Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

The market has once again declined, and the demand for financial management has risen again, suggesting an unknown inverse function between the two.

In the past two weeks, we have shared the first issue of “A More Suitable U-Based Financial Management Guide (February 24)” and the second issue of “A More Suitable U-Based Financial Management Guide (Issue 2)”, aiming to cover relatively low-risk yield strategies primarily based on stablecoins (and their derivative tokens) in the current market (systemic risks can never be completely eliminated), helping users who wish to gradually increase their capital through U-based financial management find more ideal earning opportunities.

In this issue, we will continue to focus on the latest trends in the U-based financial management market.

Base Interest Rate

- Odaily Note: The base interest rate tentatively covers single-coin financial management plans from mainstream CEXs, as well as mainstream on-chain lending, DEX LPs, RWA, and other DeFi deposit plans.

Due to the sluggish market, the base interest rates across major CEXs and DeFi platforms have also been weak — the annualized yield for USDT single-coin financial management on OKX has dropped to 1%, and the sUSDe APY on Ethena has also fallen to 4.99%.

For the CEX side, besides the funds currently planned for bottom-fishing in the short term and the shares that can earn subsidies (generally within 500 U, currently Gate and Bitget are relatively higher, allowing for multiple accounts to take advantage), it is not recommended to keep remaining funds in CEXs, as the earning efficiency is indeed too low.

The situation on the DeFi side is relatively better, but still not ideal; it is difficult to find pools with yields above 10% on the most mainstream chains like Ethereum, Solana, and Base, although there are some in smaller ecosystems. For example:

Shadow on Sonic: USDC.e/USDT LP 18.3%;

Kyo on Soneium: USDT/USDC.e LP 17.37%;

Echelon on Aptos: sUSDe 17.14%, USDC 13.53%;

Additionally, keep an eye on Fluid, which is set to be deployed on Polygon; according to the latest proposal, both parties are expected to provide some additional incentives, and with Fluid's deposit APR being relatively high among mainstream lending protocols, the expected yield after incentives should be good.

Pendle Section

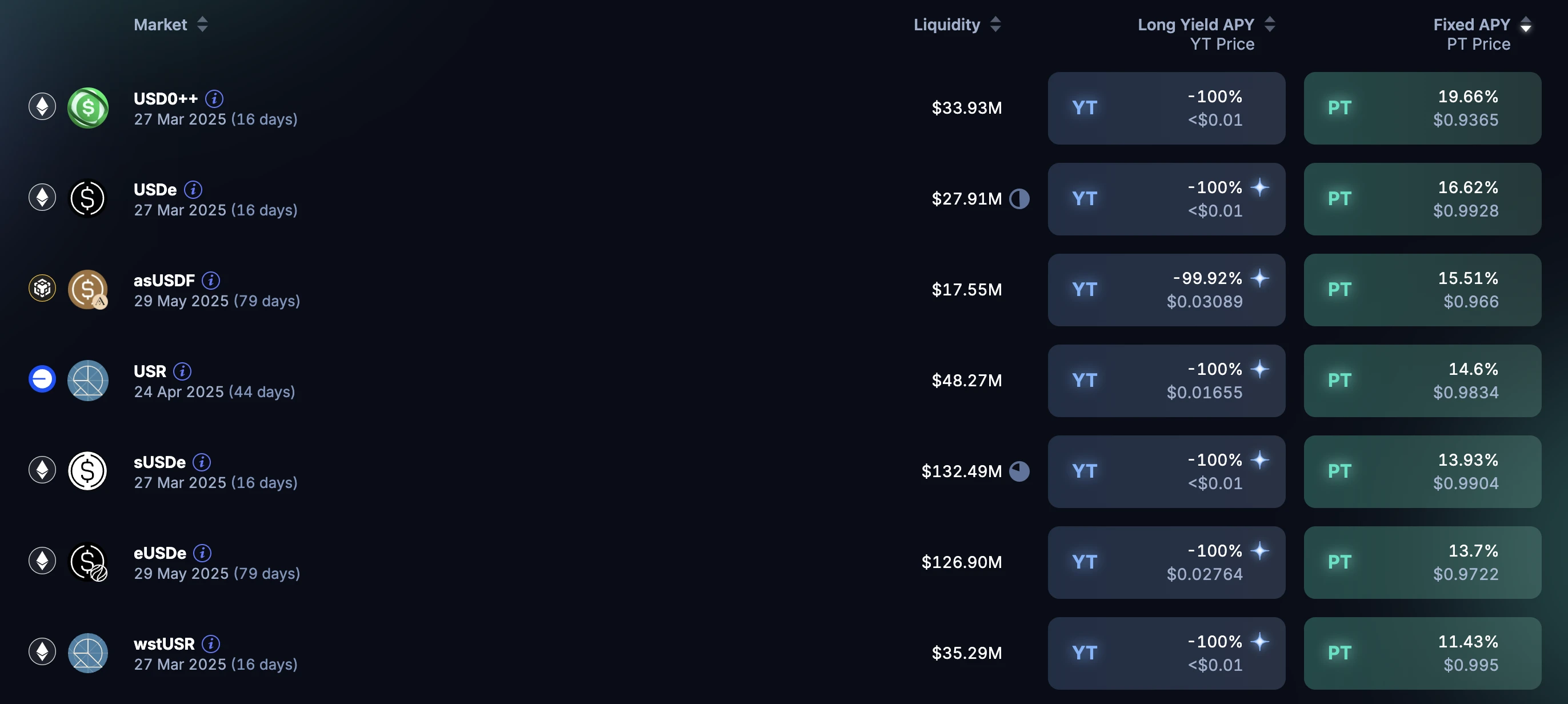

First, regarding fixed income, the real-time ranking of PT yields for various stablecoin pools in Pendle is as follows. Considering the underlying asset conditions (reputation, liquidity, etc.) and maturity dates, I personally recommend the USR expiring on April 24 on Base (PT 14.6%) and the eUSDe expiring on May 29 on the mainnet (PT 13.7%).

This week, I want to focus on the movements of the whales regarding Pendle.

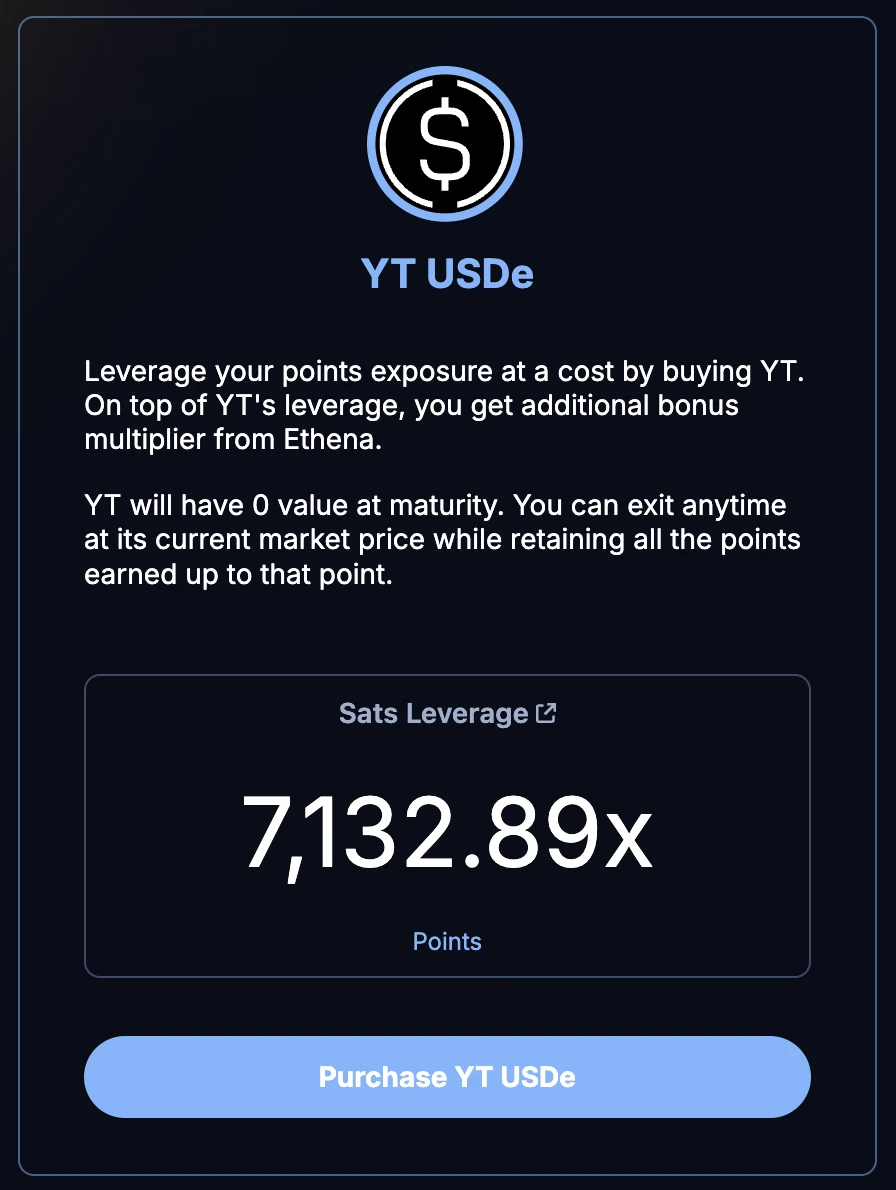

On March 8, whales swept up $70 million in USDe YT (expiring March 27), indicating that these whales are quite optimistic about the Ethena S3 airdrop landing this month. So now the consideration is how to accumulate Ethena points more efficiently and keep up with the whales.

Just to add, the leverage ratio for the USDe YT expiring on March 27 has reached 7132.89 times. If you want to accumulate Ethena points as quickly as possible, directly purchasing YT would be the most efficient path — given that the price of YT will drop to zero on the expiration date, this actually falls under trading behavior and is not covered in this series of articles.

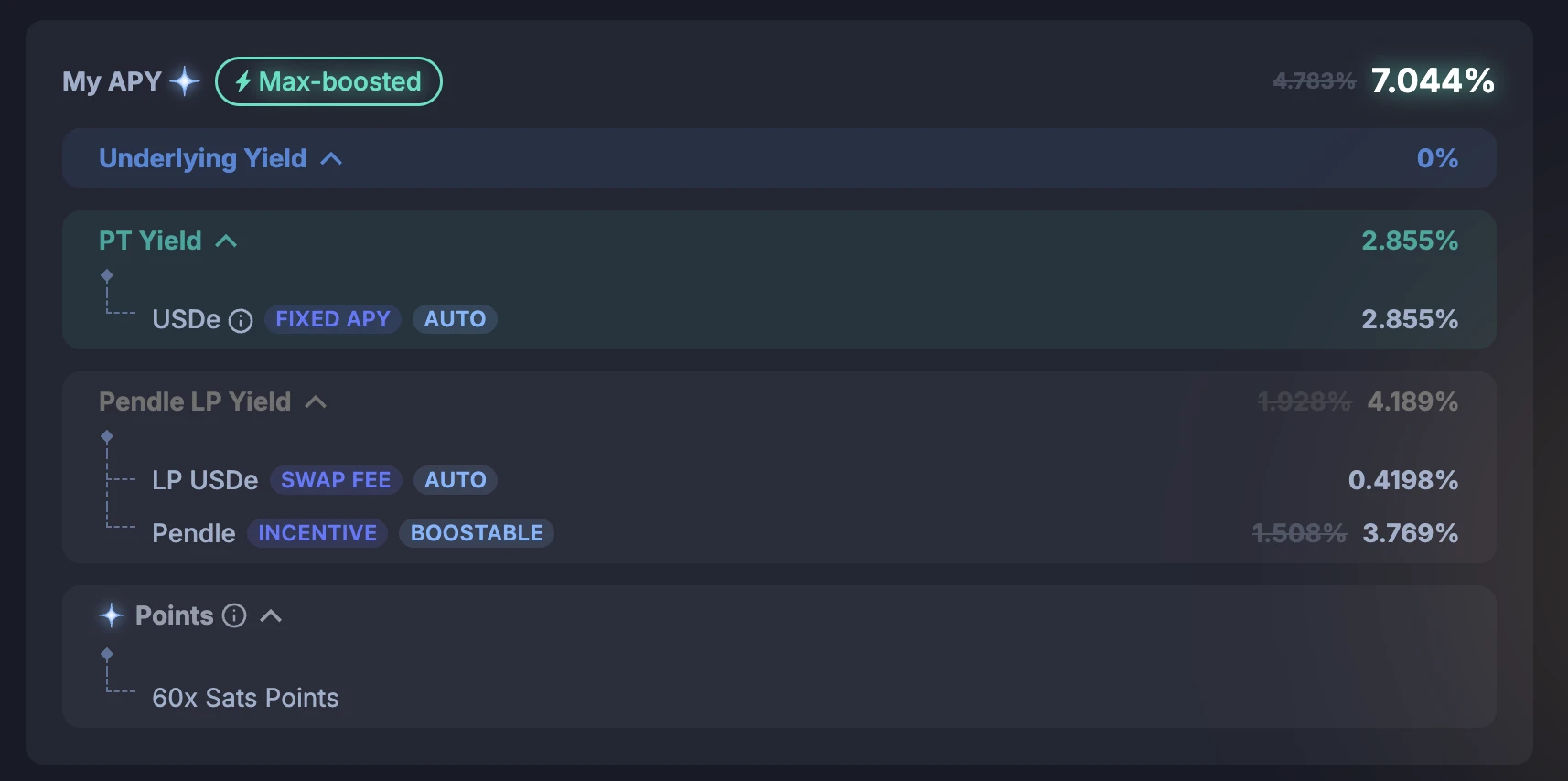

Without wanting to see the principal erode, compared to purchasing PT (which offers higher fixed income), I would currently recommend users participate in LP form (lower visible yield + retain points exposure), particularly the USDe pool expiring on July 31, which has a maximum leverage bonus of 60 times.

Other Opportunities

Last week, we also compiled and shared some scoring strategies on Sonic outside of this series (see “Three Leverage Strategies to Help You Efficiently Capture Sonic's June Airdrop”), but these strategies either require spot-futures combinations (spot + waiting for short positions) to hedge or rely on native protocols on Sonic, which raises certain safety concerns.

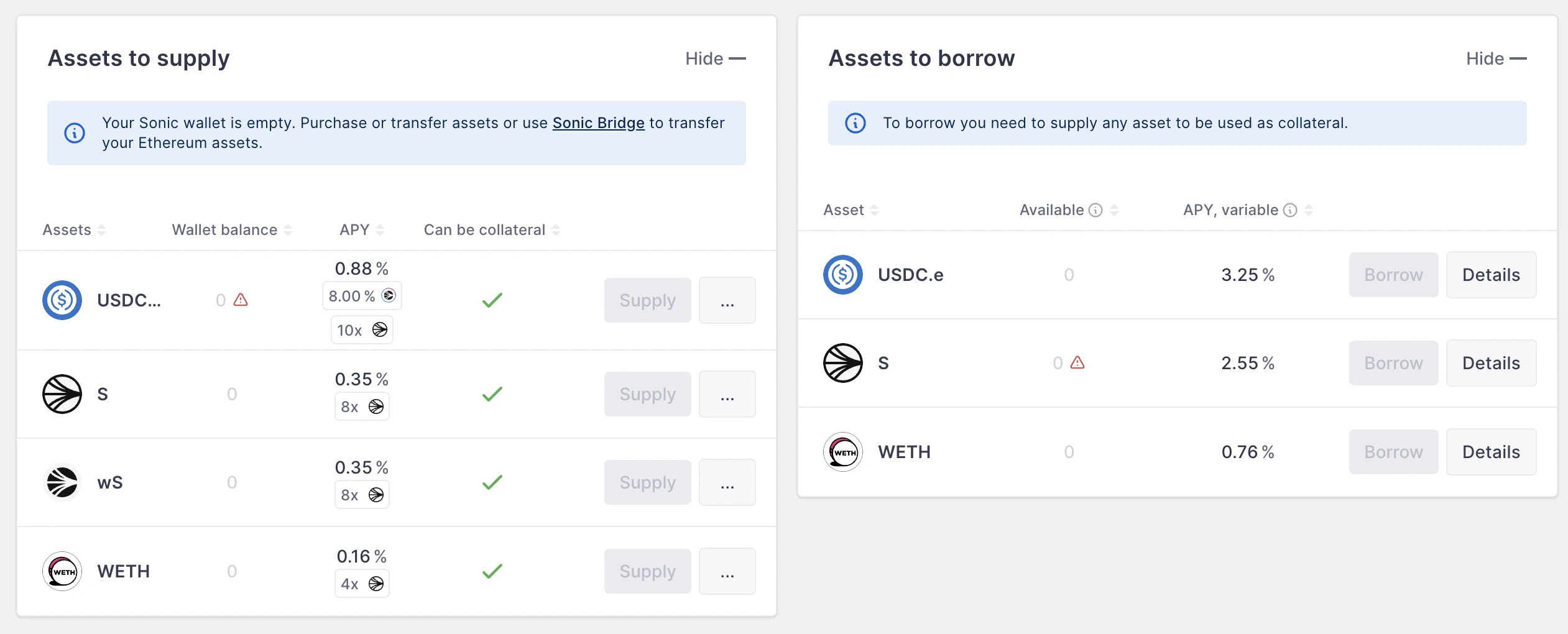

Now the situation has changed! Since Aave was deployed to Sonic last Monday, it has quickly raised the capacity limit of the stablecoin pool (USDC) to $70 million, and this pool can now earn 8% fixed incentives (incentives need to be claimed later through Aavechan, plus there is an additional 0.8% deposit APY), and can also earn 10 times Sonic points.

The key point is that since Aave itself supports lending and borrowing of the same asset (deposit USDC to borrow USDC), there is no need to worry about price fluctuations (for example, in the S/stS pool, there is always concern about unexpected decoupling), so you can leverage without restraint — currently, the borrowing cost for this pool is 3.25%, and the deposit yield is sufficient to cover it, after a few rounds of circular lending, both the base yield and point accumulation rate can be increased by n times.

So, as always, just use Aave!

Additionally, Noble launched the yield-generating stablecoin USDN last week and simultaneously launched a points activity. The awkward part is that the points pool cannot earn the native yield of USDN (4.3%), so it is not possible to enjoy both benefits, while the yield increase for the non-points pool has reached 14.1%. It is up to individual preference whether to prioritize yield or points.

Finally, Movement is expected to open its public mainnet on March 10, which may come with some mining benefits, so stay tuned. If I see good pools, I will update on X (@azuma_eth).

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。