- The misalignment between venture capital firms and founders is driving founders to turn to other financing channels.

Author: 0xLouisT

Translation: Deep Tide TechFlow

Altcoins are continuously bleeding—why? Is it due to high FDV or the listing strategies of CEXs? Should Binance and Coinbase directly invest their funds into new altcoins using TWAP (time-weighted average price)? The real culprit is not new—it all traces back to the crypto venture capital bubble of 2021.

In this article, I will analyze how we got to this point. In the following articles, I will explore the impact of this phenomenon on projects and liquid markets, potential future trends, and provide some advice for entrepreneurs in the current environment.

The ICO Craze (2017-2018)

The crypto industry is essentially a highly liquid sector—projects can issue tokens at any time, and these tokens can represent anything, regardless of their stage. Before 2017, most trading activity occurred in public markets, where anyone could directly purchase tokens through centralized exchanges.

Then came the ICO (Initial Coin Offering) bubble: a time of frenzied speculation quickly exploited by scammers. Its end was like all bubbles: lawsuits, fraud, and regulatory crackdowns. The U.S. Securities and Exchange Commission (SEC) intervened, making ICOs nearly illegal. To avoid the U.S. judicial system, founders had to seek other ways to raise funds.

The Venture Capital Craze (2021-2022)

As retail investors were forced out, founders turned to institutional investors. From 2018 to 2020, the crypto venture capital space gradually grew—some firms were pure venture capitalists, while others were hedge funds allocating a small portion of their assets under management (AUM) to venture bets. At that time, investing in altcoins was a contrarian move—many believed these tokens would ultimately go to zero.

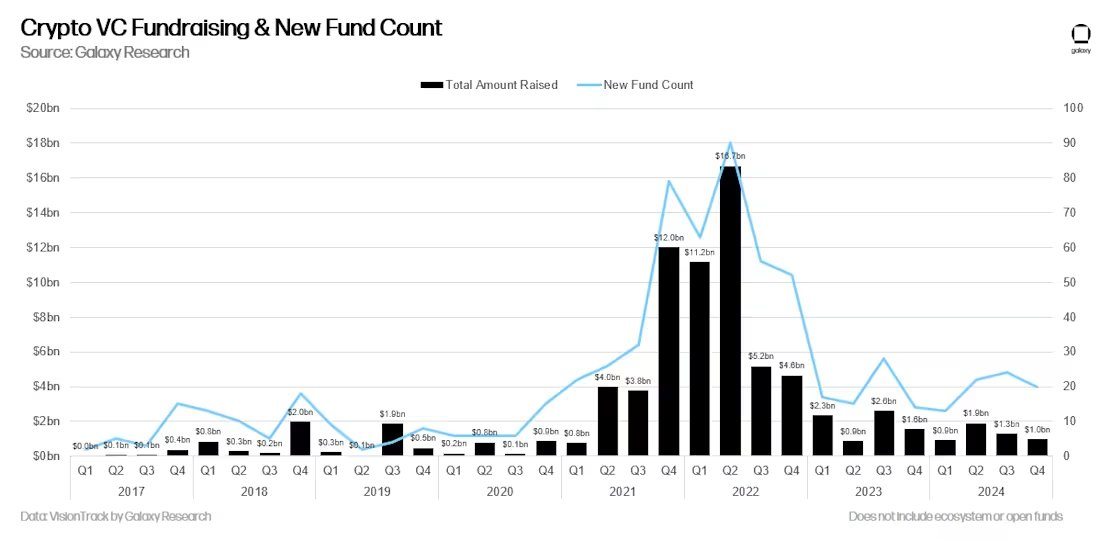

Then came 2021. The bull market caused venture capital portfolios (at least on paper) to soar rapidly. By April, many funds had returns of 20x or even 100x. Crypto venture capital suddenly looked like a "money printing machine." Limited partners (LPs) flocked in, eager to ride the next wave. Venture capital firms rushed to raise new funds, with sizes 10 times or even 100 times larger than before, convinced they could replicate these astonishing returns.

Source: Galaxy Research

Additionally, there are some psychological reasons explaining why venture capital is so attractive to LPs, which I analyzed in detail in a previous article: The Real Reason Why There Is More Venture Capital Than Liquid Funds in the Crypto Space

Hangover Period (2022-2024): The Dilemma and Transformation of Crypto Venture Capital

Then came 2022: the collapse of Luna, the bankruptcy of 3AC (Three Arrows Capital), and the collapse of FTX—billions of dollars in paper gains vanished overnight.

Contrary to popular belief, most venture capitalists did not cash out at the market peak. They, like others, experienced the downward process of the market crash. Now, they face two major challenges:

Disappointed Limited Partners (LPs): LPs who once cheered for 100x returns are now demanding quick exits, pressuring funds to reduce risk and lock in profits prematurely.

Excess Capital: There is a large amount of unused venture capital (dry powder) in the market, but quality projects are in short supply. Many funds choose to invest in economically unreasonable projects to meet investment thresholds and pave the way for the next round of financing, rather than returning capital to LPs.

Today, most crypto venture capitalists find themselves in a dilemma: unable to raise new funds, holding a bunch of low-quality projects destined to follow the "high FDV to zero" script. Under pressure from LPs, these venture capitalists have shifted from long-term vision supporters to short-term exit chasers. They frequently sell off large tokens supported by venture capital (such as alternative L1, L2, and infrastructure tokens), whose high valuations they themselves artificially inflated.

In other words, the incentive mechanisms and timeframes of crypto venture capital have changed significantly:

2020: Venture capitalists were contrarians, facing capital shortages, focusing on long-term development.

2024: Venture capitalists have become crowded, over-capitalized, and more short-sighted.

I believe that the performance of venture capital funds from 2021 to 2023 will largely fall below expectations. Venture capital returns follow a power-law distribution, where a few winners compensate for the majority of losers. However, due to forced early sell-offs, this model will be disrupted, leading to overall weaker performance.

If you want to learn more about average data on venture capital returns, I previously wrote a related article.

It is not hard to understand why more and more founders and communities are skeptical of venture capital. The incentive mechanisms and timelines of venture capitalists are misaligned with the goals of founders, and this misalignment is driving a shift towards the following trends:

Community-Driven Financing: Projects are more inclined to raise funds through community power rather than relying on venture capital.

Long-Term Support from Liquid Funds: Compared to venture capital, liquid funds are gradually becoming the mainstay for long-term support of tokens.

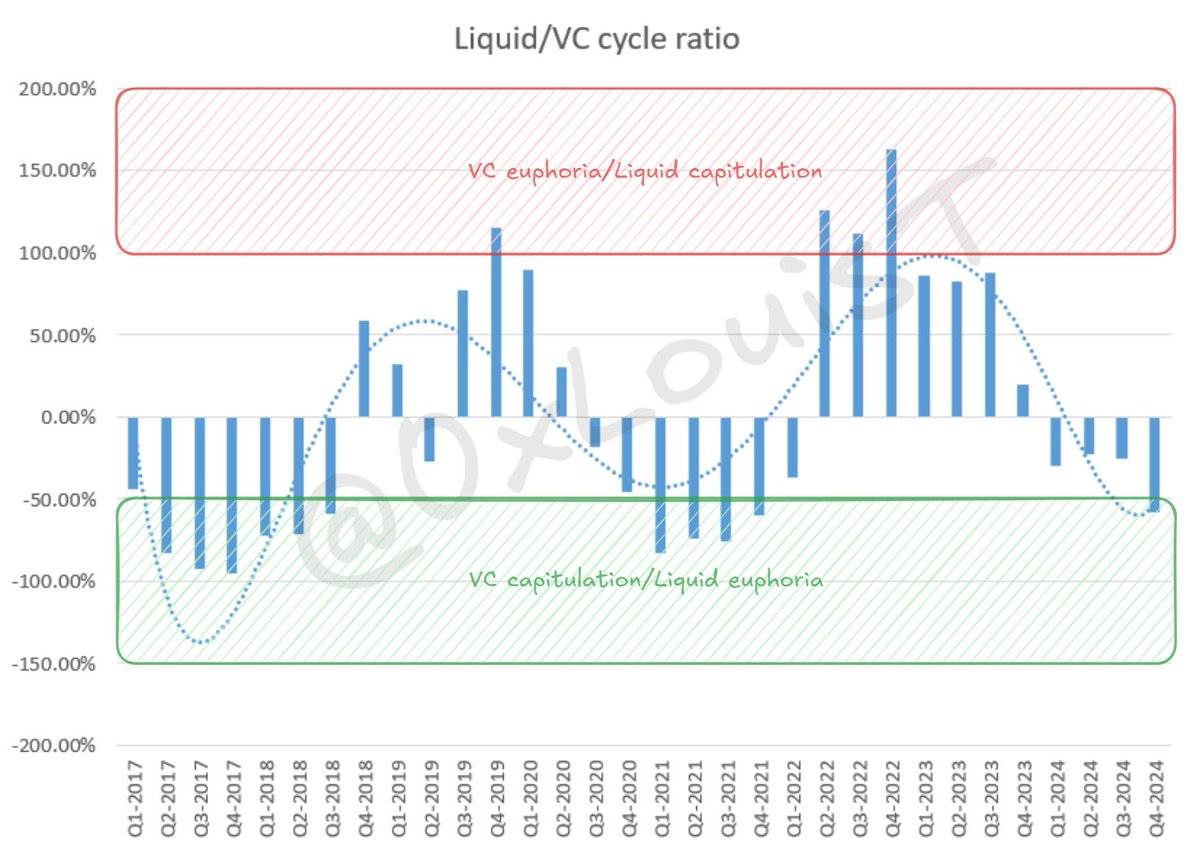

Assessing the Liquidity/Venture Capital Cycle

Tracking the capital flow between venture capital funds and liquid markets is crucial. I use an indicator to assess the state of the venture capital market. While it is not perfect, it is very informative.

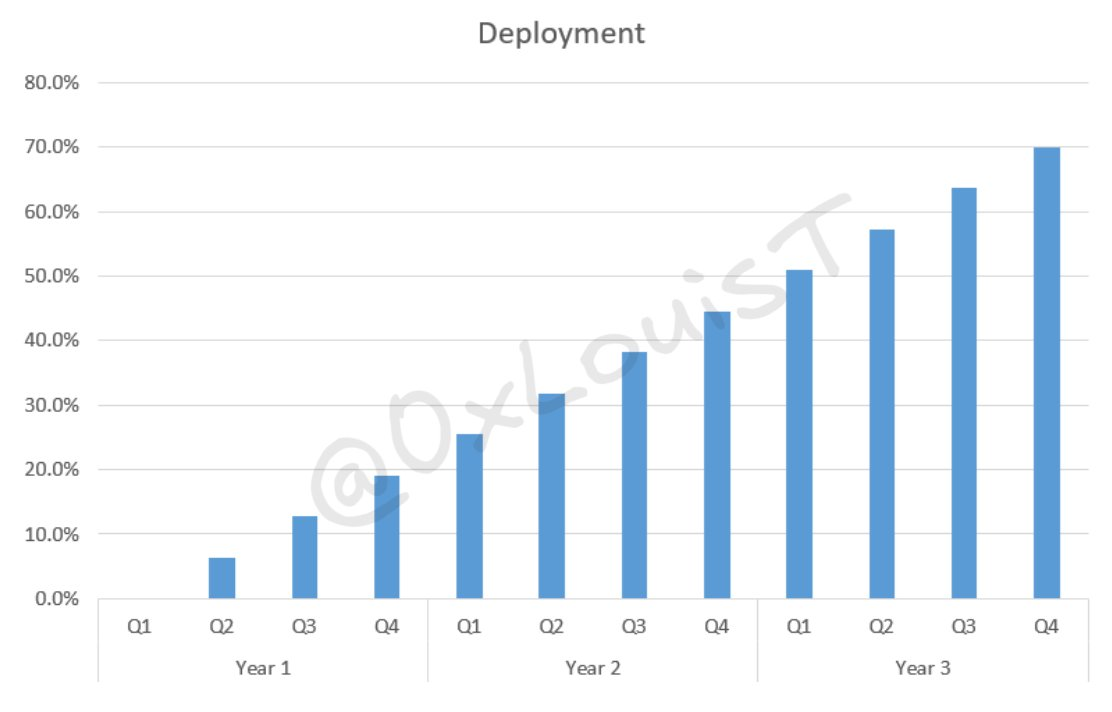

I assume that venture capitalists will linearly deploy 70% of their funds within three years—this seems to be the trend for most venture capitalists.

VC 3y Linear Deployment Visualization

Based on fundraising data provided by @glxyresearch, I applied a weighted sum model, combining the deployment rates over 16 quarters to estimate the remaining unused funds (dry powder) in the system. In the fourth quarter of 2022, approximately $48 billion in venture capital remained undeployed. However, with the new round of fundraising stagnating, this number has at least halved and continues to decline.

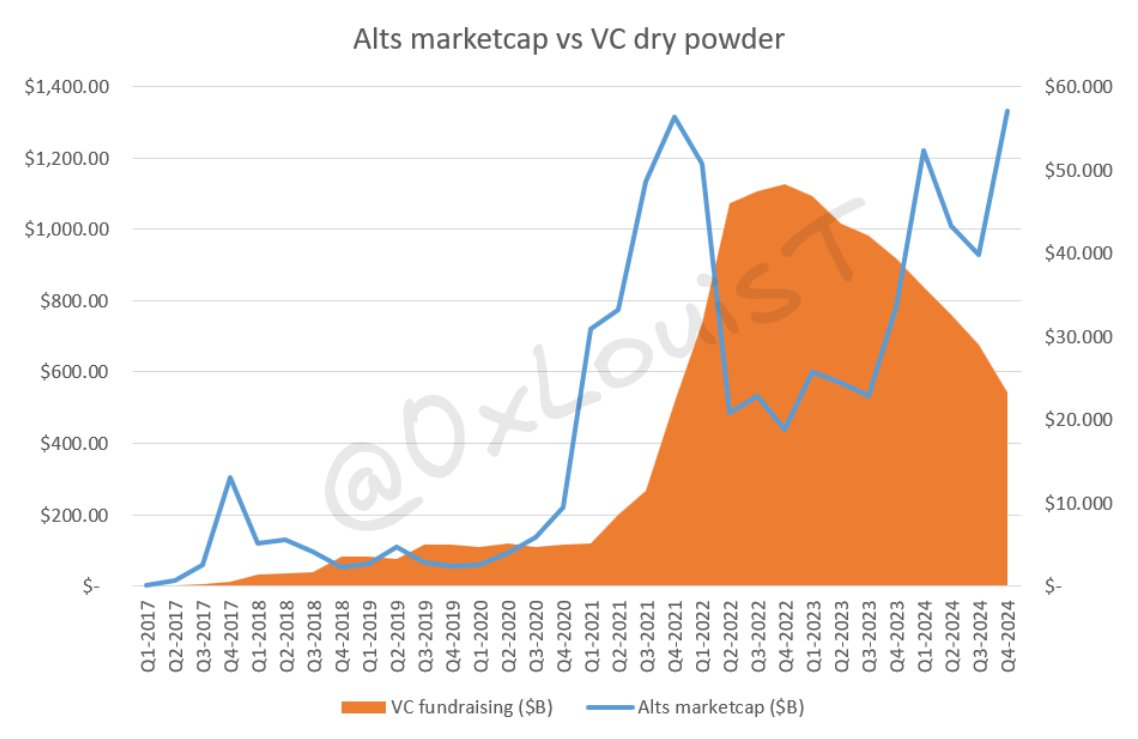

VC Undeployed Funds Visualization Chart

Next, I will compare the remaining venture capital each quarter with TOTAL2 (the total market capitalization of the crypto market excluding Bitcoin). Since venture capital typically invests in altcoins, TOTAL2 is the best proxy indicator. If venture capital funds are excessive relative to TOTAL2, the market will be unable to absorb future token generation events (TGE). Normalizing this data can reveal the cyclical characteristics of the liquidity/venture capital ratio.

Crypto Venture Capital and Liquid Markets: Cyclical Patterns and Future Outlook

Typically, during the "VC euphoria" phase, the risk-adjusted returns of liquid markets tend to outperform venture capital. The "VC capitulation" phase is more complex—it may indicate that venture capital is giving up, or it may suggest that the liquid market is overheating.

Like all markets, crypto venture capital and liquid markets follow cyclical patterns. The excess capital accumulated in 2021/2022 is rapidly being consumed, making it more difficult for founders to raise funds. Meanwhile, venture capital firms, facing capital exhaustion, have become more selective in trading and terms.

I will stop here, and the next article will delve into the impact of this phenomenon on liquid markets.

Summary

Recent venture capital fund performance has been lackluster, and venture capital firms are turning to short-term sell-offs to return capital to LPs. Many well-known crypto venture capital firms may not survive in the coming years.

The misalignment between venture capital firms and founders is driving founders to turn to other financing channels.

The oversupply of venture capital is leading to unreasonable resource allocation, which I will analyze in detail in subsequent articles.

To be continued…

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。