Original | Odaily Planet Daily

Author | jk

The price fluctuations of Bitcoin have long shown two completely different trends compared to traditional financial markets, driven by two entirely different narratives: As a risk asset, Bitcoin often performs in line with U.S. stocks during periods of high market sentiment and increased risk appetite, exhibiting a high positive correlation. This is mainly due to the increased participation of institutional investors, making its capital flow patterns similar to other high-risk assets. However, during market panic or the outbreak of risk events, Bitcoin is viewed as a safe-haven asset, decoupling from the performance of U.S. stocks and even showing negative correlation, especially when investors lose confidence in the traditional financial system.

These two narratives complicate Bitcoin's role, making it part of the risk asset category while also potentially serving as a safe-haven asset. Which one will it be? Especially at this time when Trump is about to take office?

Price Correlation: More "Safe-Haven" than U.S. Treasuries

According to TradingView statistics, over the past decade, the correlation between Bitcoin and the S&P 500 index has been 0.17, lower than that of other alternative assets. For example, the correlation between the S&P Goldman Sachs Commodity Index and the S&P 500 during the same period was 0.42. Although Bitcoin's correlation with the stock market has historically been low, this correlation has increased in recent years, rising to 0.41 over the past five years.

However, Bitcoin's strong volatility makes this correlation data less reliable: The relationship between Bitcoin and the S&P 500 showed a negative correlation of -0.76 on November 11, 2023 (around the FTX incident), but by January 2024, it had reached a positive correlation of 0.57.

In contrast, the S&P 500 has performed relatively steadily, with an average annual return of about 9% to 10%, serving as a benchmark for the U.S. economy. Although the overall return of the S&P 500 may be lower than that of Bitcoin, it excels in stability and lower volatility.

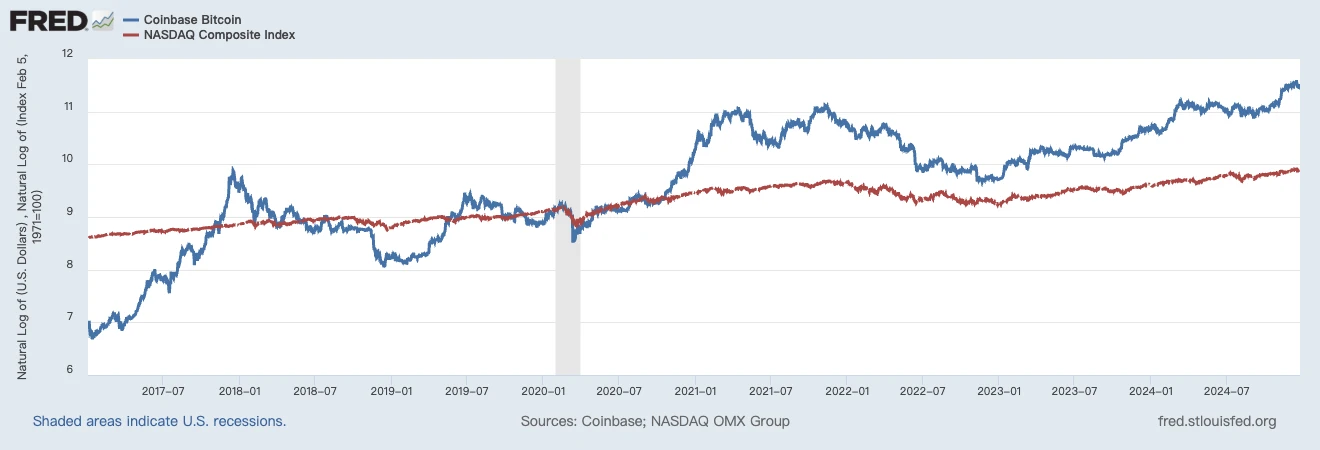

A logarithmic comparison of Bitcoin and the Nasdaq index. Source: FRED

It can be seen that during macro hot events, the two usually exhibit strong correlation: for example, during the market recovery after the COVID-19 pandemic in 2020, both showed significant upward trends. This may reflect an increased demand for risk assets in the context of loose monetary policy.

However, during other periods (such as 2022), the trends of Bitcoin and the Nasdaq diverged significantly, showing a weakening correlation, especially during black swan events that occurred specifically in the crypto market, where Bitcoin experienced unilateral crashes.

Of course, in terms of periodic returns, Bitcoin can easily outperform the Nasdaq by a wide margin. However, purely from the perspective of price correlation data, the correlation between the two is indeed increasing.

A report released by WisdomTree also mentioned a similar viewpoint, stating that although the correlation between Bitcoin and U.S. stocks is not high in absolute terms, recently this correlation is lower than the return correlation between the S&P 500 index and U.S. Treasuries.

Trillions of dollars in assets globally use the S&P 500 index as a benchmark or attempt to track its performance, making it one of the most closely watched indices in the world. If an asset can be found that has a -1.0 (completely inverse) and relatively stable correlation with the S&P 500 index, it would be highly sought after. This characteristic means that when the S&P 500 index performs negatively, this asset could potentially provide positive returns, demonstrating hedging characteristics.

Although stocks are generally considered risk assets, U.S. Treasuries are viewed by many as closer to "risk-free" assets. The U.S. government can fulfill its debt obligations by printing money, although the market value of U.S. Treasuries, especially long-term ones, may still fluctuate. A significant discussion point for 2024 is that the correlation coefficient between the S&P 500 index and U.S. Treasuries is approaching 1.0 (positive correlation 1.0). This means that both asset classes may rise or fall simultaneously during the same period.

The simultaneous rise or fall of assets is contrary to the original intention of hedging. This phenomenon is similar to 2022, when both stocks and bonds recorded negative returns, contradicting many investors' expectations of risk diversification.

Currently, Bitcoin does not show strong hedging capabilities against the return rates of the S&P 500 index. From the data, the correlation between Bitcoin and the S&P 500 index is not significant. However, recently, the return correlation between Bitcoin and the S&P 500 index is lower than that between the S&P 500 index and U.S. Treasuries. If this trend continues, Bitcoin will attract more attention from asset allocators and investors, gradually becoming a more attractive investment tool over time.

From this perspective, compared to the risk-free asset of U.S. Treasuries, Bitcoin only needs to be the "safe-haven asset that runs faster than U.S. Treasuries," and investors will naturally choose Bitcoin as part of their investment portfolio.

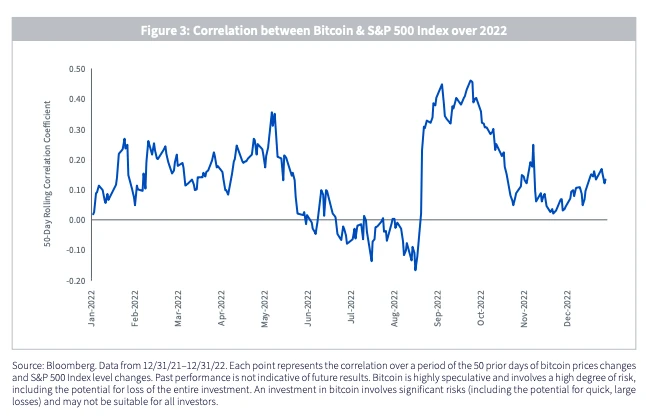

The chart shows the 50-day rolling correlation between Bitcoin prices and the S&P 500 index in 2022. On average, the correlation is about 0.1, with peaks exceeding 0.4 and lows below -0.1. Source: WisdomTree

Institutional Holdings: Increasing ETF Proportion

The role of institutional investors in the Bitcoin market is becoming increasingly important. As of now, the distribution of Bitcoin holdings shows a significant increase in institutional market influence, and this trend of centralization may further drive the correlation between Bitcoin and U.S. stock movements. Here is a specific analysis:

According to data, Bitcoin has currently mined 19.9 million coins out of a total of 21 million, leaving 1.1 million coins yet to be mined.

Among the mined Bitcoins, the holdings of the top 1,000 dormant addresses for over 5 years account for 9.15%, equivalent to about 1.82 million coins. This portion of Bitcoin typically does not enter the circulating market, effectively reducing the active supply in the market.

Additionally, according to Coingecko data, the top 20 listed companies, including Microstrategy, hold 2.63% of Bitcoin, approximately 520,000 coins, with Microstrategy alone holding 2.12% of the total Bitcoin supply (about 440,000 coins).

On the other hand, according to The Block, as of the time of writing this article, the institutional holdings of all ETFs currently amount to 1.17 million coins.

If we assume that the Bitcoin in dormant addresses, the unmined quantity, and the holdings of listed companies remain unchanged, then the theoretical circulating supply in the market = 19.9 - 1.82 - 0.52 = 17.56 million coins

Institutional holdings proportion: 6.67%

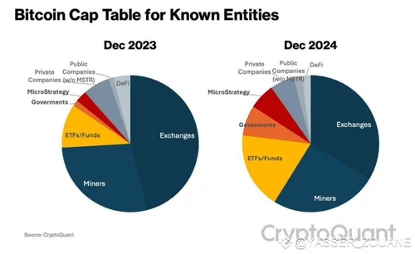

It can be seen that ETFs currently control 6.67% of Bitcoin's circulating supply, and this proportion may further increase as more institutions get involved. From the same period last year to this year, we can observe that the share from exchanges has been significantly compressed, while the share from ETFs has further grown.

Bitcoin holding proportions. Source: CryptoQuant

Similar to U.S. stocks, as the proportion of institutional investors' holdings in the market gradually increases, investment decision-making behavior (such as increasing or decreasing positions) will play a more critical role in price fluctuations. This phenomenon of market centralization can lead to Bitcoin's price movements being significantly influenced by the sentiment of the U.S. stock market, especially in the flow of investment funds driven by macroeconomic events.

The "Americanization" Process

The impact of U.S. policies on the Bitcoin market is becoming increasingly significant. This topic is currently more of an unknown: based on Trump's current style of action, if in the future key policy nodes, crypto-friendly individuals occupy important decision-making positions, such as promoting a more lenient regulatory environment or approving more financial products related to Bitcoin, the adoption rate of Bitcoin will undoubtedly further increase. This deepening of adoption will not only solidify Bitcoin's position as a mainstream asset but may also further bridge the correlation between Bitcoin and U.S. stocks, both of which reflect the direction of the U.S. economy.

In summary, the correlation with U.S. stocks is gradually increasing, primarily due to the joint response of prices to macro events, the significant impact of institutional holdings on the market, and the potential influence of U.S. policy trends on the market. From this perspective, we can indeed use the movements of U.S. stocks to gauge more trends regarding Bitcoin in the future.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。