Usual represents an important exploratory direction in the DeFi 2.0 era.

Written by: Deep Tide TechFlow

The value of the listing effect on Binance is still rising.

In recent days, Binance's sudden listing of ACT and PNUT has sparked multiple rounds of discussion and has brought significant wealth effects to everyone.

Today, according to an official announcement, Binance will list Usual (USUAL) on Launchpool and Pre-Market. The Pre-Market will go live on 2024-11-19 at 10:00 (UTC). The Launchpool will start from 2024-11-15 at 00:00 (UTC).

The total supply of USUAL is 4 billion tokens, with an initial circulation ratio of 12.37%, of which the total amount for Launchpool is 300,000,000 USUAL (7.5% of the maximum token supply).

Compared to unstable Memes, Usual is actually a stablecoin protocol.

You might ask, isn't the current mainstream narrative about Memes? What makes this token stand out? Will it follow the path of VC coins?

Top CEXs certainly do not only choose to list Memes; essentially, any coin with a compelling narrative and sufficient secondary market potential could gain favor.

If you want to participate in Usual, take a look at the interpretation below, which will quickly help you understand everything you might need to know about this protocol.

Why do we need a stablecoin?

First, let's clarify two positions: Usual is a stablecoin protocol, and its launched USD0 is a permissionless and fully compliant stablecoin backed 1:1 by real-world assets (RWA);

The USUAL token itself is the governance token of the project, allowing the community to guide the future development of the network.

Following these two positions, let's quickly understand what Usual is doing.

Everyone knows that the current stablecoin market is already quite mature, with Tether and Circle holding an unshakeable position. So, what is the necessity of a new stablecoin?

Or, what is the narrative of a credible new stablecoin? The answer starts with three real observations.

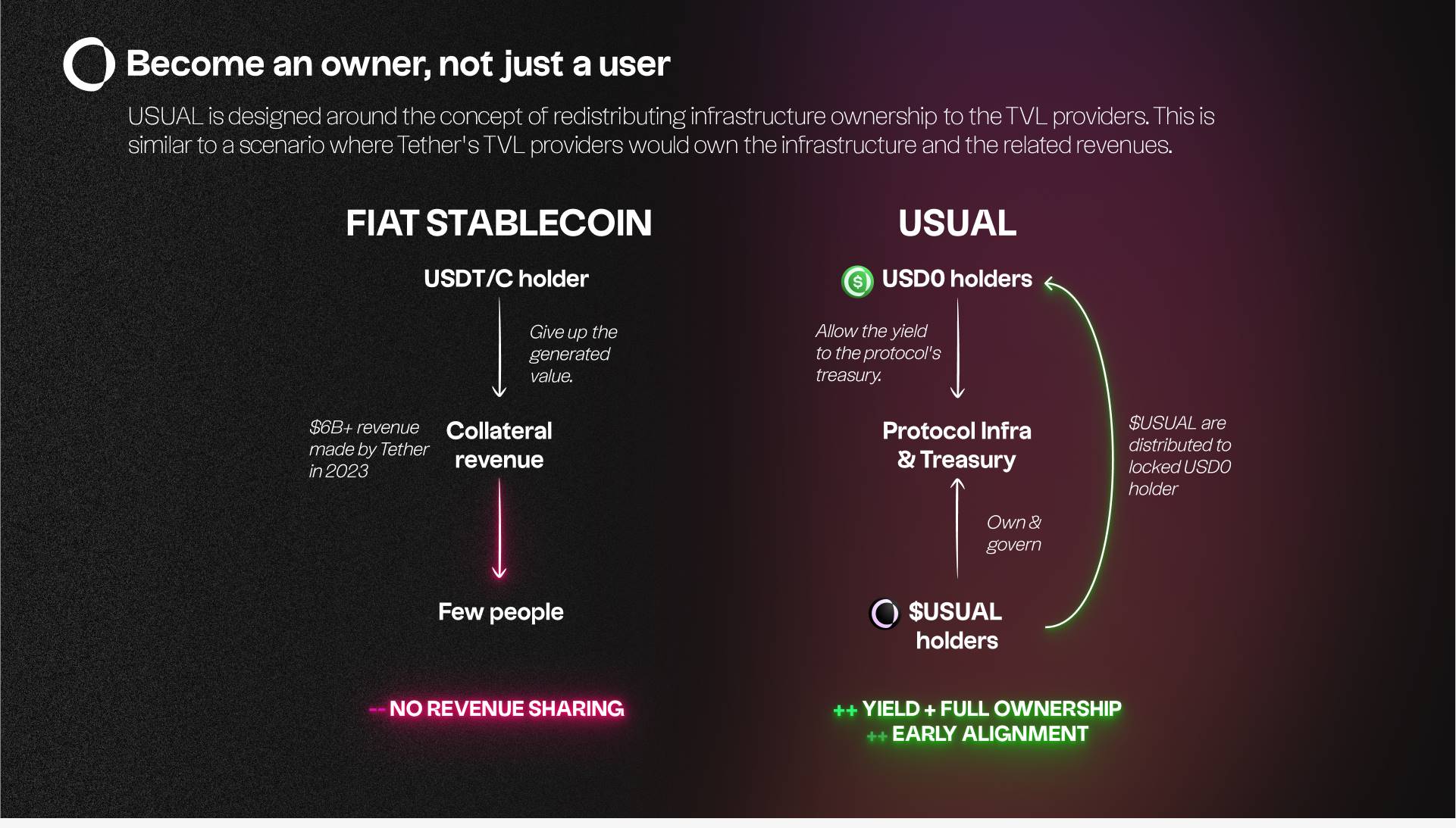

First, in 2023, Tether and Circle generated over $10 billion in revenue, with valuations exceeding $200 billion. However, users who contribute liquidity to them have not been able to share in these massive profits. This model of centralized institutions privatizing profits while socializing risks goes against the original intention of decentralized finance.

Second, while real-world assets (RWA) are gaining attention in the crypto market, even products like on-chain U.S. Treasury bonds have fewer than 5,000 holders on the mainnet. This indicates that the deep integration of RWA with DeFi still faces significant challenges.

Third, DeFi users generally hope to share in the success of the projects they support. However, existing profit distribution models often overlook the greater risks borne by early users and fail to adequately incentivize those who contribute to the project's success.

So this narrative points towards democracy and equality.

Based on these observations, Usual has proposed three of its own selling points:

First, it completely brings stablecoins on-chain. Unlike traditional stablecoins, Usual's issuance is entirely controlled by the community holding governance tokens, including important decisions such as risk policies, collateral types, and liquidity incentive strategies. This decentralized control ensures the neutrality and transparency of the protocol.

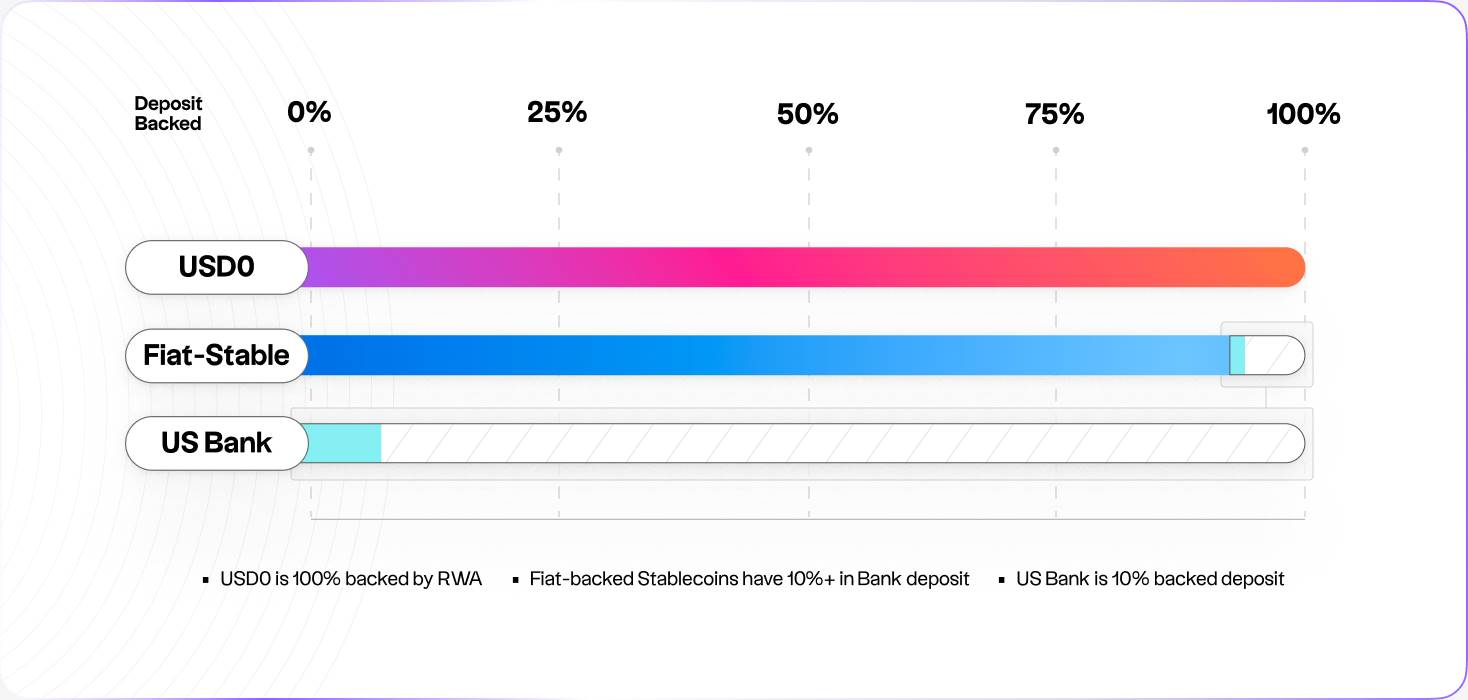

Second, it addresses the issue of bankruptcy isolation. Traditional stablecoin reserves are often held in commercial banks, exposing them to partial reserve risks within the banking system. As revealed by the collapse of Silicon Valley Bank, this model carries systemic risks. Usual takes a different approach, directly linking to ultra-short-term bonds, supplemented by strict risk policies and insurance funds, ensuring 100% collateralization of assets.

Finally, it redefines the ownership and profit distribution mechanisms of stablecoins. Users not only gain the profits generated from stablecoin collateral but, more importantly, through governance tokens, they obtain complete control over the protocol, treasury, and future revenues.

Essentially, the emergence of Usual is not simply to compete with existing stablecoins; it attempts to address a more fundamental issue: how to make stablecoins truly become the financial infrastructure owned by users, rather than a profit tool for some centralized institution.

Understanding Usual's USD0, a stablecoin backed by RWA

The ecosystem of Usual Protocol mainly consists of three core products: USD0, USD0++, and the USUAL governance token. Each product has its unique functions and value propositions, collectively forming a complete financial ecosystem.

- USD0: A Safe and Stable Foundation

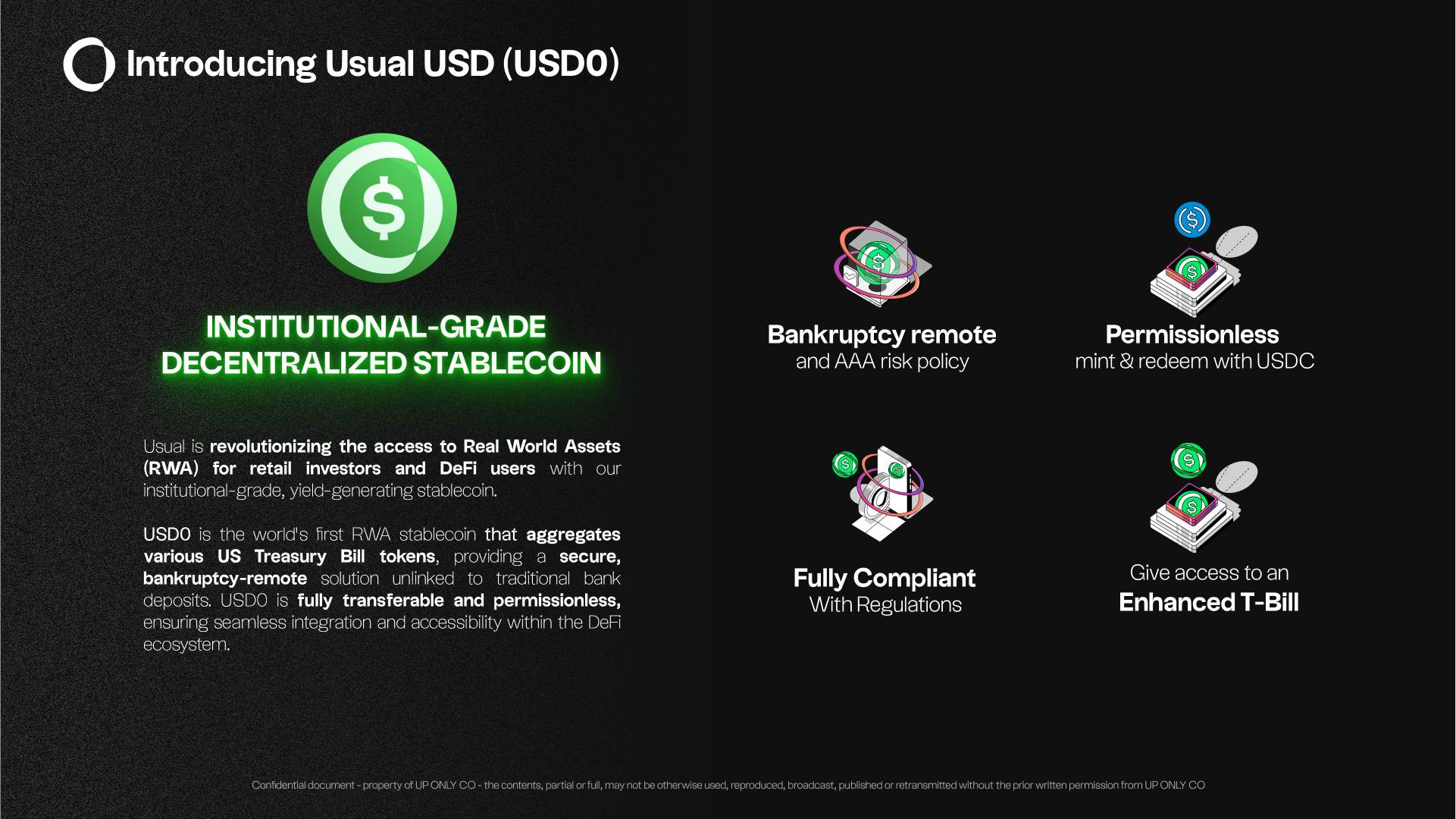

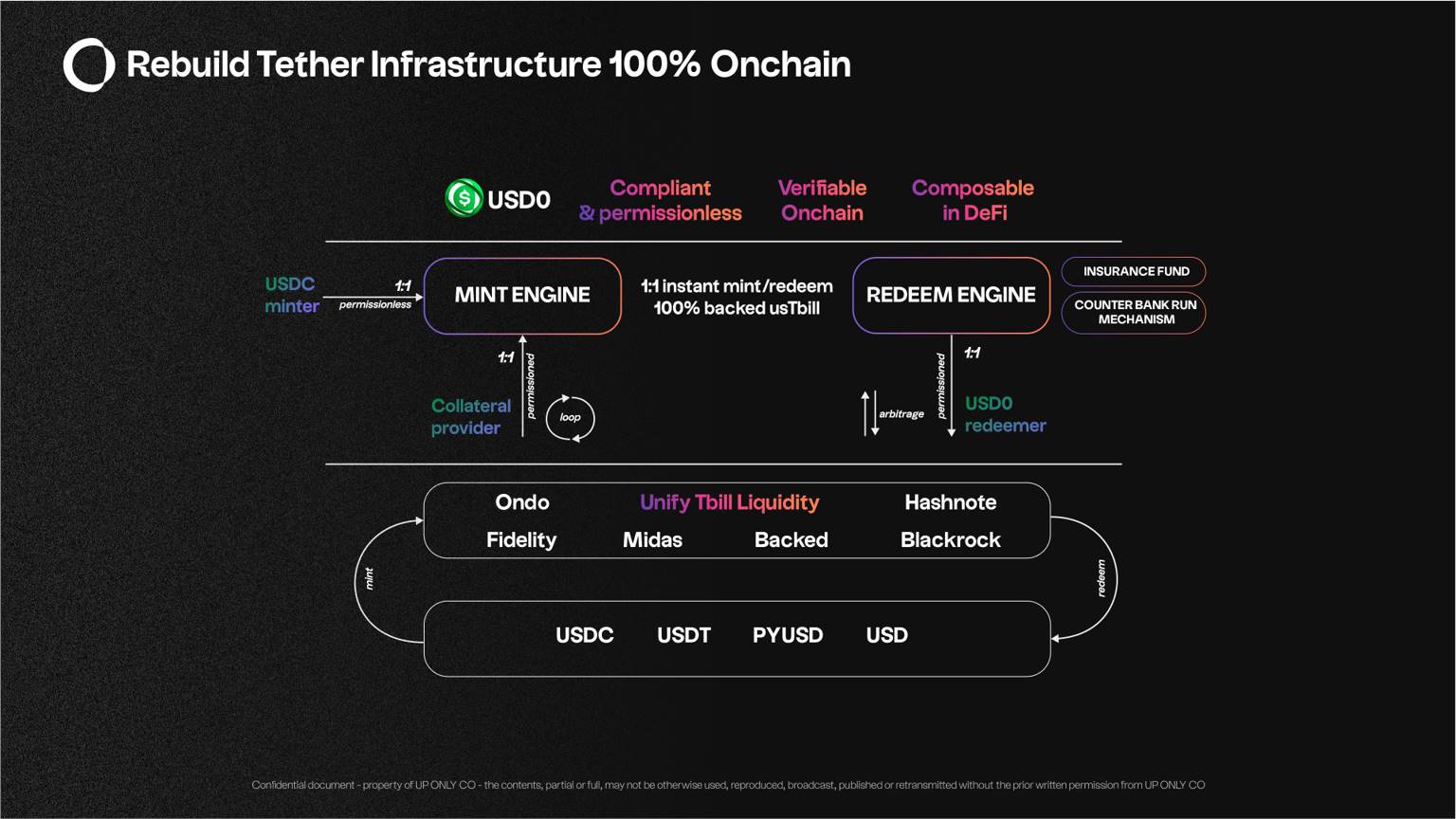

USD0 is the cornerstone of the Usual ecosystem; it is the world's first RWA stablecoin that aggregates multiple U.S. Treasury bond tokens. This design makes USD0 a secure, bankruptcy-isolated solution that does not rely on traditional bank deposits, thus avoiding the systemic risks that traditional financial systems may pose.

The reason USD0 has a "0" is that it aims to be the equivalent of central bank money (M0) within the currency protocol.

The main features of USD0 include:

Fully transferable and permissionless: ensuring seamless integration and wide accessibility within the DeFi ecosystem.

Versatility: can be used as a payment tool, counterparty, and collateral.

Transparency: provides real-time updates on collateral information, enhancing user trust.

Scalability: backed by a deeply liquid U.S. Treasury bond market, it can theoretically scale to trillions of dollars.

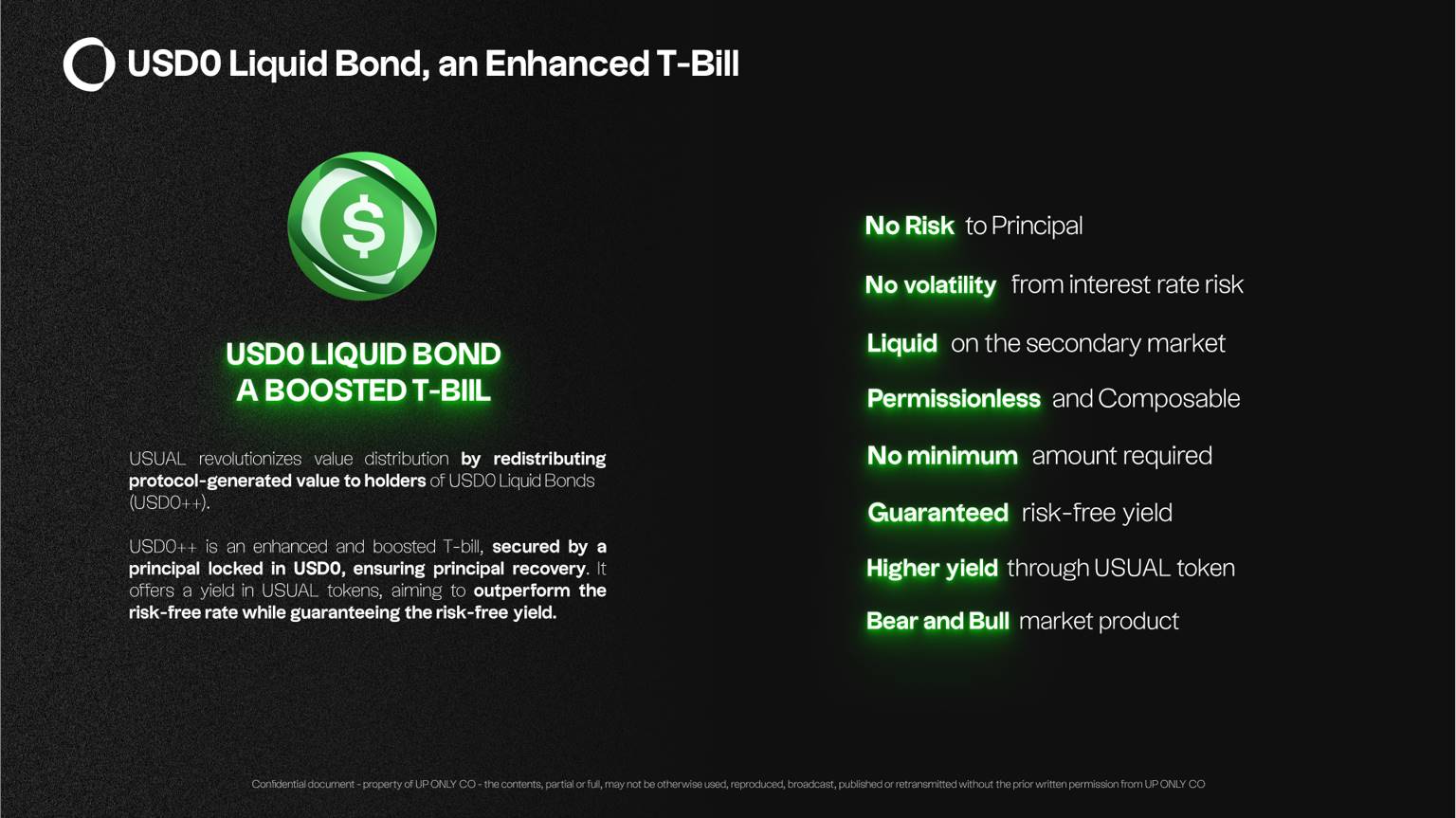

- USD0++: An Innovative Product that Doubles Treasury Returns

USD0++ is an innovative product within the Usual ecosystem, essentially an enhanced Treasury bond. Through enhanced 4-year DeFi Treasury bonds, it is backed by the principal locked in USD0 for 4 years, ensuring the principal can be recovered. It allows users to benefit from the growth and success of the protocol. Unlike traditional models, USD0++ not only provides protocol revenue but also distributes ownership of the protocol through its innovative reward mechanism.

This innovative design embodies profound financial wisdom. When users convert USD0 to USD0++, they effectively enter a carefully designed dual-yield structure. The first layer is the base yield from U.S. Treasury bonds, guaranteed by the Base Interest Guarantee (BIG) mechanism, ensuring that investors can receive returns comparable to ordinary Treasury bonds even in the worst-case scenario. The second layer comes from enhanced yields generated by the protocol's development, distributed in the form of USUAL tokens.

It is worth noting that the lock-up period for USD0++ is set at 4 years; this choice of time span is not arbitrary. It aligns with the maturity of U.S. mid-term Treasury bonds and gives the protocol sufficient time to develop and create value. During this 4-year period, USD0++ holders effectively become long-term partners of the protocol, with their interests closely tied to the growth of the protocol.

From a technical implementation perspective, USD0++ adopts an automated management approach through smart contracts. When users deposit USD0, the contract automatically allocates funds to the optimal Treasury bond portfolio while initiating a token issuance plan. This process is completely transparent and immutable, allowing users to check their investment status and expected returns at any time. More importantly, the entire system employs a modular design, meaning that parameters can be flexibly adjusted or new features added in response to market demands and regulatory requirements.

Compared to traditional financial markets, the innovation of USD0++ lies in its successful transformation of passive Treasury bond investment into active protocol participation. Investors are no longer just waiting for interest to mature; they can participate in protocol governance through USUAL tokens, share in growth dividends, and even trade these rights in the secondary market. This design essentially creates a new category of financial products that retains the safety of Treasury bonds while endowing them with the growth potential of the crypto economy.

From a risk management perspective, USD0++ offers a unique risk hedging solution. In the highly volatile environment of the crypto market, investors can obtain stable cash flow from Treasury bonds while sharing in industry growth through USUAL tokens; this combination strategy effectively balances risk and return. Especially during market downturns, the base interest guarantee mechanism can provide important downside protection, while in bullish market conditions, USUAL tokens offer considerable upside potential.

- USUAL: The Core of Governance and Incentives

As the governance token of Usual Protocol, USUAL's design concept goes far beyond a simple voting rights token. It is the core of value capture and distribution within the entire ecosystem, ensuring the sustainable development of the protocol and maximizing user interests through a carefully designed tokenomics model.

In terms of governance, USUAL adopts an innovative "value-oriented governance" model. Holders can not only participate in important decisions of the protocol, such as risk parameter adjustments and new product launches, but more importantly, their voting power is directly linked to their contributions to the protocol. This mechanism ensures that users who hold long-term and actively participate in ecological construction can gain greater influence.

The value capture mechanism of USUAL is established on multiple levels. First, all revenues generated by the protocol, including minting fees, redemption fees, etc., will be used to support the value of USUAL. Second, through a staking mechanism, USUAL holders can receive ongoing revenue sharing. More importantly, as the asset scale managed by the protocol grows, the issuance rate of USUAL will gradually decrease. This deflationary design ensures the long-term value growth potential of the token.

In practical applications, the functions of USUAL have extended beyond governance into multiple areas. It can be used as a reward token for liquidity mining, participate in the pricing of various financial products within the ecosystem, and even serve as a medium for cross-chain bridging. This multidimensional utility not only increases the demand for the token but also strengthens the network effects of the entire ecosystem.

Through this comprehensive design, USUAL successfully links the various components of the protocol organically, forming a self-reinforcing positive feedback loop. As more users participate and assets continue to accumulate, the value proposition of USUAL will become increasingly clear and powerful.

Outlook

From the current market environment, the timing of Usual's launch can be considered quite opportune. As the crypto market gradually recovers from the bear market, the demand for high-quality projects is on the rise. Unlike Meme coins that purely pursue short-term speculation, Usual offers a complete financial infrastructure solution, and this differentiated positioning may become its unique advantage.

From a valuation perspective, we need to focus on several key dimensions:

First is the overall space of the stablecoin sector. Currently, the combined market capitalization of USDT and USDC exceeds $100 billion, with annualized revenues exceeding $10 billion. If Usual can capture 5% of this market share, its stablecoin business alone could support a considerable valuation.

Second is the growth potential of the RWA sector. As traditional financial institutions gradually enter the crypto market, the demand for compliant on-chain Treasury bond products will significantly increase. As the first protocol to tokenize Treasury bond yields, Usual is likely to become an important player in this emerging market.

Looking at the market performance after Binance listings, recent cases show that the market's enthusiasm for quality projects remains high (regardless of whether they are Memes, quality projects with unique narratives are favored). Usual possesses a complete product matrix, a clear value capture model, and vast market space, all of which align closely with the characteristics of successful listed projects.

However, investors also need to be aware of several key risk points:

First is regulatory risk. Although Usual uses compliant Treasury bonds as backing, in the context of tightening global financial regulations, any innovative financial product may face policy uncertainties.

Second is the market education cost. The model that combines stablecoins, Treasury bond yields, and governance tokens, while innovative, also increases the difficulty for users to understand. The project team will need to invest significant resources in market education.

Third is competition risk. Once Usual proves this model is viable, it will inevitably attract more teams to enter the space, and maintaining a first-mover advantage will be an ongoing challenge.

Overall, Usual represents an important exploratory direction in the DeFi 2.0 era. It does not simply replicate existing models but attempts to solve real problems through technological innovation. For investors seeking long-term value, this is undoubtedly a project worth paying attention to. However, investors also need to reasonably allocate their positions based on their risk tolerance and investment horizon, and manage risks effectively.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。