Prediction markets are being given a higher profile, seen as "truth engines."

Author: michaellwy

Compiled by: Deep Tide TechFlow

The potential of prediction markets has been widely recognized, but some key issues remain unresolved. This article will reveal the challenges currently faced by prediction markets by analyzing recent controversial events, particularly the dilemmas in dispute resolution. For developers, this presents a huge opportunity: prediction markets are still in the early stages of development, and whoever can solve these core issues may lead the next wave of innovation.

Introduction

Prediction markets are tools that aggregate information using financial incentive mechanisms. By allowing traders to bet their judgments with funds, prediction markets can drive prices to gradually reflect the probabilities of collective wisdom. When this mechanism operates normally, prediction markets often yield more accurate predictions than traditional methods.

The advantages of prediction markets were fully demonstrated in the predictions for the 2024 U.S. presidential election. Among them, the Polymarket platform proved to be more reliable than traditional polls, successfully predicting Trump's victory.

As Polymarket gained credibility, mainstream media began to accept it as a data source. Media outlets that have long been skeptical of crypto projects, such as Bloomberg, not only cited its odds in their reports but also included its prediction data in search engine results like Perplexity, with traditional media increasingly referencing its predictions.

Ethereum founder Vitalik also expressed support for prediction markets, stating that they are becoming "two major social cognition technologies of the 2020s."

However, despite the immense potential of prediction markets, their decentralized "truth verification" mechanisms still face many challenges. Recently, the controversial market on Polymarket regarding "Will the U.S. government shut down?" exposed key flaws in system design, providing important insights for decentralized dispute resolution.

This article will analyze this controversy in detail, exploring the design flaws in prediction markets' dispute resolution mechanisms and proposing improvements.

How Does Polymarket Work?

Polymarket operates similarly to traditional exchanges, but users are not trading assets; they are trading probabilities. For example, in the market for “Will Bitcoin reach $100,000 in 2024?”, traders can buy or sell positions between 0% and 100% through the system.

Suppose you believe Bitcoin will reach $100,000 in 2024 and purchase $100 worth of "yes" tokens at $0.47. If your prediction is correct, you will receive $212 (calculated as 100/0.47), which is the inverse of your purchase price. This dynamic trading mechanism allows market participants to adjust their positions based on the latest information, providing real-time collective predictive insights.

Polymarket's trading mechanism is based on the Conditional Token Framework. Here’s a specific example:

Suppose the total funds in the Bitcoin prediction market are $1,000:

Alice believes Bitcoin will reach $100,000 and buys $200 worth of "yes" tokens at $0.20;

Bob believes it will not reach that price and buys $800 worth of "no" tokens at $0.80;

The system matches these two orders since they total $1,000 (i.e., 100%);

The system receives 1,000 USDC and creates 1,000 pairs of "yes/no" tokens:

Alice receives 1,000 "yes" tokens (at $0.20 each);

Bob receives 1,000 "no" tokens (at $0.80 each).

By the end of 2024, the winner can redeem each token for $1:

If Bitcoin reaches $100,000, Alice's $200 will turn into $1,000 (5x return), while Bob's tokens will lose value;

If it does not reach that price, the situation reverses, and Bob profits while Alice's tokens become worthless.

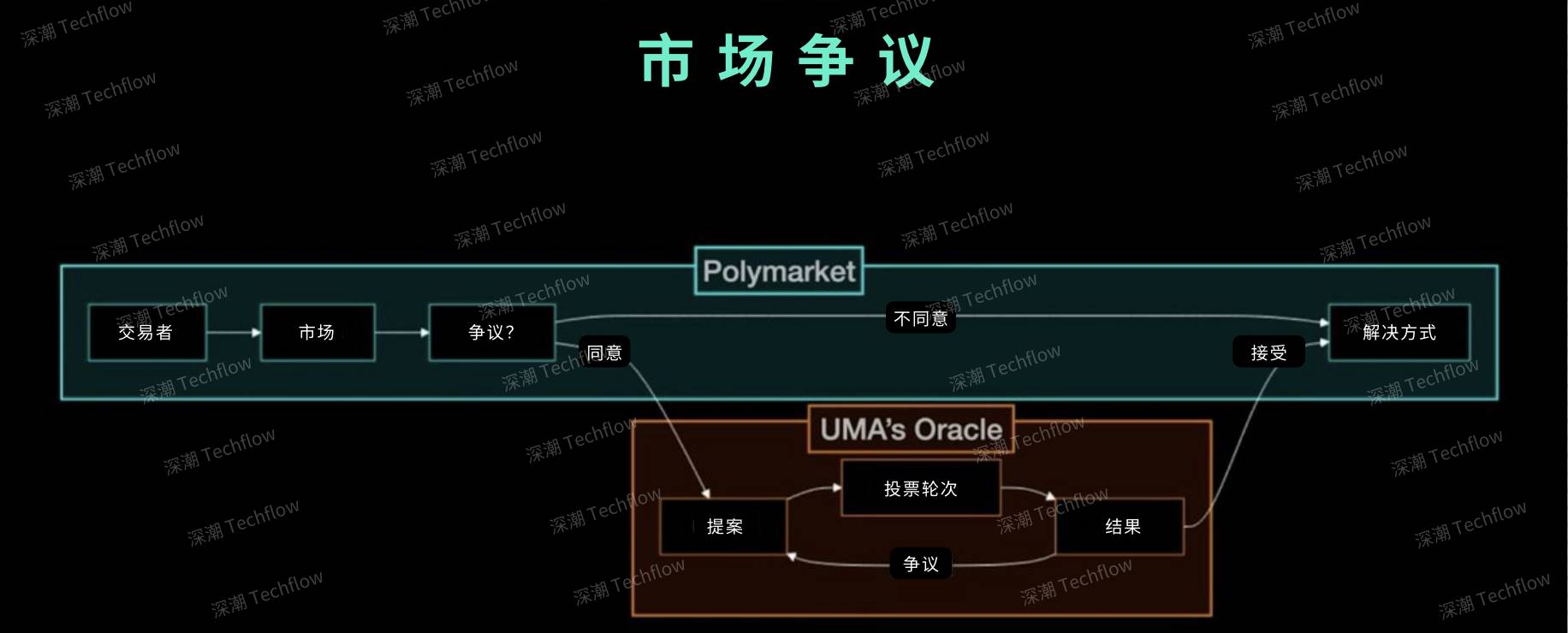

On the Polymarket platform, all transactions are automatically completed through the Polygon network, and the market's results are determined by social consensus. If there is a dispute over the market outcome, the UMA protocol (a system based on optimistic oracles) intervenes to help verify and ultimately adjudicate the market results.

The operation of the UMA protocol is as follows:

When there is a dispute over the market outcome, any user can trigger a vote;

Holders of UMA tokens will vote on the outcome;

Voting weight is proportional to the number of UMA tokens held;

The winner of the vote will receive rewards, while the losers will face penalties.

The original image is from michaellwy, compiled by Deep Tide TechFlow

A detailed explanation of this mechanism can be found in UMA's official video. Additionally, reports from ASXN and Shoal Research provide a more comprehensive analysis of how UMA works.

The Controversy of the U.S. Government Shutdown Case

Prediction markets have demonstrated strong capabilities in predicting event outcomes, and their success in the 2024 U.S. election has further enhanced their credibility.

However, what happens when the system of prediction markets encounters problems? The recent market controversy surrounding whether the U.S. government would shut down revealed some key flaws in the current design of prediction markets.

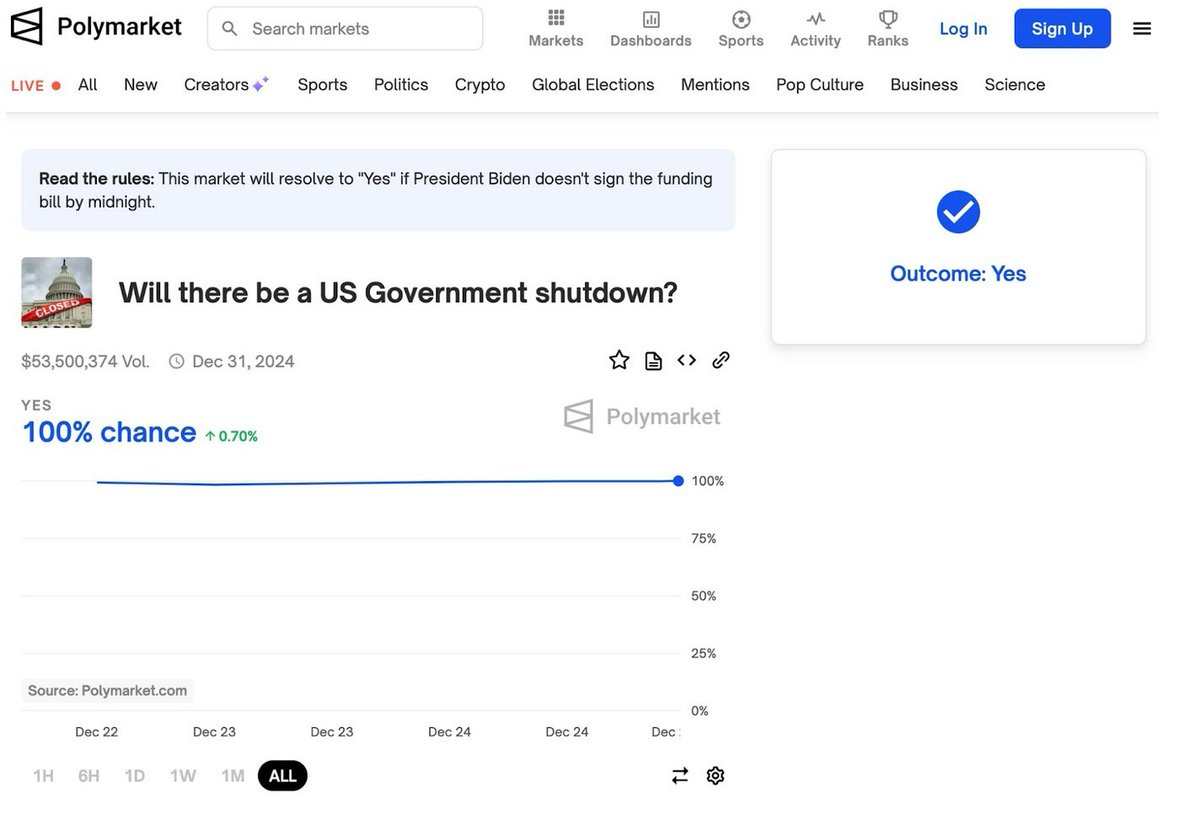

Polymarket created a market to predict whether the U.S. government would shut down between August 30 and December 31, 2024. Initially, the design of this market seemed quite straightforward. However, despite President Biden signing a funding bill (H.R. 10545 "U.S. Relief Act"), successfully avoiding a government shutdown, and major media outlets confirming unanimously across political lines that there was no interruption of federal government services, the market still showed a 99% probability of a shutdown as the trading deadline approached, ultimately ruling the outcome as "yes."

The controversy over this outcome primarily stemmed from Polymarket's modification of the rules during the market's operation. Specifically, the platform added a new "rule clarification" after a significant amount of trading had occurred, introducing a previously non-existent cutoff date—midnight on December 20, 2024. This change directly led to a disconnect between the market outcome and the actual situation.

What should have been a simple binary prediction market turned into a debate about manipulation and design flaws in prediction markets due to the temporary adjustment of rules.

Timeline of Events

- 6 PM on December 20 (EST): The probability of the "yes" option (i.e., predicting the government would shut down) was 20%, having dropped from 70% to this level. This change occurred as traders generally expected the Senate to pass the H.R. 10545 bill to avoid a shutdown.

Polymarket's official tweet: The probability of a government shutdown has dropped to just 20%. The funding bill is about to pass.

- Later that day: Polymarket added a banner to the market user interface stating that if Biden failed to sign the bill before midnight, the market would interpret it as "yes." Subsequently, the probability of the "yes" option skyrocketed to 98%, as traders bet that the Senate would not pass the bill in time for Biden to sign.

- If President Biden does not sign the funding bill before midnight, the market will interpret it as "yes."

Market Comment Section Reaction: The comment section erupted in intense debate. Holders of the "no" option were confused by the sudden spike in probability and pointed out that all news sources reported the Senate was about to pass the bill to avoid a government shutdown.

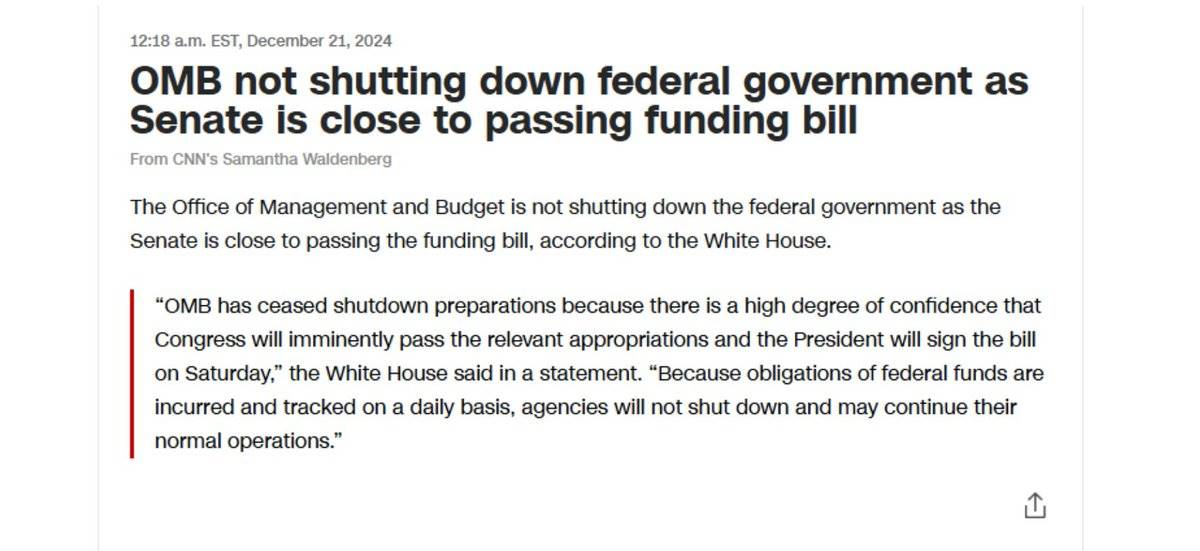

December 21, 00:38: The Senate successfully passed the funding bill.

December 21 Morning: Biden officially signed the bill into law, with major media outlets unanimously reporting that the government shutdown had been successfully avoided.

CNN Report Content:

The Senate is close to passing the funding bill, and the OMB will not shut down the federal government.

According to the White House, the Office of Management and Budget (OMB) will not shut down the federal government as the Senate is close to passing the funding bill.

The White House stated, "As Congress is about to pass the relevant appropriations bill and the President will sign it on Saturday, the OMB has stopped shutdown preparations."

"Since federal funding obligations accrue and are tracked daily, agencies will not shut down and can continue normal operations."

Why did the market interpret it as "yes" when there was actually no government shutdown?

Despite the government not actually shutting down, the market ultimately interpreted it as "yes." To understand this outcome, we need to carefully analyze the original rules of the market.

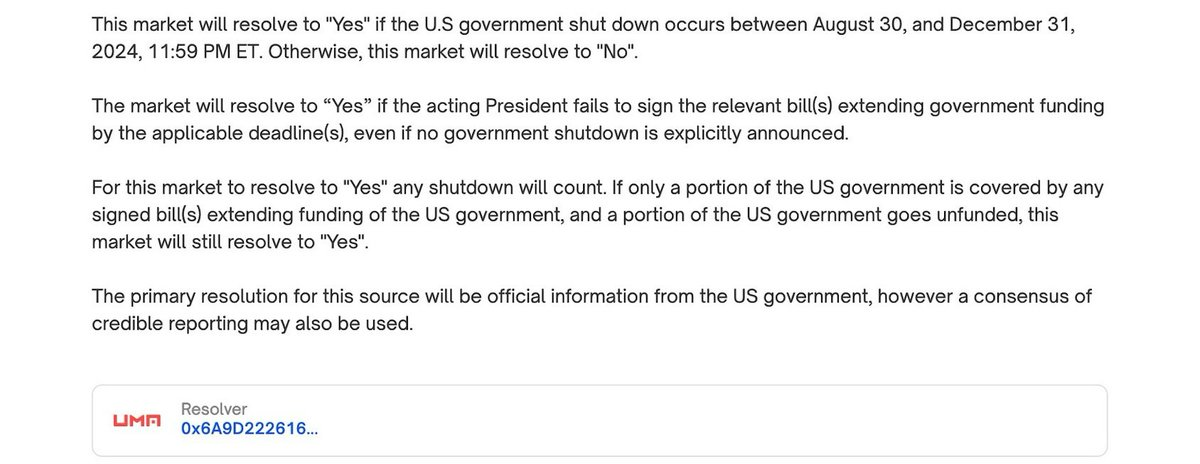

Content in the image:

If the U.S. government shuts down between 11:59 PM (Eastern Time) on August 30, 2024, and December 31, 2024, the result of this market will be determined as "yes." Otherwise, the result will be determined as "no."

If the acting President fails to sign the relevant bill to extend government funding before the applicable cutoff date, even if there is no explicit announcement of a government shutdown, the result of this market will still be determined as "yes."

Regardless of the form of shutdown that occurs, this market will determine it as "yes." For example, if only some U.S. government departments receive support from the extended funding bill while others fail to secure funding, this market will still determine it as "yes."

The primary basis for this market's determination will be official information from the U.S. government, but credible media reports may also be referenced when necessary.

Market Rule Analysis:

Point 1 – This point is relatively simple: observe whether a government shutdown occurs within the specified time frame (note that the end date of the time frame is December 31, 2024).

Point 2 – This is the core of the controversy. Holders of "yes" believe that according to the market rules, the President must sign the relevant bill before the applicable cutoff date. They argue that midnight on December 20 is the applicable cutoff date, and since it was not signed before this time, the market result should be determined as "yes" (we will discuss this further later).

Point 3 – This involves situations where some government departments shut down, but it is not closely related to the current issue, so we will not delve into it here.

Point 4 – It clarifies that the primary basis for the market result will be official information released by the U.S. government, while credible media reports may also be referenced.

Views of the "Yes" Camp:

Polymarket added a banner clearly stating that midnight on December 20 is the cutoff date.

The platform released "additional background information" on December 21, further supporting this rule.

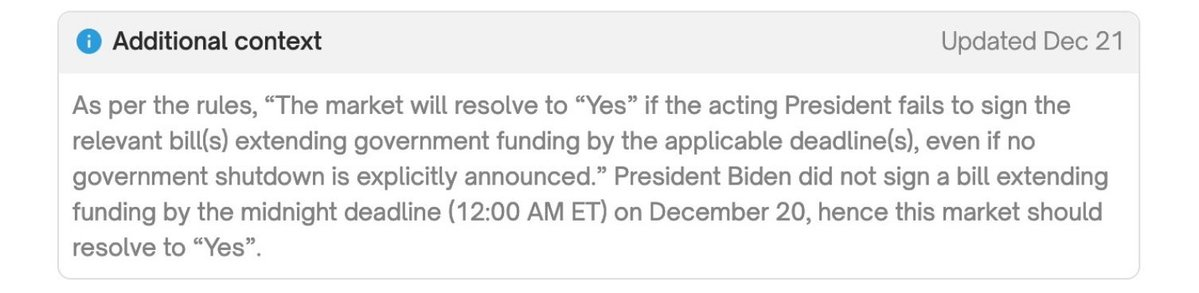

Additional Background

According to the rules, "If the acting President fails to sign the relevant bill to extend government funding before the applicable cutoff time (12:00 AM Eastern Time on December 20), even if there is no explicit announcement of a government shutdown, the market will interpret it as 'yes.'"

Since President Biden failed to sign the funding extension bill before midnight on December 20, the market should be interpreted as "yes."

Because Biden failed to sign the bill before midnight, the market should automatically interpret it as "yes" according to the rules.

They believe the rules are binding, even if a government shutdown did not actually occur.

Views of the "No" Camp:

Timing Issue:

The scope of the original market rules is from August 2024 to December 31. The "yes" camp emphasizes that the midnight cutoff on December 20 is not explicitly written in the rules, only mentioning "the applicable cutoff date."

Federal government funding operates on a daily basis, so the actual cutoff date should be 11:59 PM on December 21.

The banner stating "midnight cutoff" was still visible on December 21, which is illogical since the interpretation standard had already expired.

Actual Situation:

The White House Deputy Press Secretary previously confirmed: "Due to confidence in the bill's imminent passage, the OMB has stopped preparations."

According to conventional logic, missing the cutoff should lead to a shutdown. But since no shutdown occurred, it indicates that no critical cutoff was missed.

Finally, a separate Polymarket question about "Will the House and Senate pass the funding bill by midnight?" was correctly ruled as "no." The key point here is that missing a procedural cutoff does not equate to a government shutdown, which conflates process with outcome. This is also why there are two separate pages, as the spirit of the markets is different.

The core tension here is not just about interpretation issues but whether prediction markets should prioritize the interpretation of technical rules over the real-world outcomes they are supposed to predict. When the market rules a government shutdown that objectively never occurred as "yes," the mechanism for seeking truth is flawed.

Similar Controversies Are Not Uncommon

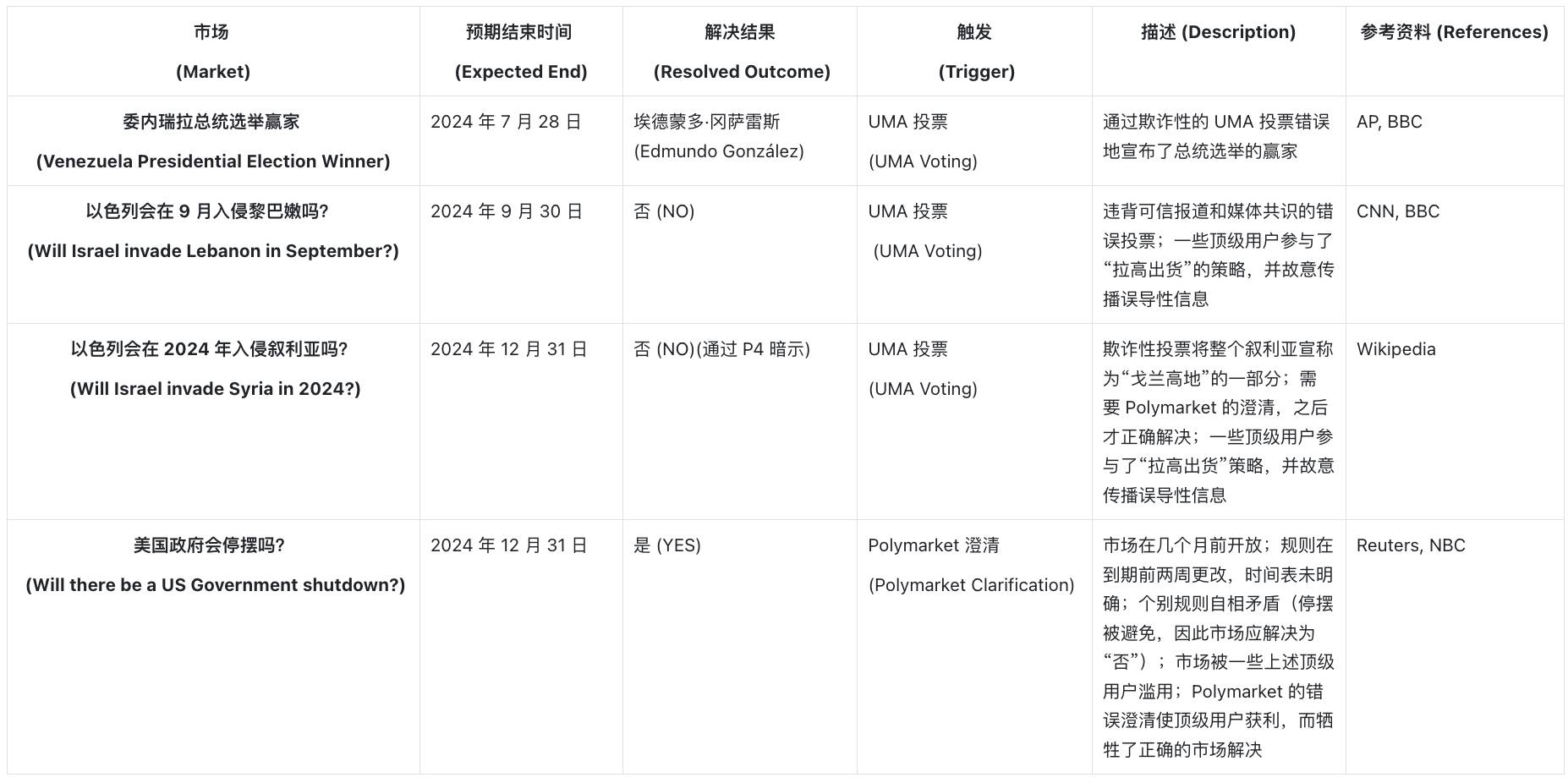

One might think this is just an isolated incident due to poorly written rules. However, similar controversies are not rare. A watchdog site called Polymarketfraud (forgive the provocative name) records many cases where market rulings contradict reality.

The market for the Venezuelan Presidential election winner is particularly interesting. Currently, the President of Venezuela is Nicolas Maduro, but the market ruled that opposition candidate Edmundo Gonzalez won in the recent election.

Frank Muci delves deeper into this in his article. Here’s a brief summary.

The market rules clearly state: "The primary basis for resolving disputes is official information from Venezuela, but if credible media reports reach a consensus, they may also be referenced."

Official election results show Maduro winning:

First announcement: 51.20000% to 42.20000%

- Second announcement: 51.9500% to 43.1800% (this level of precision, especially with multiple zeros, raises doubts about its authenticity and may indicate data manipulation).

However, according to polling station data, the opposition's vote share showed they were leading by over 20%.

UMA token holders (who have final adjudication power in resolving disputes) were strongly lobbied to ignore Venezuela's official information sources and instead accept credible media reports about electoral fraud.

Ultimately, UMA holders voted to overturn the primary basis stated in Polymarket's rules, ruling Gonzalez the winner—despite Maduro remaining in power.

This decision-making process's contradictions expose the problem. In the U.S. government shutdown case, UMA voters strictly adhered to a technical rule (the later added clause about the midnight cutoff), ignoring the media consensus reporting that "no government shutdown occurred." However, in the Venezuelan election case, they took the completely opposite approach, overturning the primary information source in favor of media consensus reports about electoral fraud.

Fraudulent Markets

(Source)

This list is still expanding, and research on other markets is ongoing. It is reasonable to speculate that in all the aforementioned markets, countless (new) users lost significant amounts of money, while some top users made substantial profits on their costs. Although there is currently no conclusive evidence, there are reasons to suspect that these accounts may have coordinated behavior in the UMA voting process and/or had insider information during the Polymarket clarifications.

Additionally, it can be further pointed out that there are suspicions of intentional misleading regarding the rules for "Will there be a US Government shutdown?" and that it is not clearly stated which cutoff dates are valid for market resolutions. However, all signs indicate that the market should resolve as "yes" (YES), for example, if a government shutdown event indeed occurs before 2025.

Polymarket should consider refunding users affected by these fraudulent markets and/or adopting a 50/50 solution where applicable. If no action is taken, this controversial market trend will continue, leading to profits for a small number of large users while a large number of new users suffer losses. This may be a matter that the U.S. Commodity Futures Trading Commission (CFTC) and/or the Federal Bureau of Investigation (FBI) should pay attention to and investigate as soon as possible.

Another case involves the Israel-Hezbollah Ceasefire Market. Despite reliable reports that military actions are still ongoing, the market still determined the outcome as "yes." A video titled Game Prediction Markets: Lessons Worth $40 Million on YouTube details this event.

Furthermore, Lou Kerner proposed an interesting theory in his article, exploring potential issues in the U.S. election market. Although he refers to it as a "conspiracy theory," his analysis suggests that Polymarket's presidential election market may structurally favor Trump.

The scenario he envisions is as follows: if Trump loses, he may refuse to concede defeat as he did in 2020, claiming voter fraud and contesting the election results. Therefore, even if Kamala Harris actually wins the election, the market may not determine the outcome in her favor.

This situation creates a "win for me if I win, and I don't lose if I lose" scenario for Trump's supporters. If Trump wins, bettors will profit directly; if he loses but contests the results, the market resolution may be delayed or changed due to UMA token holders' voting.

Issues Arising

First is the issue of rule manipulation. When the platform can arbitrarily add clarifications, the role of the oracle becomes meaningless. In the government shutdown case, the posting of a new banner caused market odds to rapidly spike to "yes," changing the originally effective cutoff date from December 31 to December 20, 2024.

This also raises other questions about resolution standards. When rules conflict, which rule should take precedence? Although the primary resolution standard clearly specifies news sources and credible reports and sets the cutoff date as December 31, the market ultimately made its resolution based on the later added clarification of midnight on December 20. This inconsistency in rule prioritization severely undermines the market's credibility.

Another structural challenge lies in the relationship between UMA holders and the Polymarket resolution system. Since UMA token holders can both trade and vote, this creates a strong conflict of interest between large traders and oracle voters.

While Polymarket and UMA should function as independent systems to check and balance each other, in reality, UMA is the only oracle provider for Polymarket. This reminds me of a scene in the movie The Big Short, where a ratings agency employee admits they must give a AAA rating, or else the banks will turn to competitors. When the success of a system relies on pleasing powerful participants, independence is out of the question.

Dispute Resolution: The Fatal Weakness of Prediction Markets

The core value of prediction markets lies in their ability to accurately adjudicate facts. Even with the most sophisticated user interface (UI), complex trading systems, and ample liquidity, if they cannot reliably determine who won the bet, all of it becomes meaningless. Polymarket currently relies on UMA's oracle system to resolve disputes, but the operational mechanism of this system may have potential vulnerabilities.

Overview of UMA's Basic Mechanism:

When there is a dispute over market results, any user can trigger the voting process.

UMA token holders vote on the outcome according to the rules.

The size of the voting power depends on the number of UMA tokens held by the user.

The winning voters receive rewards, while the losing voters face penalties.

In the blog Dirt Roads, Luca Prosperi proposed a concept called "Corruption Value Multiple (CVM)" to measure the potential risks of the market. Here is his analysis:

Currently, the total value of unresolved bets on Polymarket is about $300 million, while the total market cap of UMA is only $220 million.

Controlling half of the UMA tokens requires about $110 million.

This means that for every $1 spent to control UMA, it could potentially influence bets worth $1.36.

However, the actual risk may be higher for several reasons:

The actual voting rate of UMA tokens is usually only 20%, far below 100%.

Market rules are often vague, leaving gray areas for dispute resolution.

Voters may be influenced by public opinion or stakeholders.

The funds required to influence market outcomes may be far less than the theoretically calculated $110 million.

This means that if traders believe they can manipulate the oracle's adjudication to influence outcomes, they may artificially drive market prices far above the true probabilities.

These issues reflect the complexity of prediction market design. Although there is currently no "one-size-fits-all solution," improving the dispute resolution mechanism is undoubtedly one of the most significant challenges facing prediction markets. If market adjudications show inconsistencies, user trust in the system will gradually erode, ultimately causing the market to deviate from its original purpose.

Directions for Improvement: How to Optimize the Dispute Resolution Mechanism?

Fix market rules and prohibit post-hoc modifications. Once a market is launched, its rules should be locked and not subject to change. No form of "supplementary explanation" or "post-hoc clarification" should be allowed after the market terms are created. The original rules should serve as the sole reference. When disputes arise, the oracle should strictly adjudicate according to these foundational rules, without interference from content added by the platform.

Establish rule prioritization and on-chain records. Market rules need a clear hierarchy of priorities. For example, when conflicts arise between rules, which rules hold greater authority? Primary interpretive standards (such as credible media reports) should be clearly superior to secondary mechanisms. This hierarchy of rules should be recorded on the blockchain at the time of market creation, forming an immutable chain of evidence to ensure the transparency and authority of the rules.

Reputation-based verification mechanism. In addition to existing token voting, the market could introduce a reputation-based council system. This system would consist of respected industry experts who participate in adjudicating market outcomes, backed by their professional reputations. This mechanism not only introduces higher professionalism but also increases the sense of social responsibility in the verification process.

Inter-subject fork mechanism. The inter-subject fork is a mechanism inspired by Eigenlayer, specifically designed to handle obvious errors recognizable by human consensus. When significant disputes arise in the market, the community can split the tokens used for adjudication (whether oracle tokens or protocol tokens) into two versions, each supporting different interpretations of the outcome. Subsequently, the market's selection mechanism will determine which version of the tokens retains value. The side supporting the incorrect interpretation will face economic penalties as their token value declines, effectively curbing manipulative behavior.

AI agents as independent arbitrators. To avoid potential manipulative behavior by token holders due to economic incentives, we could develop a dedicated AI agent whose sole purpose is to adjudicate market outcomes. Unlike humans who may vote based on their own positions, AI agents can be designed to be completely neutral, focusing on fairly analyzing evidence to provide more accurate market adjudications. This approach can significantly enhance the market's credibility and decision-making efficiency while reducing the likelihood of human interference.

Conclusion

First, it should be noted that this article is not specifically intended to criticize Polymarket. However, as the largest (and frankly, the only one with actual influence) participant in the current cryptocurrency prediction market, it serves as the best case study for understanding the challenges facing the entire industry.

Why are these issues so important? If we view prediction markets merely as speculative platforms for traders to bet on outcomes, their flaws have relatively limited impact. Indeed, some individuals may incur losses as a result, but ultimately, it is just another betting venue.

However, prediction markets are being given a higher status; they are seen as "truth engines"—objective tools capable of filtering out noise and bias to reveal the true probabilities of future events.

This is precisely why the government shutdown case has drawn attention. When the market confidently predicts and validates a government shutdown event that never actually occurred, it reveals how these so-called "truth engines" can create a false reality that does not align with the facts. The issue is not just the economic losses of some traders; the greater danger lies in the fact that these "objective verification systems" we are building may be exploited by those with capital and motives to manipulate public perception.

As the influence of prediction markets grows, their structural weaknesses become a problem that everyone must confront. If we cannot address these fundamental vulnerabilities, we risk turning prediction markets into powerful tools for distorting truth rather than discovering it.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。