Stablecoin-supported payments are one of the most influential and adoptable use cases of cryptocurrency beyond BTC as a store of value.

Author: Nathan

Compiled by: Deep Tide TechFlow

The supercycle of stablecoins has arrived.

This is not only because the total supply of stablecoins has exceeded $230 billion, Circle has filed for an IPO, or because I often mention that "the supercycle has arrived." The more fundamental reason is that stablecoins are profoundly disrupting traditional payment systems, and this disruption will continue at an exponential pace.

My point is simple: stablecoins will surpass traditional payment methods because they are superior, faster, and cheaper.

However, the term "payment" covers a wide range. Today's payment systems are primarily dominated by traditional payment channels, banks, and fintech companies, each playing different roles in the Web2 payment system. Although stablecoins offer a more efficient and user-friendly alternative compared to traditional systems, the cryptocurrency payment system is gradually exhibiting a complexity similar to that of the Web2 system, which warrants a deeper analysis.

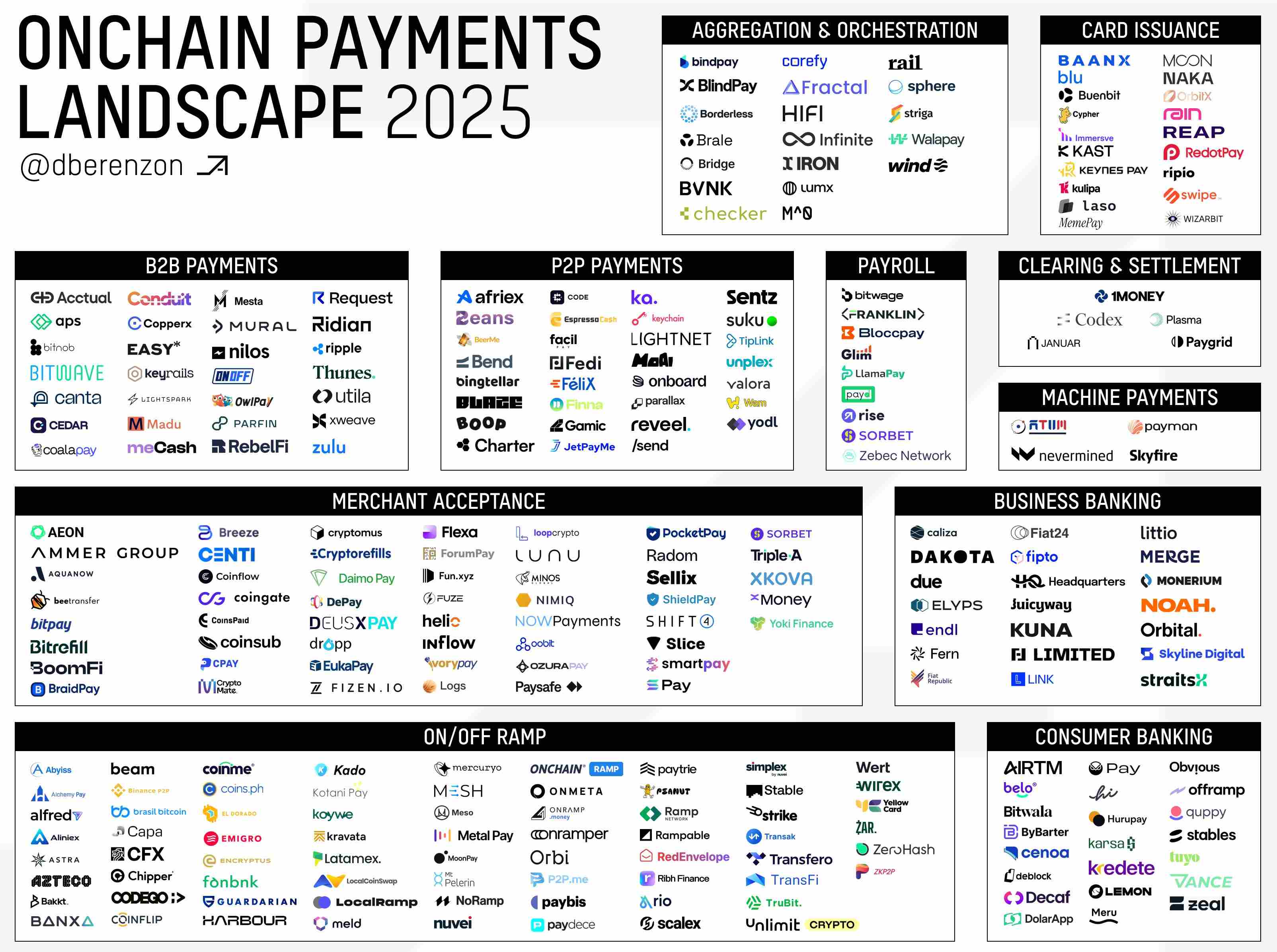

Currently, hundreds of companies are developing based on or around stablecoin payment channels.

@Dberenzon has organized a great page that breaks down the on-chain payment ecosystem into nine different areas, which you can find below.

Related link:

https://x.com/dberenzon/status/1889717634800758858

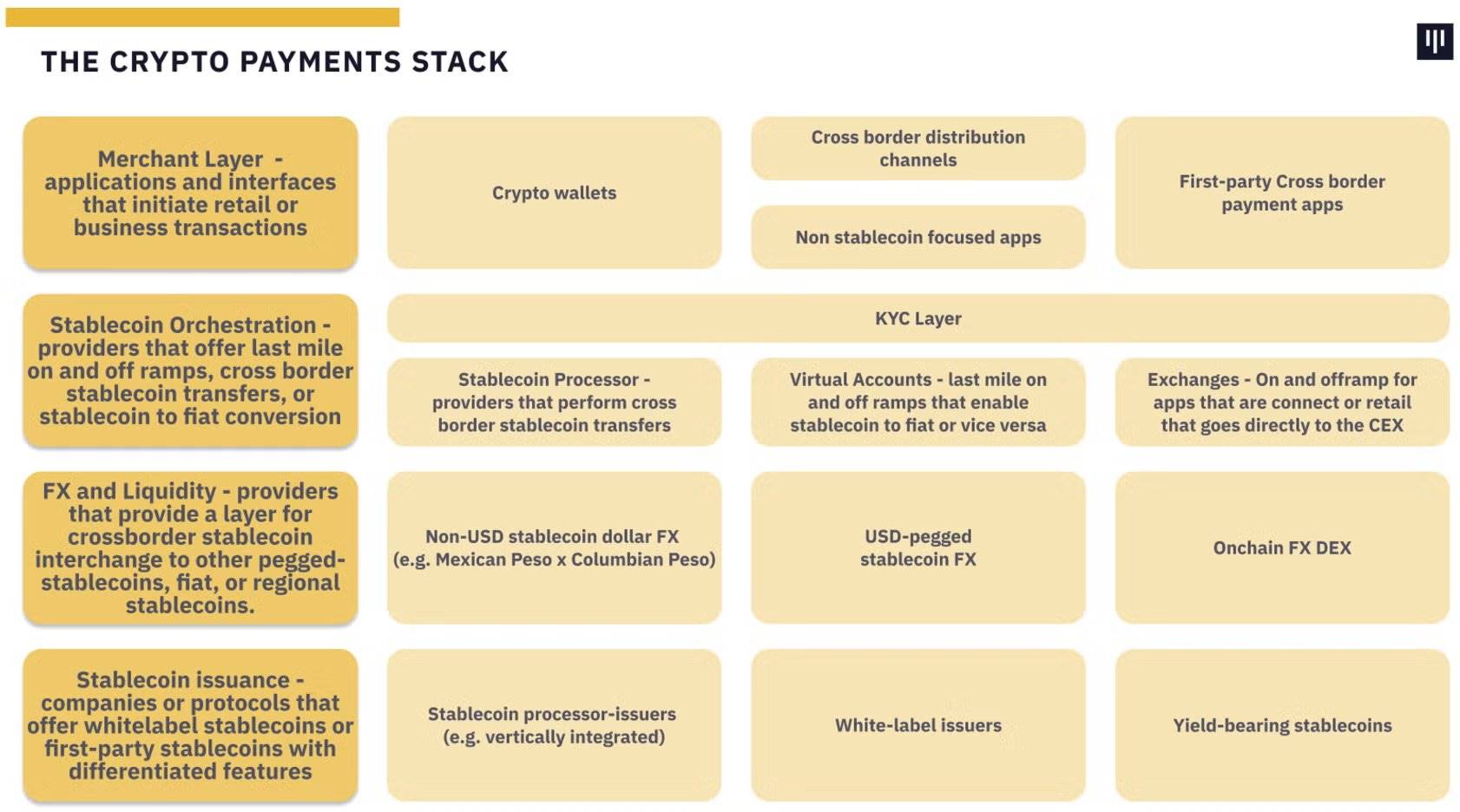

Dmitriy provides an in-depth and technical perspective, while other institutions, such as Pantera in their report “The Trillion Dollar Opportunity”, categorize the payment system into four levels from a higher perspective.

In this article, I will provide another way to dissect the payment system from the perspective of cryptocurrency's native first principles. However, the hierarchical divisions proposed by Dmitriy, Pantera, and others still offer valuable classifications from different angles.

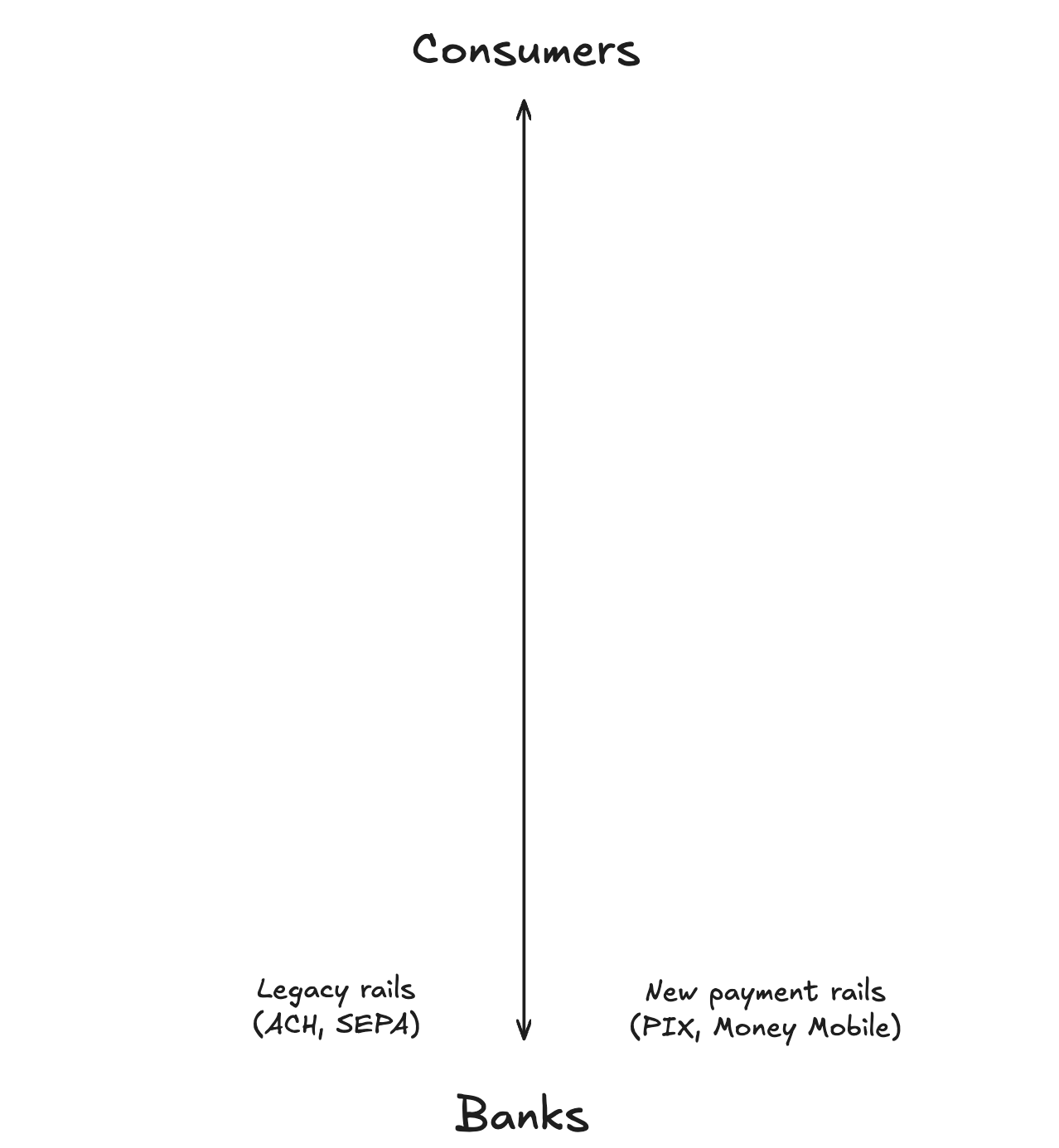

To provide some background, I believe the payment system operates along a vertical line, with one type of user at the top and another type at the bottom. Furthermore, I believe the ultimate goal of the payment system is to serve billions of users, so the aim of this analysis is to focus on ordinary retail users who may not even realize they are using cryptocurrency.

Cryptocurrency Payment System

From a first principles perspective, stablecoins are tokens on the blockchain that represent a unit of fiat currency—most commonly the US dollar. There are different types of stablecoins, including:

Fiat-backed (e.g., USDT)

Crypto-backed (e.g., DAI)

Synthetic (e.g., USDe)

Among these, fiat-backed stablecoins are currently the largest in scale. These stablecoins are backed 1:1 by highly liquid assets, including US Treasury bonds, cash, and other cash equivalents, held by custodians. Therefore, at the very bottom of the payment system, the users are traditional banks and payment systems.

As mentioned earlier, stablecoins are disrupting traditional payments because they are indeed superior, faster, and cheaper. This advantage not only brings higher profit margins for fintech and payment companies but also provides a better experience for end users. Thus, at the top of the payment system, the users are consumers.

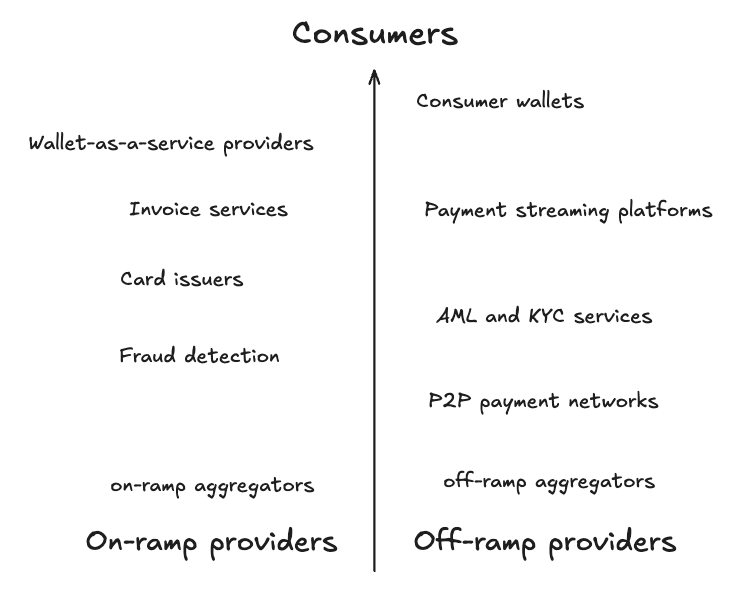

Currently, the structure of the payment system is illustrated in the following diagram:

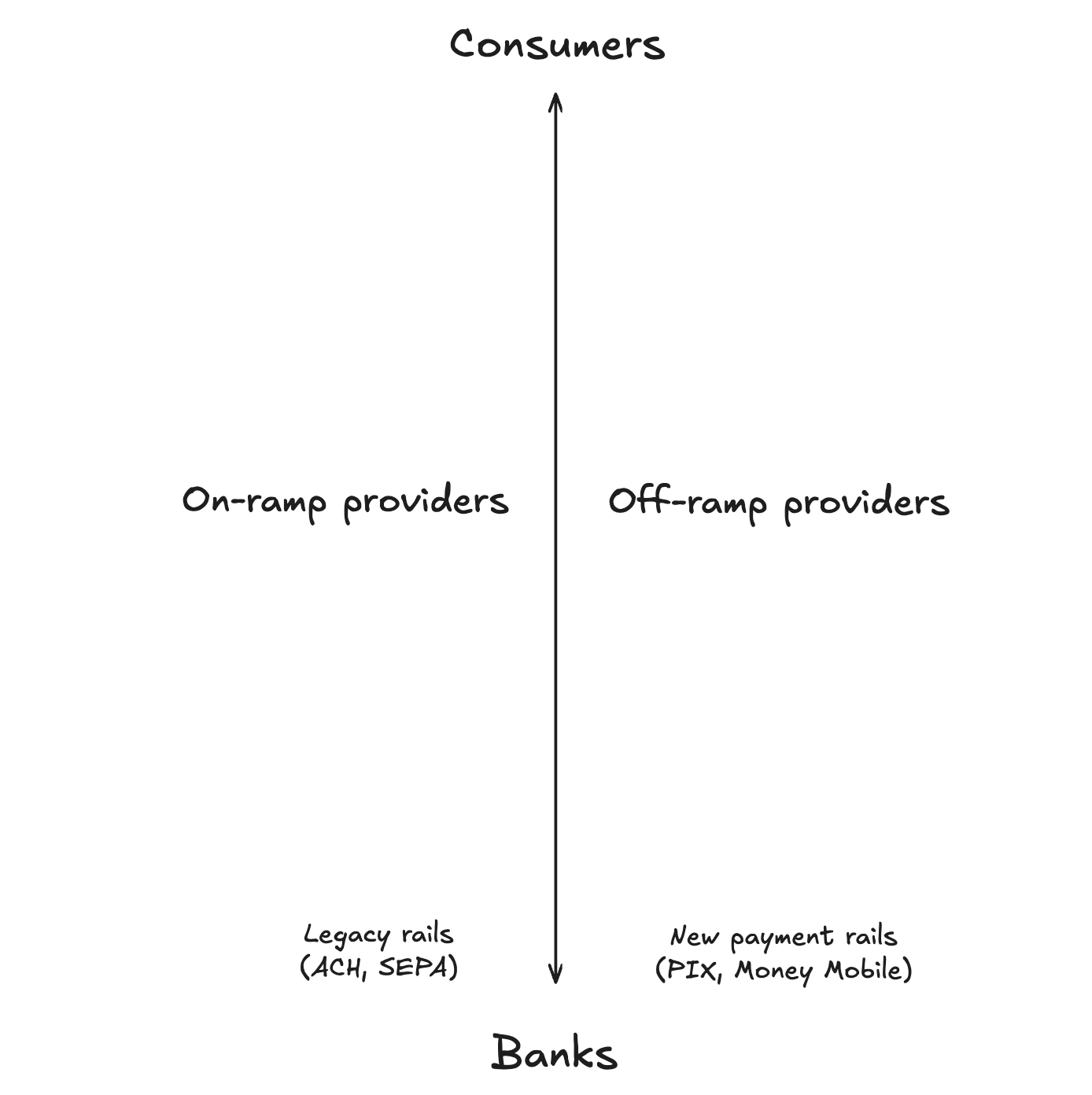

Next, let's look at the main application scenarios within the payment system. We have seen that one high-retention use case for cryptocurrency is "off-ramping." While "on-ramping" is also popular, the ability to easily use cryptocurrency (especially stablecoins) for consumption has always been the primary demand. In our system, the on-ramping/off-ramping service providers are positioned in the middle.

All parts above these service providers are consumer-facing applications or tools that support consumers, which I refer to as the "Consumer Services Layer." In contrast, the portion from on-ramping/off-ramping services down to traditional banks is the part that integrates stablecoins into the existing financial system, which I call the "Financial Integration Layer."

It is worth noting that the number of entities in the Consumer Services Layer is significantly greater than in the Financial Integration Layer. This is because building the Financial Integration Layer requires licenses, structured operations, and compliance requirements, while the Consumer Services Layer can leverage the services and relationships already established in the lower layer. Although the Consumer Services Layer may have other sub-layers, I emphasize those that play the most critical roles in the payment system based on functionality and dependencies.

Consumer Services Layer

From the consumer's perspective, the journey into the cryptocurrency payment system begins with wallets. Consumer wallets are not just storage tools; they are the entry point for users to save, spend, and earn cryptocurrency. Wallet functions include debit card payments, virtual banking services, and peer-to-peer transfers, designed to meet users' diverse needs. There are countless wallet options available in the market, some with global coverage and others designed for specific regional markets.

Developing a wallet is a complex task. It requires integrating multiple services while minimizing the risk of being hacked, which is why many companies choose to use “Wallet as a Service (WaaS) providers.” These providers deliver audited, battle-tested solutions that come pre-integrated with key functionalities such as on-ramping/off-ramping services and card issuers.

For consumer wallets to truly function, they must rely on various business-to-business stablecoin payment service providers. Core components include:

Invoice Services: These platforms allow individuals to issue invoices to employers in fiat or cryptocurrency. They are responsible for generating invoices, receiving funds, and converting currencies when necessary, then depositing the corresponding currency into the wallet.

Payment Flow Platforms: As companies become increasingly globalized, these platforms support seamless, recurring payments using stablecoins. This is particularly useful for employees in countries without local banking options.

Card Issuers: As cash payments decline, cryptocurrency cards become essential. By partnering with networks like Visa or Mastercard, card issuers enable wallet providers to issue branded debit or credit cards, enhancing convenience for everyday use.

Compliance plays a critical role at this layer as well. To protect consumer wallets, many platforms integrate strict “Know Your Customer (KYC)” and Anti-Money Laundering (AML) measures, along with on-chain fraud detection services. These service providers play an important role in the Consumer Services Layer, ensuring security and compliance.

Additionally, the Consumer Services Layer includes Peer-to-Peer (P2P) payment networks. These networks operate somewhat independently of the payment system, directly connecting individuals and businesses for cryptocurrency and fiat transactions. P2P solutions provide an alternative to traditional channels and have seen significant adoption in developing regions. However, P2P payment networks are less efficient, and the volume of settled funds is far lower than that of the entire payment system.

Finally, on-ramping/off-ramping aggregators sit at the bottom of the Consumer Services Layer. They consolidate multiple on-ramping/off-ramping service providers into a single, easy-to-integrate API, allowing wallet providers to automatically select the best option based on a combination of speed, cost, and regional service.

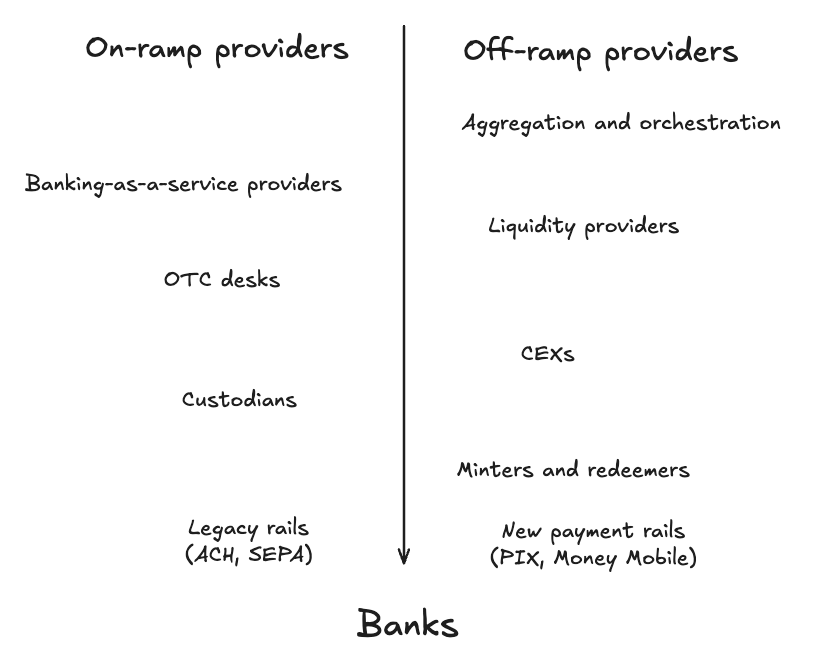

Financial Integration Layer

Entering the Financial Integration Layer, we arrive at the pillar part of the cryptocurrency payment system.

In many other payment systems, the part I am about to discuss is typically referred to as the “Aggregation and Coordination Layer.” However, to achieve aggregation and coordination, there must be lower-level support. Therefore, my view is that the aggregation and coordination layer sits at the top of this category.

Beneath this layer are the companies and services that help stablecoins and fiat currencies flow as seamlessly as possible. Here are three key layers that are typically aggregated and coordinated:

Banking as a Service (BaaS) providers: These platforms offer modular financial infrastructure, allowing companies to integrate virtual bank accounts, cards, and payment services into their products. BaaS providers manage compliance and backend operations, enabling businesses to offer bank-like functionalities without holding licenses themselves.

Over-the-Counter (OTC) desks: OTC desks handle large transactions, providing a liquidity bridge for companies lacking direct relationships with major exchanges or liquidity providers. They efficiently convert stablecoins to cash and vice versa, making the settlement of large transactions more practical.

Liquidity providers: Liquidity providers work closely with OTC desks to ensure sufficient funds are available globally to settle transactions. They abstract the liquidity sourcing process, eliminating much of the complexity involved in converting fiat to cryptocurrency.

In many cases, no company is willing to hold or manage wallets that may contain millions of dollars in stablecoins (or other crypto assets) themselves. Therefore, they rely on custodians to store liquidity in a trustworthy and insured manner. Custodians are positioned at the lower layer of the payment system, as almost all applications and services depend on them to store stablecoins as securely as possible.

Centralized Exchanges (CEX) also play a critical role in the Financial Integration Layer. They settle large-scale cryptocurrency and cash transactions by collaborating with liquidity providers and minting/redeeming services. CEXs hold reserves of stablecoins and cash, effectively facilitating transactions between both parties.

Finally, at the very bottom of the cryptocurrency payment system are the minting and redeeming services or companies. Tether operates through a limited network, allowing it to mint and redeem USDT, receiving cash directly into bank accounts or stablecoins through custodians. On the other hand, Circle's Circle Mint allows qualified companies, verified through "Know Your Business" (KYB) checks, to mint and redeem USDC.

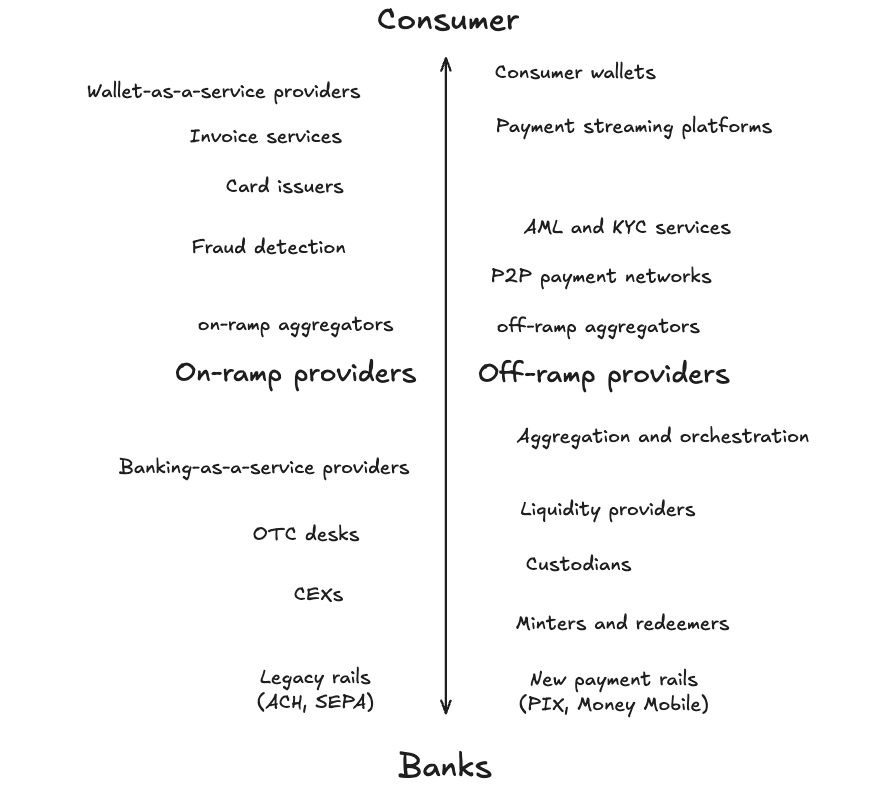

Complete Picture

The payment system is dynamic and highly interwoven. Each layer relies on the tools, services, and providers of the layer below it. Overall, the cryptocurrency payment system looks like this:

Summary Thoughts

Stablecoin-supported payments are one of the most influential and adoptable use cases of cryptocurrency beyond BTC as a store of value.

@PlasmaFDN, a blockchain designed specifically for stablecoin payments, is in a favorable position, but I expect that almost all blockchains will eventually turn to the stablecoin and payment space. To do this, they must rethink their payment systems, as merely being EVM (Ethereum Virtual Machine) compatible is no longer sufficient.

In summary, stablecoins indeed represent a trillion-dollar opportunity, and those participants playing key roles in the payment system will reap the greatest rewards.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。