Author: Luke, Mars Finance

On April 1, 2025, the crypto market was in disarray. The ACT token plummeted 55% in just 36 minutes, with its market value evaporating into thin air. A slew of altcoins followed suit, experiencing declines ranging from 20% to 50%. The liquidity-drained bear market felt like a meat grinder, leaving retail investors with nothing. Just as everyone lamented the arrival of the "altcoin zero era," an old face staged a "miraculous comeback"—EOS, now branded with the new label "Web3 Bank" Vaulta, surged over 30% in 24 hours, with its price breaking the $0.8 mark. This wave of buying acted like a flare, dazzling the eyes amidst the ruins of collapsing liquidity.

Looking back to 2017, the crypto space was a gold rush, with the cheers of Bitcoin breaking $10,000 still echoing. EOS entered the scene with the boast of "one million TPS." A year-long ICO raised $4.2 billion, marking one of the most extravagant "money-raising shows" in blockchain history. Founder Dan Larimer was hailed as a "technical prophet," and CEO Brendan Blumer became the "conductor of capital," with EOS positioned as the "chosen one" to dethrone Ethereum. Seven years later, its market value plummeted from $18 billion to less than $800 million, the community as desolate as a no-man's land, and Block.one was left battered by regulatory scrutiny. However, this "old horse" reignited controversy with its transformation through Vaulta and a 30% counter-trend surge amidst the collective collapse of altcoins.

Is EOS a "dead ember rekindled," or is it making a "last-ditch effort" before liquidity runs dry? Let’s trace back the ups and downs of these seven years, dissect Vaulta's movements, and explore the endpoint of this $4.2 billion marathon—will it be the rebirth of a "Web3 bank," or yet another tombstone in the crypto space?

From ICO Frenzy to Technical Waterloo: EOS's "Flash in the Pan"

The $4.2 Billion "Dream Machine"

In the crypto world of 2017, speculation was rampant. EOS seized the opportunity, proclaiming itself as the "ultimate blockchain solution": processing a million transactions per second, no fees, and a developer's paradise. This pitch attracted global capital like a magnet. Over a year-long ICO, EOS raised $4.2 billion, with ETH flowing in like water, setting an unbeatable record. That year, the air in the crypto space was filled with the scent of "all-in to get rich," and EOS became the brightest "dream machine."

In the spring of 2018, EOS's price soared from $5 to $23, with a monthly increase of over three times, briefly placing its market value in the top five. The election of 21 supernodes became a global event, with exchanges, mining pools, and retail investors scrambling for positions, and the community was fervent, as if EOS were the future "United Nations of Blockchain." At that time, no one doubted that EOS would become the "Ethereum killer," even Vitalik Buterin had to take notice.

The "Power Game" of DPoS and Technical Shortcomings

EOS's trump card was its DPoS (Delegated Proof of Stake) mechanism, with 21 nodes responsible for block production, theoretically outperforming Bitcoin and Ethereum in efficiency. But what about actual operations? This system became a "concentration camp for power": major exchanges controlled the nodes, rendering retail investors' voting rights worthless; on-chain arbitration institutions were manipulated, and the farce of frozen accounts led to a collapse of trust. Research indicated that most on-chain transactions on EOS were "empty rotations," with activity levels as low as a "digital desert."

Technically, the claim of "one million TPS" became the biggest joke. After the mainnet launch, the actual peak was just over 4,000, falling several orders of magnitude short of the promotional target. BM explained that "it relies on sidechains," but years later, the sidechain ecosystem remained sparse. Meanwhile, Ethereum broke through with layer technology, and new public chains like Solana and BNB Chain sprang up, causing EOS's "technical halo" to fade completely. Some joked: "EOS's TPS must have included 'one million dreams per second.'"

The "Self-Destructive Mode" of User Experience

EOS touted "zero fees," yet required users to exchange tokens for CPU and RAM resources. It sounded enticing, but using it was maddening: when the network got busy, resource prices skyrocketed, and transfer costs increased instead of decreasing; RAM was speculated to absurd levels, leaving developers in despair. During one peak period, a few thousand EOS could only be exchanged for a few seconds of computing time, and the operation was as complex as solving a math problem. Compared to Ethereum's "simple and straightforward" approach, EOS's DApp ecosystem quickly withered. By 2022, developers fled faster than rabbits, and even wallet and browser projects shut down.

Block.one's "Retreat" and the Community's "Self-Rescue Path"

The "Mysterious Flow" of $4.2 Billion

As the EOS ecosystem collapsed, all eyes turned to Block.one: where was the $4.2 billion? The company's response was to showcase a "capital magic trick" through its actions. The funds on hand were directed towards U.S. Treasury bonds, Bitcoin, and even vacation hotels, having nothing to do with the EOS mainnet. Now, they hold 160,000 BTC, with their wealth skyrocketing to $16 billion, yet they remain indifferent to the community's pleas for help. The community was furious: "We invested in a public chain, not for you to speculate on coins!" Some jokingly remarked: "Block.one is not a blockchain company; it's the Buffett of the crypto world."

Regulatory Scrutiny and Internal Chaos

In 2019, the SEC intervened, accusing Block.one of illegal fundraising and imposing a $24 million fine—just a drop in the bucket compared to $4.2 billion. The company paid the fine and continued to "silently amass wealth." Internal management was even more outrageous: the BB family operated the company, with relatives managing marketing and investments, while a plethora of money-burning projects yielded little results. BM was marginalized, becoming a "figurehead" in name only, spending more time discussing the "Bible" and the end of the world on Twitter than blockchain.

Community Takeover and the Rise of the Foundation: Why Did EOS "Not Die"?

Just when EOS seemed on the brink of collapse, the community stepped up. In 2021, the EOS Foundation (ENF), led by Yves La Rose, initiated a "rebellion," uniting 17 nodes to kick Block.one out and take control of the project. In the following years, the foundation engaged in a tug-of-war with Block.one; although they did not regain control of the $4.2 billion, they managed to pull EOS back from "barely alive" to "struggling to survive" through self-reliance.

Why didn't EOS die? Simply put, Block.one's inaction fueled the foundation's determination. They fought legal battles with the original project team for years, effectively taking over EOS's lifeblood. After all the turmoil, the foundation introduced several new concepts: RAM resource optimization, exSat Bitcoin expansion, and 1DEX decentralized exchange, ultimately rebranding as Vaulta. EOS's survival to this day is entirely due to the "tenacity" of the ENF team.

The Arrival of Vaulta and the "Self-Rescue Experiment" of New Concepts

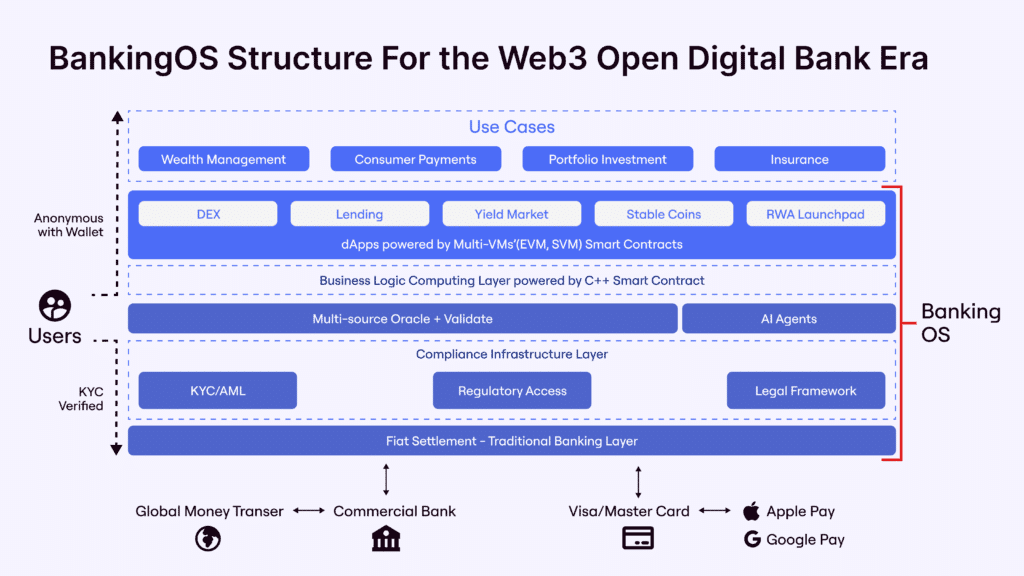

From Public Chain to "Web3 Bank": The Transformation Drama of Vaulta

In March 2025, EOS announced its rebranding to Vaulta, positioning itself as a "Web3 bank operating system," aiming to reshape finance with blockchain. The plan includes wealth management, consumer payments, investment portfolios, and insurance, along with a "bank advisory group" to lend credibility. Tokens will be exchanged 1:1 for new coins, with exchanges starting at the end of May, offering an additional 17% annual yield as staking rewards—this combination looks quite impressive. Some on X joked: "EOS has gone from 'Ethereum killer' to 'Bitcoin's little brother,' and now wants to be a bank teller; what a versatile chain."

However, a closer look raises suspicions of "same soup, different herbs." Vaulta's foundation still relies on the old EOS architecture, with its core selling points supported by new projects, while other functionalities have already been explored on Ethereum and Solana. Community reactions were polarized: optimists saw it as a "bottoming rebound," while pessimists scoffed: "It's just a name change to fleece investors."

RAM, exSat, 1DEX, RWA: The Foundation's New "Lifelines"

After taking over, EOS's "self-rescue" relied on these four strategies, which we will break down one by one:

EOS RAM: The hidden gem of the memory market: EOS's RAM (memory resource) is a unique design, essential for on-chain storage, with limited supply but increasing demand as DApps grow. The foundation optimized the RAM mechanism, launching XRAM (extended RAM), allowing users to stake tokens for resources while also sharing gas fees—this gas fee is directly given in Bitcoin. This innovative approach linked EOS with BTC, riding the wave of "digital gold." For instance, users staking a few hundred MB of XRAM can receive gas fee distributions in BTC, indicating that there is still demand in the RAM market, especially as new projects elevate its value. Some joked: "RAM is more like an asset than EOS tokens."

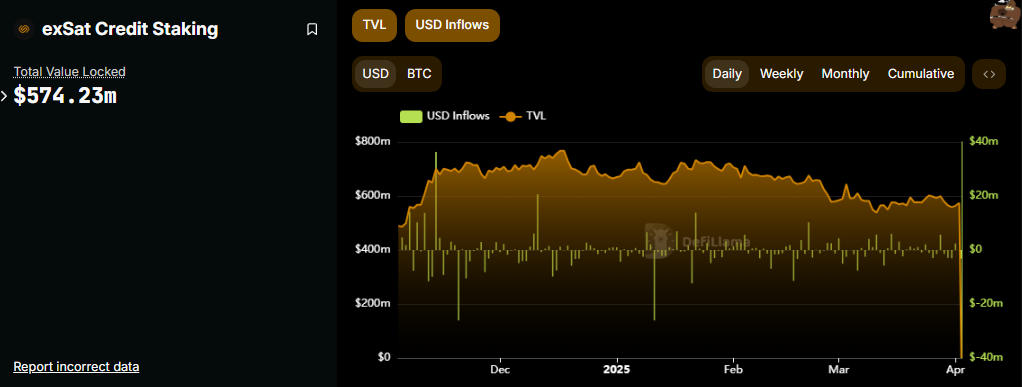

exSat: Bitcoin's "EOS plugin": exSat is a new attempt in 2024, using EOS's RAM to store BTC's UTXO data, aiming to solve Bitcoin's slow transactions and high costs. It sounds cool: BTC can run smart contracts and engage in DeFi, with EOS transforming into a "Bitcoin Layer 2." In March 2025, exSat locked up 5,413 BTC, with a total value of $587 million, far exceeding EOS's mainnet value of $174 million, seemingly becoming the "new leader" of the ecosystem. However, there are significant issues: Bitcoin's mechanism does not support staking, and the RAM capacity cannot support large-scale operations, leading the community to question: "Isn't this just painting a big picture for BTC?"

1DEX: The belated attempt at a decentralized exchange: 1DEX is EOS's newly launched DEX, aimed at filling the DeFi gap. EOS's mainnet is fast (1-second block time) and low-cost, theoretically suitable for trading, but unfortunately, the early resource model was too complex, driving developers away. Now, 1DEX is back, supporting unique asset trading and cross-chain operations, but it has not resolved EVM compatibility issues, and the documentation is poor, resembling a "half-finished product." Users on X have complained: "If 1DEX had launched five years ago, EOS could have captured some market share; now it feels a bit late."

RWA: Vaulta holders will soon have the opportunity to access exclusive investment options in tokenized real-world assets (RWA), including decentralized ownership in traditional illiquid markets such as real estate, commodities, and stocks. Strategic partnerships with leading tokenization platforms will unlock these complex financial products, significantly enhancing portfolio diversification and fostering a vibrant, liquid market.

Market Surge: The "Rebound Moment" with a 30% Increase

On the day of Vaulta's announcement (March 18), EOS surged 30%, jumping from $0.65 to $0.84. By today (April 1), it rose another 30%, breaking through $0.8021, with technical charts indicating a breakthrough of key resistance levels and a surge in trading volume, prompting some to shout "back to $1.4." Even more exaggerated, someone on X raised the question: "Is EOS about to perform another April 2018 miracle to save the crypto market?" Many newcomers might be confused, but seasoned investors remember: in April 2018, EOS skyrocketed from $5 to $23, with a monthly increase of over 360%, managing to rebound for a month during the bear market, becoming that year's "market savior."

Now, with Vaulta's continuous 60% rise and seamless technical alignment, it inevitably leads to speculation—can this old horse pull off another "dog-headed salvation"? However, veteran players scoff: "It's just a pump-and-dump routine." OKX and Binance preemptively launched trading pairs, quantitative robots saw "volume and price rise together," and FOMO sentiment was ignited—this wave of continuous gains feels like a "duet" of the foundation's self-rescue and new concept hype, or perhaps a prelude to the 2018 miracle? It depends on the subsequent momentum.

The Three Major "Behind-the-Scenes Drivers" of the Surge

- Concept Hype: Vaulta's "Web3 bank" narrative is fresh, with Bitcoin linkage and DeFi layout being speculative hotspots. Once the news broke on March 18, trading volume surged by 631%, with strong short-term buying pressure, and on April 1, it rose another 30% taking advantage of the momentum.

- Technical Signals: The daily chart broke out of the box, with a bullish short-term trend attracting a large number of traders. Some analysts even suggested that it broke a descending triangle, targeting $1.4.

- The Foundation's Last Stand: The ENF has been holding its breath for years, fighting legal battles vigorously, and with exSat and 1DEX gaining some popularity, the rebranding is a concentrated release, effectively giving EOS a new lease on life.

BTC Distributions from Staking XRAM: The "Unique Highlight" of the Ecosystem

In the EOS ecosystem, users staking XRAM can receive gas fee distributions in the form of BTC, which is quite intriguing. As a scarce resource, RAM still has a market even if the mainnet is barely alive, especially with the surge in demand after the launch of exSat. The gas fees are given directly in BTC rather than EOS tokens, indicating that the foundation no longer relies on the EOS token itself. After the Vaulta swap, governance functions may further weaken. This "quirky mechanism" has become a microcosm of EOS's transformation.

Can EOS Still Catch Up?

In the short term, if EOS can hold above $0.8, there is a chance for $1.4, and it might even be speculated into double digits. The BTC distributions from XRAM staking can continue for a while, and closely monitoring the progress of exSat and adjusting flexibly is a good strategy. However, there are three major vulnerabilities in the long-term outlook:

- Competitive Pressure: The Web3 banking sector is not new; Ethereum has MakerDAO, and Solana has Serum, while EOS's technical foundation is not superior.

- Implementation Challenges: exSat and 1DEX sound fancy, but their compliance and technical stability are questionable. Whether Vaulta's blueprint can be realized remains a big unknown.

- Trust Crisis: The "historical burden" left by Block.one is too heavy; no matter how hard the foundation tries, it is difficult to completely clear its name.

Conclusion

EOS's seven years reflect the crypto market's transition from fervor to calm. The $4.2 billion created a "technological utopia," but it fell into decline due to a broken user experience and chaotic management. After the foundation took over, RAM, exSat, 1DEX, and Vaulta became new tactics for "self-rescue," allowing EOS to remain "alive but not thriving." This recent 30% increase is fueled by new concepts and a market frenzy, but how far it can go depends on whether Vaulta can tell a complete story.

An old saying in the crypto world: "The biggest risk with EOS is that you dare not hold it." Facing this "old horse," do you dare to place your bet? Perhaps you should ask yourself if your heart is big enough. Because in the blockchain race, what is harder to gauge than code is the fluctuations of human sentiment. Your XRAM distributions are still there, and EOS's marathon has not stopped—this $4.2 billion journey will ultimately reveal whether the endpoint is a "bank" or a "tombstone."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。