This year, policy uncertainty is relatively high, and we need to continue waiting for more favorable developments to reverse the market's short-term recession expectations.

Author: Jinze, pretending to be in Flower Street

The earnings for S&P 500 companies in 2024 have been released, with 97% of the results essentially settled. Today, I will provide an early analysis of the earnings situation and potential investment considerations.

In the fourth quarter, overall earnings grew by 18.2% year-on-year, the highest quarterly earnings growth since 2021. Revenue growth was 5.3%, lower than earnings growth, reflecting an improvement in corporate profit margins, which is a very healthy sign. (This article will focus on earnings, which have a greater impact on valuation, so revenue will be overlooked.)

Market Anomalies

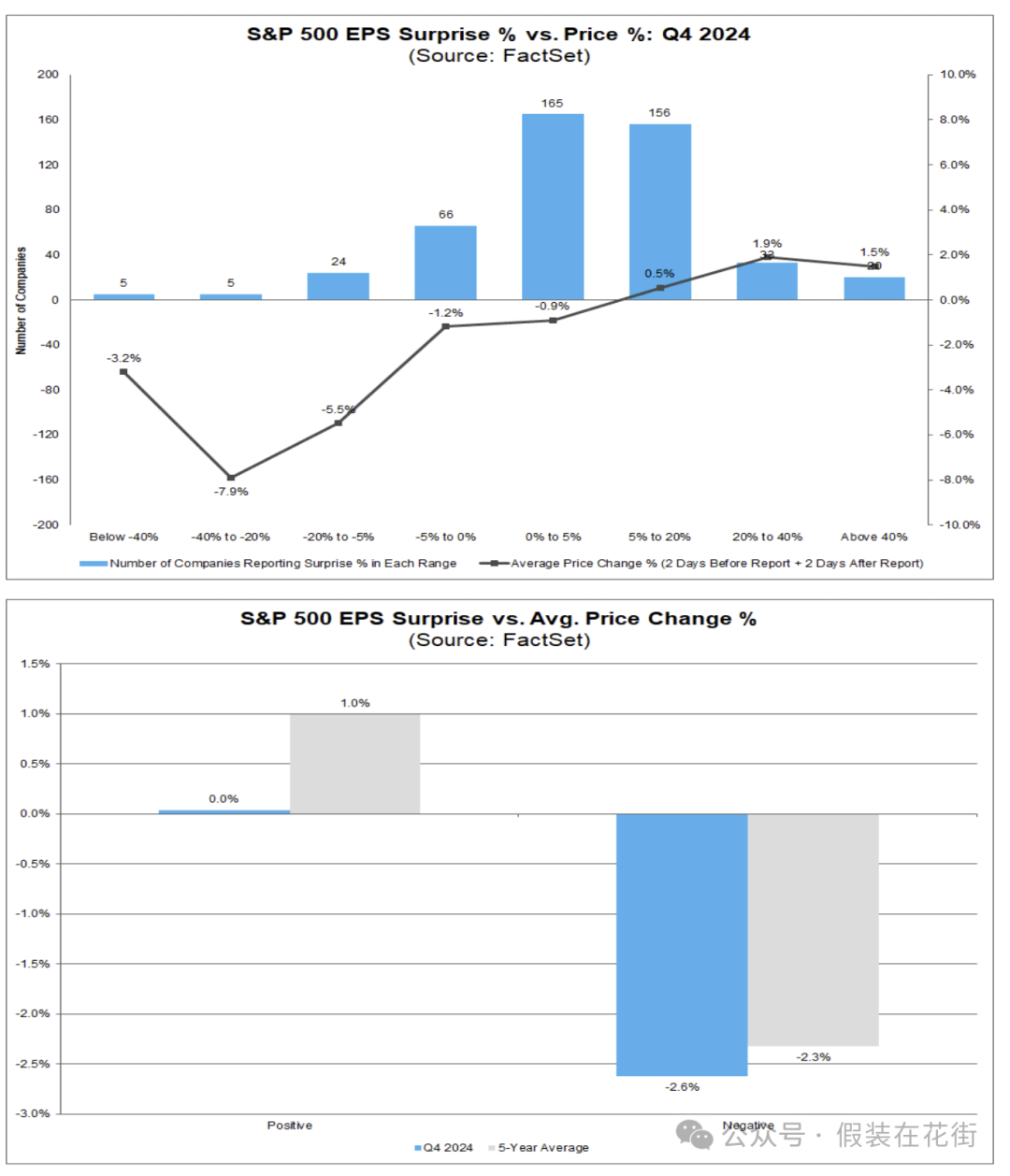

Let’s start with an unusual phenomenon—revenue figures are good, but the market reaction is negative.

Most companies reported better-than-expected earnings, but the revenue surprises were somewhat lacking:

● 75% of companies had earnings per share (EPS) above analyst expectations, slightly below the 77% average over the past five years;

● Only 63% of companies exceeded revenue expectations, significantly lower than the five-year average of 69%;

The market reaction is abnormal:

● No premium for positive surprises: Companies that exceeded expectations saw an average stock price change of 0%, below the five-year average (+1.0%).

● Increased punishment for negative surprises: Companies that missed expectations saw an average stock price drop of 2.6%, higher than the five-year average (-2.3%).

This means that current investors are cautious about good news but particularly sensitive to bad news. This is clearly because the market has already digested optimistic expectations, and stock price valuations are at high levels, making it a better choice to lock in profits in the face of insufficient marginal (surprise) good news.

Currently, the technology and consumer discretionary sectors, both growth-oriented, enjoy high valuation premiums (forward P/E ratios around 26-27 times), the highest among all industries, indicating that investors have high expectations for their earnings growth in the coming years. However, high expectations also mean that if growth falls short, valuations may be quickly compressed (as seen in recent weeks).

For example, there are renewed concerns in the market about technology companies' significant investments in AI not meeting expectations, putting upward pressure on high stock prices for downward revaluation. Recently, the market has shown a punitive reaction to companies that did not meet expectations (average stock price drop of -2.6% for companies with disappointing earnings), warning us to be particularly cautious with sectors that are overvalued. Once there is a "mismatch" between fundamentals and expectations, the pullback in high-valuation sectors could be significant.

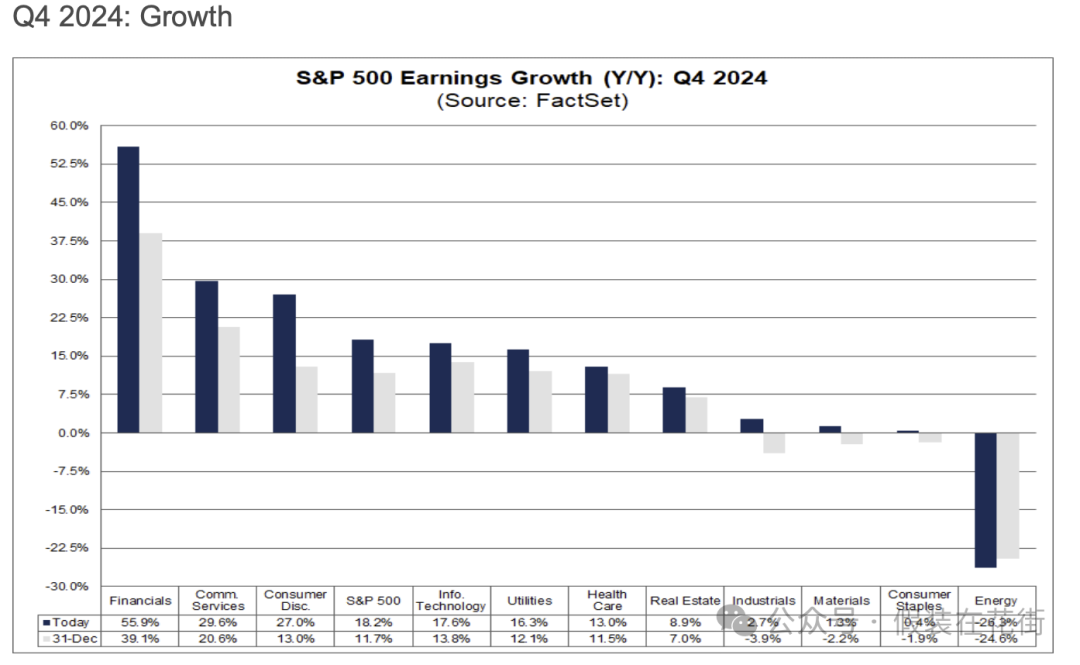

Earnings Growth Generally Strong, Energy Sector as an Exception

Among the eleven sectors of the S&P, ten achieved year-on-year earnings growth, with six sectors experiencing double-digit growth.

● The financial sector benefited from a base effect in the banking industry, with a staggering year-on-year increase of 56%.

● The earnings growth rates for the communication services and consumer discretionary sectors reached approximately 30% and 27%, respectively.

● The information technology sector grew by about 17.6% year-on-year, driven by large tech companies' earnings.

● Defensive sectors like utilities and healthcare also recorded double-digit growth (ranging from about 10% to 16%).

● The only exception is the energy sector, which saw a year-on-year decline in earnings of about 26% due to last year's high base and falling commodity prices.

Note that the exceptionally high growth in the financial sector has a one-time factor, primarily due to a 216% year-on-year surge in banking profits, as last year's figures were depressed by one-time expenses like FDIC special assessments, leading to an unusually low base this year. If we exclude the banking sector, the earnings growth rate for the financial sector would drop significantly from 55.9% to 25.3% (still quite high).

Overall, the environment is very favorable for the financial sector, with net interest margin expansion, a bull market in stocks, and strong borrowing demand driven by high consumer enthusiasm. The only area in the financial sector experiencing shrinking profits is insurance, due to increased claims from well-known natural disasters.

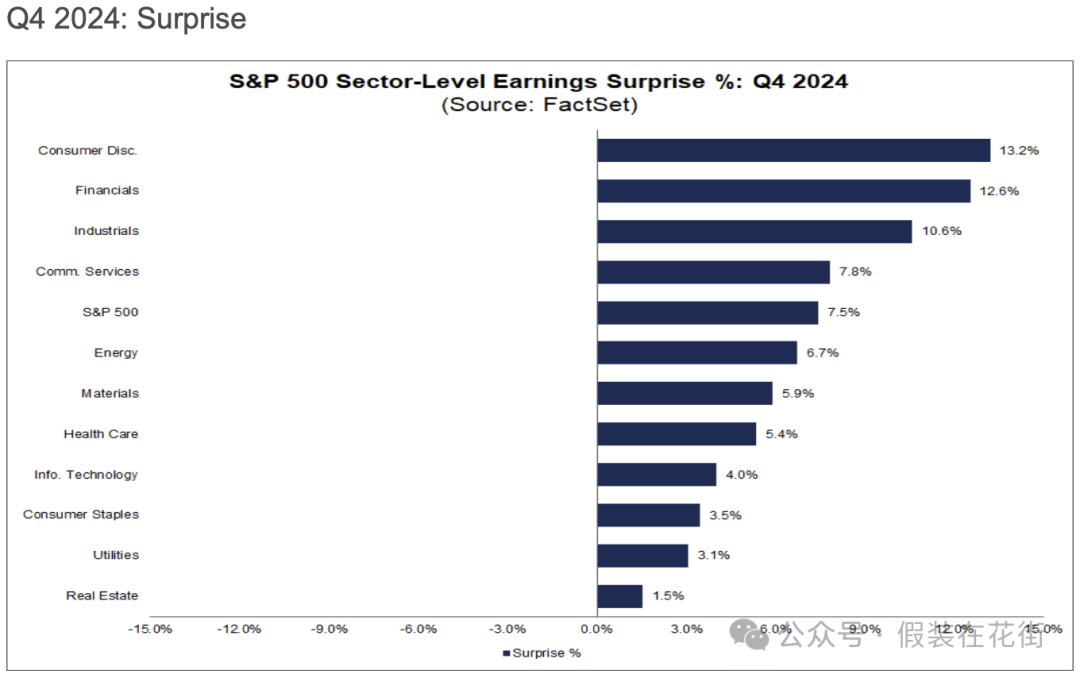

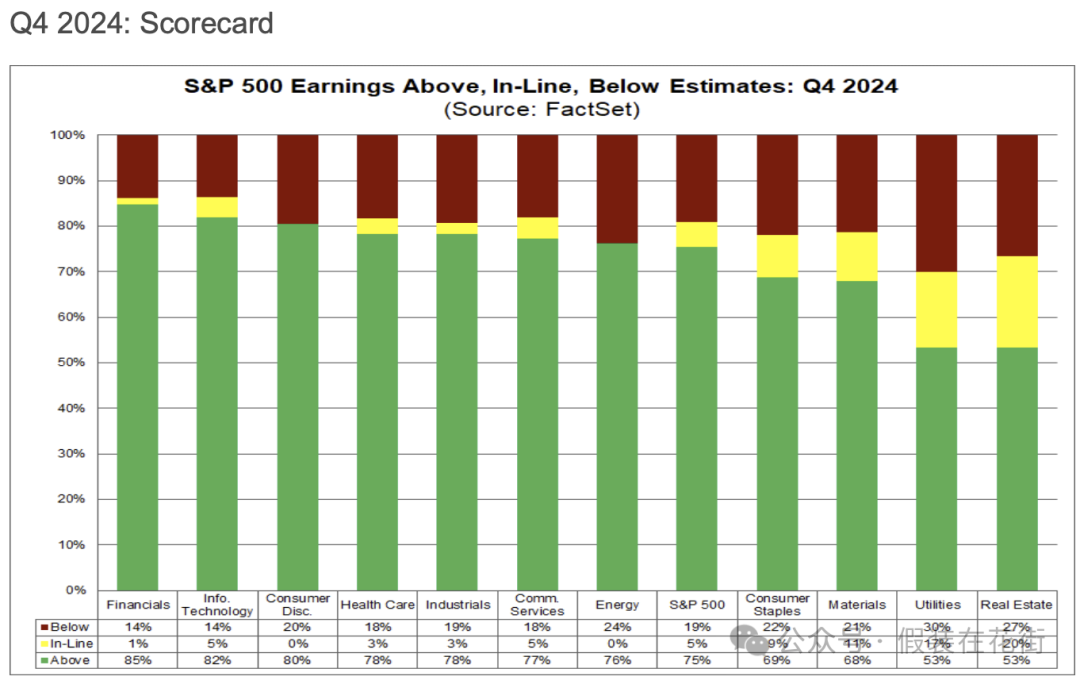

Earnings "Surprise" Situation (Marginal Surprises Declining)

● The strongest earnings surprise sector: The consumer discretionary sector recorded a +13.2% EPS surprise (actual earnings exceeded expectations by 13.2%), leading all sectors.

Several companies in this sector performed exceptionally well, such as Amazon (Amazon.com) with fourth-quarter EPS of $1.86, far exceeding the expected $1.49, Norwegian Cruise Line ($0.26 vs. $0.11), and Wynn Resorts ($2.42 vs. $1.34).

● The financial sector's overall earnings exceeded forecasts by 12.6%, represented by companies like Berkshire Hathaway ($6.74 vs. $4.62) and Goldman Sachs ($11.95 vs. $8.21), Morgan Stanley ($2.22 vs. $1.70).

● The industrial sector had an unexpected EPS surprise of about +10.6%, with Uber's earnings soaring ($3.21 actual vs. $0.50 expected), Axon ($2.08 vs. $1.40), GE Aerospace ($1.32 vs. $1.04), and Southwest Airlines ($0.56 vs. $0.46) showing strong performances.

● The communication services sector also performed well, with overall earnings exceeding expectations by about 7.8%, including major companies like Disney ($1.76 vs. $1.45) and Meta ($8.02 vs. $6.76) delivering significantly better-than-expected results.

● Underperforming sectors: The proportion of companies in the real estate and utilities sectors that exceeded expectations is only about 53%, significantly below the average level.

Valuation Levels

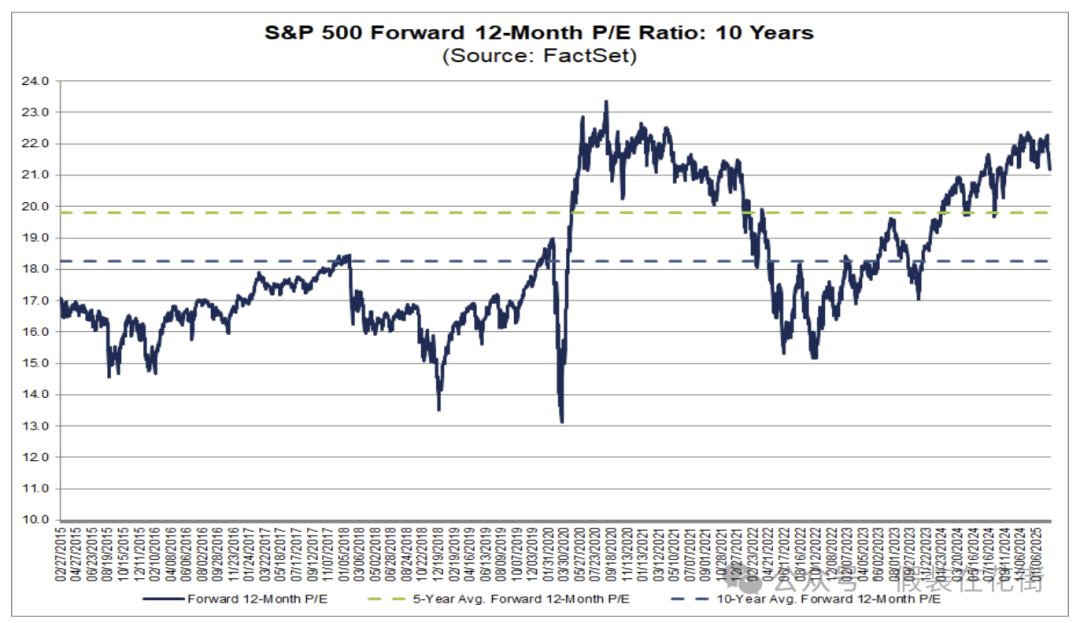

The latest forward 12-month price-to-earnings ratio (P/E) for the S&P 500 index is about 21.2 times, higher than the five-year average of 19.8 times and the ten-year average of 18.3 times.

However, compared to the end of last year, the index's forward P/E has slightly decreased from 21.5 times, partly due to the index price decline this year and partly because future earnings expectations have been raised by 1.1% during the same period, with earnings growth absorbing some of the valuation.

The recent pullback between 18.3 and 19.8 times can find historical average support, corresponding to S&P 500 points of 4964 to 5371 (considering the March 4 closing price of 5778, the market could gradually enter a safer zone after a 7.5% decline).

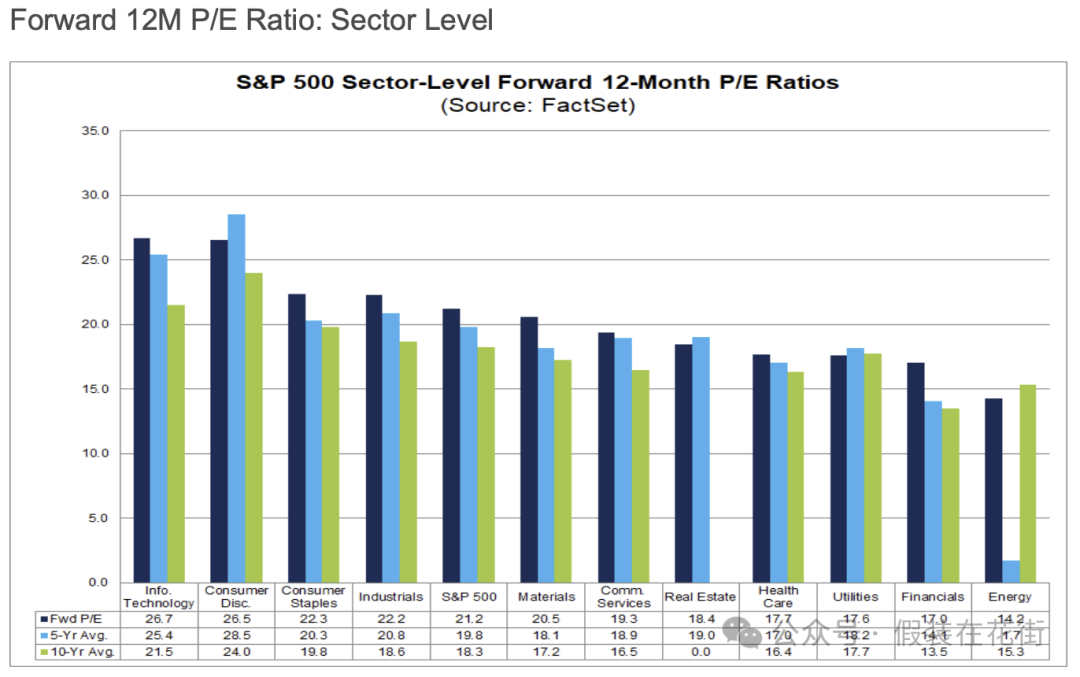

At the industry level, valuation levels vary across different sectors:

The information technology (about 26.7 times) and consumer discretionary (about 26.5 times) sectors currently have the highest forward P/E ratios, reflecting investors' high expectations for their future growth;

In contrast, the energy sector's forward P/E is only about 14.2 times, the lowest among all sectors.

Other sectors, such as financials, have moderate valuations (around 16 times), while defensive sectors like utilities and healthcare are in the 17-18 times range.

Overall, most industries currently have valuations above their historical averages, needing sustained future earnings growth to absorb current price levels.

The blue bars in the chart below represent the current forward P/E, while the green and gray bars represent the historical levels of the sector. The vast majority of industries currently have valuations (blue bars) above their historical averages.

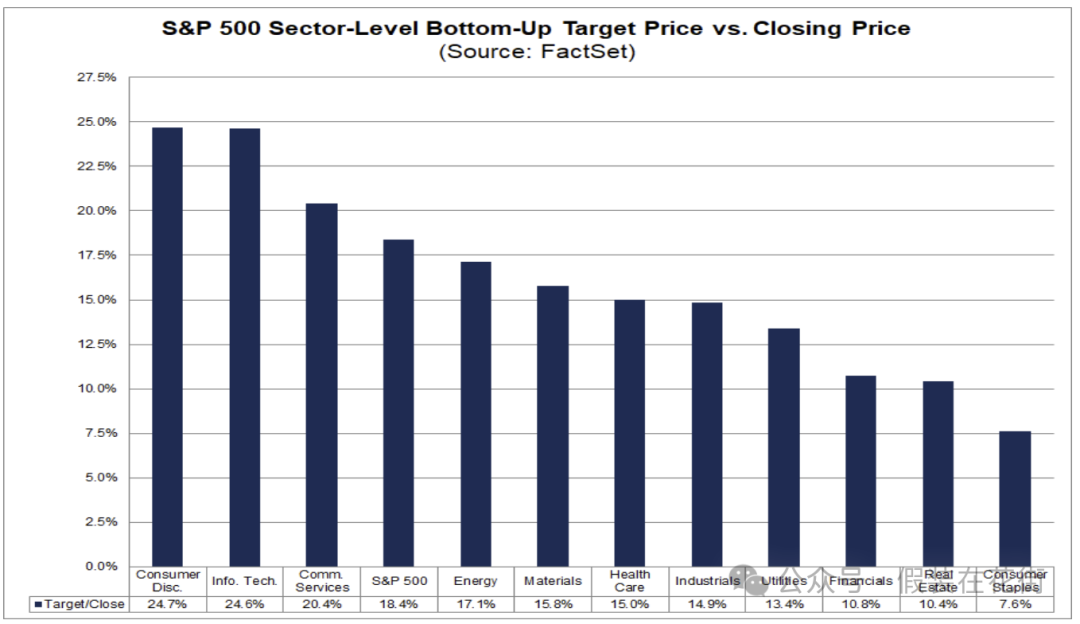

Analysts now have a target price of 6938 for the S&P 500, with an 18.4% upside potential from the closing price at the end of February (5861), led by consumer services (+24.7%) and technology (+24.6%), while consumer staples (+7.6%) have the weakest expectations.

Changes in Profit Margins

Improvements in net profit margins can confirm the high quality of corporate earnings and even the U.S. economy.

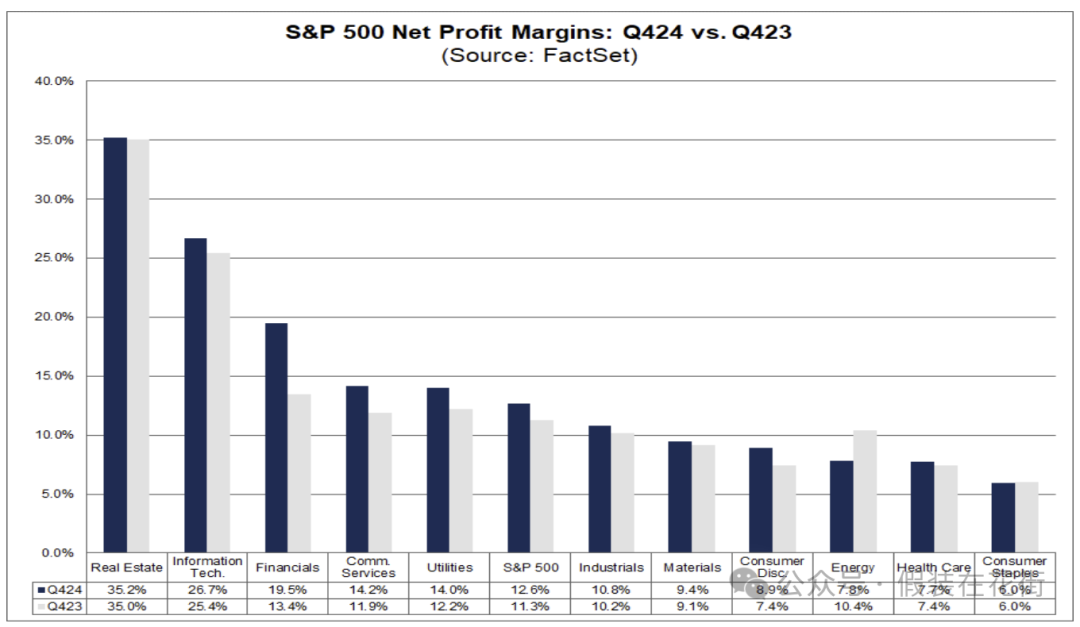

The net profit margin for the S&P 500 index rose to 12.6% in the fourth quarter, up from 12.2% in the previous quarter and significantly higher than 11.3% in the same period last year.

Most sectors saw year-on-year margin expansion, with the financial sector's net margin jumping from 13.4% in the same period last year to 19.5%, marking the largest increase among sectors.

Sectors like communication services and consumer discretionary also achieved significant margin improvements (for example, communication services rose from 11.1% to around 14.2%).

On the other hand, the net margin for the consumer staples (daily consumer goods) sector was only 6.0%, unchanged from the same period last year, showing no improvement.

The energy sector's net margin fell from 10.4% last year to 7.8%, the only sector to experience a year-on-year decline.

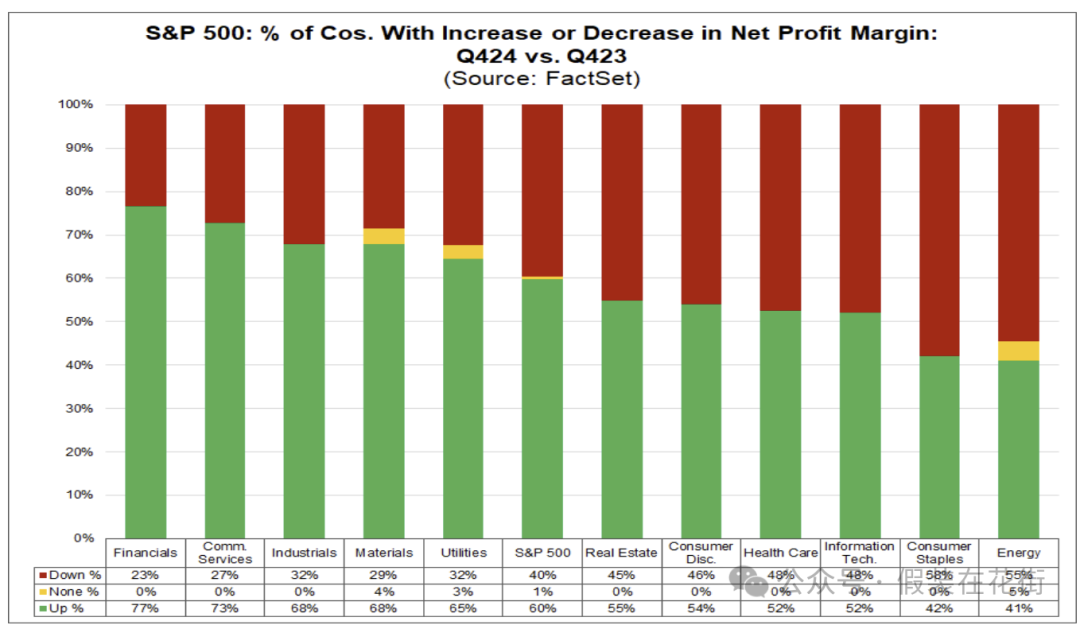

Among S&P 500 companies, 60% reported an increase in profit margins, while 40% reported a decline, mainly concentrated in the consumer staples and energy sectors.

Although six sectors still have net margins below their respective five-year averages (for example, the healthcare sector's net margin is 7.7%, below its five-year average of 9.6%), the overall trend is positive: companies have generally improved their profitability this quarter through price increases and cost reductions.

This improvement in profit margins lays a more solid foundation for future earnings growth, and long-term investors should prioritize industries and companies with rising margins and pricing power.

2025 Outlook Changes

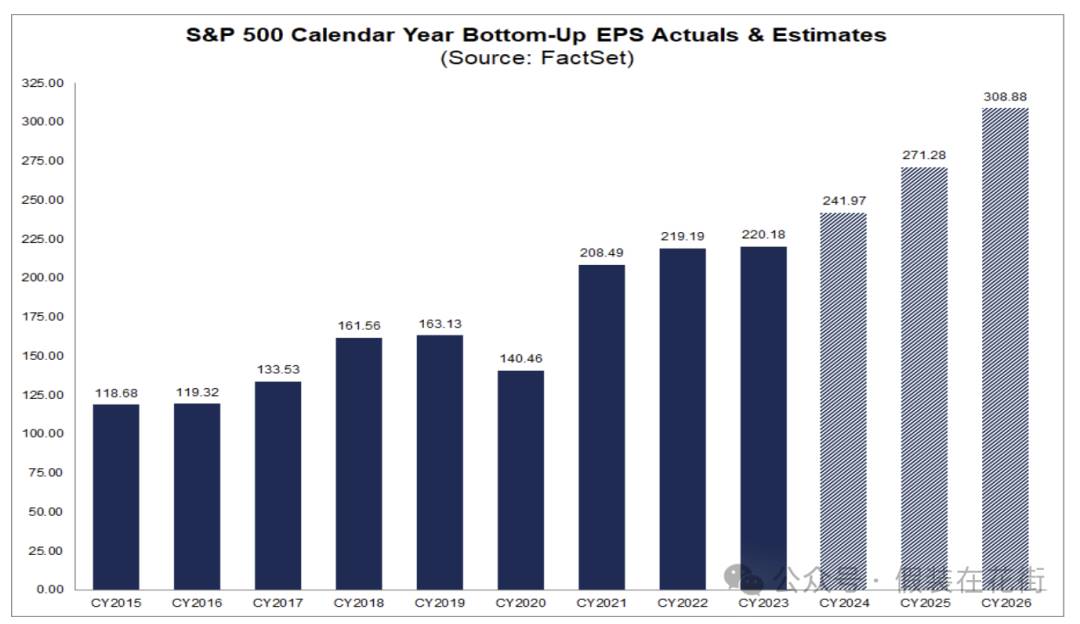

The market generally expects the S&P 500 index's earnings growth rate to maintain high growth in 2025 and 2026.

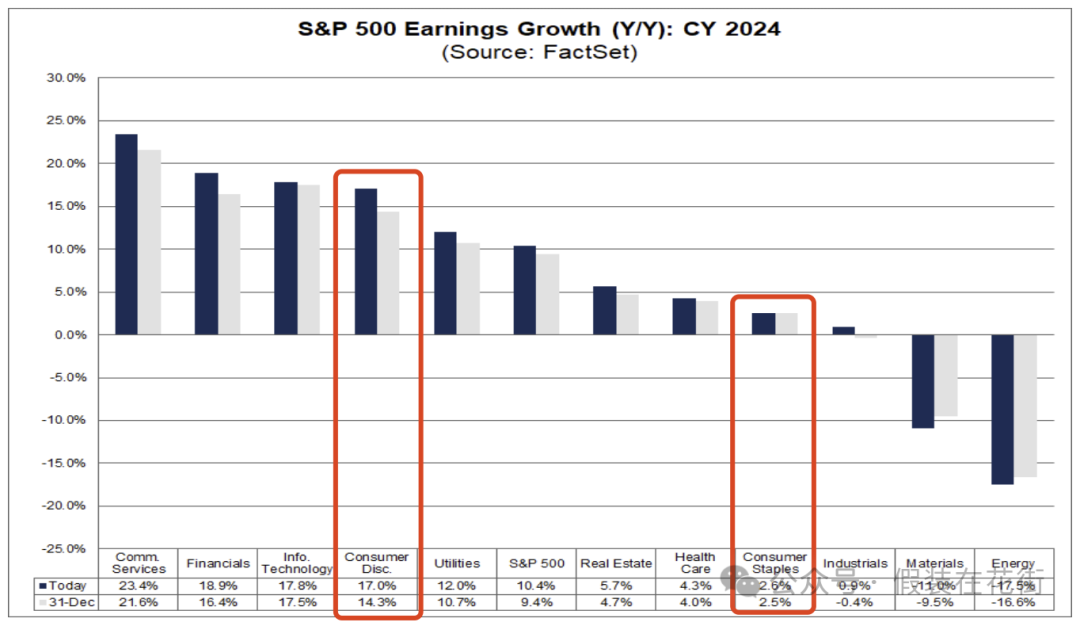

According to analysts' consensus forecasts, the earnings growth rate for S&P 500 companies is expected to rise from 10.4% in 2024 to about 12% in 2025, and further to about 14% in 2026.

It is important to note that these growth expectations assume that the macro economy can avoid recession and maintain moderate expansion; otherwise, expectations may be adjusted downward.

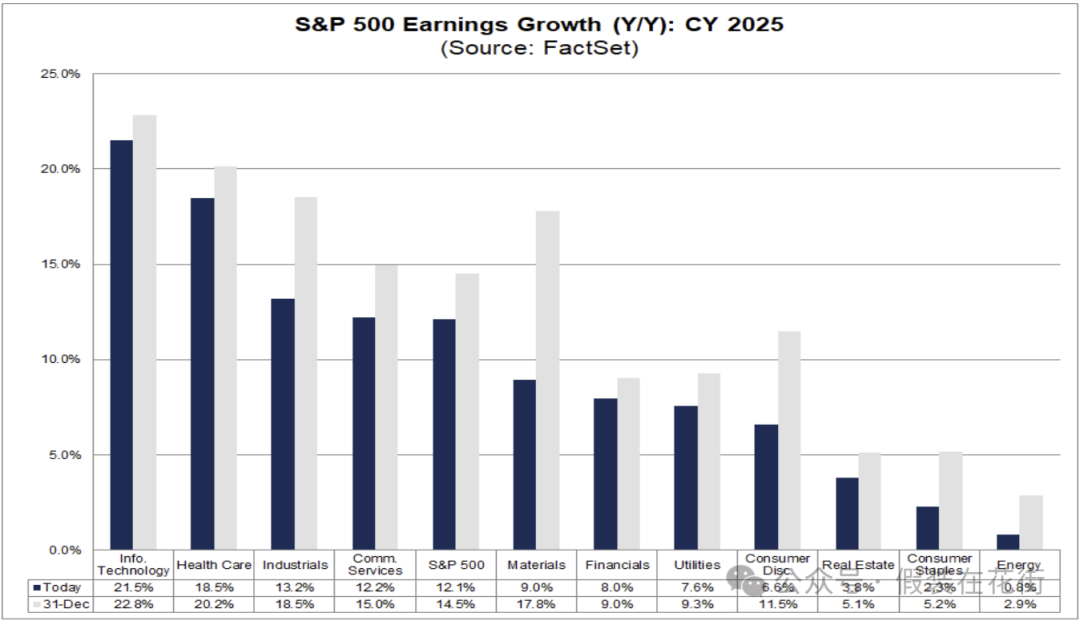

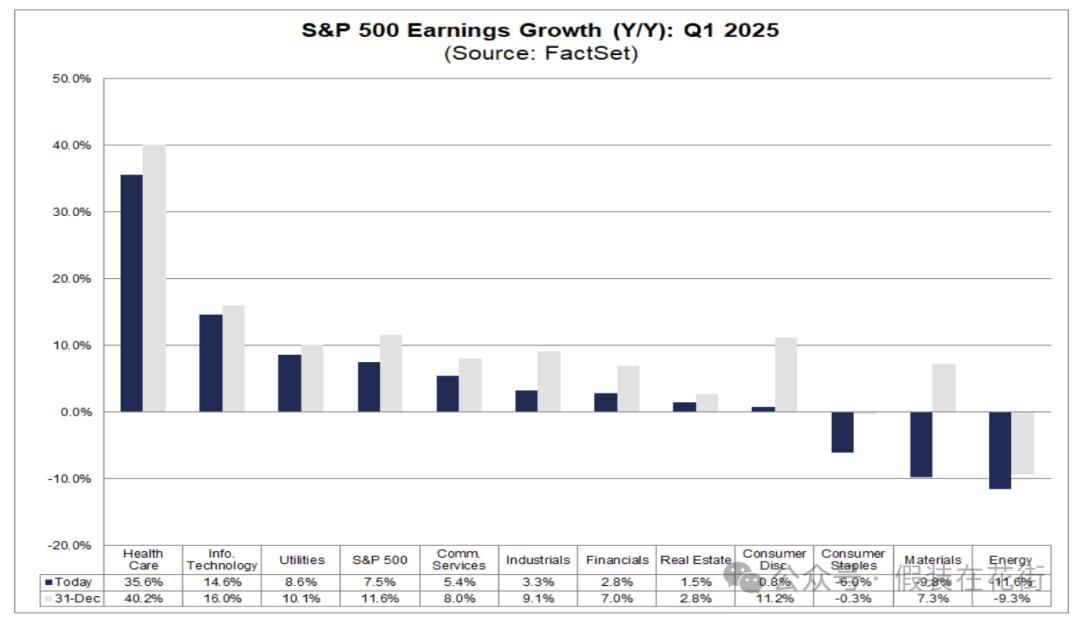

Analysts' top sectors for 2025 are IT +21.5%, healthcare +18.5%, and industrials +13.2%. Compared to expectations at the end of last year, there have been downward adjustments, particularly for materials, consumer staples, and consumer discretionary:

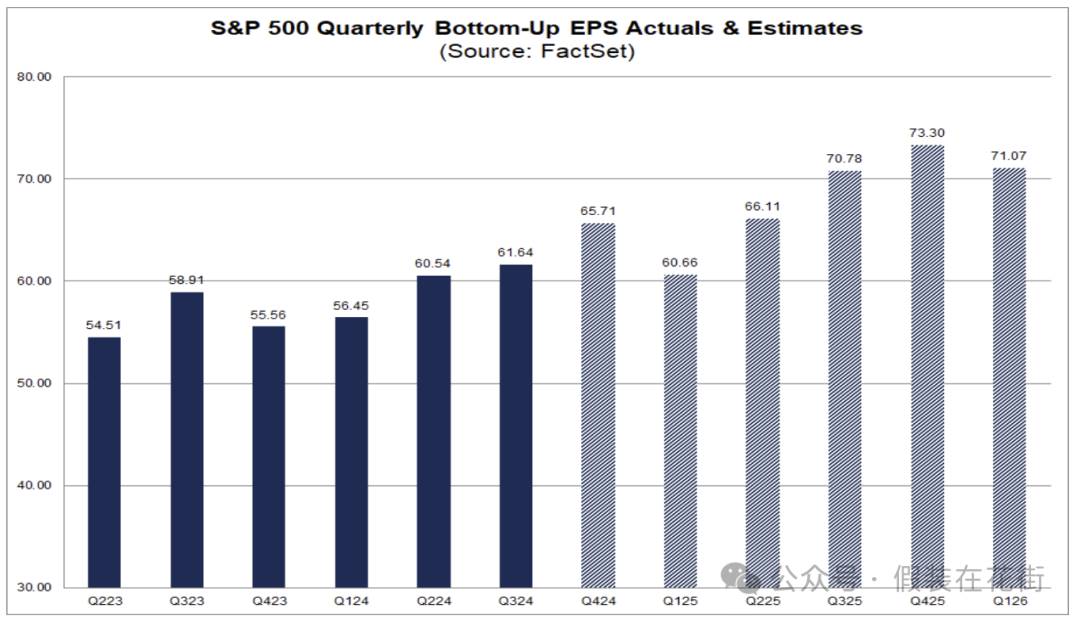

However, it is important to note that despite an overall positive outlook, the S&P 500 earnings forecast for the first quarter of 2025 is particularly low. Recently, companies have lowered their Q1 earnings guidance by 3.5%, a decline that exceeds the averages for the past 5, 10, and 15 years.

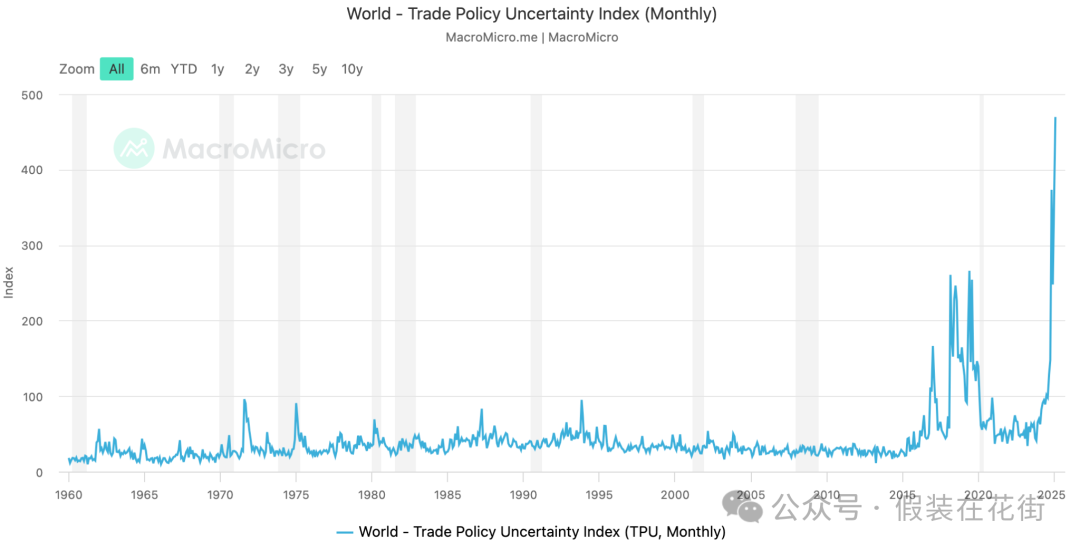

In addition to the seasonal tendency for companies to proactively lower market expectations at the beginning of the year to facilitate "better-than-expected" performance later, concerns about inflation and tariffs, especially for companies reliant on international markets or production/sourcing channels, seem to confirm this significant decline in materials and consumer sectors:

Higher tariffs not only directly increase corporate costs but also create uncertainty in supply chains and demand outlooks. Many experts worry that if a new round of tariff retaliation erupts between major economies, corporate earnings will face substantial blows. This macro-level tension has risen to historical highs in the first quarter:

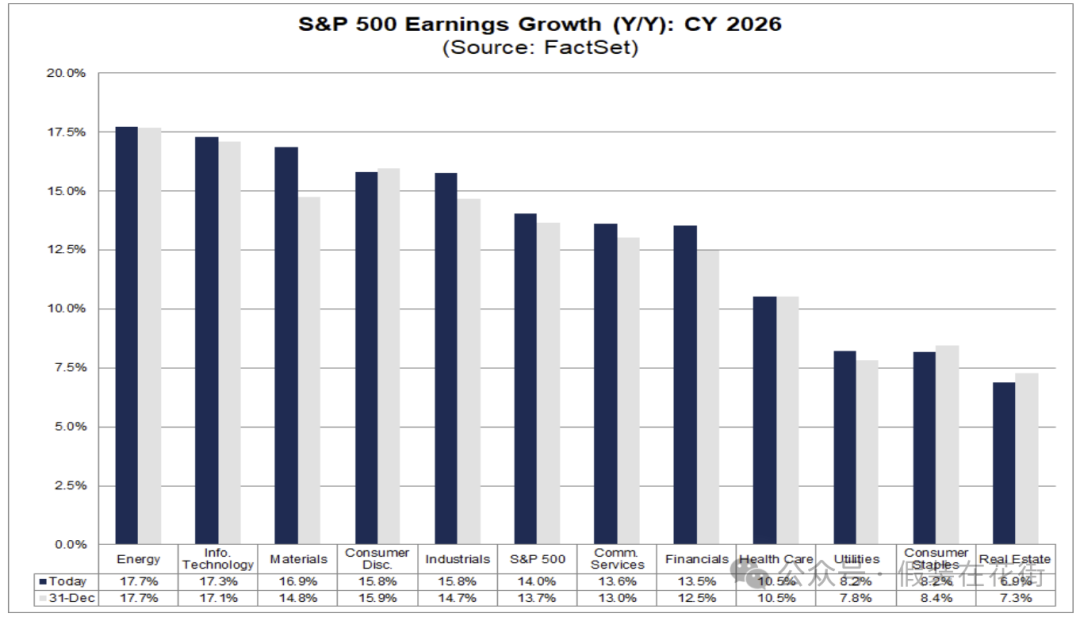

In contrast, analysts are much more optimistic about 2026, and the recent increase in uncertainty has not shaken the market's long-term confidence:

Contradictory Phenomenon: Stagnation in Consumer Staples Growth, Strong Growth in Consumer Discretionary

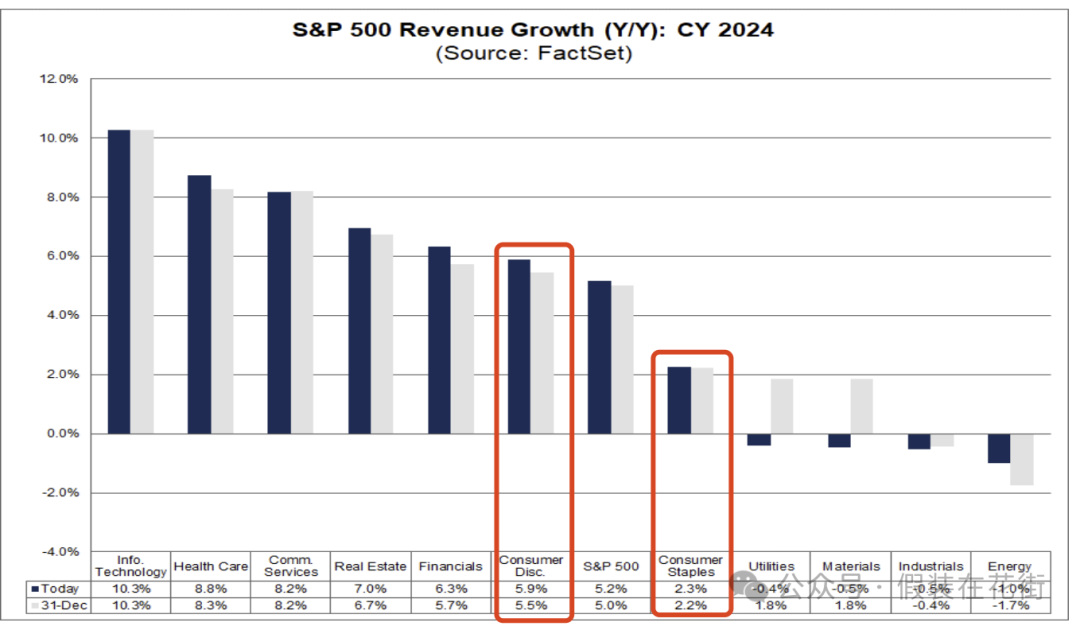

Last year's financial reports showed that the consumer staples sector (such as food, beverages, and household goods) experienced stagnation, while the consumer discretionary sector (such as automobiles, luxury goods, and entertainment) performed strongly.

For the entire year, industry revenue: discretionary +5.9% vs. staples +2.3%

Profit growth comparison: discretionary +17% vs. staples +2.6%

Observing individual stocks provides a clearer understanding, for example: PepsiCo's year-on-year growth was only about 0.42%, Coca-Cola grew by 3%, Procter & Gamble grew by only 2%, and Johnson & Johnson grew by 4.3%.

I believe the divergence here may be due to two main reasons:

- Income disparity leading to differentiated consumption structures:

Wealthier households benefit from stock market and real estate appreciation, leading to increased net worth and stronger consumption willingness, allowing them to spend more on discretionary items like luxury goods, travel, and entertainment, thus driving the boom in travel and leisure industries. For instance, companies like Royal Caribbean Cruises and DraftKings performed exceptionally well in 2023 because consumers shifted more spending towards travel and entertainment.

In contrast, low-income households are reducing non-essential spending under inflation and debt pressure. Low-income groups are becoming more frugal with essentials, purchasing discounted items: in the realm of daily necessities like food and cleaning supplies, consumers tend to choose cheaper private label alternatives over well-known brands. This limits the pricing power of consumer staples companies, so despite the fact that U.S. wage growth outpaced inflation in 2024, boosting consumers' real disposable income, consumers began to "buy less and buy cheaper," making it difficult for staples sales to improve.

Retail data for 2024 shows that spending among high-income households has significantly increased, with inflation-adjusted consumption of goods rising nearly 17% compared to pre-pandemic levels, while low-income households only increased by 7.9%.

Thus, while inflation suppresses low-end demand, economic growth has released high-end demand, creating a macro environment that is generally favorable for discretionary consumption while relatively dragging down staples consumption.

- Corporate profitability and pricing strategies:

The profit growth of consumer staples companies is constrained by limited pricing power. In the early stages of inflation, these companies raised prices to boost profits, but by 2024, as consumer resistance increased, the pricing power for staples companies has narrowed. For example, General Mills saw a 3% decline in sales in the first half of fiscal 2024, and although it managed to achieve a 1% revenue increase through a 4% price hike, it had to lower its full-year revenue growth forecast to 1% or flat. This indicates that staples companies' strategy of "making up for volume with price" is unsustainable, as declining sales nearly offset the benefits of price increases. Cost pressures and promotional competition have stagnated their profit margins, leading to stagnant profit growth.

In contrast, consumer discretionary companies have greater profit elasticity. The recovery in demand in 2024 has allowed many discretionary companies to regain pricing power or achieve economies of scale. For instance, Amazon achieved an EPS of $1.86 in Q4, far exceeding the previous year's $1.00, significantly surpassing expectations. Not only Amazon, but other sectors within discretionary consumption also performed well: the overall retail sector saw a year-on-year profit increase of 87%, and the automotive sector grew by 13%. The consumer discretionary sector's Q4 revenue increased by about 6% year-on-year, but profits surged by 26%—indicating that companies successfully passed on costs and improved profit margins. Many discretionary companies expanded unit profits through price increases or cost controls. Even in price-sensitive areas, the recovery in consumption has brought operational leverage effects (for example, cruises and airlines turning from losses to profits), leading to a noticeable improvement in overall profit margins.

Investment Insights

◆ Adjust return expectations and focus on cash flow: After two consecutive years of over 20% high returns, future gains in U.S. stocks may trend towards moderation. Valuations are already high, making it difficult to replicate the past two years' surge driven by valuation expansion. Investors should lower their expectations for overall index gains in 2025 and focus more on earnings growth and dividends as "endogenous" returns. Market returns will increasingly depend on whether companies can deliver double-digit earnings growth expectations from Wall Street.

This year, policy uncertainty is relatively high, especially with Trump’s short-term policies that are detrimental to the economy being implemented, such as tariffs, layoffs, spending cuts, decoupling, and driving out low-end labor;

Conversely, most supportive growth measures remain verbal or progress slowly:

For example, further reducing corporate taxes, exempting certain incomes (like tips and overtime pay) from taxes, or even overall lowering personal income taxes; only the energy and technology sectors have seen some policy relaxations, which have limited benefits for the overall economy;

We need to continue waiting for more favorable developments to reverse the market's short-term recession expectations.

Otherwise, if valuations continue to contract, offsetting earnings growth, the stock market may experience zero or negative returns. Therefore, investors should prepare mentally: be cautiously optimistic, avoid over-reliance on bull market inertia, and be ready for longer-term holdings to wait for earnings realization. At the same time, pay attention to the return structure, shifting from pursuing capital gains to balancing dividend income, to obtain stable cash flow in a volatile market.

Opportunities and Risks in Specific Sectors

◆ Utilities Sector – Short-term performance pressure and interest rate sensitivity. As a high-dividend defensive sector, utilities are extremely sensitive to interest rate changes. In the current environment where rates are expected to decline, their dividend attractiveness may rebound. However, if rates rise further or AI demand expectations cool, they may face dual pressures.

◆ Consumer Staples Sector – Growth stagnation, lack of upward drivers. The profit growth of the consumer staples industry (such as food and daily necessities) has essentially stagnated, with a slight year-on-year decline of about -1% in Q4 and no improvement in profit margins (remaining at 6.0%). The proportion of analysts giving "buy" ratings to companies in this sector is the lowest among all industries (about 41%). Under inflation, tariffs, and layoff pressures, staples companies face difficulties in passing on costs, with unclear growth prospects and limited profit margins. However, if the economy shows clear signs of slowing down or even recession, their stable cash flow and counter-cyclical characteristics will provide downside protection. Additionally, after the recent valuation correction, some leading stocks have relatively attractive dividend yields, making them suitable for long-term defensive positioning in a downturn.

◆ Financial Sector – Rapid profit growth and significant margin improvement, with a sector valuation of only about 16 times forward P/E, which is relatively low among industries. As long as the fundamentals are not too poor, combined with relatively low valuations, the financial sector remains attractive in the long term even if interest rates decline slightly.

◆ Information Technology Sector – Large tech companies are expected to continue leading profit growth, with surprise performances from chip and software giants like NVIDIA and Microsoft supporting the industry. Although current valuations are high (about 26.7 times forward earnings), the tech sector possesses high profit quality and moats. Long-term trends such as digital transformation and artificial intelligence will continue to drive sector growth. Accumulating quality tech leaders during pullbacks may become a source of long-term returns.

◆ Healthcare Sector – Defensive sector performance stabilizing. The healthcare industry saw a return to double-digit profit growth in Q4, with 82% of companies exceeding revenue expectations. Large pharmaceutical and medical device companies benefited from a rebound in demand and a weaker dollar, leading to improved profits. Although the sector's net margin (7.7%) remains below historical levels, the rigidity of healthcare demand makes its profits relatively stable and strong against economic cycles. During periods of market volatility, healthcare can provide robust returns as a defensive allocation, making it worthwhile to maintain a certain weight in long-term investment portfolios.

◆ Consumer Discretionary Sector – Consumption upgrade is a long-term trend, with high profit elasticity. The consumer discretionary sector's profits surged by 27% year-on-year in Q4, marking a strong rebound for several consecutive quarters. The recovery in consumer spending on travel, entertainment, and luxury goods has driven cruise companies, casino resorts, and brand retailers to exceed expectations (for example, Norwegian Cruise Line and Wynn Resorts both had profit surprises exceeding 80%). Although the sector's forward P/E exceeds 26 times, as long as the economic environment remains stable and employment and income trends are positive, high growth is expected to partially absorb the high valuations.

High-quality discretionary stocks still have the potential for excess returns in the long term, but it is essential to closely monitor consumer confidence and the macro environment. Like tech stocks, despite recent pullbacks, the long-term outlook remains positive. Considering that if the Federal Reserve begins to cut rates in the second half of 2025, large consumer goods like automobiles and home improvement may see a rebound.

However, it is crucial to be cautious about whether the high growth in discretionary consumption can be sustained, as it depends on consumers' financial health: currently, excess savings among U.S. consumers have significantly declined, and factors such as the resumption of student loan repayments and soaring credit card rates may weaken some consumer demand in 2025. Therefore, it is also necessary to closely monitor signs of consumer weakness and maintain a moderate allocation to consumer staples to hedge against potential risks.

◆ Industrials and Materials Sector – Cyclical industries showing resilience. The industrial sector was initially expected to see a decline in profits in Q4, but it actually achieved slight positive growth (+2.7%, compared to an expectation of -3.3%), indicating that economic resilience exceeded expectations. Some industrial companies (such as those in aviation and manufacturing) experienced profit surprises due to cost control and improved demand. In the materials sector, year-on-year profit margins improved (10.2%, up from 8.3% last year), indicating alleviated pressures in the manufacturing chain. If the economy achieves a soft landing in the future and tariffs do not escalate, these cyclical stocks may have room for both valuation and performance increases. Currently, the valuations of the industrial and materials sectors are not high (forward P/E around 18 times), providing potential value recovery opportunities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。