The Double-Edged Sword of Crypto Compliance

Author: YBB Capital | Plain Language Blockchain

TL; DR

In the long run, Bitcoin through ETFs is not beneficial. The trading volume of Bitcoin ETFs in Hong Kong is vastly different from that in the United States, and it is undeniable that American capital is gradually enveloping the crypto market. Bitcoin ETFs divide the market into two parts: the white part, which under the framework of centralized financial regulation, retains only the speculative trading financial attribute, and the black part, which has more native blockchain activity and trading opportunities but faces regulatory pressure due to being "not legal."

MicroStrategy has achieved efficient arbitrage through capital structure design, closely linking the volatility of its stock with Bitcoin prices, thus achieving lower-risk returns in the long term. However, MicroStrategy is issuing unlimited debt to elevate its value, which requires a long-term Bitcoin bull market to sustain its worth. Therefore, Citron's short position on MicroStrategy has a higher payout than directly shorting Bitcoin, but MicroStrategy is confident that the future price trend of Bitcoin will be a slow rise without significant fluctuations.

Trump's crypto-friendly policies will not only maintain the dollar's status as the global reserve currency but will also strengthen the dollar's pricing power in the crypto market. Trump is uncompromising in holding onto the dollar's dominant position with one hand while grasping Bitcoin, the strongest weapon against the loss of trust in national fiat currencies, with the other, thus reinforcing and hedging risks in both directions.

01

American Capital Gradually Enveloping the Crypto Market

1) Hong Kong and U.S. ETF Data

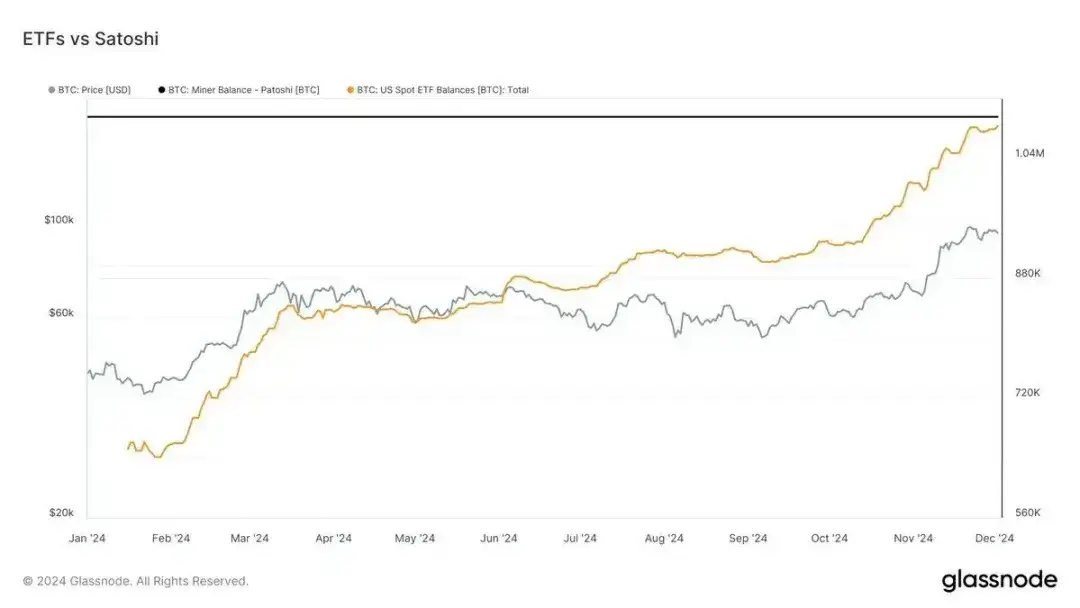

According to Glassnode data from December 3, 2024, the holdings of U.S. Bitcoin spot ETFs are just 13,000 coins away from surpassing Satoshi Nakamoto, with holdings of 1,083,000 and 1,096,000 coins respectively. The total net asset value of U.S. Bitcoin spot ETFs has reached $10.391 billion, accounting for 5.49% of Bitcoin's total market value. Meanwhile, according to Aastocks on December 3, data from the Hong Kong Stock Exchange shows that the total trading volume of three Bitcoin spot ETFs in Hong Kong was approximately HKD 1.2 billion in November.

Source of data: Glassnode

American capital is deeply intervening in and influencing the global crypto market, even dominating the development of the crypto industry. ETFs have pushed Bitcoin from an alternative asset to a mainstream asset, but they have also weakened Bitcoin's decentralized characteristics. ETFs have brought a large influx of traditional capital, but they have also firmly placed the pricing power of Bitcoin in the hands of Wall Street.

2) The "Black and White Division" of Bitcoin ETFs

Characterizing Bitcoin as a commodity means that it must adhere to the same rules as other commodities like stocks and bonds under tax law. However, the impact of Bitcoin ETFs is not entirely equivalent to the launch of other commodity ETFs, such as gold ETFs, silver ETFs, and oil ETFs. Currently approved or authorized Bitcoin ETFs differ from the market's recognition of Bitcoin itself:

The path to commodity ETFization is akin to a person holding physical assets or commodities (the trustee) needing to have them custodied by an intermediary (like a copper warehouse or a gold bank vault), and authorized institutions to complete transfers and record-keeping. After initiating shares (like fund shares), there will be shareholders to buy and sell shares using funds.

However, in the aforementioned process, the front end (design, development, sales, and after-sales service) will involve physical delivery, spot delivery, and cash delivery. But currently, the front end of the Bitcoin ETFs approved by the U.S. SEC is cash settlement, which is also the point that Cathie Wood has been arguing about, hoping to achieve physical delivery, but this is practically impossible.

Because the cash custodians in the U.S. are institutions operating under traditional centralized financial frameworks for cash purchase and redemption transactions, this means that the first half of Bitcoin ETFs is completely centralized.

At the end of Bitcoin ETFs, the centralized regulatory framework is difficult to confirm. The reason is that if Bitcoin is to be recognized, it must become a commodity under the existing centralized financial framework, and it will never recognize Bitcoin's attributes of being a substitute for fiat currency or its non-traceable decentralized properties. Therefore, Bitcoin can only undergo various financial product derivatives, such as futures, options, and ETFs, if it fully complies with regulatory conditions.

Thus, the emergence of Bitcoin ETFs signifies a complete failure of Bitcoin ETFs to counter fiat currency, and the decentralization of Bitcoin ETFs has become meaningless. The front end must rely entirely on the legitimacy of custodians like Coinbase, ensuring that the entire trading chain is legal, public, and traceable.

The black and white of Bitcoin will be completely divided by ETFs:

The current white part: Under the centralized regulatory framework, through extensive financial product derivatives, it reduces market price volatility, and as legitimate participants become more widespread, the speculative volatility of Bitcoin commodities will gradually decrease. After Bitcoin goes through ETFs, the white part in the market's supply and demand relationship has lost its important demand side (the decentralization and anonymity of Bitcoin), leaving only a single speculative trading financial attribute. At the same time, under the legalized regulatory framework, it also means that more taxes need to be paid, rendering Bitcoin's original functions of asset transfer and tax evasion obsolete. That is, the endorsement has shifted from a decentralized chain to a centralized government.

The former black part: The main reason for the crypto market's wild fluctuations lies in its opacity and anonymity, making it susceptible to manipulation. At the same time, the black part of the market will be more open, with more native blockchain value vitality and more trading opportunities. However, due to the emergence of the white part, those unwilling to transition to the white part will forever be excluded from the centralized regulatory framework and lose pricing power, akin to paying fines to the SEC.

02

Trump's Crypto All-Star Cabinet Picks

1) Cabinet Picks

In the 2024 U.S. presidential election, Trump's victory compared to the restrictive policies of the SEC, Federal Reserve, and FDIC during the Biden administration may lead the U.S. government to adopt a more developmental attitude towards crypto. According to Chaos Labs data, the nominations for Trump's new government cabinet are as follows:

Source: @chaos_labs

Howard Lutnick (Transition Team Leader and Commerce Secretary Nominee): Lutnick, as CEO of Cantor Fitzgerald, openly supports cryptocurrencies. His company actively explores the blockchain and digital asset space, including strategic investments in Tether.

Scott Bessent (Treasury Secretary Nominee): Bessent is a senior hedge fund manager who supports cryptocurrencies, believing they represent freedom and will exist long-term. He is more crypto-friendly than former Treasury Secretary candidate Paulson.

Tulsi Gabbard (Director of National Intelligence Nominee): Gabbard, with a core philosophy of privacy and decentralization, supports Bitcoin and invested in Ethereum and Litecoin in 2017.

Robert F. Kennedy Jr. (Secretary of Health and Human Services Nominee): Kennedy openly supports Bitcoin, viewing it as a tool against the devaluation of fiat currency, and may become an ally of the crypto industry.

Pam Bondi (Attorney General Nominee): Bondi has not made a clear statement on cryptocurrencies, and her policy direction remains unclear.

Michael Waltz (National Security Advisor Nominee): Waltz actively supports cryptocurrencies, emphasizing their role in enhancing economic competitiveness and technological independence.

Brendan Carr (FCC Chairman Nominee): Carr is known for anti-censorship and supporting technological innovation, which may provide technical infrastructure support for the crypto industry.

Hester Peirce & Mark Uyeda (Potential SEC Chairman Candidates): Peirce is a staunch supporter of cryptocurrencies, advocating for regulatory clarity. Uyeda criticizes the SEC's tough stance on cryptocurrencies, calling for clear regulatory rules.

2) Crypto-Friendly Policies as Financial Tools to Hedge Against the Erosion of Trust in the Dollar as a Global Reserve

Will the White House's promotion of Bitcoin undermine people's trust in the dollar as the global reserve currency, thereby weakening the dollar's position? American scholar Vitaliy Katsenelson suggests that as market sentiment towards the dollar has already been disturbed, the White House's promotion of Bitcoin may shake people's trust in the dollar as the global reserve currency, thus weakening its position. Regarding current fiscal challenges, "what can truly keep America great is not Bitcoin, but controlling debt and deficits."

Perhaps Trump's actions may become a hedge against the risk of the U.S. government losing its dominant position over the dollar. In the context of economic globalization, all countries hope to achieve the international circulation, reserve, and settlement of their national currencies. However, in this issue, there exists a trilemma of monetary sovereignty, free capital flow, and fixed exchange rates. The significant value of Bitcoin is that it provides a new solution to the contradictions of national systems and economic sanctions in the context of economic globalization.

Source: @CitronResearch

Overall, the stock premium of MicroStrategy (MSTR) and its strategy to achieve profits through the ATM (At The Market) mechanism, along with the leverage operations in Bitcoin investment and the views of short-selling institutions, can be summarized as follows:

1) Source of Stock Premium:

Most of MSTR's premium comes from the ATM mechanism. Citron Research believes that MSTR's stock has become an alternative investment to Bitcoin, with its stock price showing an unreasonable premium compared to Bitcoin, thus deciding to short MSTR. However, Michael Saylor refuted this view, arguing that short-sellers overlook MSTR's important profit model.

2) MicroStrategy's Leverage Operations:

Leverage and Bitcoin Investment: Saylor pointed out that MSTR leverages its investment in Bitcoin through debt issuance and financing, relying on Bitcoin's volatility for profit. The company flexibly raises funds through the ATM mechanism to avoid discounted issuance in traditional financing while utilizing high trading volumes to achieve large-scale stock sales, gaining arbitrage opportunities from stock premiums.

3) Advantages of the ATM Mechanism:

The ATM mechanism allows MSTR to flexibly raise funds and transfer the volatility, risk, and performance of debt to common stock. Through this operation, the company can achieve returns far exceeding borrowing costs and Bitcoin price increases. For example, Saylor pointed out that by financing Bitcoin investments at a 6% interest rate, if Bitcoin rises by 30%, the actual return for the company would be about 80%.

4) Specific Profit Cases:

By issuing $3 billion in convertible bonds, the company expects earnings per share to reach $125 within 10 years. If Bitcoin prices continue to rise, Saylor predicts that the company's long-term earnings will be substantial. For instance, two weeks ago, MSTR raised $4.6 billion through the ATM mechanism, trading at a 70% premium, earning $3 billion in Bitcoin within five days, equivalent to $12.5 per share, with long-term earnings expected to reach $33.6 billion.

5) Risks of Bitcoin Decline:

Saylor believes that purchasing MSTR stock means investors have accepted the risk of Bitcoin price declines. To achieve high returns, one must bear corresponding risks. He anticipates that Bitcoin will rise by 29% annually in the future, while MSTR's stock price will increase by 60% each year.

6) MSTR's Market Performance:

So far this year, MSTR's stock price has risen by 516%, far exceeding Bitcoin's 132% increase during the same period, and even surpassing AI leader Nvidia's 195% rise. Saylor believes MSTR has become one of the fastest-growing and most profitable companies in the U.S.

Regarding Citron's short position, MSTR CEO stated that Citron does not understand where MSTR's premium relative to Bitcoin comes from and explained:

“If we invest Bitcoin with financing at a 6% interest rate, when Bitcoin prices rise by 30%, what we actually get is an 80% Bitcoin price difference (a function of the combined stock premium, conversion premium, and Bitcoin premium).”

“The company issued $3 billion in convertible bonds, and based on an 80% Bitcoin price difference, this $3 billion investment could bring $125 in earnings per share over 10 years.”

This means that as long as Bitcoin prices continue to rise, the company can continue to profit: “Two weeks ago, we did $4.6 billion in ATM and traded at a 70% price difference, which means we earned $3 billion in Bitcoin within five days. About $12.5 per share. If calculated over 10 years, the earnings will reach $33.6 billion, approximately $150 per share.”

In summary, MicroStrategy's operational model achieves efficient arbitrage among stocks, bonds, and cryptocurrencies through capital structure design, closely linking its stock with Bitcoin price fluctuations to ensure low-risk profits for the company over the long term. However, the essence of MicroStrategy is to issue unlimited debt and elevate its value with unlimited leverage, which requires a long-term Bitcoin bull market to sustain its value. Undoubtedly, Citron's short position on MicroStrategy has a much higher payout than shorting Bitcoin directly, so MicroStrategy is also confident that the future price trend of Bitcoin will be a slow rise without significant fluctuations.

03

Conclusion

Source: Tradesanta

The U.S. is continuously strengthening its control over the crypto industry, and market opportunities are increasingly shifting towards centralization. The decentralized crypto utopia is gradually compromising towards centralization and "handing over" power. Every remedy has its drawbacks; the influx of funds from ETFs is merely a pain-relieving capsule that cannot cure the disease.

In the long run, Bitcoin through ETFs is not beneficial. The trading volume of Bitcoin ETFs in Hong Kong is vastly different from that in the United States. Based on the flow of capital, American capital is gradually enveloping the crypto market. Currently, even though China is an absolute leader in the mining sector, it still lags behind in capital markets and policy direction. Perhaps the long-term impact of Bitcoin ETFs will accelerate the normalization of crypto asset trading; this is both a beginning and an end.

Original Title: The Demise of Decentralization and the Consolidation of Power: U.S. Capital Poised to Complete the Transfer of Authority in the Crypto Utopia

Original Author: YBB Capital

Original Link: https://medium.com/ybbcapital/the-demise-of-decentralization-and-the-consolidation-of-power-u-s-b5086ec57be4

Article Link: https://www.hellobtc.com/kp/du/12/5587.html

Source: https://mp.weixin.qq.com/s/71VGpU-JjVqHcRwYBWfqXg

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。