Base will play an increasingly important role in guiding new companies and users, and in the long term, Solana will become the main platform for stablecoin payments.

Author: Squads

Compiled by: Deep Tide TechFlow

At the inauguration of President Donald Trump, the market capitalization of stablecoins reached a record $210 billion—this figure is just a glimpse of how stablecoins are reshaping global capital flows.

Accompanying this growth, competition among businesses to integrate stablecoins and their payment infrastructure into products and services is intensifying. In October 2024, Stripe acquired the stablecoin payment platform Bridge for approximately $1.1 billion, marking the largest acquisition in the crypto space to date. In the same year, stablecoin payment companies secured over $309 million in funding, reflecting growing market confidence in this sector.

Blockchain ecosystems are competing to position themselves as the ideal foundation for payment use cases, each with its unique trade-offs affecting implementation costs, user experience, and market coverage. This report explores the key factors that enterprises and developers should consider when choosing a blockchain platform to build stablecoin payment solutions, highlighting Solana and Base as the two most suitable blockchains for payments today.

On-chain Payment Landscape

As noted in our previous report, stablecoins are evolving from a crypto-native tool to mainstream financial infrastructure, fundamentally reshaping the flow of capital:

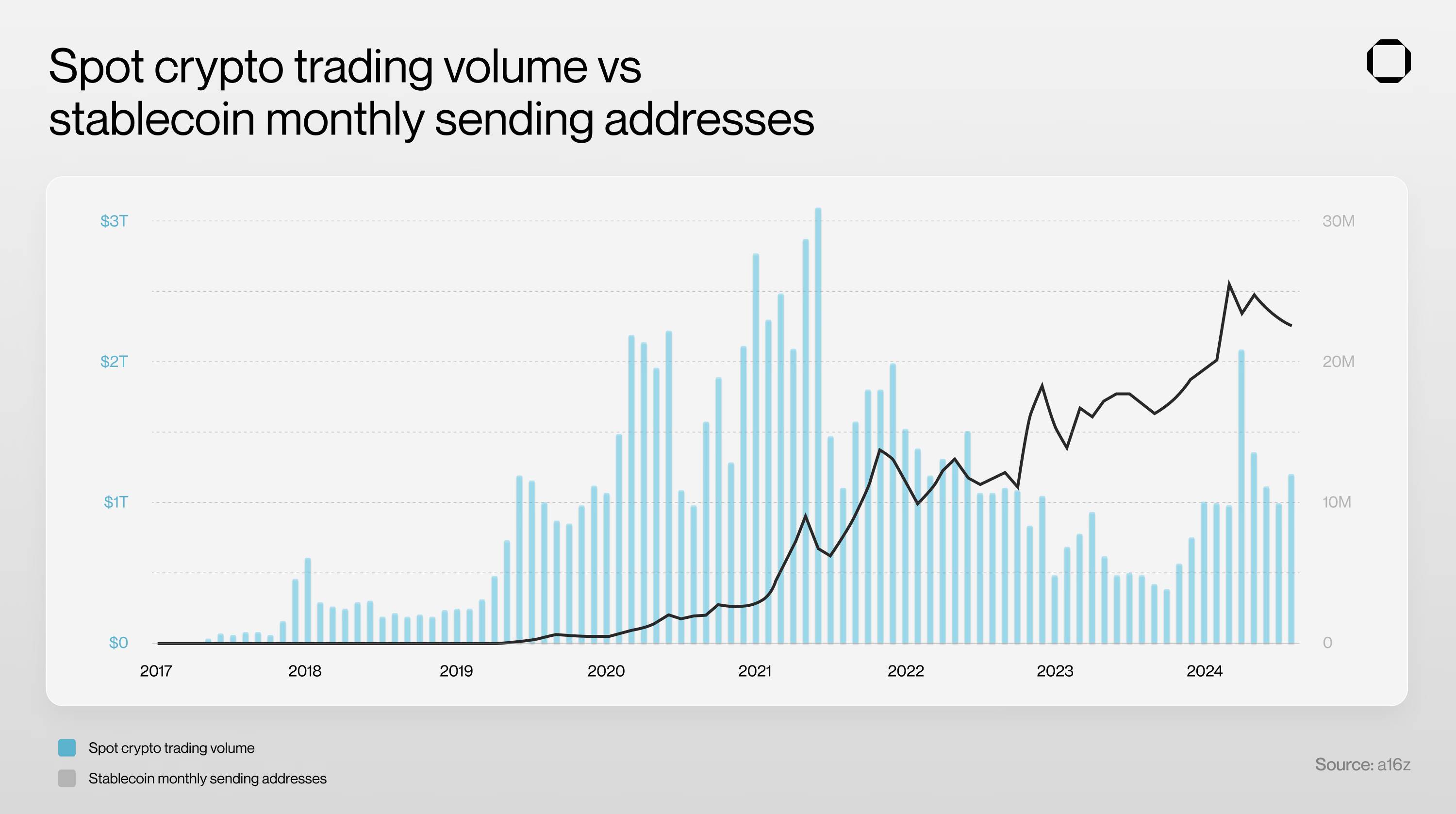

The annual transaction volume of stablecoins surged from $5.7 trillion in 2023 to $8.3 trillion by the end of 2024.

Active stablecoin users are spread across major blockchains, totaling 29 million addresses.

**Stablecoins now drive 32% of daily crypto activity, second only to *Decentralized Finance* (DeFi).**

Crypto-native companies, traditional enterprises, and startups are embracing stablecoins and their payment rails, with applications extending across several major industries, such as e-commerce (over $25 trillion), B2B payments (over $1.3 trillion), and cross-border remittances (over $700 billion).

For instance, SpaceX aggregates part of Starlink's global revenue in stablecoins to avoid foreign exchange risks. In late September 2024, PayPal completed its first commercial transaction with Ernst & Young using its stablecoin PYUSD through SAP's digital currency platform. Additionally, major U.S. retailers like Overstock, Chipotle, Whole Foods, and GameStop now accept stablecoin payments.

The surge in enterprise adoption highlights a key point: choosing the right blockchain infrastructure is no longer a trivial choice but a strategic necessity that will determine a company's competitiveness in the rapidly evolving digital payment ecosystem.

Evaluating Blockchain's Stablecoin Payment Capabilities

Successfully integrating stablecoins and their payment rails into products or services requires the blockchain to meet the following four key requirements:

High-performance architecture

Low/predictable fees

Market demand

Regulatory clarity

We will analyze how Solana and Base, two major public chains, meet these requirements.

You may wonder why we chose these two blockchains. After all, Ethereum leads by a wide margin in total value locked (TVL) for stablecoins, Tron is one of the most popular blockchains for stablecoin payments, and Celo has driven significant stablecoin adoption through Minipay (Opera's mobile wallet, which has attracted over a million users in Africa).

Despite the advantages of these blockchains, they were ultimately excluded from our analysis for the following reasons:

Ethereum: While suitable for high-value transfers, its high gas fees and slow transaction speeds limit its application in stablecoin payments. This has led to a bifurcated ecosystem: Ethereum retains high-balance holders while delegating payment applications and mainstream use cases to sidechains or application chains.

Tron: This blockchain is very active in the stablecoin payment space, particularly serving users who cannot access traditional financial rails. However, as noted in our previous report, its prevalence in sanctioned regions, controversial associations with Justin Sun, and reports of use by terrorist organizations have heightened regulatory scrutiny. With Circle ceasing support for native USDC in February 2024, Tron's ability to attract major stablecoin issuers has gradually diminished, making it less likely to become a foundation for new stablecoins and payment applications.

Celo: Although it has shown good user adoption through Minipay in Africa, this blockchain faces significant hurdles: low TVL, limited institutional adoption, a short track record, and an evolving technical roadmap after its transition to L2 in 2024. Celo is a blockchain to watch, but it is not yet ready to handle mainstream stablecoin payment applications.

Of course, there are other blockchains that perform well in stablecoin payment applications, such as BNB, Arbitrum, Avalanche, and TON. While these blockchains have great potential, they have not met the core standards for mainstream payment adoption that Solana and Base have achieved.

In addition to public chains, application chains like SphereNet and Payy are also emerging in the stablecoin payment space. However, no application chain has yet proven itself as a dominant platform for stablecoins and payments, facing significant challenges such as limited developer and user infrastructure, long-term neutrality concerns, and difficulties in attracting institutional adoption and stablecoin issuers.

Launching an application chain is akin to opening a Shopify store and attracting traffic, but in the financial realm, liquidity attracts more liquidity, making the challenges much greater.

Based on the above analysis, let’s see how Solana and Base currently meet the conditions for stablecoin payments.

High-Performance Architecture

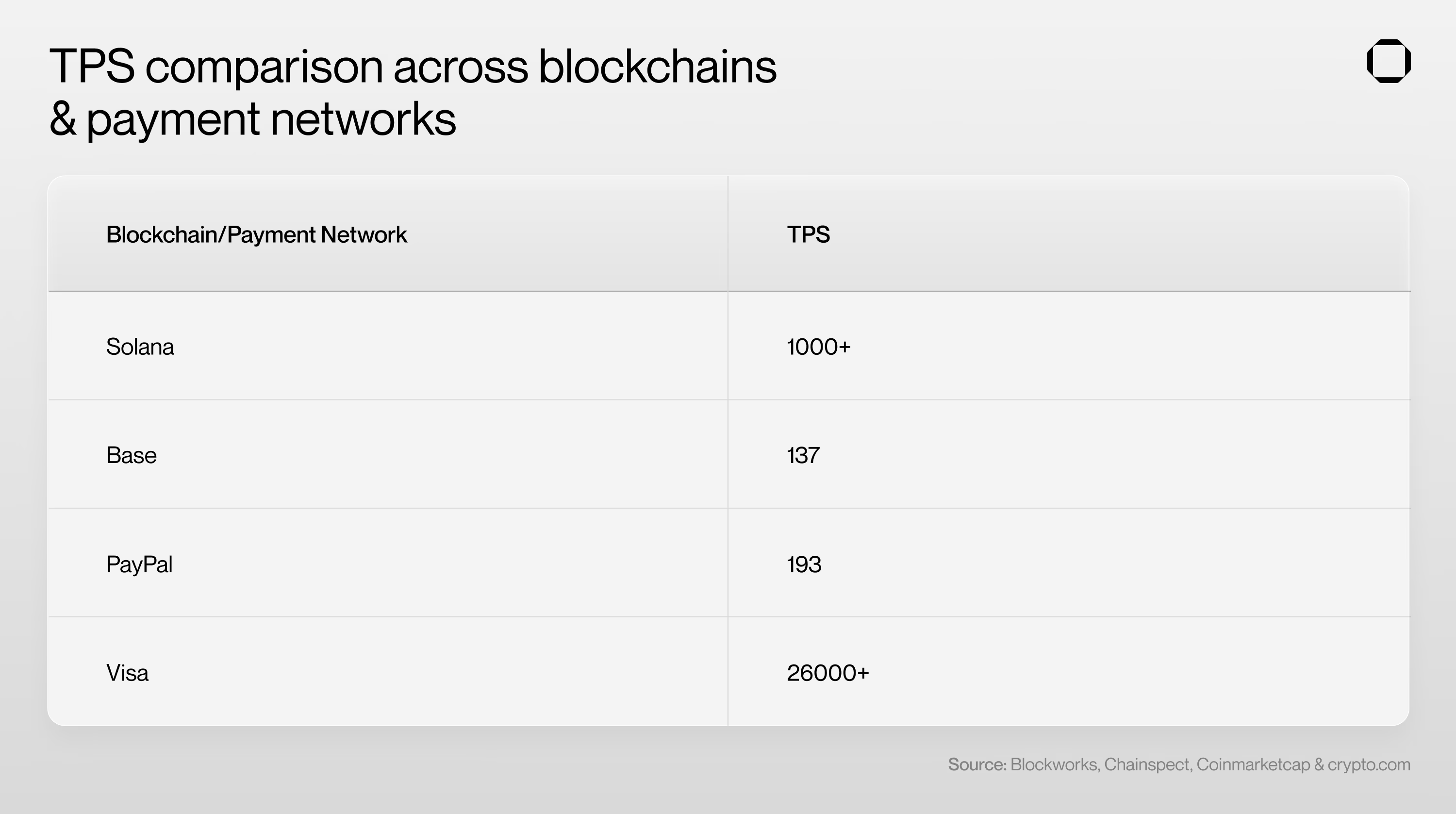

Stablecoin payment use cases require fast transactions, typically measured in transactions per second (TPS) and blockchain finality. Solana and Base achieve high TPS and rapid finality functionally, making them ideal choices for stablecoin payments.

TPS reflects a network's capacity and efficiency; higher TPS means the ability to handle a larger volume of real-time activity.

Finality refers to the time required for a transaction to be irreversibly confirmed. Fast and secure finality in payment systems is crucial for ensuring that transactions are irreversible and preventing double-spending. If a blockchain cannot prevent double-spending, its significance as a ledger is nullified. Finality also assures users that their transactions have been settled and can be used for financial agreements.

Solana and Base achieve finality through two different mechanisms:

Solana achieves two levels of commitment (finality states) for transactions: confirmation and finalization. Confirmed transactions achieve supermajority (66% of stake weight) consensus within 800 milliseconds, while finalized transactions require an additional 31 confirmation blocks (approximately 13 seconds) to ensure maximum security. In practice, no optimistic confirmation blocks have been rolled back in the four years of Solana's existence.

Base, on the other hand, takes a different approach through a sequencer operated by Coinbase, providing near-instant pre-confirmations with a block time of 2 seconds. These pre-confirmations rely on Coinbase's reputation rather than economic incentives, with true finality requiring about 15 minutes as transactions settle on Ethereum. The centralized sequencer design enables rapid iteration, quick confirmations, and reduces toxic MEV, but also introduces risks of censorship and single points of failure.

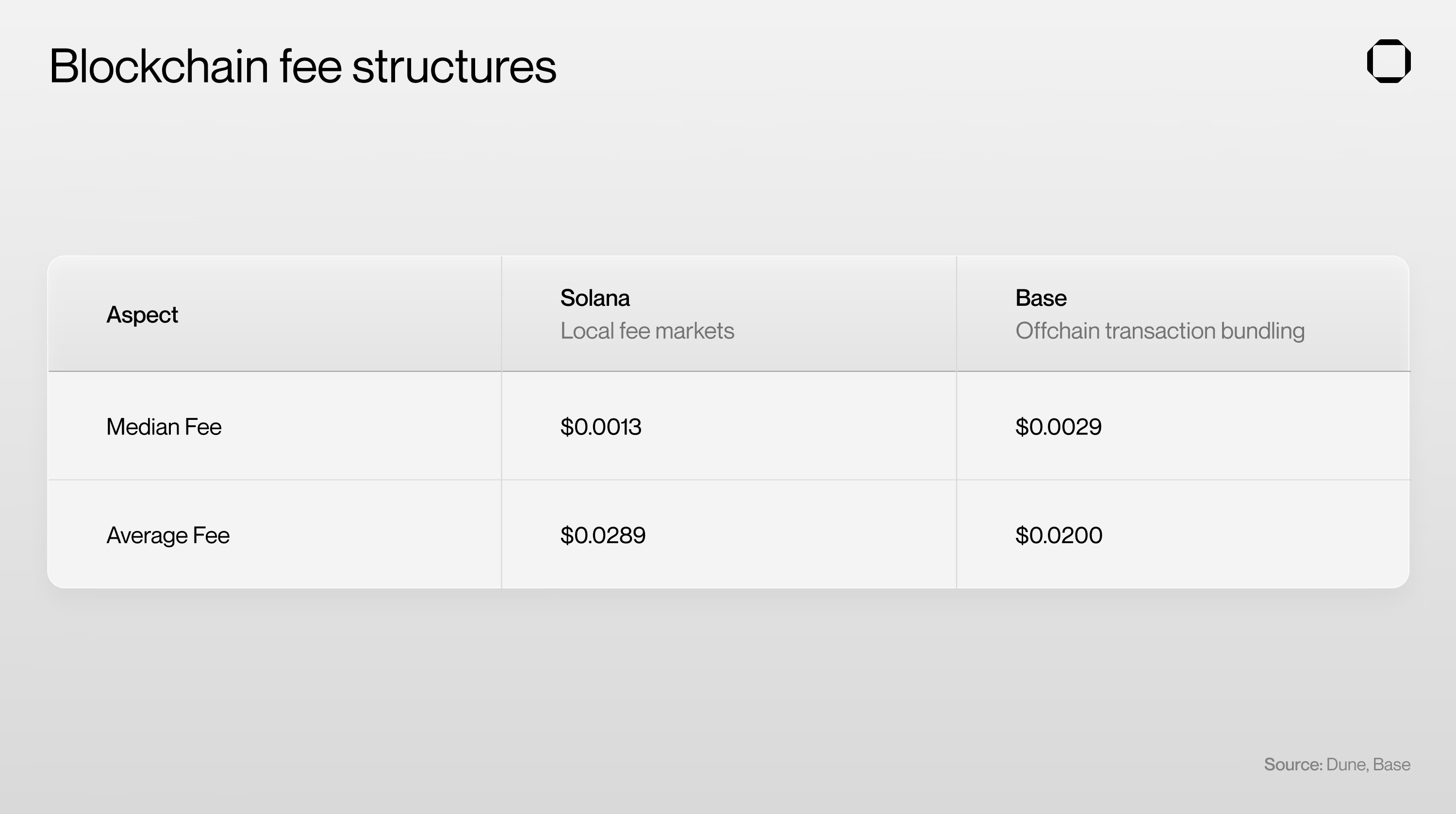

Low/Predictable Fees

For any payment use case, low and predictable fees are essential so that businesses and users can estimate transaction costs without significant volatility.

A key component of Solana's payment capability is that, unlike Ethereum L1/L2, it segments database hotspots through a local fee market. The local fee market and Jito's transaction segmentation engine make Solana's transactions both cheap and predictable for ordinary users, which is a critical requirement for stablecoin payment applications. Solana's native parallelization further enhances throughput by executing multiple transactions simultaneously rather than sequentially.

Additionally, don’t forget Firedancer. Firedancer is an independent Solana validator client developed by Jump Crypto, achieving 1 million TPS in a test environment, and is expected to roll out in phases this year.

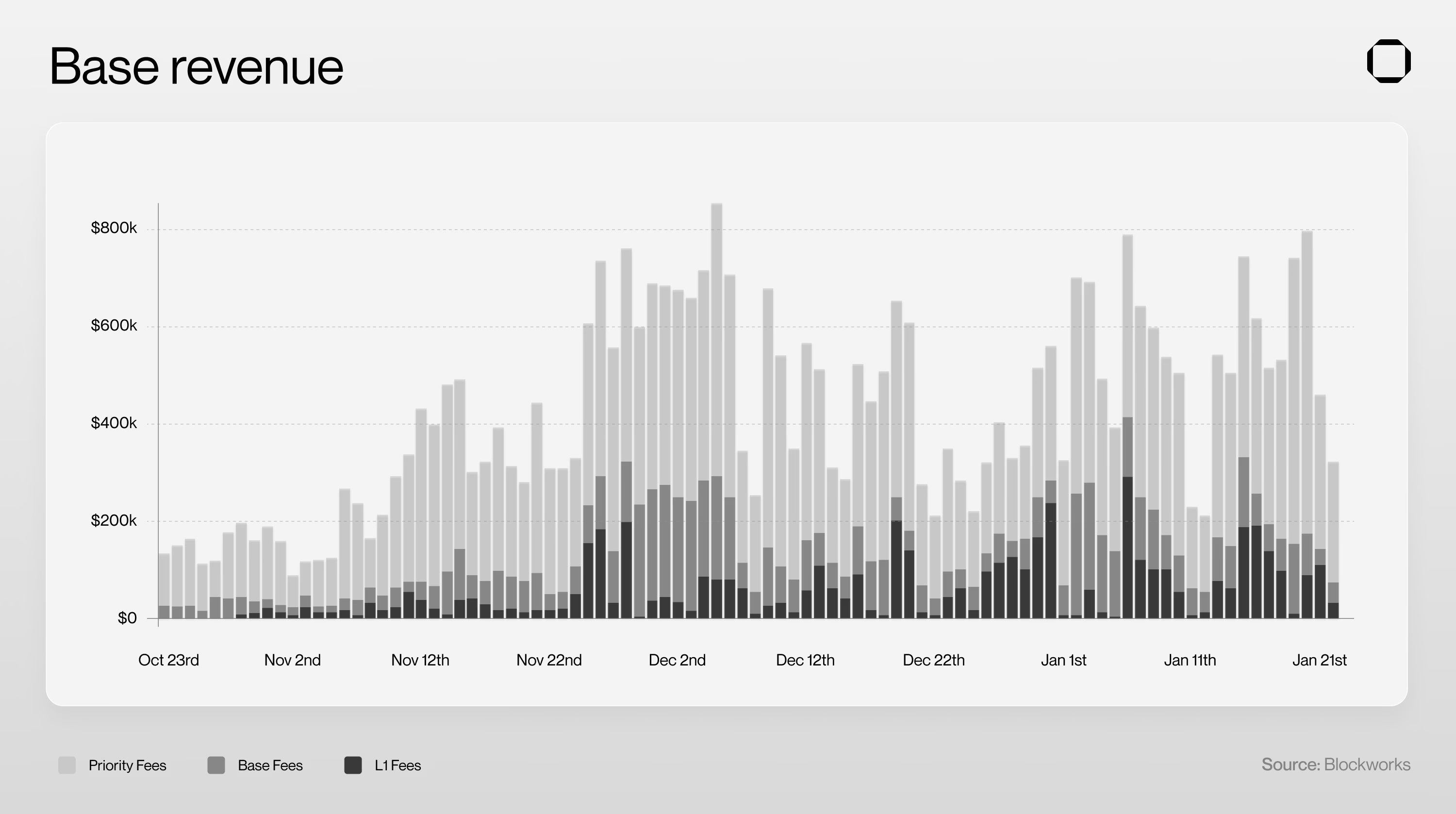

Meanwhile, Base operates on a single-threaded EVM (Ethereum Virtual Machine), enhancing performance through software optimizations and hardware scaling. Its performance is steadily improving, with a commitment to increase Base's block capacity by 1 Mgas/s weekly by 2025.

Furthermore, Base's sequencer transactions are batched off-chain before finalizing on Ethereum. This approach decouples user fees from Ethereum's congestion, allowing Base to consume over 40% of Ethereum's blob space while only allocating 8% of fee revenue for settlement. This design enables Base to offer users more stable and predictable transaction fees while alleviating the burden on Ethereum's main chain.

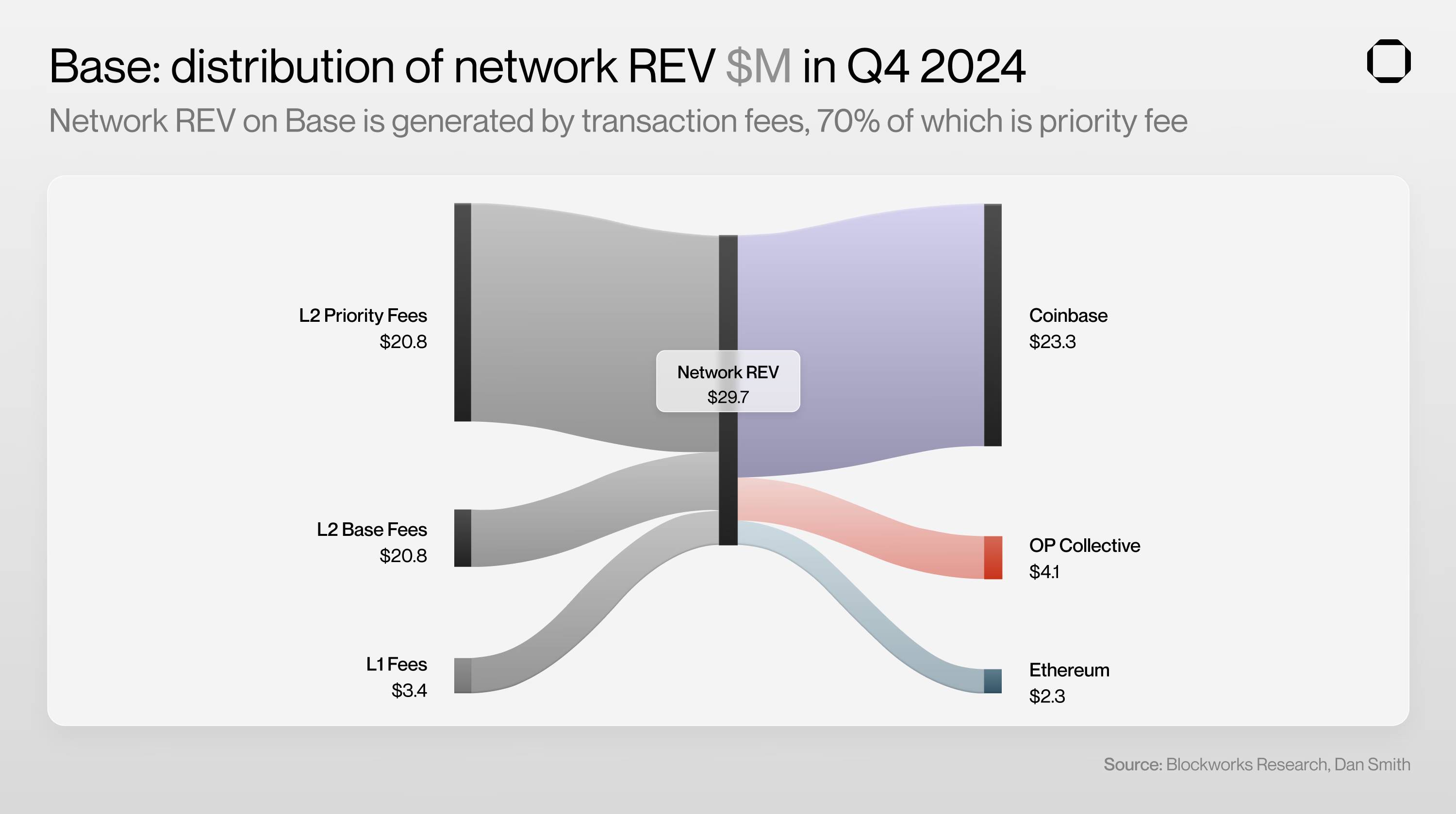

Another key difference between Solana and Base lies in the beneficiaries of fee revenue. On Solana, fees are paid to a decentralized set of validators, while on Base, fees flow directly to Coinbase. In 2024 alone, Coinbase generated at least $56 million in revenue from fees charged through its sequencer.

Solana has fostered a diverse ecosystem of companies dedicated to scaling solutions, from optimizing validator clients to ZK state compression. Base lacks this diversity; instead, it leverages Optimism's OP stack and relies on Coinbase to define its technical roadmap.

This reduces the innovation potential of Base, but due to significantly lower coordination costs, it can adopt breakthrough technologies more quickly. Base can implement future upgrades and EVM research (e.g., Monad's experiments on parallelization and EVM database optimization) at a faster pace than its decentralized counterparts like Solana.

Market Demand

On-chain payments are only viable when there is sufficient demand to use stablecoins as "currency." With on-chain activity on Solana and Base reaching historical highs, both blockchains are well-positioned in the stablecoin payment space.

The "Real Economic Value" (REV) of a blockchain is the best indicator of user demand. Daily or monthly active users (DAUs/MAUs) are unreliable metrics for assessing blockchain usage, as they are easily manipulated. In contrast, exaggerating REV is significantly more difficult and economically unfeasible. High REV (rather than DAUs/MAUs) signals to businesses and developers that the blockchain is a robust commercial platform, triggering a powerful flywheel effect.

Solana

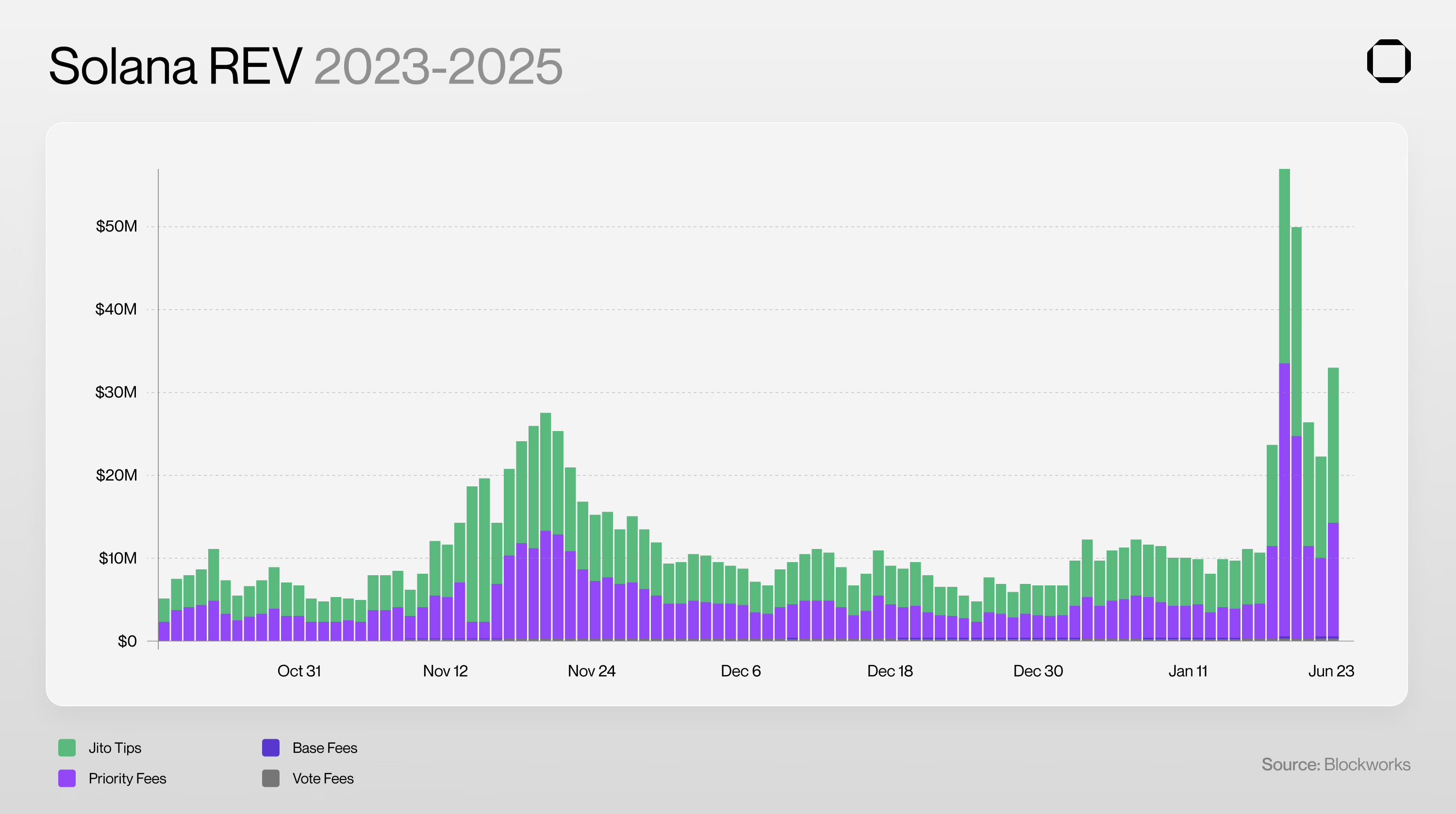

As of January 23, 2025, Solana leads all blockchains in REV, generating $751 million in revenue just in the fourth quarter of 2024.

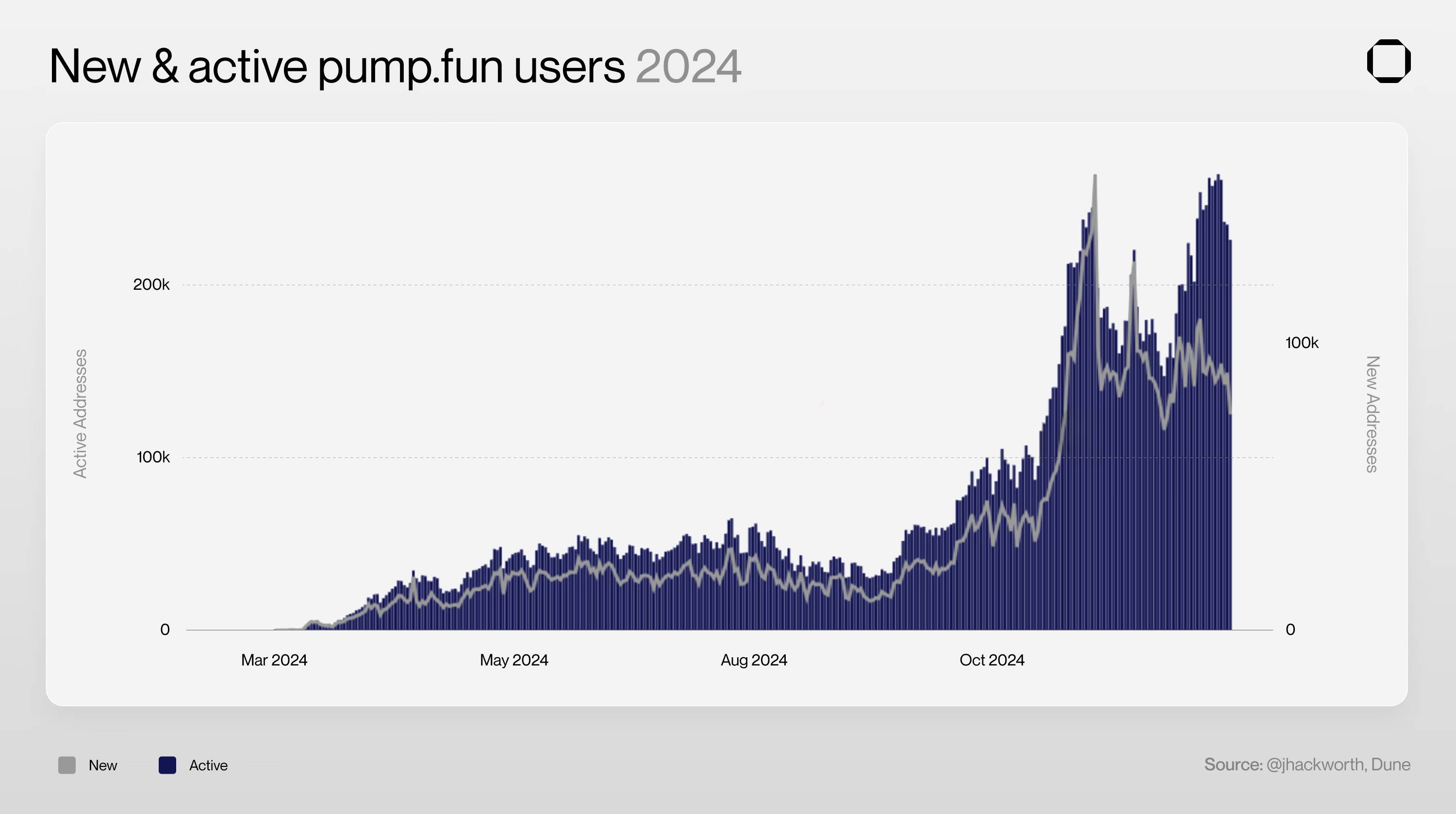

Solana's dominance is attributed to its relatively simple onboarding process, low fees, and a strong DeFi application ecosystem, including Jito, Jupiter, Kamino, Drift, Moonshot, and pump.fun. Notably, pump.fun has attracted significant trading activity and new users since its launch in March 2024, generating over $450 million in fees. This clearly indicates that Solana is a platform capable of supporting viable business models.

Speaking of onboarding, on January 18, 2025, President Trump launched his official meme coin $TRUMP on Solana, generating over $7 billion in on-chain trading volume within 24 hours. By January 19, 2025, Solana's daily REV exceeded $56 million, while Moonshot—an app allowing users to purchase cryptocurrencies using Apple Pay—became the top-ranked financial app in the U.S. App Store.

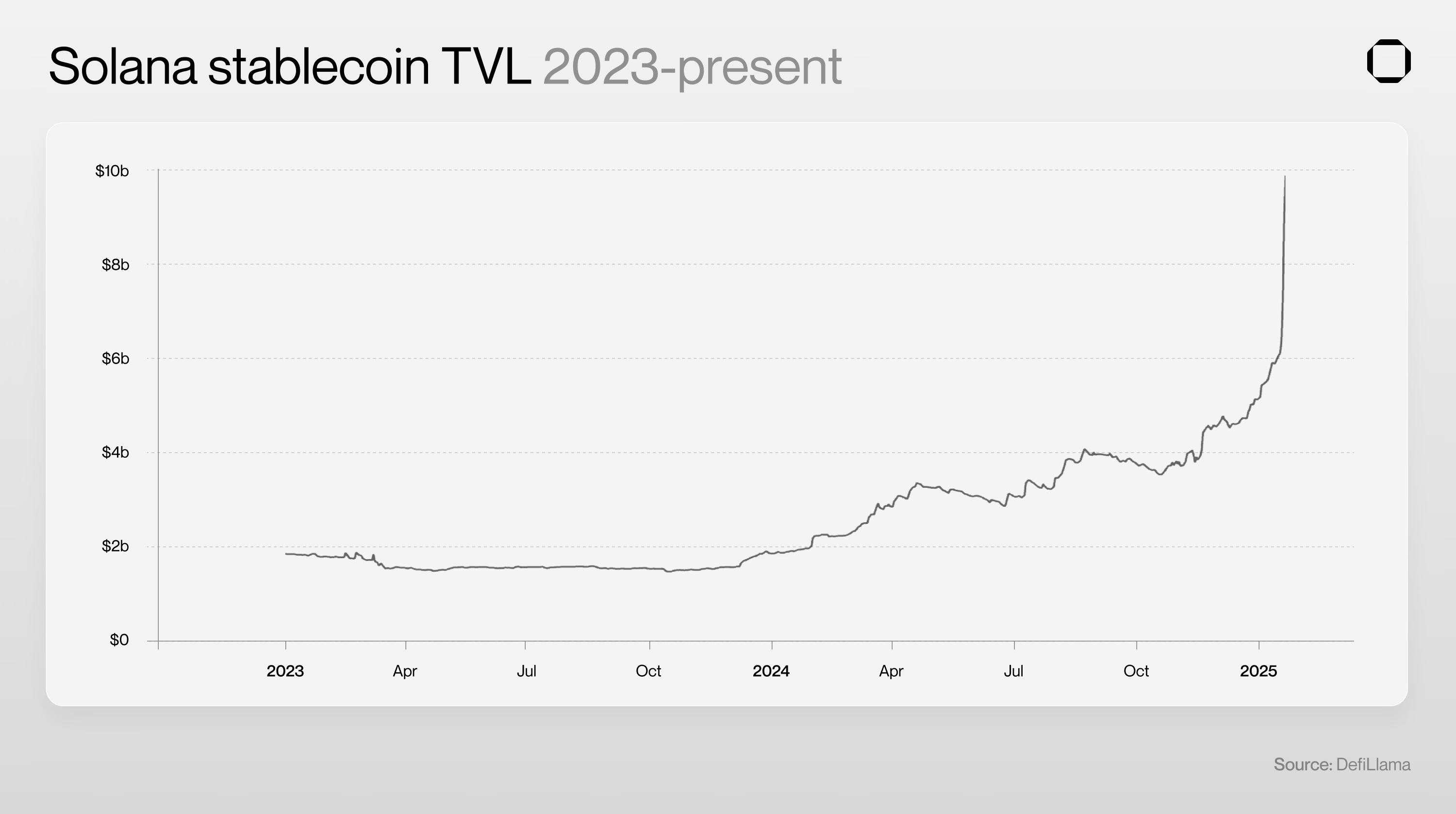

Other key metrics include the availability of stablecoins and the number of stablecoin payment applications in development. As of January 2025, Solana's total value locked (TVL) in stablecoins reached $10.7 billion, a historic high. Between January 15 and 21, 2025, over $3 billion in stablecoins were minted solely on Solana. This significant growth indicates a tremendous opportunity for stablecoin payment use cases.

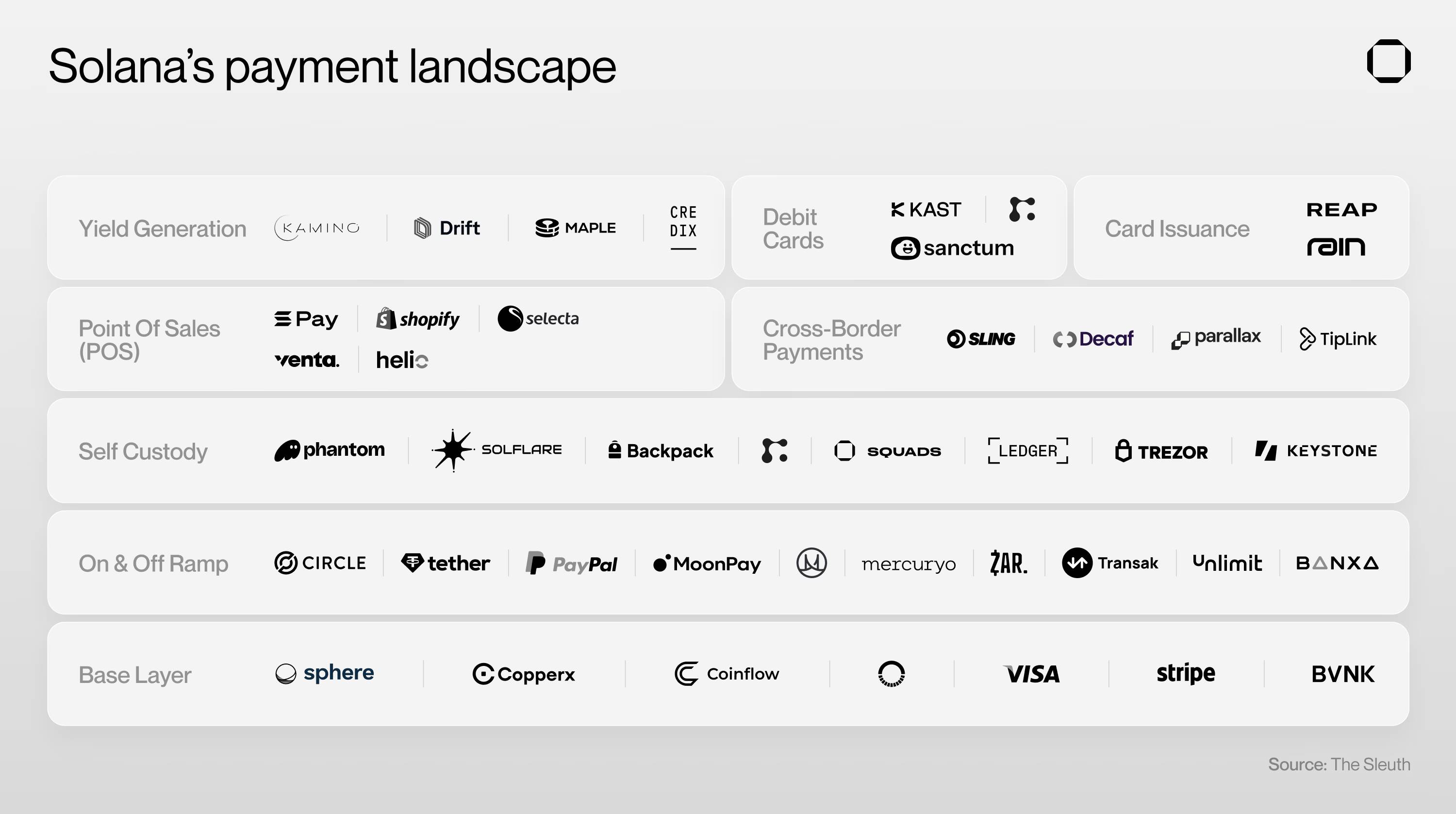

As a result, many verticals in stablecoin payments have already been developed on Solana, such as cross-border payments, point-of-sale payments, debit cards, and yield generation.

Base

Although Base's total value locked (TVL) is far lower than that of Ethereum and Solana, it excels in real economic value (REV) and stablecoin growth.

Today, Base has become the most widely used L2 network globally, with Coinbase increasingly storing user deposits on the blockchain—an important milestone in the history of on-chain economics.

Base's users are unique, as most may have been directly routed from Coinbase (the largest centralized exchange in the U.S.). Coinbase holds a 45% market share in the U.S., so many of Base's users are likely from the North American demographic. This metric is particularly significant for U.S. businesses looking to integrate on-chain payments.

A key factor in Base's success is its unique partnership with Circle. In 2018, USDC was launched by Circle and Coinbase, becoming the first stablecoin supported by a centralized exchange. Additionally, Coinbase initially served as a key member of the Circle Consortium (now dissolved), responsible for the dollar reserves backing USDC. As a subsidiary of Coinbase, Base offers unparalleled advantages to developers and users, such as providing free gas allowances for applications, gas fee discounts when users pay with USDC, and zero fees for USDC on-chain.

Thus, it is not surprising that new native stablecoin payment applications have emerged on Base, such as Peanut, LlamaPay, Superfluid, and Acctual. However, the overall stablecoin payment ecosystem on Base remains significantly smaller than that of Solana, and it is worth noting that Base's ecosystem is still in a relatively young stage.

Regulatory Clarity

From a regulatory perspective, both Solana and Base are currently in good standing, and the incoming Trump administration may further enhance regulatory clarity.

What sets Base apart from other blockchains is that it does not have a native token, so it has not yet faced any regulatory scrutiny. However, Coinbase has not been so fortunate, still embroiled in litigation with the SEC.

Moreover, Base's design limits its neutrality in the face of changing regulations. Under the current design, Base can unilaterally impose geographic restrictions on users, require KYC data for on-chain operations, blacklist tokens or applications, freeze wallets, or require verification through Coinbase to operate on its blockchain. Coinbase's certification feature is already live, providing the necessary tools to enforce these rules. In contrast, Solana operates through over 1,000 validator nodes, ensuring that regulatory requirements are not managed by a centralized entity but enforced through front-end or token expansion.

The regulatory challenges surrounding stablecoins and on-chain payments are not insurmountable; the adoption of blockchain technology by banks (such as Société Générale and Deutsche Bank) or companies (like Visa, Stripe, Venmo, PayPal, Robinhood, Nubank, and Revolut) indicates that the advantages of these technologies may outweigh the temporary risks.

Conclusion

Traditional enterprises and startups looking to integrate stablecoins and on-chain payments cannot overlook the rise of Solana and Base. Solana has significant advantages in demand, a diverse ecosystem, and resistance to censorship. Meanwhile, Base holds advantages due to its strong presence in the U.S., close ties with Coinbase, USDC subsidies, and rapid development pace.

The key distinction lies in trusted neutrality. We believe Base will play an increasingly important role in guiding new companies and users, especially in the U.S. However, in the long term, Solana will emerge as the primary platform for stablecoin payments.

Applications driving borderless capital flows will tend to choose Solana's neutral infrastructure, which is built on distributed innovation rather than relying on a centralized sequencer driven by a single incentive mechanism. Solana provides a fair and future-oriented environment for businesses and developers to create innovative stablecoin payment applications.

The race to build the next on-chain payment super application is intensifying—now is the best time to take action.

If you find this research valuable, please follow us on 𝕏 for the latest research and insights.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。