The problems won't suddenly become perfect, and comprehensive tariffs cannot resolve this complexity.

Author: Yuqian Lim

Translation: Deep Tide TechFlow

Fake Headlines and Stock Market Volatility

Earlier this week, the stock market surged significantly due to a fake headline claiming that President Trump might suspend the implementation of new tariffs for 90 days. However, just a few hours later, when people realized the news was not true, the stock market quickly fell again. This fake news originated from a Twitter account named Walter Bloomberg (which is not affiliated with Bloomberg and has shown signs of being operated by an individual), and it seems that the account copied a headline from somewhere (or perhaps intentionally manipulated the market, who knows).

The market's reaction is important because it reveals a strong desire for an end to tariffs. Investors are eager to believe any glimmer of good news, to the extent that even false information can trigger a market rebound.

However, so far, the government has not provided any real good news. On Tuesday, the market was filled with hope and was on an upward trend, but then, upon realizing that tariffs were imminent, the market let out a resigned sigh and quickly fell.

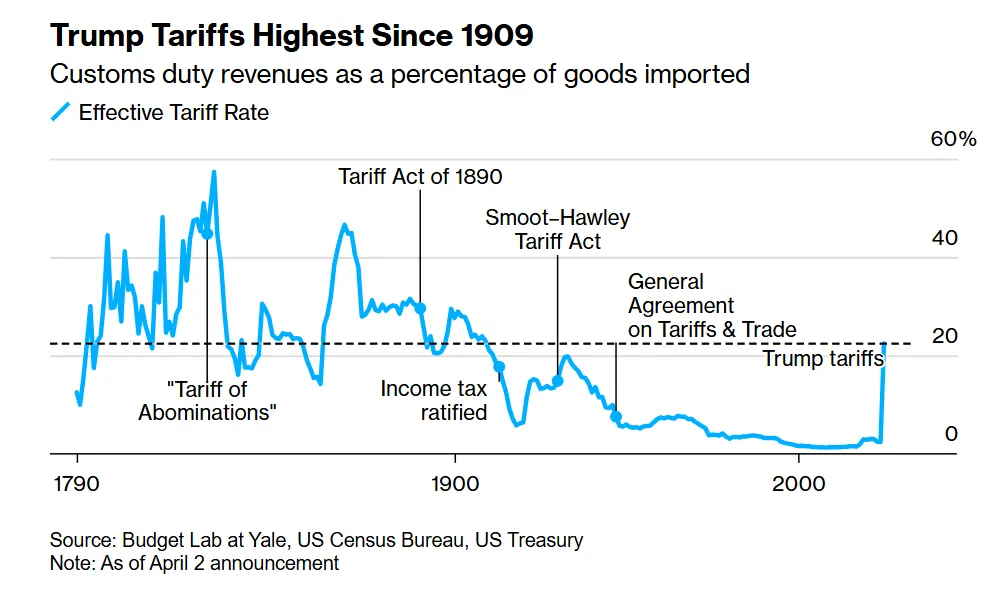

And indeed, these tariffs are coming—America's largest tariff increase in history took effect at 12:01 AM on April 9. In fact, these tariffs are so punitive that they are starting to reduce fiscal revenue, as Ernie Tedeschi has written.

There are many questions here: Why does the fantasy of 1950s factory America obscure the realities of modern labor and technology? Is the bond market failing? What actions will Congress take? How will China respond? What should we do next?

What’s Wrong with the Bond Market?

First, let’s look at the bond market.

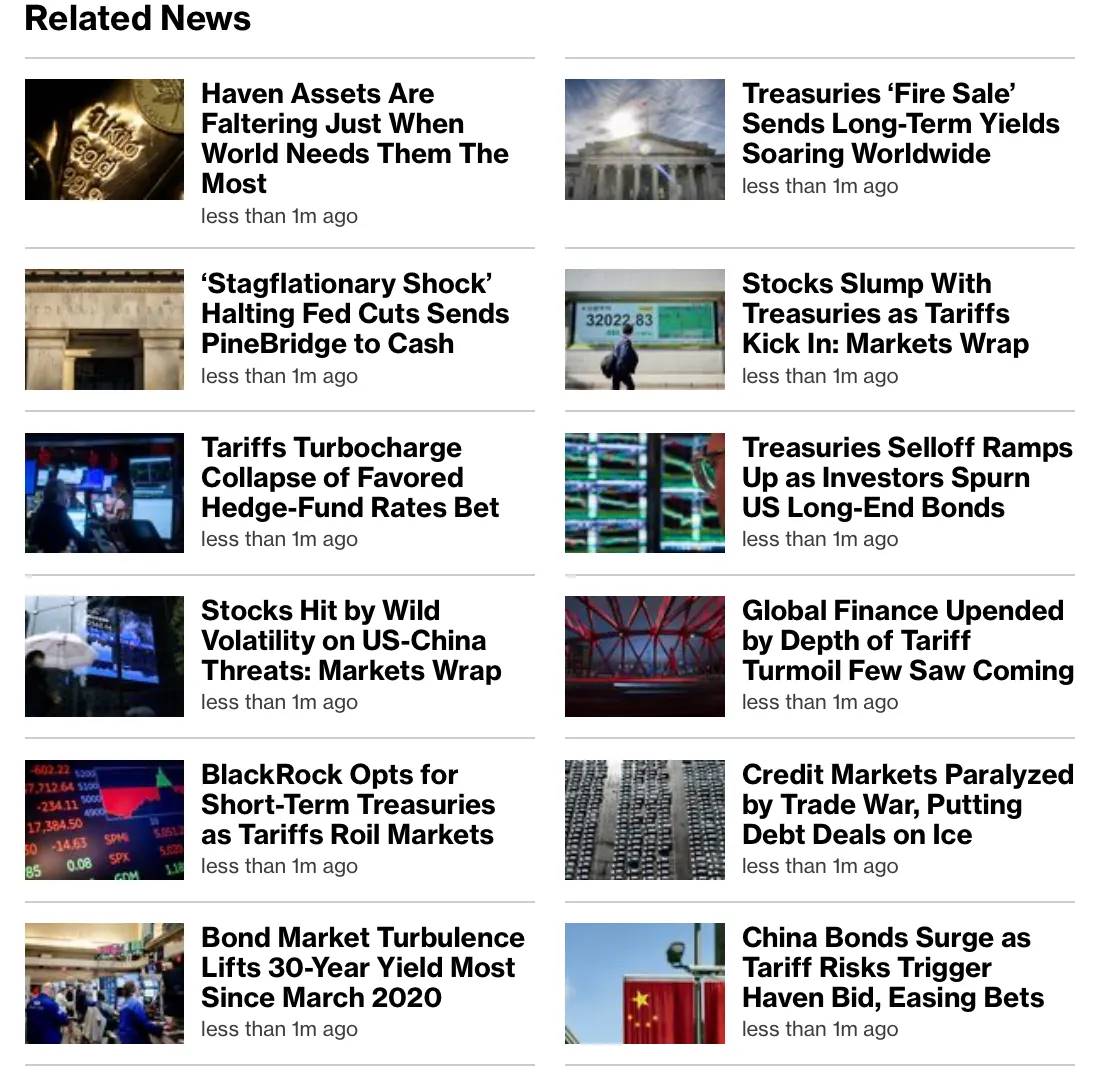

The bond market is selling off, and this is happening in the midst of a stock market crash. Right now, the U.S. is a risk to the world and is temporarily throwing the market into chaos. Here are some headlines that give us a sense of the current turmoil.

The stock market is down because tariffs will affect the real economy. Typically, when the stock market falls, we see money flowing into safe assets—when the market panics, people think, “Well, U.S. Treasuries look safe. The U.S. is a stable country; I’ll buy some Treasuries! Nothing will go wrong!” So, people buy Treasuries, pushing bond prices up and yields down.

But now, that’s not the case. Yields are rising, which means people are selling bonds, and this could signal the arrival of a new era. Why is this happening? Here are a few reasons:

China is selling off: The bond sell-off may be due to China or other foreign governments selling U.S. Treasuries in retaliation or fear.

Forced selling: As Matt Levine explains, market deleveraging could trigger the unwinding of underlying trades, leading to forced selling and even hedge fund blowups.

Safe haven status no longer: Perhaps people are starting to worry that the “safe haven” is no longer safe. If other countries believe the U.S. government might withdraw the Fed's currency swap lines for political gain, or suspect the White House might continue to impose tariffs until the economy collapses—they might decide, “Forget it, I won’t buy Treasuries, thanks.”

Market sentiment: This largely depends on people's perceptions. Market sentiment is indeed important because it is a leading indicator of actual data and market positioning.

This raises a tricky question—when and how will this situation stop? Right now, everything is falling—dollars, oil, bond prices, stocks, while credit spreads are soaring. This is also bad news for the real estate market. Everything is moving in a direction it shouldn’t be. So, who can do something about it?

Can the Fed or Congress Intervene?

Perhaps the Fed will intervene? But with inflation pressures so high (due to tariffs), the Fed cannot easily lower interest rates and has chosen to maintain the status quo, as San Francisco Fed President Mary Daly has said. Of course, the Fed could also engage in quantitative easing (QE) and buy some bonds, but this would further exacerbate inflationary pressures.

Congress can also intervene. That is their responsibility. Don’t forget, all these policies are being implemented in the name of emergency actions. They can halt these measures at any time. As The Washington Post wrote, “Seven Republican senators support a bipartisan bill that would cancel the new tariffs in 60 days unless Congress votes to approve them.” But they need at least 2/3 of the senators (and 20 Republicans) to override Trump’s potential veto. They don’t seem inclined to do so.

- Therefore, some senators—especially those from manufacturing-dominant states—may push for more targeted trade agreements to mitigate the impact of tariffs on local businesses. Others, particularly from regions where agriculture is the main employer, may lobby for exemptions or partial tariff relief to counter retaliation against U.S. agricultural exports. If the situation worsens, there may be relief programs for farmers, similar to previous tariff policies (though this would offset any revenue from tariffs).

At the state level, governors may negotiate local business collaborations or foreign direct investment agreements. For example, a state could offer tax incentives or streamline approval processes to attract businesses to set up shop locally, effectively creating small trade or investment zones. This could create tension between state governments and White House policies, but state governments need to protect local jobs.

The real issue lies with the federal government: Ideally, the government would eliminate tariffs, but such things don’t happen when policy becomes performative. According to Politico, as of the morning of April 9, Trump had refused to respond to anyone in negotiations (even though they “flattered him”), and now he is even talking about imposing tariffs on drugs.

The core of the yield issue is that the government wants to push it down to refinance debt at lower rates, reducing interest payments, and then move on. But now, not only is the possibility of recession looming, but yields are not falling—this is a perfect stagflation combination: high inflation, low economic growth, and high unemployment.

The Shift in World Order:

If you’ve read my previous articles, you’ll know I have been critical of these tariff policies (even before the election, when I first interviewed Erica York from the Tax Foundation). The current government’s basic demand is that other countries either pay new trade costs or forget about trading with us.

So, what does America really mean for the rest of the world? Many believe that America subsidizes other countries, but in reality, the opposite is true, as Ben Hunt has written.

The U.S. is a major beneficiary of a global system based on stability and trust. In fact, other countries have been subsidizing the American way of life. This stable system has been referred to as “Pax Americana,” where for nearly 80 years, the U.S. has provided security, open trade routes, and a stable dollar to other countries, in exchange for which these countries have allowed the U.S. to exert broad influence over global rules and institutions. As a result, the U.S. enjoys unique privileges, such as lower borrowing costs and a persistent trade deficit (which is not necessarily a bad thing), while other countries’ demand for dollars and U.S. Treasuries effectively subsidizes the American standard of living.

But now, the U.S. is demanding an extra fee that does not match any reasonable calculation (in fact, the mathematical models used are incorrect, as the American Enterprise Institute (AEI) has pointed out). Thus, countries are starting to question: “If the U.S. is going to nitpick every cargo ship and submarine, why don’t we just establish our own trade agreements and avoid this hassle?” As a result, we are pushing them away while also undermining our own advantage—trust.

All of this is changing, and perhaps the status of the reserve currency will change as well. In the past, we had one big question: “Will China replace the dollar?” But that question may be overly simplistic. We may see the formation of a series of “currency clubs,” as previously discussed by the International Monetary Fund (IMF), such as small groups or bilateral agreements, some based on digital clearing systems, some partially pegged, all gradually reducing dependence on the U.S.

Rather than a single competing currency replacing the dollar, we may see a patchwork currency system that collectively reduces U.S. influence. The end result is the same: a decrease in automatic demand for U.S. Treasuries, a more fragmented market, and a weakening of the “safe haven” reflex.

How Will China Respond?

Many believe that the ultimate goal of this game is to weaken China’s power. U.S. Treasury Secretary Bessent has stated that they may delist Chinese companies from U.S. stock exchanges because “all options are on the table.” Meanwhile, China has retaliated by imposing a 50% tariff on U.S. imports. This marks our official entry into a trade war.

The renminbi exchange rate is falling, and China is attempting to make its export goods more competitive through currency devaluation (this strategy is extremely complex and brings many secondary effects), while also possibly preparing for a capital war with the U.S. China is a difficult opponent to deal with for several reasons:

China's dependence on the U.S. is greatly diminished: China has diversified its export markets, sending more goods to Latin America, Africa, and Southeast Asia. The U.S. share of China's total exports is no longer as significant. Some might argue, “The U.S. is bankrupting all countries with these tariffs, making them unable to afford Chinese goods.” This statement sounds like rearranging the chessboard on another dimension, but it may hold some truth.

China can endure more pain than the U.S.: This is a complex argument, but in the last year of the Biden administration, the American public is angry due to inflation. If tariffs push inflation up again (which is likely, as tariffs from Trump's first term have already led to rising import prices), this could severely impact Trump's approval ratings (perhaps?), even though the government seems to believe this will solidify its standing among the general public. (To be frank, the current “general public” and “Wall Street” are almost the same thing.)

China has excellent factories: Unlike the U.S., China is not afraid of automation. Their factories have achieved a high level of automation, even complete automation.

This does not include many high-end electronics, batteries, and almost all products on Amazon that still rely on Chinese supply chains. If the U.S. truly wants to isolate China, then product prices will rise significantly. American consumers are accustomed to cheap goods, and one can imagine the reaction to such price increases.

We often assume that the decisions of large trade groups are government-led. But let’s not forget that tariffs are paid by companies exporting goods to the U.S., not by the countries themselves. Increasingly, multinational companies like Apple and Samsung may need to engage in some form of “corporate diplomacy” to ensure the continuity of their supply chains. They may need to establish new shipping routes and manufacturing bases outside the U.S., creating a quasi-private global network that could ultimately be more important than the official institutions dominated by Washington.

However, all of this is certainly very complex. As Scott Galloway has pointed out, Trump has caused significant damage to the “American brand,” which is undoubtedly bad news for American companies.

The Myth and Reality of Reshoring Manufacturing

One of the government’s official reasons is, “We just need to produce everything locally.” This reflects their excessive obsession with reviving traditional manufacturing. However, the reality is much more complex, and the following points are worth noting:

Manufacturing is actually growing: As Joe Weisenthal pointed out, driven by the Inflation Reduction Act (IRA) and the CHIPS Act, U.S. manufacturing has actually thrived over the past four years, and this growth has not relied on widespread tariff policies.

Nostalgia for a bygone era: The government repeatedly refers to scenes from the 1950s where workers assembled screws for phones, and Trump even prefers to compare America to the “Gilded Age” from 1870 to 1913 (when there was no income tax). These nostalgic images do have some political appeal: the image of steel mills or assembly lines symbolizes the strength of the American economy, especially after the two World Wars when the U.S. was the only country with production capacity. But that era is long gone.

This does not solve our social problems: Many people try to position themselves as representatives of the general public, such as certain commentators. They believe that returning to manufacturing is the key to solving problems. However, in reality, once given the opportunity, people have left manufacturing in droves. This is not to say that manufacturing is unimportant (it is indeed very important!), but the issues are far more complex than they appear.

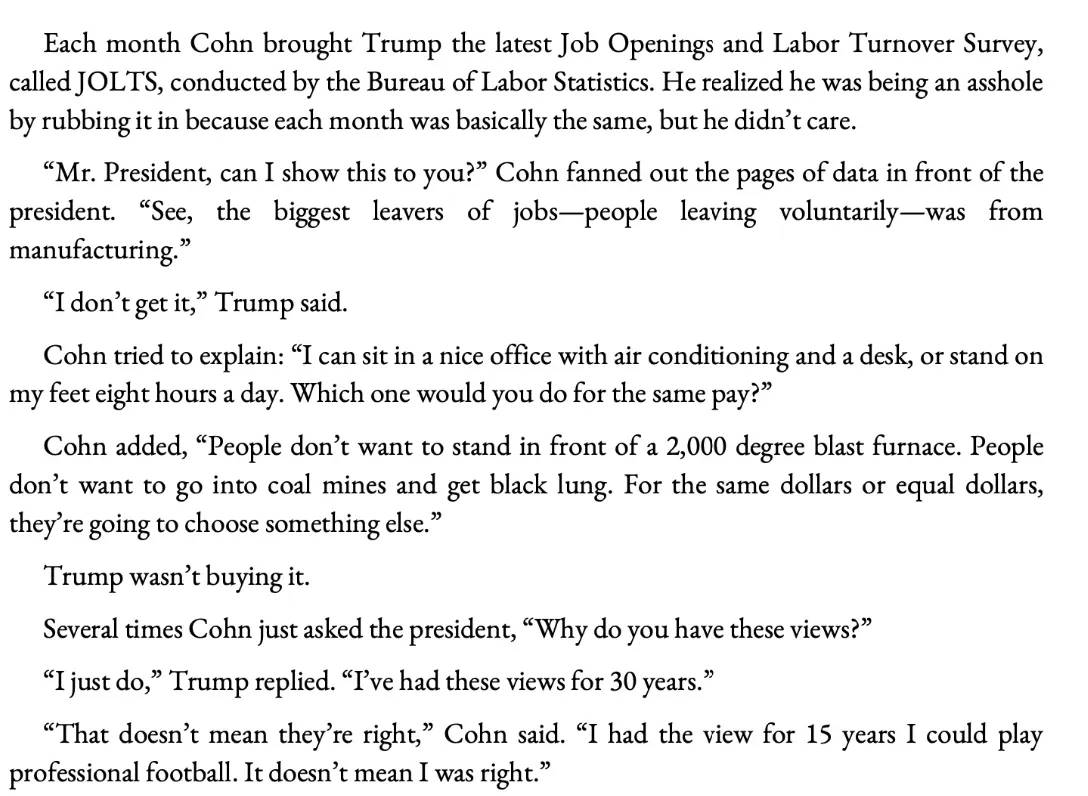

- Anecdote: Reflecting on Trump’s first term, Jordan Schneider shared a remark from Gary Cohn to Trump. People are leaving manufacturing partly because the work is both hard and monotonous. Although we have made significant progress in using machines to improve working conditions, if given a choice, people would certainly prefer jobs that do not involve screwing tiny screws into phones. In contrast, people would be more inclined to work in aviation or enter semiconductor factories (if the CHIPS Act had not been canceled, there might have been more such opportunities!).

- Concerns beyond Wall Street: David Bahnsen compiled a list of the impacts of tariffs on the economic lives of ordinary people (Main Street), showing a great deal of concern and fear. The belief that reshoring manufacturing can solve the “loneliness crisis” or other social issues completely misunderstands the real root problems in our world. The issues lie in the proliferation of smartphones and the housing crisis. When Trump took office, the U.S. was already at full employment.

- This will not bring back many jobs: The labor required to operate modern factories has significantly decreased, and the government acknowledges this. Today’s manufacturing jobs typically require higher skills, such as programming CNC machines, which necessitates labor training, faster approval processes, and support from factors beyond taxation. As Alex Tabarrok has detailed, tax incentives alone cannot solve these issues.

This leads to a “lose-lose-lose-lose-lose” situation.

If we push for onshoring production but rely on robots to do the work, we will neither gain cheap foreign labor nor create a large number of domestic job opportunities.

Therefore, you might see a reduction in foreign supply chains (which means a decline in America’s soft power), while also not witnessing a wave of new American jobs.

Under the influence of uncertainty, manufacturers are actually cutting back on spending. For example, Haas Automation (a company that produces CNC machines) has shown this trend, and Microsoft has also decided not to build its $1 billion data center in Ohio, a decision that will result in the loss of 1,000 jobs and cost the local economy $150 million annually.

Trump is trying to cancel the CHIPS Act, which makes everything even more uncertain. If you really want to promote manufacturing, retaining such policies is key!

Companies have stopped providing guidance for the future, as Sam Ro has written.

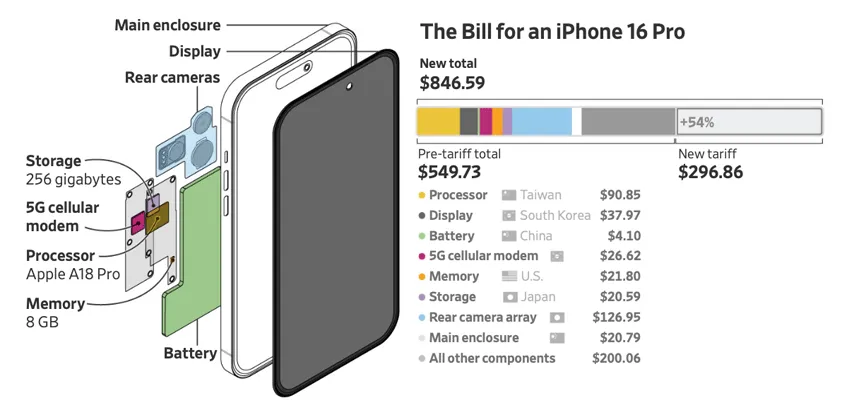

Even if we truly push for onshoring production—like Trump believes the U.S. can manufacture the iPhone 4—the costs will be extremely high. The Wall Street Journal (WSJ) has an excellent article that explores the scenario of manufacturing iPhones under tariff policies. Besides the enormous effort and cost required to shift production to the U.S., the final price of the phone will also become extremely expensive.

In discussions about manufacturing, people often focus too much on the production of goods while neglecting the areas where the U.S. truly excels—“financialization.” As Matt Levine has written:

Currently, many foreign countries sell goods to the U.S., obtain dollars, and use part of that to purchase American goods, while the rest is used to buy American financial assets. Under Trump’s system, these countries would have to use all their dollars to buy American goods instead of financial assets.

This means that other countries will no longer be able to purchase American stocks and bonds but must find a way to buy American-made goods. These goods need to be cheap enough for developing countries to afford, which will:

force the U.S. to significantly lower its standard of living to produce sufficiently cheap goods for export.

Indeed, the U.S. has a trade deficit in goods, but a surplus in services—finance, software, media, etc., are our strengths. If other countries develop parallel entertainment, payment systems, or capital markets, we will lose this intangible advantage.

Moreover, people completely overlook the fact that the U.S. cannot produce chocolate, bananas, or other raw materials. Some might say, “That’s okay, I don’t eat bananas,” but this view is too narrow and ignores how the global economy operates. For example, YouTuber Mr. Beast produces chocolate in the U.S., but the cocoa needed for it must be imported because the U.S. does not produce cocoa. Similarly, while you may not need to eat bananas, what about the small businesses (or even large creators) that rely on these raw materials?

Take coffee, for example. I had two cups of coffee this morning while editing this article, and the coffee beans came from Colombia. The U.S. cannot grow these coffee beans because the climate is unsuitable. Therefore, we have a trade deficit in coffee, but that is not a bad thing. Colombia has a comparative advantage in coffee production, and we buy their coffee because Americans like to drink coffee, and they use dollars to purchase other goods. Both sides benefit.

Frustratingly, we should not dream of manufacturing socks in the U.S. The real focus for America should be on advanced technologies such as artificial intelligence, chips, and biotechnology. If we decouple from foreign partners or punish them, it may accelerate their establishment of their own R&D ecosystems. If they succeed, it will reduce dependence on these critical technologies from the U.S. At that point, what we lose will not just be shoe factories, but the next wave of innovation. This is the deeper and more severe consequence.

Potential Next Policy Steps:

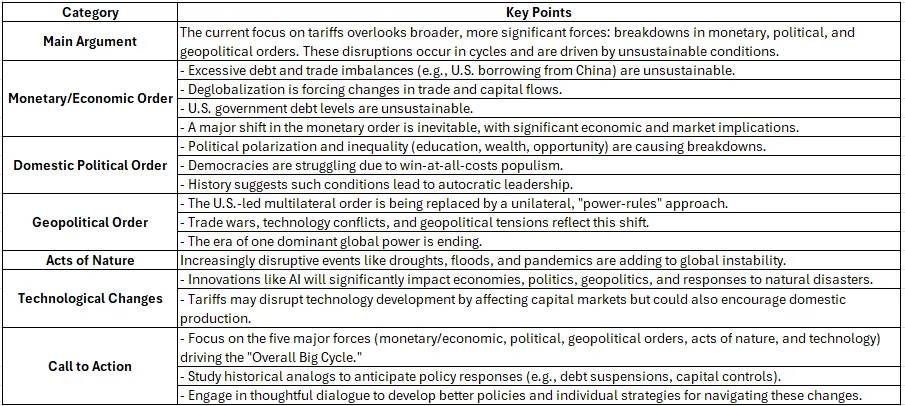

Ray Dalio has stated, “Everyone should note that this is not a tariff issue, but a debt issue, and we ultimately need to rebalance.” This does make some sense. He points out that we are in a turbulent world and need to find a way forward.

Ray Dalio is right. We are discussing a trust ecosystem that has taken decades to build. Until recently, the world was willing to inject funds into U.S. Treasury bonds and allow the U.S. to dominate many affairs because they believed the U.S. would be a relatively stable hegemonic power.

But if we continue to express emotions in unpredictable ways or view alliances as subscription fees, this intangible trust will gradually erode, along with the various benefits we derive from it—such as low borrowing costs, supply chain stability, and a dominant seat at the negotiating table. The "Overall Big Cycle" that Dalio speaks of has arrived, but solving problems by triggering a global economic recession and weakening industries is clearly not the optimal solution.

Even if the White House announces next month: “Oh, never mind, we’re not imposing tariffs anymore!” other countries have already seen the risk of the U.S. taking similar actions again. This alone is enough to prompt them to formulate contingency plans—such as strengthening trade ties with each other or seeking alternative reserve currencies.

How should the U.S. respond?

- Target real trade abuses:

Focus on verifiable intellectual property theft, forced technology transfers, or unfair subsidies. Instead of imposing blanket tariffs on entire industries, establish precise exemptions (e.g., for shrimp farmers) or impose punitive tariffs only on clear violations, thereby reducing collateral damage to U.S. businesses.

- Invest in labor and technology:

Restore the CHIPS Act! High-tech manufacturing incentives can encourage the construction of fabs in the U.S. without punishing consumers through blanket tariffs. Fund vocational training, apprenticeship programs, and community college initiatives.

- Develop smart industrial policies:

Modernize roads, ports, and broadband facilities to reduce supply chain friction and enhance domestic competitiveness. Instead of relying on tariffs, attract high-value industries through incentives, especially those critical to national security.

- Revitalize trade alliances:

Improve the USMCA or rejoin an improved version of the CPTPP under conditions that protect domestic interests.

- Global leadership:

Demonstrate policy consistency, stop making arbitrary statements on social media, and show commitment to fulfilling negotiation terms.

Let’s hope so. But what comes next? We can imagine several scenarios:

Slow fragmentation: The trade war will not trigger a single dramatic collapse but will gradually reshape the global system. Over time, the U.S. will become one of many important players rather than the global center.

Partial retreat: The government realizes that a recession is imminent and quietly rolls back some tariffs. The market calms slightly, but the damage is done, and trust remains low.

Full-blown crisis and reconstruction: A collapse in some sector—such as a massive sell-off of U.S. Treasury bonds or a breakdown in supply chains—forces all parties back to the negotiating table to establish a new Bretton Woods system. The U.S. may have to relinquish some privileges to restore stability.

In any case, we will not return completely to the previous "normal." Once the illusion of reliability or hegemony is shattered, it cannot be simply rebuilt. We may salvage a new balance, but it will be based on entirely new terms.

Meanwhile, nearshoring may skip the U.S., allies may be indifferent to our threats, and the "automation plus tariffs" strategy may ultimately fail to create a significant number of manufacturing jobs.

These tariff wars and bond market panics are not just short-term news; they may reshape capital flows, the formation of supply chains, and global cooperation on issues like financial crises and wars. We may not see a single catastrophic moment but rather a series of smaller collapses, ultimately forming a world where the U.S. is no longer at the core, and other countries have started anew.

Once we destroy this intangible trust framework, partial retreats will not fix it. If we do not recognize this early, we may get lost in a series of small crises and temporary alliances, ironically discovering that despite the flaws of the old system, it was actually the best deal the U.S. could have.

What can you do?

The following content is not investment advice and is for reference only.

- Check your portfolio:

Ensure you know how much stock, bonds, and other assets are in your portfolio. Consider diversifying investments overseas. Understand the specific composition of the ETFs or mutual funds you hold. A mix of stocks, cash, bonds with different maturities, and even other assets like real estate can help balance risk.

- Build a cash reserve:

Having a cash reserve (or near-cash assets) equivalent to a few months of living expenses is a good buffer if the market is volatile. This can prevent you from being forced to sell investments at inappropriate times.

- High-yield savings accounts (HYSA):

If you have a low-risk tolerance, consider putting funds into a high-yield savings account. These accounts not only generate interest but also allow for quick withdrawals when needed. Personally, I keep about half of my portfolio in such accounts.

- Avoid panic selling:

News headlines can be alarming, but panic selling is usually unhelpful. If you have a diversified long-term investment portfolio, short-term market fluctuations are often just "noise."

If you see concerning news, do not let fear dictate your decisions. This uncertainty will not disappear in the short term, so stay calm, clarify your investment time horizon, and adjust your portfolio's risk level to what you can accept. Thank you all!

- Discussion on tariffs:

I have discussed the issue of tariffs in detail in many previous newsletters and have interviewed Erica York from the Tax Foundation and Stan Veuger from the American Enterprise Institute (AEI) four times; no one likes tariffs!

- Impact of foreign investors:

Foreign investors hold 18% of the U.S. stock market, which may exacerbate market volatility.

- Simultaneous collapse of oil prices and the bond market:

The simultaneous collapse of oil and bonds is unprecedented. Russia is clearly not pleased about this.

- Complexity of manufacturing:

Consider the various inputs in the manufacturing process—processors, displays, camera modules, memory, batteries, glass, chips, casings, assembly, etc. This is a complex process, and establishing such production capabilities locally in the U.S. will take a long time.

- Importance of labor issues:

Regarding labor, it is important to note that we do outsource many external costs to other countries, where workers often perform very hard jobs for extremely low pay. Part of the reason is the existence of a development ladder—while the work is tough and the pay is meager, factory wages may be better than other options for emerging economies. The problems will not suddenly become perfect, and blanket tariffs cannot solve this complexity. In fact, if thousands lose factory jobs and fall back into extreme poverty, tariffs may worsen the situation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。