The "Tariff Liberation Day" that Trump has mentioned for several weeks is approaching, and global markets are experiencing a new round of volatility. After encountering "Black Friday" last week, U.S. stocks fell again on Monday, with the Nasdaq down 8.21% in March. The cryptocurrency market was also affected, with Bitcoin recording an 18% drop in February and ending March with a further decline of 3.5%. Ethereum disappointed many, with a cumulative drop of nearly half in the first quarter, leading to very negative market sentiment.

Deteriorating Macroeconomics, Continued Decline in Consumer Confidence

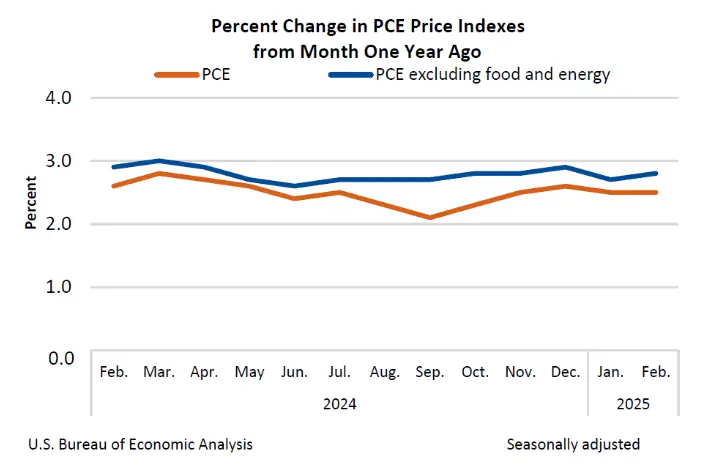

The PCE price index, the Federal Reserve's preferred inflation indicator released last week, shows that inflation remains stubbornly high, and consumer spending is becoming more cautious. The month-on-month and year-on-year increases in core PCE for February were both higher than expected, with core service costs rebounding significantly, pushing up "super core inflation."

As key inflation indicators rise, the savings rate has also noticeably increased. Consumer spending in February fell short of expectations again, with a clear trend indicating that personal consumer spending on goods is beginning to outpace spending on services, suggesting that the consumption willingness of high-income groups, which has supported U.S. GDP growth over the past two years, is also declining, leading to a more cautious outlook for the future.

In line with the consumption data, the latest consumer confidence index released by the University of Michigan fell to 57, with consumers' inflation expectations for the next year rising to 5%, both at their worst levels in over two years.

From the Federal Reserve, several voting members have spoken out, emphasizing that maintaining patience is a consensus while also acknowledging that the inflation path has deviated from expectations and the uncertainty surrounding tariff impacts has made the economic outlook for 2025 more ambiguous.

With consumer and business sentiment weak, the economy is entering a fragile phase, and the impact of policy risks is greater than in recent years. Goldman Sachs raised the probability of a U.S. recession in its report last week from 20% to 35%, with GDP growth slowing to 1.0%.

Trump's Tariffs as a Market Turning Point, This Week May See Peak Volatility

The "reciprocal tariffs" that Trump plans to implement on Wednesday are the direct trigger for recent market turmoil. Goldman Sachs expects that tariffs will average 15% on all trading partners, an increase of 5 percentage points from previous expectations, which could raise import costs and trigger global retaliatory actions.

In its latest report, Citigroup summarized three main scenarios and their corresponding market impacts: first, only announcing reciprocal tariffs, which would have a limited market reaction; second, reciprocal tariffs plus a value-added tax (VAT), which could immediately raise the dollar index by 50-100 basis points and lead to a decline in global stock markets; third, including industry-specific tariffs in addition to reciprocal tariffs and VAT, which could result in a more severe market reaction.

As these policies have not yet been announced, and given Trump's unpredictable and inconsistent style, the market is more focused on positioning based on expectations, which often change due to various news. This week may become a peak of volatility. Furthermore, once policies are finalized or their impacts become apparent, the market may readjust its positioning, leading to more fluctuations.

Risk Aversion as the Current Market Theme

Whenever significant events approach, investors tend to avoid risks. U.S. stocks have been sold off and continue to show weakness, with last week's strong rebound cut short, and the cryptocurrency market is experiencing lackluster trading, with funds accelerating into safe-haven assets.

Since March 14, the net inflow of Bitcoin spot ETFs has exceeded net outflows for 10 consecutive days. However, starting from March 21, net inflows have not exceeded $100 million again, and on March 28, the streak of 10 consecutive net inflows ended, with institutional funds experiencing continuous net outflows.

Meanwhile, gold has performed exceptionally well. Spot gold rose 1.25% on Monday, reaching a historic high of $3,145, having set new records 19 times this year. In March, it accumulated a rise of 9.33%, with a quarterly increase of 18.48%, marking the strongest quarterly performance since 1986 and becoming the most eye-catching asset globally.

Trump will announce reciprocal tariffs at 3 a.m. on April 3, and the current market is on high alert, with risk aversion dominating a very fragile market. If the tariff measures are severe and trigger global trade frictions, risk assets may further decline. 4E Exchange, as the official partner of the Argentine national team, offers a USDT stablecoin financial product with an annualized return of 8%, providing investors with a potential safe-haven option. Additionally, 4E supports bulk gold trading, allowing investors to seize potential growth opportunities in safe-haven assets amid market turmoil.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。