Original Author: Joy Lou

Bit Deer (US stock code BTDR) updated its operational figures for November, with the market-focused A2 mining machine (Sealminer A2) starting mass production, with the first batch of 30,000 units for external sale.

First Growth Curve: Self-Developed Chips, Mining Machine Sales, Self-Operated Mining Farms

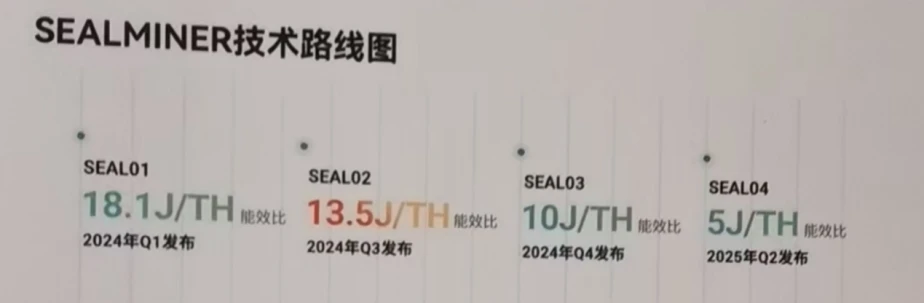

The ability to self-develop chips has always been the core competitiveness of mining machine manufacturers. In the past six months, Bit Deer has successfully completed a chip production run for the A2 and A3 mining machines.

Figure 1: Bit Deer Technology Roadmap

Source: Bit Deer Official Website

Figure 2: Bit Deer Main Mining Machine Parameter Forecast

Source: Model Forecast, Company Guidance

According to publicly available information, the operational parameters of the A2 mining machine are currently at a historically leading position compared to all mining machines available on the market. Although the A3 has not yet officially launched, based on known parameters, it is expected to become the largest single hash power mining machine globally, with leading energy consumption. The possibility of short-term external sales for this product is extremely low, as it will be prioritized for deployment in self-operated computing power.

Figure 3: Latest Global Mining Machine Companies and Mining Machine Parameters

Source: Bitmain, Bit Deer, Shenma Mining Machine, Canaan Technology Official Website

In terms of power plants, as of the end of November, the company has completed the deployment of a total of 895MW of power plants in the United States, Norway, and Bhutan. There are still 1645MW projects under construction, of which 1415MW will be completed in the second half of 2025. According to the conference call minutes from Guosheng, the company has established a special department dedicated to acquiring more power plant projects, with the expectation of adding over 1GW of power plants by 2026; the average electricity price of all self-operated power plants is less than $0.04 per kilowatt-hour, which is an absolute leading advantage compared to peers.

Figure 4: Bit Deer Built and Under Construction Power Plants

Source: Company Official Website

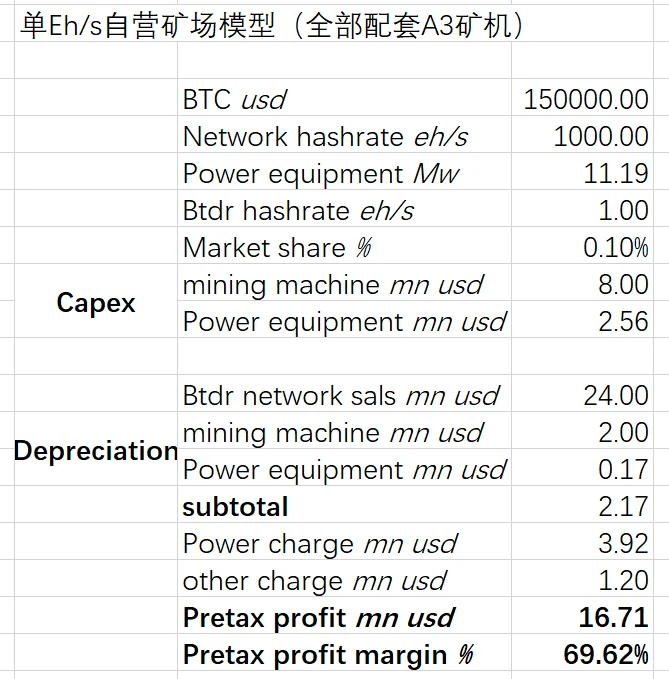

Given the above operational figures, Bit Deer's 1EH/s model is as follows:

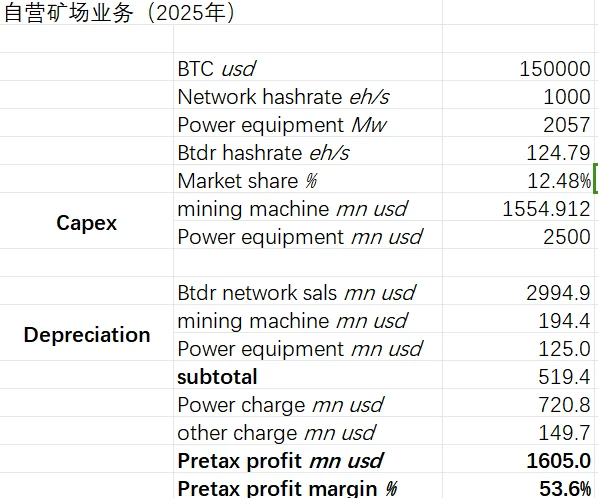

Figure 5: Bit Deer Single EH/s Model

Source: Model Forecast

The key assumptions of this model include a mining machine depreciation period of 4 years (depreciation can be up to 5 years under North American financial standards), a power plant depreciation period of 15 years (depreciation can be up to 20 years under North American financial standards), and other costs (including labor and operation) accounting for 5% of revenue (the company's historical operational figures are only 1-1.5%). According to the model, Bit Deer's self-operated mining farm shutdown price is $35,000 per Bitcoin.

Figure 6: Bit Deer Self-Operated Mining Farm Pre-Tax Profit Margin and Bitcoin Price Relationship

Source: Model Forecast

When the price of Bitcoin exceeds $150,000, the pre-tax profit slope of Bit Deer's self-operated mining farm can exceed the rate of Bitcoin's increase. If the price of Bitcoin reaches $200,000, Bit Deer's pre-tax profit margin for its self-operated mining farm will approach 80%.

For Bit Deer's first growth curve, the market still has two major concerns:

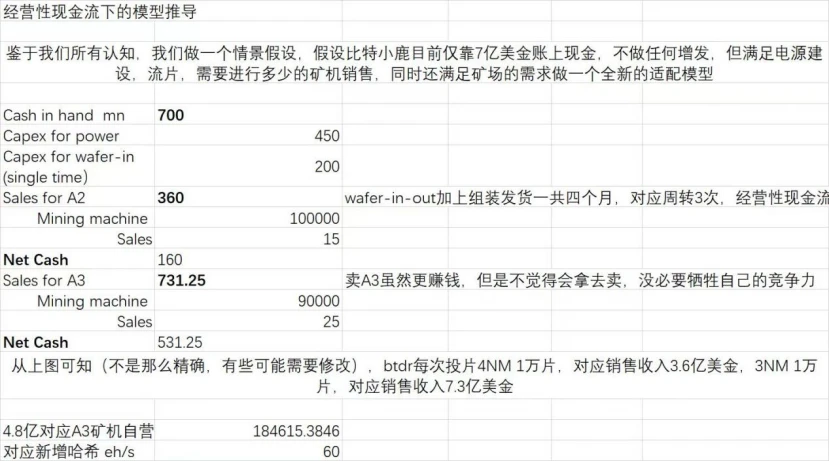

- Regarding the ratio of mining machine sales to self-use. As mentioned earlier, Bit Deer is expected to reach a power plant reserve of 2.3GW by mid-2025. If all these power plants are equipped with A3 mining machines, the self-operated computing power will be close to 220EH/s. Assuming linear growth of the total network computing power, it will account for about 20% of the total network computing power by the end of 2025. According to the company's Q3 2024 report, the company has $291 million in cash and cash equivalents, completed $360 million in convertible bonds by the end of November, and has about $690 million in cash on hand, including $40 million in options. Based on the company's power plant investment and self-operated demand, due to the time lag between self-operated computing power deployment and output, further financing may be needed. However, Bit Deer’s current stock price is undervalued, and the company has low willingness to issue additional shares. Therefore, starting from cash flow needs, a production run of 10,000 4nm wafers can generate an annual net cash flow of $480 million (calculated based on a 4-month mining machine turnover). If this cash flow is reinvested into self-operated computing power (fully equipped with A3 mining machines), it will increase computing power by 60EH/s. After 2025, Bit Deer's overall cash flow will no longer be a problem, and the combination of mining machine sales and mining operations can ensure that the Bitcoin produced by Bit Deer is not sold but retained.

Figure 7: Operating Cash Flow Derivation Model

Source: Model Forecast

- Regarding the competitive relationship between Bitmain and Bit Deer. The core of the commercial competition relationship is still the performance of mining machines and the cost of self-operated computing power. According to publicly available data and laboratory data, Bit Deer has a sufficient competitive advantage in both the mining machines it has produced and its self-operated costs. With the development of high-end process chips, mining machines, as the downstream of the industry, will also be affected by the competitive landscape upstream.

Second Growth Curve: AI Computing Power

In addition to mining machine sales and self-operated mining farms, the company's operational figures report for November shows that it has begun deploying Nvidia H200 chips in TIER3 data centers for AI computing power construction.

Mr. Wu Jihan wrote an article titled "The Beauty of Computing Power" in 2018: Computing power may be an effective means for humanity to reach a higher civilization and the most effective way to counteract entropy increase. The original intention remains.

According to a Tianfeng research report, the power deployment plans of major Bitcoin mining companies in North America exceed 1GW, with 3471MW already powered on, and it is expected to complete 5969MW before 2028. This power deployment will meet 56% of the electricity demand for data centers in North America. Bit Deer stated in the Tianfeng conference call on December 6 that it will deploy at least 200MW of power in the short term to support Nvidia's high-end chips and begin serving clients like MEGA 7 for cloud calls, emulating the COREWEAVE model.

Investment Recommendations and Valuation

Timing, location, and human factors best describe the current investment point for Bit Deer. The company is well-prepared for growth, with the first and second growth curves expected to rise in tandem, creating a synergistic effect, making it the most cost-effective target among current US mining stocks.

However, valuing the company and defining its value within the profit model presents challenges. The profit valuation from mining machine sales alone or from self-operated mining farms is insufficient to cover Bit Deer's true operational situation. Therefore, the two business models are fitted as follows:

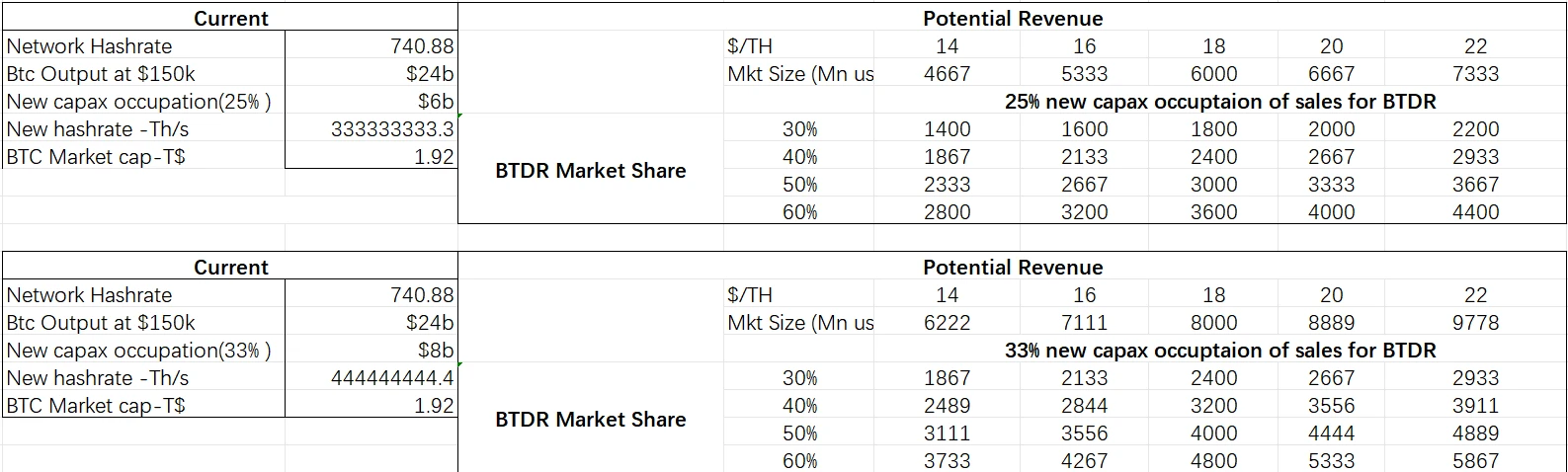

Figure 8: Bit Deer Mining Machine Sales Model Calculation

Source: Model Forecast

Figure 9: Bit Deer Self-Operated Mining Farm Forecast Model

Source: Model Forecast

The current valuation method for mainstream mining companies in North America is approximately $170 million/EH, which is closest to market consensus. It is reasonable to believe that in the next two years, Bit Deer's actual self-operated mining farms will reach between 120–220EH/s, with a market value estimated between $20.4 billion and $37.4 billion, representing a potential upside of 4.8–9.7 times from the current stock price.

Figure 10: Valuation of Major North American Mining Companies

Investment Risks:

Bitcoin price volatility risk;

Risks from sanctions leading to TSMC wafer production issues.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。