fusion Markets, easyMarkets, etc. This trading method is more suitable for professional traders familiar with gold forex trading rather than cryptocurrency investors.

Furthermore, although gold tokens possess RWA attributes, the adoption of such products on mainstream DeFi lending platforms appears limited. Aside from PAXG, which can be staked for yield through Morpho, leading protocols like Aave and Compound have not accepted gold tokens as native collateral. This may stem from several factors: first, the challenge of having reliable, decentralized gold price oracles, which are crucial for the liquidation mechanism; second, potential regulatory uncertainties; and third, the relatively low market demand for gold tokens as collateral compared to ETH or mainstream stablecoins.

Overall, among the current exposures to gold assets in the crypto market, the most mainstream method may still be holding mainstream, highly liquid gold tokens like PAXG or XAUT. Additionally, while there are many similar tokenized gold products, users may need to consider the security issues involved when choosing these assets due to the identification of issuers and transparency issues. Purchasing physical gold directly from traditional precious metal traders that accept cryptocurrency payments provides the most direct ownership but also comes with higher thresholds and potential product premium issues. In the DeFi space, the participation of gold-related assets remains relatively limited, which may also be a challenge for the deep integration of most RWA assets with on-chain finance.

As Bitcoin holders in the current downturn begin to turn their attention to real gold, this not only marks a maturation of the crypto market but may also represent a counteroffensive of digital gold against the real world.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。