Original Title: “Type III Stablecoins”

Original Author: STANFORD BLOCKCHAIN CLUB

Compiled by|Odaily Planet Daily Ethan (@ethanzhang_web3)

Stablecoins, as a key component of the cryptocurrency space, have seen their total market capitalization of liquid assets surpass $200 billion, firmly establishing their central role in today's crypto market. Some believe that the scale of stablecoins has decoupled from the volatile cryptocurrency market—despite a correction in the crypto market in 2025, stablecoins continue to demonstrate strong resilience, with an increasing number of traditional financial institutions integrating decentralized finance (DeFi) into their solutions.

Currently, stablecoins serve two main functions: fiat currency settlement and store of value (SoV). The daily trading volume of stablecoins has reached a historic high of $81 billion, with USDT and USDC capturing over 95% of the market share in both mature economies and emerging markets. They represent not just simple transactions but also financial inclusivity and the demand for low-volatility currencies.

However, the acceptance of yield-bearing stablecoins is vastly different from that of store of value stablecoins. Despite the continuous innovations in the DeFi space, yield-bearing stablecoins remain a niche application within the stablecoin ecosystem. The total market capitalization of yield-bearing stablecoins is about 10% of that of USDT and USDC.

What accounts for this disparity? More importantly, how can we improve the current state of yield-bearing stablecoins?

This article will explore the evolution of yield-bearing stablecoins, analyze the mechanisms of yield execution, and ultimately discuss how Cap addresses scalability and security issues.

The "Coming of Age" of Yield-Bearing Stablecoins: From "Survival" to "Profit Generation"

In earlier times, the yields of stablecoins primarily came from endogenous mechanisms; yields were entirely derived from DeFi platforms. Specifically, yields were generated through liquidity provision and platform rewards, creating a closed loop where users continuously jumped from one protocol to another in search of higher annual interest rates. Thus, the scale of yields could only increase with the expansion of platforms.

The most representative example is the crypto over-collateralized stablecoin or collateralized debt position (CDP). A typical example of a CDP is the early MakerDAO, which minted DAI by using ETH as collateral. This model generates yields by charging interest to borrowers who use their collateral to mint stablecoins. The interest is then redistributed to participants in the protocol, and the entire mechanism operates entirely within the DeFi ecosystem. However, the scalability of this model can only grow with the demand for ETH.

Another popular model relies on voting escrow tokens (veTokens), where locking these tokens allows protocols to distribute rewards to specific liquidity pools. This has led to the so-called “Token Wars”, in which stablecoin protocols compete for the ability to control liquidity pools to earn rewards from decentralized exchanges (DEXs). These token wars, such as CRV and BAL, involve strategies to drive yields by purchasing DEX tokens.

While the total value locked (TVL) in both of these models has reached billions of dollars, their yields are often highly volatile and speculative. Most importantly, the demand for these models is limited, especially when compared to applications outside of DeFi mechanisms, where demand appears relatively small.

As a result, founders have been striving across the industry to push for the expansion of stablecoins to break through the limitations of endogenous yield models. With the rise of more synthetic dollar strategies backed by fiat or other assets, from T-Bills to hedge fund strategy experiments, stablecoins are beginning to attempt to address the scalability issues of yield-bearing stablecoins.

So, what perspective should we adopt to view these new types of stablecoins?

The "Power Games" of Stablecoins: The Survival Rules of Three Types of Players

The core concept of yield-bearing stablecoins is as the name suggests: reserves issue new currency by lending out high-liquidity assets to execute investment strategies.

Aside from choosing supported assets and lending parameters, the core distinction of yield-bearing stablecoins lies in how they execute yields: who decides which strategies to implement? In the event of bankruptcy, how do users maintain their rights?

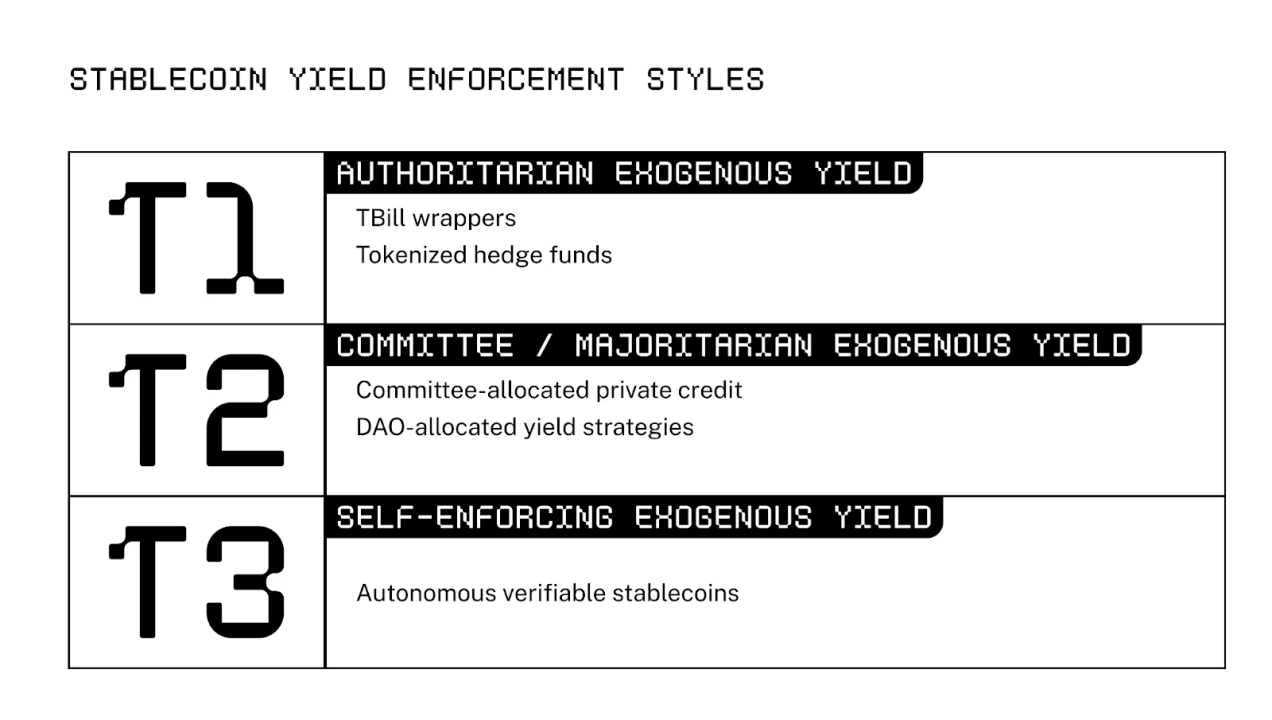

In other words, the framework relied upon when assessing execution mechanisms is the capital allocation mechanism and security guarantees. Currently, there are mainly two execution methods in the DeFi space: dictatorial and committee-based. This article also introduces a third type—the self-reinforcing yield mechanism that the Cap team is pioneering.

The following sections will delve into each type of stablecoin, particularly focusing on capital allocation and security incentive mechanisms, as well as the corresponding trade-offs.

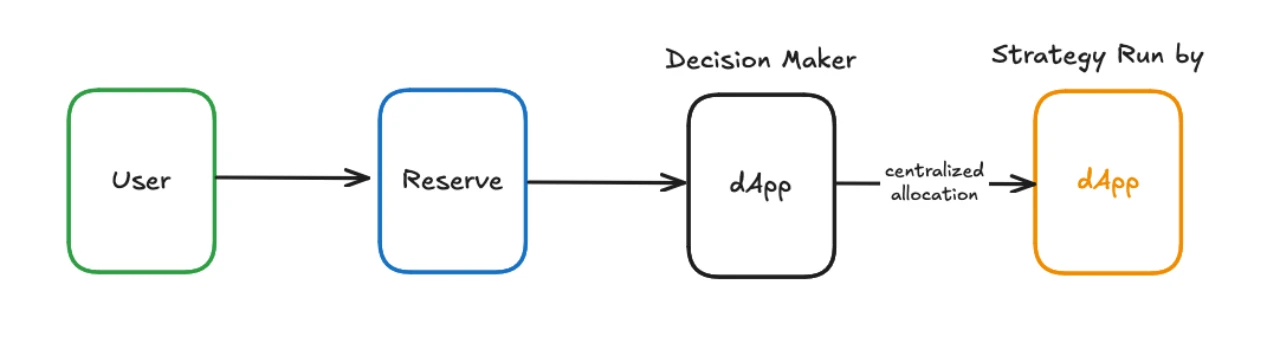

Type One: The Dictator's Dilemma—Efficiency and Risks of "I Call the Shots"

The first type of stablecoin operates in a unilateral market, where a single entity utilizes depositor capital to generate yields. Examples of this type of stablecoin include Ondo, Ethena, Usual, Agora, Resolv, and other teams operating strategies supported by synthetic assets. They are akin to hedge funds, with dApp teams selecting and executing a single (sometimes few) strategy. As the name suggests, the first type of stablecoin is centralized, with the team having the final say on capital allocation and recourse. Depending on the team, they may offer security guarantees including over-collateralization, decentralization, and transparency, but this is at the team's discretion, thus concentrating risk.

The primary motivation for adopting this model is to reduce development costs for the team and enhance user agency. Development costs are low because the protocol focuses on a single strategy (such as basic trading). At the same time, users can switch between different stablecoins of this type, choosing specific strategies.

Incentive Mechanism Adjustments

In this model, the decision-makers are the dApp teams. Generally, the team will optimize yields and security to attract more users. If the yields are not competitive, or if user funds suffer losses, as more projects are launched, the project may quickly become obsolete. Therefore, the team's attention is often focused on continuously growing TVL and maintaining competitive yields.

In theory, the team should minimize the risks of the strategies. However, these stablecoins often exist in the form of bankruptcy-remote entities, and users have no means to protect their rights through regulatory or legal channels, so the team does not have to prioritize user protection and transparency as strictly regulated financial institutions do.

Trade-offs

The main reason for choosing the design of the first type of stablecoin is simplicity. Since this model can concentrate resources to achieve a single strategy, they have lower startup costs and can also reduce concerns about potential vulnerabilities. Another advantage is user choice. By focusing on one or two strategies, the team returns decision-making power to users, who can shift funds between different applications based on market changes.

However, as mentioned earlier, the first type of stablecoin often lacks effective recourse mechanisms. Their operation resembles unsecured loans to application teams. If a strategy leads to losses, the custodian goes bankrupt, or the team absconds with user deposits, users have little recourse to recover their losses. Moreover, due to the lack of regulation, teams may protect themselves through legal structures, thereby evading responsibility.

Another key issue is the obsolescence of strategies—no strategy can indefinitely generate returns that exceed the market efficiently. When a team selects a strategy that aligns with market conditions, it may achieve over 30% abnormal returns. However, as market conditions change, the team's yields gradually diminish or become diluted as scale increases. At this point, the team must continuously seek new strategies to adapt to market changes.

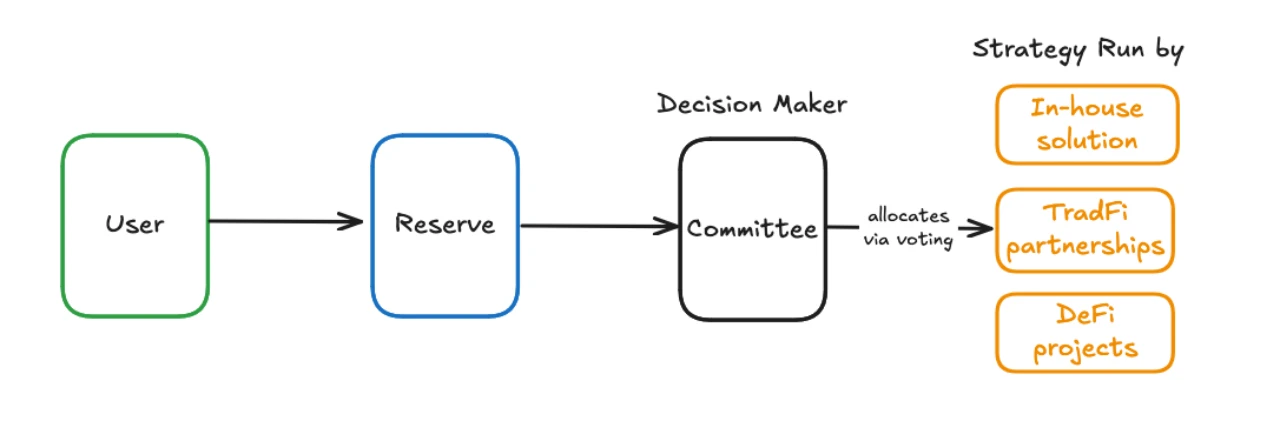

Type Two: The Committee's Game—Can "Collective Decision-Making" Cure All Ills?

To address the issue of strategy obsolescence, the second type of stablecoin introduces a mechanism for multiple strategies to operate in parallel. Examples of the second type of stablecoin include Maple and Sky (formerly MakerDAO). They delegate user deposits to various yield strategies through the establishment of committees or decentralized autonomous organizations (DAOs), including teams from the first type of stablecoin as well as banks and market makers from outside the crypto space. Thus, this model shifts the execution responsibility from a single team to a collectively decision-making organization.

The primary motivation for adopting the second type of stablecoin is scalability. If the current strategy fails to yield substantial returns or poses excessive risks, the DAO can decide to switch to a better strategy, thereby providing users with stronger guarantees of robustness.

Incentive Mechanism Adjustments

Overall, the capital allocation decision-making is completed by three parties: governance token holders, representatives, and committees.

The goal of governance token holders is to vote for the most expressive and scalable third-party strategies. Unlike governance tokens in the first type of stablecoins, governance token holders in the second type have greater decision-making power, allowing them to exert more influence on the DAO's decisions in open forums. However, it should also be noted that governance token holders are not necessarily the participants who understand risk management the best.

Representatives are actors without governance tokens who exercise voting rights through the authorization of governance token holders. Typically, investors and founders delegate voting rights to professional representatives, DAO service providers, or university blockchain clubs. It is worth noting that representatives are not necessarily bound by the interests of depositors, as their primary source of income comes from fees for their agency services rather than user interests.

The committee serves as the decision-making body within the project, responsible for making a series of specific decisions, including the introduction of new collateral, the formulation of marketing strategies, and the management of other core functions. In the process of allocating capital to generate yields, the committee acts as the direct decision-maker. Similar to the representatives, the committee aligns its interests with depositors through monetary compensation obtained from the project. The entry requirements for committee members are generally stricter than for representatives. Members of these committees are often "doxxed," which adds an extra layer of protection for those who value their public brand.

Trade-offs

A significant feature of the second type of stablecoin is achieving scalability through outsourcing. They act as a layer above yield-bearing stablecoins (including the first type), leveraging market forces to achieve large-scale yields. In this model, capital allocation changes with market conditions, and the governance structure reallocates capital based on performance in terms of yield and security. Therefore, the second type of stablecoin offers stronger guarantees of robustness compared to the first type.

However, like the first type of stablecoin, the second type also faces the issue of recourse not being guaranteed. If a third-party team incurs financial losses, end users will be unable to recover those losses. Since these organizations are decentralized, legal recourse is also unfeasible.

Another important factor to consider is the issue of corruption. As past DAO experiments have shown, bribing and corrupting DAO representatives, voters, and committee members can directly influence the security of capital allocation. Special advisory positions, regular payments, and token distributions are common ways to corrupt decision-makers. This directly impacts the security of the second type of stablecoin, as corrupted decision-makers may allocate capital to unsafe or malicious actors.

Type Three: Mechanism as Rule—When Stablecoins Learn to "Self-Sustain"

The third type of stablecoin represents a shift away from human subjective decision-making towards an automatically executed system of mutual rewards and penalties. In a sense, they resemble a protocol rather than a traditional hedge fund. Immutable rules set by smart contracts replace the process of capital allocation and recourse handling by human decision-makers.

The core motivation for adopting the third type of stablecoin is to enhance security and reduce latency. Users are protected at the smart contract level, allowing them to inspect the code to verify the recourse mechanism when strategies fail. Additionally, the response speed to strategy switches in the open market is greatly accelerated, enabling quick adjustments to market dynamics. This allows the third type of stablecoin to fully leverage market forces and rapidly deploy multiple parallel yield strategies.

Cap's Ambition: Creating a "Yield Perpetuum Mobile" for Stablecoins

Currently, there are no third type stablecoins in the market, and Cap is the first to pioneer this category.

Cap utilizes the lending market and Shared Security Model (SSM) to provide efficient capital allocation and reliable financial guarantees, thereby innovating the first third type stablecoin. The protocol supervises the ability of third-party operators to generate yields by publishing participation rules at the smart contract level. Interested readers are encouraged to read the introduction article for an overview of its mechanisms.

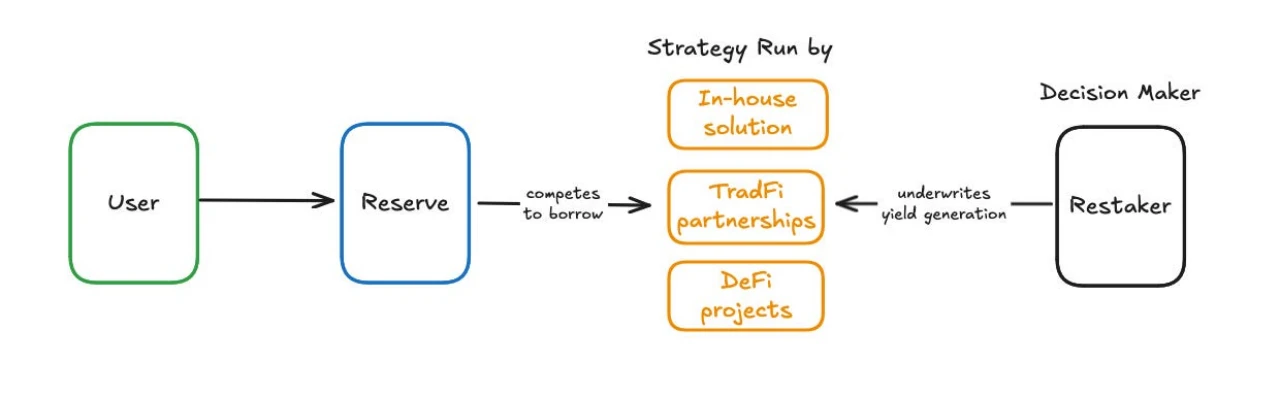

Cap is a three-party market that integrates operators, stakers, and end users.

Cap is a three-party market that integrates operators, stakers, and end users.

Operators are financial institutions responsible for generating yields. Their participation is regulated by smart contracts and market dynamics. Before operators borrow any assets, the protocol first checks for common over-collateralization or excessive guarantees in the crypto lending market. The difference here is that operators do not invest capital themselves, as doing so would reduce capital efficiency; instead, they accept the delegation of stakers, using locked crypto assets as collateral. Previously idle staked assets begin to earn yields through this new use. Operators need to persuade stakers to delegate their stakes to them.

The capital allocation to operators is economically adjusted through interest rates set by the lending market mechanism. It is not the team that decides how much funding each operator should receive; rather, operators choose whether to join the protocol based on whether they can provide yields at the current benchmark interest rate. The benchmark interest rate is also programmatically determined—it is the deposit rate of the main lending market plus Cap's usage premium. This usage premium is calculated as a percentage of the borrowed capital, indicating the competitiveness of capital supply under specific market conditions.

Stakers earn rewards by delegating to operators. The interest rate is determined by the agreement between stakers and operators. Similarly, end users also receive rewards for providing funds, with the interest rate determined by the benchmark yield. The amounts they receive are recorded and distributed on-chain, ensuring the transparency of the protocol.

If operators engage in malicious behavior or experience a black swan event that leads to losses in borrowed amounts, stakers will suffer penalties. The penalties will remove the staker's held cryptocurrency as collateral to compensate end users. The penalized funds will be redistributed to end users, ensuring that recourse is always available and can be verified through code.

Incentive Mechanism Adjustments

Since third-party operators must obtain delegation from stakers to borrow, the decision-makers in Cap are effectively the stakers. Stakers have the final say on which third parties can enter the protocol and generate yields.

Stakers are incentivized through the delegation premium provided by operators. Staked assets, being locked crypto assets, have low opportunity costs and low capital premiums. In other words, these assets cannot be used to generate significant returns. Therefore, stakers have the motivation to delegate this idle value to operators for use. While holding decision-making power, stakers are also directly exposed to the outcomes of those decisions, encouraging them to prioritize security.

It is noteworthy that Cap's ultimate goal is to become a fully permissionless, minimally governed protocol, where operators and stakers can participate freely. However, given the novelty of the design, in the early stages of the protocol, stakers and operators will be certified institutions and will be whitelisted. This provides a security mechanism for stakers, as they have a way to reach agreements with each other and execute legal recourse.

Trade-offs

The key advantage of this model lies in its security. Since decision-makers bear the full risk of their decisions, retail holders do not need to worry about the process of generating yields. All rules are enforced by smart contracts, eliminating the need for human arbitration. This provides retail investors with stronger regulatory protection than traditional finance.

Similar to the second type of stablecoin, the latency in identifying and adopting new strategies is reduced. The system incurs no conversion costs when reallocating capital. Unlike the second type of stablecoin, capital allocation does not require lengthy DAO and committee deliberations. Each staker has the right to allocate capital to operators individually at the same time.

However, compared to the second type of stablecoin, the third type has a higher complexity. This complexity may introduce risks associated with smart contracts, as the entire system relies on code to regulate the execution process.

Conclusion: A Paradigm Shift is Inevitable

Currently, interest yields are still far from reaching levels sufficient to unlock the potential of DeFi. As the stablecoin market continues to grow, there will be an increasing number of interest-yielding stablecoins supported by strategies. However, unless a paradigm shift occurs in the fundamental design of these stablecoins, the same risks and fatigue will be faced again, preventing scalability. Therefore, there is an urgent need to develop a more efficient, scalable, and secure system that transcends the limitations of traditional human decision-making and promotes the widespread application of stablecoins.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。