Introduction

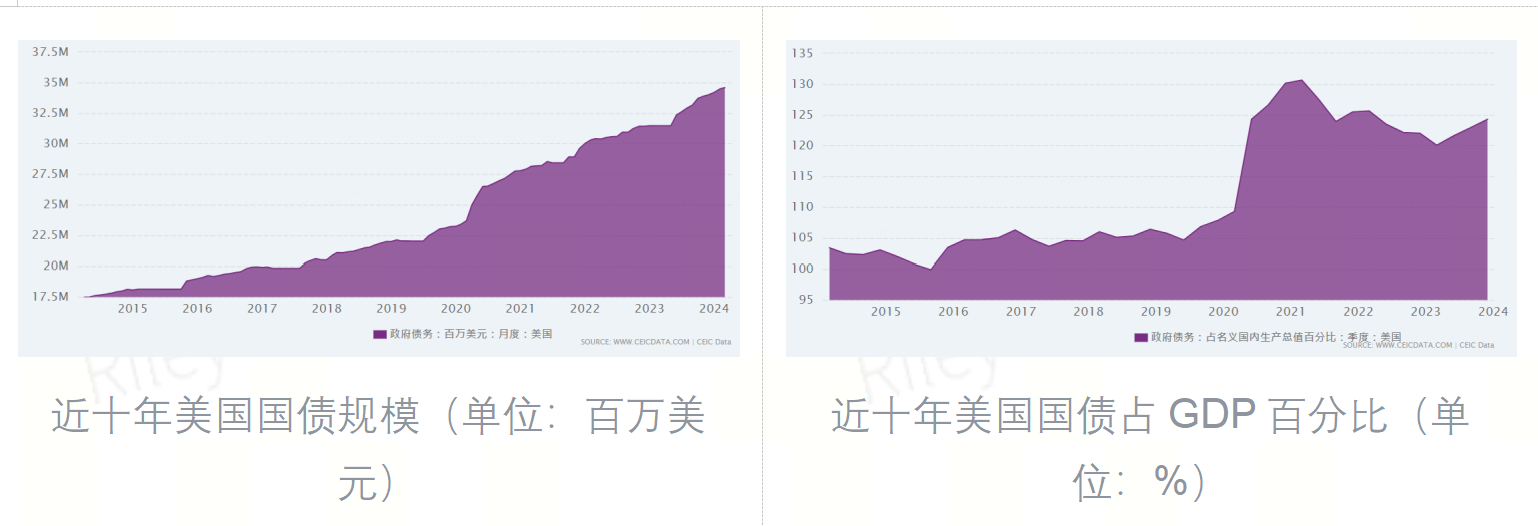

At the beginning of the new year, the scale of U.S. national debt has surpassed $36.4 trillion. How can the U.S. debt crisis be resolved, and can the international hegemony of the dollar continue? How will Bitcoin respond, and how will future international settlement units be replaced?

We will start by discussing the U.S. debt economic model, then explore the current debt risks facing the internationalization of the dollar, and analyze whether the repayment plans for U.S. debt are feasible. Looking at history, we will see where U.S. debt points Bitcoin.

Establishment of the U.S. Debt Economic Model

After the collapse of the Bretton Woods system, the hegemony of the dollar grew recklessly within the debt economic model.

Collapse of the Bretton Woods System: The Dollar Becomes a Fiat Currency

After World War II, the Bretton Woods system was established, linking the dollar to gold, with the International Monetary Fund (IMF) and the World Bank controlling the relevant rules, forming a dollar-centered international monetary system. However, the famous "Triffin Dilemma" accurately predicted the collapse of the Bretton Woods system: the demand for international settlements continued to grow, dollars flowed out of the U.S. and accumulated overseas, leading to a long-term trade deficit for the U.S.; while the dollar, as an international currency, needed to maintain value stability, which required the U.S. to have a long-term trade surplus. Coupled with the Vietnam War exacerbating the dual deficits, President Nixon announced in 1971 that the dollar would be detached from gold, transforming the dollar from a commodity currency into a fiat currency, with its value no longer guaranteed by precious metals but by the national credit of the U.S.

Establishment of the Debt Economic Model: Continuation of Dollar Hegemony

On this basis, the U.S. debt economic model was established: global trade is settled in dollars, and the U.S. must maintain a huge trade deficit to allow other countries to acquire large amounts of dollars; countries around the world purchase U.S. Treasury bonds to preserve and increase the value of their dollars, reinvesting in U.S. financial products, causing dollars to flow back into the U.S.

As a world currency, the dollar is a global public good and should maintain value stability. However, after abandoning the gold standard, U.S. monetary authorities gained the power to issue currency, allowing the U.S. to change the value of the dollar according to its own interests. The hegemony of the dollar has been strongly sustained through the debt economic model.

Risks Facing Dollar Internationalization

The dollar faces risks from the U.S. national debt economic model and commercial real estate debt.

Dollar Internationalization Contradicts Manufacturing Reshoring

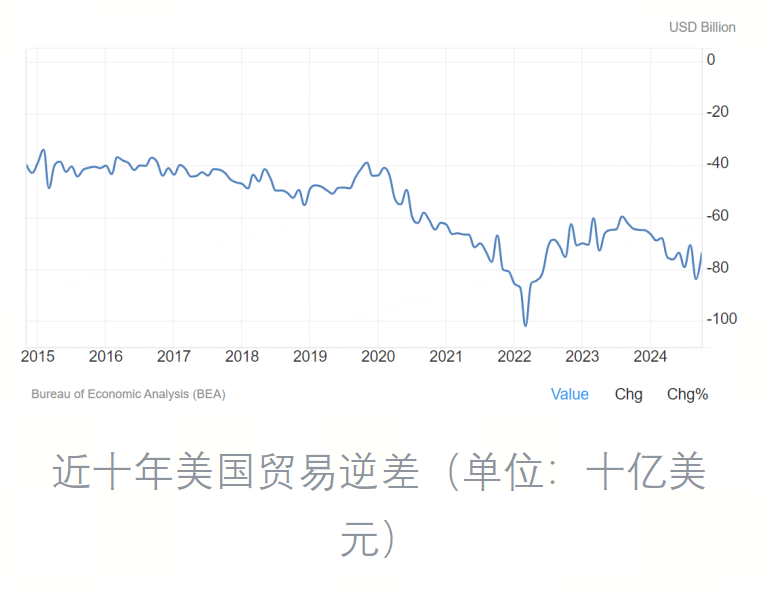

The U.S. debt economic model is an important support for dollar internationalization, but it is not sustainable. The Triffin Dilemma still exists. On one hand, dollar internationalization requires maintaining a long-term trade deficit, exporting dollars and accumulating them overseas. Once overseas investors become concerned about the repayment ability of U.S. Treasury bonds, they may turn to other alternatives and demand higher interest rates on U.S. Treasury bonds to balance future repayment risks, leading the U.S. into a vicious cycle of "dollar credit weakening - dollar-denominated commodity prices rising - inflation resilience strengthening - U.S. Treasury yields remaining high - U.S. interest burden increasing - U.S. debt repayment risk rising - dollar credit weakening."

On the other hand, the U.S. needs to promote manufacturing reshoring, which will reduce the trade deficit and lead to a supply-demand imbalance for dollars, causing a long-term significant appreciation. This will hinder the dollar's role as an international settlement currency. Although President Trump proposed reshoring manufacturing while also imposing high tariffs, which may benefit manufacturing reshoring in the short term, it will lead to inflation in the long run, indicating a conflict between the two.

The idea of wanting both dollar hegemony and manufacturing is unrealistic. Currently, the pressure for dollar appreciation is not yet clear, and it is expected that there will not be a fundamental change in the trade deficit in the short term, with depreciation pressure on the dollar prevailing.

Commercial Real Estate Debt Crisis

In addition to the risks associated with U.S. Treasury bonds, commercial real estate also faces debt risks.

According to a recent report from Moody's, due to the continued expansion of remote work, the vacancy rate for office buildings in the U.S. is expected to rise from 19.8% in the first quarter of this year to 24% by 2026. Compared to pre-pandemic levels, the demand for office space in the white-collar sector has decreased by about 14%. McKinsey predicts that by 2030, the demand for office space in major global cities will decline by 13%, and in the coming years, the market value of global office properties may shrink significantly by $800 billion to $1.3 trillion.

CICC research shows that as of the end of 2023, commercial real estate loans accounted for 26% of total loans in the U.S. banking system, while large banks' commercial real estate loans accounted for only 13%, and small and medium-sized banks accounted for as much as 44%. The U.S. has experienced waves of bank bankruptcies and restructurings due to real estate risks in the late 1980s and 2008, and the risks in U.S. commercial real estate remain after the pandemic, showing no signs of improvement. The $1.5 trillion in commercial real estate liabilities in the U.S. will mature next year, and if small and medium-sized banks face defaults, it could trigger a financial crisis.

Analysis of U.S. Debt Repayment Plans

How to break this vicious cycle mainly depends on how such a large scale of U.S. national debt should be repaid. Borrowing new debt to pay off old debt is similar to a "Ponzi scheme," and the dollar will eventually lose its credibility, thus losing its status as a world currency, which is clearly not feasible. We will analyze whether the following repayment plans are feasible.

Selling Gold to Repay U.S. Debt?

Analysis of the Federal Reserve's Assets

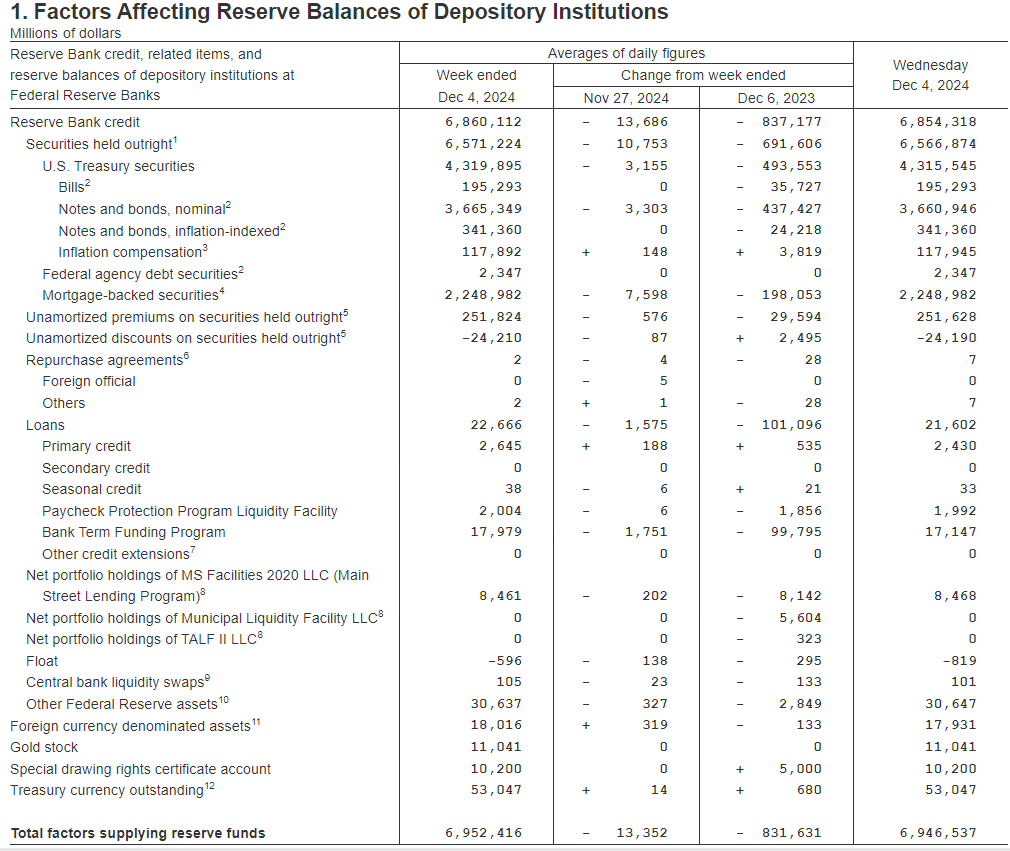

The following chart shows the details of the Federal Reserve's assets as of December 4.

Federal Reserve assets as of December 4 (in millions of dollars)

Source: Federal Reserve Balance Sheet: Factors Affecting Reserve Balances - H.4.1 - December 05, 2024

The main assets held by the Federal Reserve are bonds, including Treasury bonds and quasi-Treasury bonds, totaling about $6.57 trillion, accounting for approximately 94.45% of total assets.

The gold holdings amount to $11 billion, but this portion is calculated at prices after the collapse of the Bretton Woods system. Referring to the exchange rate at the time of the complete collapse of that system, 1 troy ounce of gold = $42.22, and based on the spot price of about $2700 per ounce on December 11, the value of this gold is approximately $704.358 billion. Therefore, the adjusted gold accounts for about 10% of total assets.

Liquidity Crisis of U.S. Debt

Therefore, some have proposed selling gold to repay U.S. debt. While it seems that the gold scale is large, it is actually not feasible. Gold is a universally accepted currency based on international consensus, playing a key role in stabilizing currencies and responding to economic crises. The large gold reserves give the U.S. significant influence in the international financial market, making its position very important. If the Federal Reserve sells gold, it would indicate that the Fed has completely lost trust in U.S. debt, seemingly "having no way out," and would rather weaken its own influence to fill the "black hole" of U.S. debt, which would undoubtedly create a liquidity crisis for U.S. debt, amounting to self-sabotage.

Selling BTC to Repay U.S. Debt?

Recognition Issues of Bitcoin Checks

Trump once said, "Give them a little cryptocurrency check. Give them a bit of Bitcoin, and then wipe out our $35 trillion." Although BTC serves a role similar to a store of value in cryptocurrencies, it still has greater value volatility compared to traditional fiat currencies, and whether the check can be cashed at the recognized value remains to be seen, as U.S. debt holders may not necessarily recognize it. Furthermore, the economies holding U.S. debt may not implement Bitcoin-friendly policies, such as China, which may not accept Bitcoin checks due to internal regulatory issues.

Insufficient Bitcoin Reserves to Repay

Secondly, the amount of Bitcoin held by the U.S. is insufficient to resolve the debt crisis. Current data shows that, according to Arkham Intelligence's data from July 29, the U.S. government holds $12 billion in Bitcoin, which is merely an ant's leg compared to the $36 trillion in U.S. debt. Some speculate whether the U.S. could manipulate Bitcoin prices. This is unrealistic; extracting money is a concern for speculators, and the U.S., facing the terrifying $36 trillion debt, cannot solve the problem with $12 billion even if it manipulates Bitcoin prices.

In the future, it is possible for the U.S. to establish Bitcoin reserves, but it cannot solve the debt problem. Senator Cynthia Lummis has proposed that the U.S. establish a reserve of 1 million Bitcoins, but this plan remains controversial.

Firstly, establishing Bitcoin reserves would weaken global confidence in the dollar, and the world would see this as a signal of imminent collapse of U.S. debt risk, potentially causing interest rates to soar and triggering a financial crisis.

Secondly, the U.S. is currently negotiating whether to implement Bitcoin reserves through legal or executive orders. If Trump were to use an executive order to force the purchase of Bitcoin, it could be interrupted due to public dissent. The American public does not have a profound understanding of the potential dollar crisis, and if the Trump administration were to acquire a large amount of Bitcoin through executive means, it might face public questioning: "Wouldn't this expenditure be better used elsewhere?" or even, "Is it necessary to spend so much money on Bitcoin?" Legislative measures would face even more daunting challenges.

Thirdly, even if the U.S. successfully establishes Bitcoin reserves, it would only slightly delay the debt collapse. Proponents of using Bitcoin reserves to repay U.S. debt cite conclusions from asset management company VanEck: establishing a reserve of 1 million Bitcoins could reduce U.S. national debt by 35% over the next 24 years. This assumes that Bitcoin will grow at a 25% compound annual growth rate (CAGR) to $42.3 million by 2049, while U.S. national debt will grow at a 5% CAGR from $37 trillion at the beginning of 2025 to $119.3 trillion during the same period. However, we can convert the remaining 65% of the debt into a specific amount, indicating that by 2049, the U.S. national debt will still have approximately $77.3 trillion that cannot be resolved with Bitcoin. How will this huge gap be filled?

Dollar and BTC Pegging?

Another bold idea is that if Trump continuously releases positive news to boost Bitcoin prices, and then uses other methods to facilitate transactions between countries and the U.S. using Bitcoin for settlement, it could decouple the dollar from national credit and link it to Bitcoin. Could this solve the massive U.S. debt problem?

"New Bretton Woods System"

Linking to Bitcoin is akin to a return to the Bretton Woods system, similar to the dollar's link to gold. Supporters argue that the similarity between Bitcoin and gold lies in: rising mining costs with increased supply, limited supply, and decentralization (de-sovereignization).

The cost of gold mining increases as the shallower surface gold is extracted, similar to the rising difficulty of Bitcoin mining. Both have a supply limit and can serve as good stores of value. They both exhibit characteristics of decentralization. Modern fiat currencies are enforced by sovereign states, while gold naturally becomes a currency that no single country can control. Due to the global and relatively stable distribution of gold supply and demand across various regions and industries, gold priced in different currencies has a very low correlation with local risk assets. Bitcoin, due to its decentralized operation, can avoid the regulation of sovereign governments.

Threat to Dollar Internationalization

The unreasonable aspect is that pegging the dollar to BTC would threaten the internationalization of the dollar.

Firstly, if the dollar is pegged to Bitcoin, it would mean that any group or individual has the right to issue their own currency using Bitcoin. This is reminiscent of the free banking era from 1837 to 1866, before the establishment of the Federal Reserve, where the right to issue currency was unrestricted, leading to the prevalence of "wildcat banks"—various states, cities, private banks, railroads, construction companies, stores, restaurants, churches, and individuals issued about 8,000 different currencies by 1860, often located in remote areas where wildcats outnumbered people, earning the nickname "wildcat banks" due to their extremely low viability.

Today, Bitcoin's decentralized nature means that if the dollar were to be pegged to Bitcoin, it would significantly weaken the international status of the dollar. The interests of the United States require the defense of the dollar's internationalization and the promotion of dollar hegemony, which would not be counterproductive, and thus there would be no push for a dollar-BTC peg.

Secondly, Bitcoin is highly volatile. If the dollar were pegged to Bitcoin, the real-time transmission of international liquidity could amplify the volatility of the dollar, affecting the international community's confidence in the dollar's stability.

Thirdly, the amount of Bitcoin held by the U.S. is limited. If the dollar needs to be pegged to Bitcoin and the U.S. does not hold enough Bitcoin reserves, it would lead to constraints on its monetary policy.

Manipulating the Dollar through BTC?

There is also a viewpoint suggesting that if Bitcoin is the future "digital gold," could the U.S. manipulate Bitcoin like it does gold to control the dollar?

Reviewing How the U.S. Manipulated the Dollar through Gold

After the 1976 Jamaica Agreement, the interests of large investment banks, governments, and central banks aligned. Fiat currencies are based on confidence; if gold prices rise too quickly, it undermines confidence in the currency, making it difficult for central banks to control liquidity and inflation targets.

Thus, the U.S. suppressed gold prices to encourage capital to hold dollars, thereby boosting the dollar. Conversely, it could raise gold prices to induce dollar depreciation.

If the U.S. were to manipulate Bitcoin prices, could it control the dollar? The answer is no.

Unrealistic to Manipulate the Dollar through BTC

Firstly, Bitcoin operates on a decentralized network, and no single entity, including the U.S. government, can manipulate prices like it can with gold.

Secondly, Bitcoin captures global liquidity and is influenced by a complex array of international factors. Even if the U.S. government wanted to manipulate Bitcoin prices, the effectiveness would be significantly diminished.

Finally, even if the U.S. could manipulate Bitcoin prices, lowering Bitcoin prices would not necessarily lead to liquidity flowing into dollars. Bitcoin holders generally have a higher risk appetite compared to traditional dollar holders and may turn to other high-risk assets. It is important to note that both the dollar and gold belong to the category of high liquidity, low-risk assets, with overlapping safe-haven attributes and similar recognition, thus exhibiting a clear substitution effect, while there are still distinctions between Bitcoin and the dollar.

Killing the Creditors: Japan and the Jewish Consortium?

Continued U.S.-Japan Cooperation

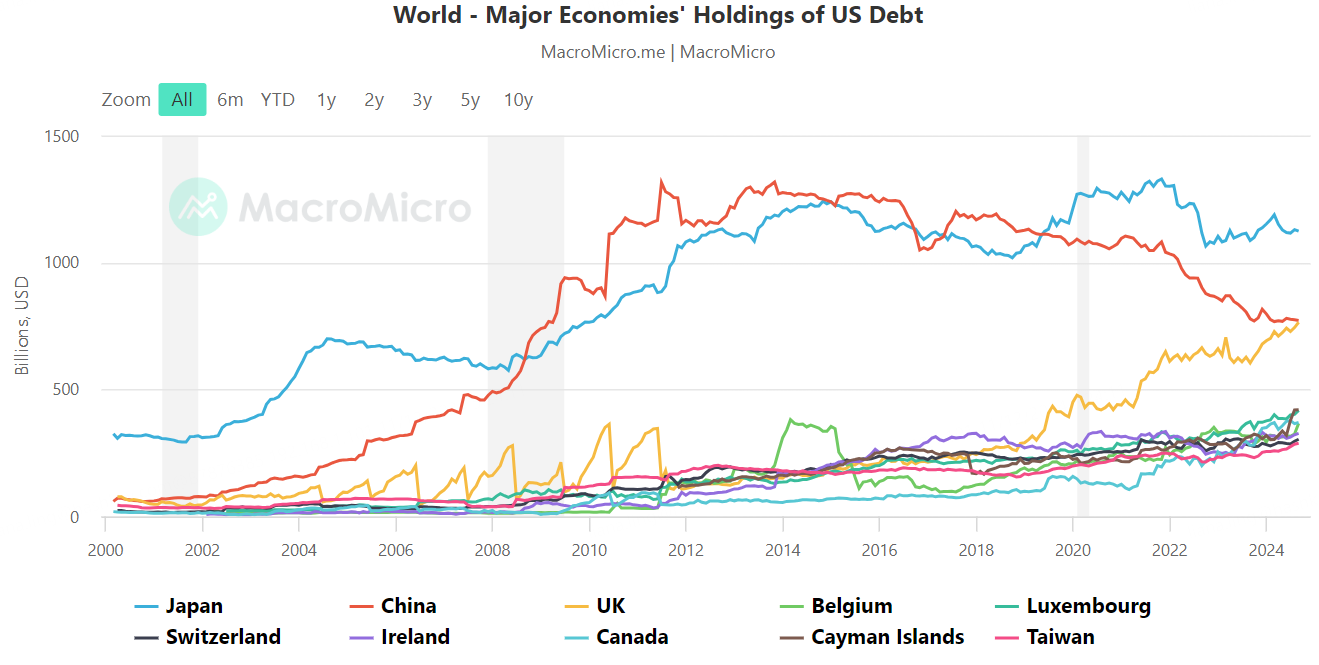

Some suggest that an alternative plan is to "kill" the creditor Japan, as Japan is the largest holder of U.S. Treasury bonds. This is impossible in the short term.

The Ishiba Cabinet needs to restore trust due to issues with black money and is constrained by the opposition parties. Therefore, overall, it has turned pragmatic, seeking to maintain vested interests through strategic ties with the U.S.

The U.S. is burdened by the Ukraine crisis and turmoil in the Middle East, thus requiring Japan to play the role of "deputy police chief" in the alliance system, sharing the strategic burden in the Asia-Pacific direction.

Therefore, the overall cooperation between the U.S. and Japan in the field of economic security will continue, and the U.S. will not be in a hurry to eliminate Japan.

Jewish Consortium Should Not Be Challenged

In addition to state holders, the Jewish consortium plays an important role on Wall Street. About 80% of the debt is held by domestic investors and financial institutions in the U.S., such as pension funds, mutual funds, and insurance companies. Most shareholders of these financial institutions are Jewish, referred to as the Jewish consortium. Some believe that the Federal Reserve may leverage the growing public discontent towards the "rich" to partially blame the economic crisis on the Jewish consortium. We believe this approach is too costly and not easily achievable.

Attacking the Jewish consortium would impact economic stability, potentially leading to rising unemployment, stagnation in innovation, and a decline in investor confidence and international competitiveness. This is a self-destructive act, especially as the debt crisis approaches; such actions would only accelerate economic collapse.

Furthermore, the Jewish consortium has strengthened its political influence over the years. For example, the Biden administration has a high proportion of Jewish members, and the core members of the cabinet have remained particularly stable during his tenure, unlike in other government periods, possibly indicating that the Jewish consortium intends to step out from behind the scenes to seize power. In the future, it can be anticipated that the Jewish consortium will actively engage in political power to counter the U.S. government, making it not easy to target the Jewish consortium.

Impact of Debt Crisis on International Settlement Units

Therefore, we will see that the inability to repay U.S. debt and increased tariffs on goods will lead to imported inflation. If this interacts with the U.S. commercial real estate debt crisis, the effects will compound, and inflation will rise rapidly. A financial crisis is imminent; Bitcoin may experience a short-term decline alongside the financial market but will rise in the long term.

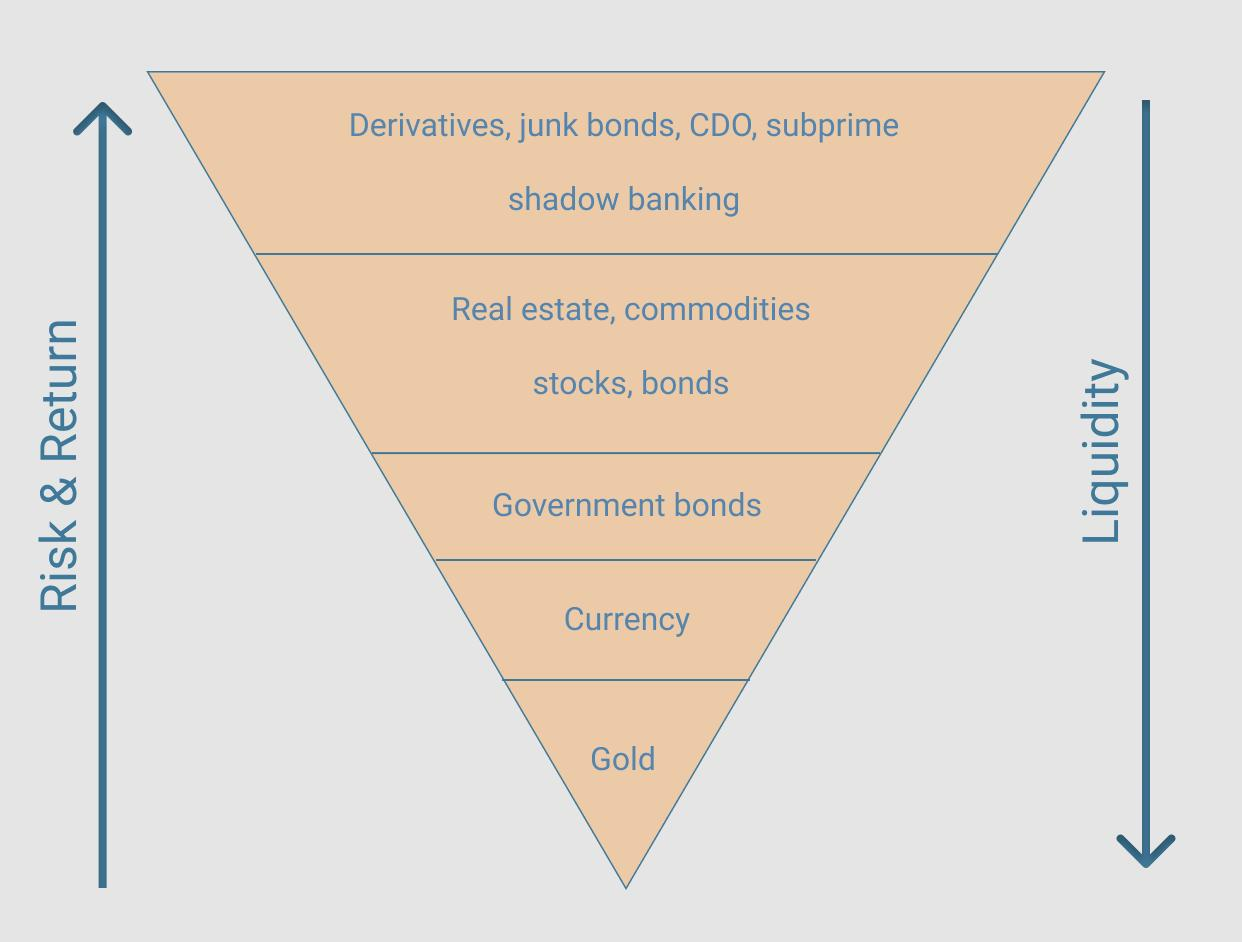

Short-term Decline of Bitcoin

In the Exter’s Pyramid proposed by the late Vice President of the New York Federal Reserve, John Exter, Bitcoin is currently closer to the top of the pyramid as a leveraged product rather than a safe-haven asset at the bottom; it is a high-risk asset, and if a financial crisis erupts, short-term investment demand will decrease.

Bitcoin as Noah's Ark

In the long run, Bitcoin will become Noah's Ark in a financial crisis, likely becoming an important pillar of the future international settlement system.

Firstly, Bitcoin is a strictly scarce liquid asset. In the face of significant dollar depreciation, Bitcoin can maintain its scarcity and has broad applicability globally, making people more willing to hold it as a long-term store of value. In other words, Bitcoin will be closer to the bottom of Exter’s Pyramid, highlighting its safe-haven attributes. Despite being affected by short-term market sentiment, the precious nature of Bitcoin as a store of value will still be recognized by the market.

Secondly, the behavior of investors and consumers will also change after the crisis. The collapse of U.S. debt will be an epic shock, leaving devastation in its wake. Trust in financial institutions and sovereign states/governments and monetary authorities will be shattered and rebuilt. Bitcoin, as a relatively independent asset not controlled by states/governments, will become the top choice for future investments.

Therefore, given that the debt economic model is unsustainable, the collapse of U.S. debt is only a matter of time, and the internationalization of the dollar will be severely impacted, the world will witness another wave of Bitcoin adoption.

Will Bitcoin Become Tomorrow's International Currency?

Once the dollar system collapses, what will take over the baton from the dollar and become the next generation of international settlement currency?

Looking back at the history of currency, the three main elements of currency are a measure of value, a medium of exchange, and a store of value. Among these, the most important is the function of a medium of exchange. In this regard, Bitcoin can operate around the clock, without geographical limitations, and can avoid sovereign state transactions, capturing global liquidity and completing transactions more effectively than traditional finance. In terms of value measurement, the application scenarios of Bitcoin are continuously expanding, effectively measuring the value of many goods and services. In terms of the store of value function, as Bitcoin mining progresses, the marginal supply decreases, further strengthening its store of value function.

Is there a possibility for other fiat currencies to replace the dollar as the international settlement currency? Currently, there are no other fiat currencies that can rival the dollar. Moreover, after the outbreak of the U.S. debt crisis and the explosive destruction of the dollar system, it is believed that people will have more doubts about traditional financial markets. If there were truly a free currency, could it lead humanity towards true freedom and genuine decentralization, avoiding the impacts of traditional sovereignty on the economy?

Some may argue that there are cryptocurrencies that are technically more advanced than Bitcoin and can facilitate smooth transactions; why can't other cryptocurrencies become international settlement units? This is because value is based on consensus. Among cryptocurrencies, Bitcoin achieves the highest level of consensus, with the greatest recognition, the widest acceptance, and the strongest influence.

Therefore, in summary, Bitcoin already possesses the potential to become the next generation of international settlement unit; it just depends on whether the times will grant it the opportunity.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。