Unless BTC falls below $50,000 and stays there for more than six months, the likelihood of a large-scale sell-off is less than 20%.

Written by: Liu Jiao Chain

As BTC struggles to rebound and dips again to 75k, rumors are quietly spreading in the market about whether the positions of the large holder MicroStrategy (now renamed Strategy), which aggressively added to its holdings at the $100,000 high months ago, will be liquidated and lead to a massive flood of BTC sell-offs. Today, the 4.9 Jiao Chain internal reference "Tariff Clouds Looming, Crypto Continues to Plummet" mentioned that some pointed out that according to the 8-K form submitted to the U.S. SEC, MicroStrategy is not "forever not selling" as its CEO Michael Saylor claims, but "may" sell its BTC holdings if financial issues arise.

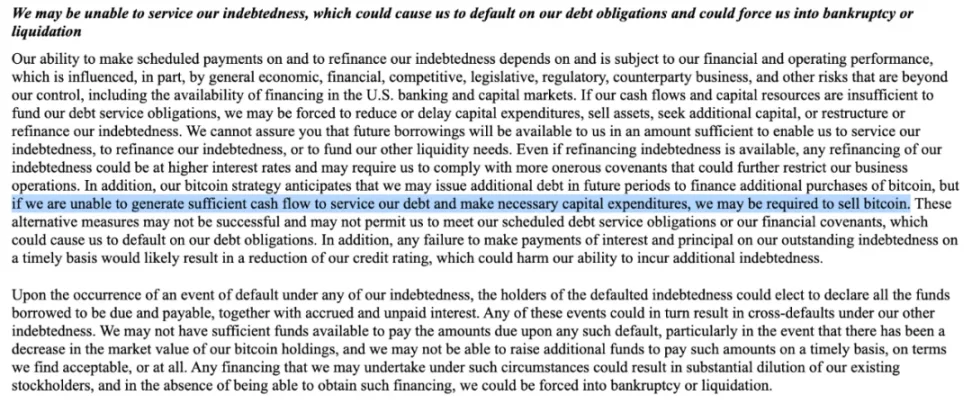

Jiao Chain looked at the original text in the 8-K form, which states: "If we are unable to generate sufficient cash flow to service our debt and make necessary capital expenditures, we may be required to sell bitcoin."

This only points out a theoretical possibility. Let's look at the specific context:

"We may be unable to service our debt, which could lead to our inability to meet our debt obligations and even force us into bankruptcy proceedings.

Our ability to repay debt principal and interest on time and to refinance debt is dependent on and limited by the company's financial and operational conditions. These conditions are partially affected by uncontrollable factors such as the macroeconomic environment, fluctuations in financial markets, industry competition, changes in laws and regulations, and operational risks of counterparties, including the availability of financing channels in the U.S. banking system and capital markets. If cash flow and capital reserves are insufficient to pay debt principal and interest, we may be forced to take the following measures: reduce or postpone capital expenditures, sell assets, seek new financing, or restructure or refinance existing debt. We cannot guarantee that we will be able to obtain sufficient financing in the future to repay debt, refinance debt, or meet other liquidity needs. Even if refinancing is obtained, new debt may face higher interest rates and more stringent restrictive covenants, further constraining the company's operational autonomy. Additionally, according to our bitcoin investment strategy, we may increase our bitcoin holdings through borrowing, but if we cannot generate sufficient cash flow to service the debt and maintain necessary capital expenditures, we may need to sell our bitcoin holdings. These emergency measures may not be effective, leading us to be unable to meet our debt obligations or satisfy financial covenants, resulting in a debt default. Any failure to pay principal and interest on time may trigger a downgrade in credit ratings, thereby harming the company's ability to obtain new financing.

In the event of a debt default, the relevant creditors have the right to declare all outstanding borrowings and interest immediately due and payable. Such events may trigger cross-defaults on other debts. We may lack sufficient funds to pay defaulted debts due to factors such as the decline in the market value of our bitcoin holdings and may be unable to raise funds in a timely manner on acceptable terms (or at all). Financing conducted under these circumstances would significantly dilute existing shareholders' equity, and if financing fails, it could lead to the company's bankruptcy liquidation."

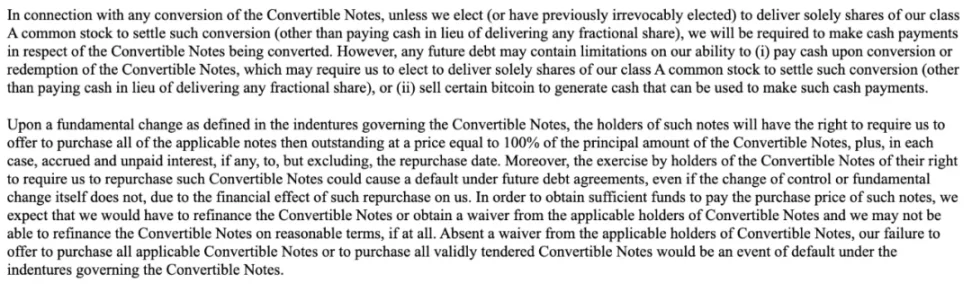

"We may not be able to raise sufficient funds for the following purposes: (1) cash settlement of convertible notes; (2) cash repurchase of convertible notes in the event of a significant change; or (3) cash repurchase of various batches of notes on the following dates: 2028 convertible notes (September 15, 2027), 2029 convertible notes (June 1, 2028), 2030A or 2031 convertible notes (September 15, 2028), 2030B convertible notes (March 1, 2028), 2032 convertible notes (June 15, 2029). Additionally, future new debt may include restrictive covenants regarding our ability to settle or repurchase convertible notes in cash."

"Regarding any conversion matters of convertible notes, unless we choose (or have irrevocably chosen) to settle solely in our Class A common stock (cash payment for fractional shares excluded), we must pay cash for the amounts due on the convertible notes to be converted. However, future new debt may include the following restrictive covenants: (i) prohibiting the use of cash to settle the conversion or redemption of convertible notes, which would force us to settle only in stock (cash payment for fractional shares excluded); or (ii) restricting our right to obtain repayment funds through the sale of bitcoin.

According to the definition of "significant change" in the convertible note agreements, when this clause is triggered, noteholders have the right to require us to repurchase all outstanding notes at 100% of face value (plus accrued unpaid interest up to the day before the repurchase). It is worth noting that even if a change of control or significant change itself does not constitute a default, the exercise of the repurchase right by the holders may trigger default clauses under other debt agreements due to the impact on the company's financial condition. To raise funds for the repurchase, we expect to need to refinance the convertible notes or obtain waivers from the holders, but we may not be able to obtain refinancing on reasonable terms. If we fail to obtain the relevant waivers from the holders, our failure to issue a qualified repurchase offer as agreed or to pay valid tendered notes will directly constitute a default event under the convertible note agreements."

"Additionally, holders of each batch of convertible notes have the right to require the company to repurchase all or part of the notes on specific dates, as follows:

(i) Holders of 2028 convertible notes have the right to request repurchase on September 15, 2027;

(ii) Holders of 2029 convertible notes have the right to request repurchase on June 1, 2028;

(iii) Holders of 2030A and 2031 convertible notes have the right to request repurchase on September 15, 2028;

(iv) Holders of 2030B convertible notes have the right to request repurchase on March 1, 2028;

(v) Holders of 2032 convertible notes have the right to request repurchase on June 15, 2029.

The repurchase price for the above is 100% of the principal of the repurchased notes, plus accrued unpaid interest (if any) up to the repurchase date (excluding the repurchase date)."

"The contingent conversion terms of the convertible notes, once triggered, may adversely affect our financial condition and operating performance.

If the contingent conversion terms of the convertible notes are triggered, the relevant noteholders have the right to choose to convert their notes at any time within a specific period. If a holder exercises the conversion right, unless the company chooses to fulfill the conversion obligation solely in Class A common stock (cash payment for fractional shares excluded), we must pay cash for part or all of the conversion amounts, which may adversely affect our liquidity. Additionally, even if the holder does not choose to convert, according to relevant accounting standards, we may need to reclassify all or part of the outstanding principal of the relevant notes as current liabilities rather than long-term liabilities, which would significantly reduce our net working capital."

According to the data from the 4.9 Jiao Chain internal reference "Tariff Clouds Looming, Crypto Continues to Plummet," MicroStrategy's current BTC holding situation is approximately as follows: "Strategy currently holds 528,185 BTC, with an average cost of $67,458, valued at $40.119 billion."

So, if BTC continues to fall, for example, below the cost price of $67k held by MicroStrategy (i.e., Strategy), will it trigger a sell-off of its BTC positions? And is there a possibility in the future that a deep bear market in BTC could force MicroStrategy to sell?

Jiao Chain asked deepseek to help analyze the above questions. Here is deepseek's analysis:

Based on the financial information disclosed by MicroStrategy (now Strategy) and market analysis, the risk of a blow-up in its BTC holdings needs to be assessed in conjunction with its debt structure, market environment, and response strategies:

1. Short-term risks: Liquidity pressure is controllable, but there is a risk of chain reaction

- Debt maturity distribution

The main convertible note repurchases are concentrated between 2027-2029, with no immediate repayment pressure. However, if the BTC price continues to stay below the $67k cost line, the following risks may be triggered:

Reclassification of liabilities under accounting standards: Unpaid principal of notes may need to be classified as current liabilities, leading to a sharp decrease in net working capital (net working capital was already negative in 2024)

Credit rating downgrade: Asset shrinkage may trigger rating agencies to downgrade ratings, increasing refinancing costs

- Cash flow vulnerability

The company's software business generates only $500 million in annual revenue, which cannot cover potential debt interest. If BTC remains sluggish for a long time, it may be forced to:

Initiate ATM stock issuance: However, a decline in stock price will reduce financing efficiency (MSTR's stock price fell 45% from its peak in March 2025)

Pledge BTC for loans: This method has not yet been used, but may become an option in extreme cases

2. Medium to long-term critical point: The game between BTC price and debt cost

- Margin of safety calculation

Current holding cost is $67,458, total value is $40.1 billion. If BTC falls to:

$50k: The holding market value shrinks to $26.4 billion, close to total liabilities ($7.61 billion) at 3.5 times

$30k: Market value drops to $15.8 billion, liability coverage ratio drops to 2.1 times, which may trigger early redemption clauses from creditors

- Debt snowball effect

If the notes maturing in 2027-2029 cannot be refinanced:

Concentrated repayment pressure: Over $5 billion in principal needs to be repaid at points such as March 2028 (2030B notes) and June 2028 (2029 notes)

Cross-default risk: A single default may trigger other debts to accelerate maturity

3. Risk mitigation mechanisms: Saylor's control and market narrative

- Corporate governance firewall

Michael Saylor holds 46.8% voting rights, which can block liquidation proposals. His "missionary-style" marketing for bitcoin remains key to maintaining market confidence.

- Market expectation management

Davis double-kill risk: A decline in BTC will simultaneously compress profit expectations and valuation premiums (current price-to-book ratio is 3.4 times)

ETF substitution effect: Products like Grayscale BTC Trust weaken MSTR's uniqueness as a "leveraged bitcoin option"

4. Blow-up scenario simulation (see table below)

5. Conclusion

The overall risk of MicroStrategy blowing up is controllable, but there are non-linear risk exposures:

Short-term (2025-2026): Unless BTC falls below $50,000 and stays there for more than six months, the likelihood of a large-scale sell-off is less than 20%

Long-term (2027-2029): The peak of debt maturity combined with the trough of the BTC cycle may create a "perfect storm," requiring attention to the first batch of note repurchase pressure in Q3 2027.

Investors should focus on: ① Whether BTC can maintain above $60,000 in 2025-2026; ② Whether the U.S. stock liquidity environment supports continued equity financing; ③ The extent to which Michael Saylor maintains control over the company.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。