The original text is from Grayscale Research

Translation|Odaily Planet Daily Golem (@web3golem)_

Summary:

Summary:

The crypto market surged significantly in Q4 2024, with the FTSE/Grayscale Crypto Sectors Index showing strong market performance. The increase largely reflects the market's positive reaction to the results of the U.S. elections.

Competition in the smart contract platform sector remains fierce. The leading player, Ethereum, has underperformed compared to its second-largest competitor, Solana, and investors are increasingly focusing on other Layer 1 networks such as Sui and The Open Network (TON).

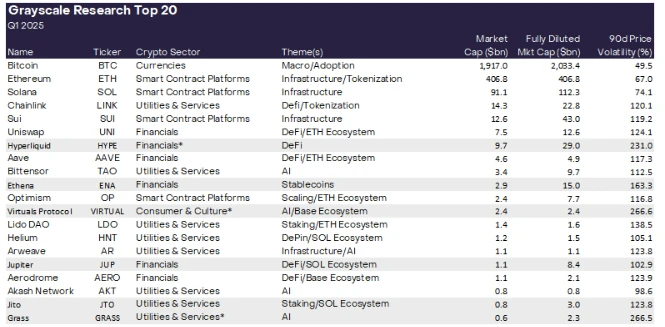

Grayscale Research has updated its Top 20 token list. This list represents a diversified set of assets in the cryptocurrency industry that may have high potential in the upcoming quarter. New assets added in Q1 2025 include HYPE, ENA, VIRTUAL, JUP, JTO, and GRASS. All assets in the Top 20 list exhibit high price volatility and should be considered high risk.

Grayscale Crypto Sectors Index

Grayscale Crypto Sectors provides a comprehensive framework for understanding the range of investable digital assets and their relationship to underlying technologies. Based on this framework and in collaboration with FTSE Russell, Grayscale has developed the FTSE Grayscale Crypto Sectors index series to measure and monitor crypto assets (Figure 1). Grayscale Research incorporates this index into its analysis of the digital asset market.

Figure 1: Positive Returns of the Grayscale Crypto Sectors Index in 2024

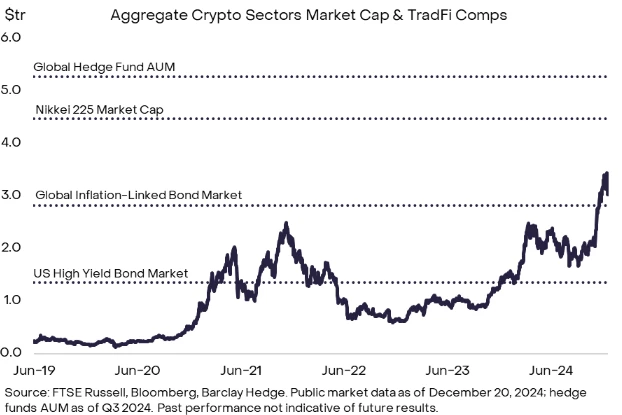

Cryptocurrency valuations soared in Q4 2024, primarily due to the market's positive reaction to the U.S. election results. According to the Cryptocurrency Sector Market Index (CSMI), the total market capitalization of the industry increased from $1 trillion to $3 trillion this quarter. Figure 2 compares the total market capitalization of cryptocurrencies with various traditional public and private market asset classes. For example, the current market capitalization of the digital asset industry is roughly equivalent to that of the global inflation-linked bond market—more than twice that of the U.S. high-yield bond market, but still far below the global hedge fund industry or the Japanese stock market.

Figure 2: $1 Trillion Increase in Cryptocurrency Market Capitalization in Q4 2024

Due to the increase in valuations, many new tokens met the inclusion criteria of the Grayscale Crypto Sectors framework (which has a minimum market capitalization requirement of $100 million for most tokens). In this quarterly rebalancing, Grayscale added 63 new assets to the index series, now totaling 283 tokens. The consumer and culture sectors saw the most new tokens added, reflecting the continued strong returns of meme coins and the appreciation of various assets related to gaming and social media.

By market capitalization, the largest new asset in the Crypto Sectors is Mantle, an Ethereum Layer 2 protocol that has now met the minimum liquidity requirements (for more details on Grayscale's index inclusion criteria, see here).

Competition in Smart Contract Platforms

The smart contract platform sector may be the most competitive sub-market in the digital asset industry. While 2024 was a milestone year for the sector leader Ethereum—having received approval for U.S. exchange-traded products (ETPs) and undergone significant upgrades—the performance of ETH has lagged behind some competitors, such as Solana, which is the second-largest asset in the sector by market capitalization. Investors are also turning their attention to other L1 networks, including high-performance blockchains like Sui and the blockchain TON integrated with the Telegram platform.

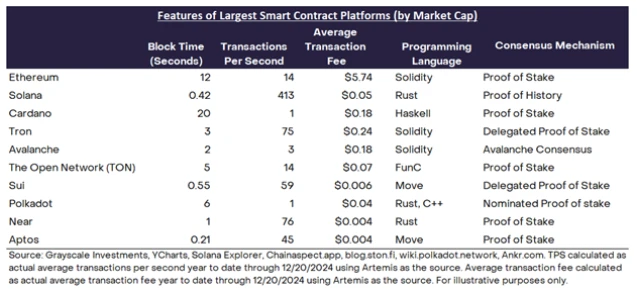

When creating infrastructure for application developers, architects of smart contract blockchains face various design choices. These design choices affect the three factors that constitute the "blockchain trilemma": network scalability, network security, and network decentralization. For example, prioritizing scalability often manifests as high transaction throughput and low fees (e.g., Solana), while prioritizing decentralization and network security may lead to lower throughput and higher fees (e.g., Ethereum). These design choices result in different block times, transaction throughput, and average transaction fees (Figure 3).

Figure 3: Smart Contract Platforms with Different Technical Characteristics

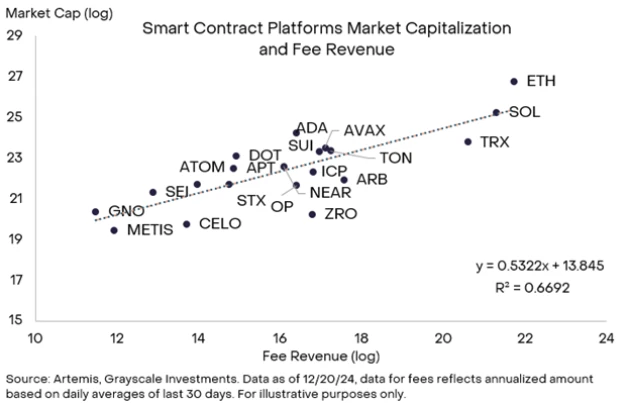

Regardless of the design choices and the strengths and weaknesses of the networks, smart contract platforms derive their value from the network fee revenue they generate. While other metrics (such as total TVL) are also important, fee revenue can be seen as the primary driver of token value accumulation in this market segment (related reading: The Battle for Value in Smart Contract Platforms).

As shown in Figure 4, there is a statistical relationship between fee revenue and market capitalization for smart contract platforms. The stronger the network's ability to generate fee revenue, the greater its ability to pass value to the network in the form of token burn or staking rewards. This quarter, the Top 20 token list compiled by Grayscale Research includes several smart contract platform tokens: ETH, SOL, SUI, and OP.

Figure 4: All Smart Contract Platforms Competing for Fee Revenue

Grayscale Research Top 20 Token List

Each quarter, the Grayscale Research team analyzes hundreds of digital assets to inform the rebalancing process of the FTSE/Grayscale Crypto Sectors series of indices. Following this process, Grayscale Research generates a list of the top 20 assets within the Crypto Sectors. The top 20 represent a diversified set of assets across Crypto Sectors, and these assets may have high potential in the upcoming quarter (Figure 4). The selection criteria for this list combine a range of factors, including network growth/adoption, upcoming catalysts, sustainability of fundamentals, token valuation, token supply inflation, and potential tail risks.

In Q1 2025, Grayscale will focus on tokens that involve at least one of the following three core market themes:

The U.S. elections and their potential implications for industry regulation, particularly in areas such as decentralized finance (DeFi) and staking;

Ongoing breakthroughs in decentralized AI technology and the use of AI agents in blockchain;

Growth of the Solana ecosystem.

Based on these themes, the following six assets have been added to the Top 20 list for Q1 2025:

Hyperliquid (HYPE): Hyperliquid is an L1 blockchain designed to support on-chain financial applications. Its primary application is a decentralized exchange (DEX) for perpetual futures, featuring a fully on-chain order book.

Ethena (ENA): The Ethena protocol has evolved into a new type of stablecoin, USDe, primarily backed by hedged positions in Bitcoin and Ethereum. Specifically, the protocol holds long positions in Bitcoin and Ether, as well as short positions in perpetual futures contracts of the same assets. The staked version of the token provides yield through the difference between spot and futures prices.

Virtual Protocol (VIRTUAL): Virtual Protocol is a platform for creating AI agents on the Ethereum L2 network, Base. These AI agents are designed to mimic human decision-making and autonomously execute tasks. The platform allows for the creation and co-ownership of tokenized AI agents that can interact with their environment and other users.

Jupiter (JUP): Jupiter is the leading DEX aggregator on Solana, boasting the highest TVL on the network. As retail traders increasingly enter the cryptocurrency market through Solana, and speculation around Solana-based memecoins and AI agent tokens intensifies, we believe Jupiter is fully capable of capitalizing on this growing market.

Jito (JTO): Jito is a liquidity protocol on Solana. Jito has seen significant growth in adoption over the past year and has the best financial health in the cryptocurrency space, with fee revenue exceeding $550 million in 2024.

Grass (GRASS): Grass is a decentralized data network that rewards users for sharing unused internet bandwidth through a Chrome extension. This bandwidth is used to scrape online data, which is then sold to AI companies and developers for training machine learning models, effectively conducting web data scraping while compensating users.

Figure 5: The Top 20 additions include DeFi applications, AI agents, and the Solana ecosystem.

Note: The shaded area indicates new tokens for the upcoming quarter (Q1 2025). “*” denotes assets in related fields not included in the Crypto Sectors index. Source: Artemis, Grayscale Investments. Data as of December 20, 2024, for reference only. Assets may change. Grayscale and its affiliates and clients may hold positions in the digital assets discussed in this article. All Top 20 assets exhibit high price volatility and should be considered high-risk assets.

In addition to the new themes mentioned above, Grayscale remains optimistic about themes from previous quarters, such as Ethereum scaling solutions, tokenization, and decentralized physical infrastructure (DePIN). These themes are still reflected in some protocols returning to the Top 20, such as Optimism, Chainlink, and Helium.

This quarter, we removed Celo from the Top 20. Grayscale Research continues to view these projects positively and believes they remain important components of the crypto ecosystem. However, the revised Top 20 list may offer more attractive venture capital returns in the upcoming quarter.

Investing in the cryptocurrency asset class involves risks, some of which are unique to the cryptocurrency asset class, including smart contract vulnerabilities and regulatory uncertainties. Additionally, all assets in the Top 20 exhibit high volatility and should be considered high-risk, making them unsuitable for all investors. Given the risks of the asset class, any investment in digital assets should be considered in the context of the overall portfolio and the investor's financial goals.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。