Original Title: "Black or White?"

Author: Arthur Hayes

Translation: Deep Tide TechFlow

(This article expresses the author's personal opinions and should not be used as a basis for investment decisions, nor should it be considered investment trading advice.)

What do you think the price of Bitcoin will be on December 31, 2024? Over $100,000 or under $100,000?

There is a famous saying in China: "It doesn't matter if a cat is black or white, as long as it catches mice, it's a good cat."

I will refer to the policies implemented by President Trump after his election as "American capitalism with Chinese characteristics."

The elites ruling Pax Americana do not care whether the economic system is capitalism, socialism, or fascism; they only care whether the policies implemented help maintain their power. The United States has not been purely capitalist since the early 19th century. Capitalism means that when the rich make bad decisions, they lose money. This situation was prohibited when the Federal Reserve System was established in 1913. With the privatization of profits and socialization of losses affecting the nation, and the extreme class division created between the "deplorables" or "lower class" living in the interior and the noble, respected coastal elites, President Roosevelt had to correct course by dispensing some crumbs to the poor through his "New Deal" policies. Then, just like now, expanding government relief for the disadvantaged was not a welcomed policy by the so-called wealthy capitalists.

The shift from extreme socialism (in 1944, raising the highest marginal tax rate on incomes over $200,000 to 94%) to unrestricted corporate socialism began in the 1980s under Reagan. Subsequently, the central bank injected funds into the financial services industry through money printing, hoping that wealth would gradually trickle down from the top. This neoliberal economic policy continued until the COVID pandemic in 2020. President Trump, in response to the crisis, displayed his inner Roosevelt spirit; he directly distributed the most funds to the entire populace since the New Deal. The U.S. printed 40% of the world's dollars between 2020 and 2021. Trump initiated the distribution of "stimulus checks," and President Biden continued this popular policy during his term. When assessing the impact of the government's balance sheet, some peculiar phenomena emerged between 2008-2020 and 2020-2022.

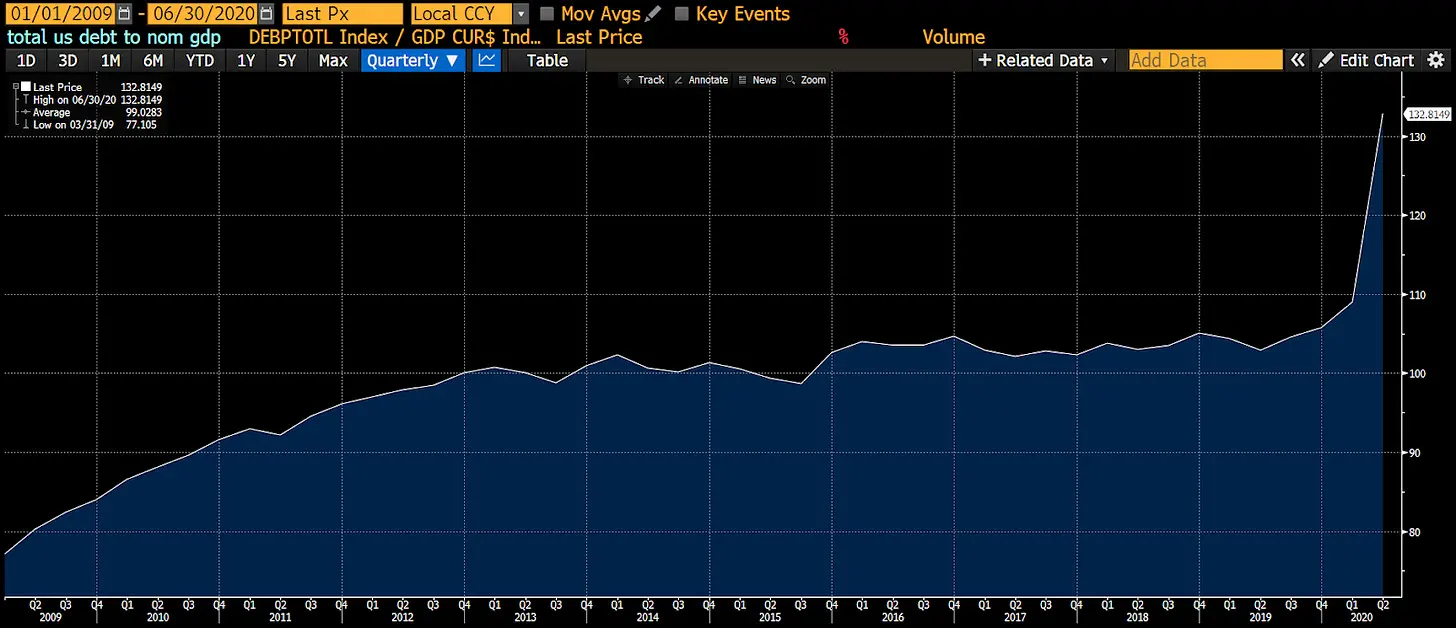

From 2009 to the second quarter of 2020 was the peak of so-called "trickle-down economics," during which economic growth primarily relied on the central bank's money printing policy, commonly known as quantitative easing (QE). As you can see, the growth rate of the economy (nominal GDP) was lower than the accumulation rate of national debt. In other words, the rich used the funds they received from the government to purchase assets. Such transactions did not generate substantial economic activity. Therefore, providing trillions of dollars in debt to wealthy financial asset holders actually increased the ratio of debt to nominal GDP.

From the second quarter of 2020 to the first quarter of 2023, Presidents Trump and Biden took different approaches. Their Treasury issued debt purchased by the Federal Reserve through quantitative easing (QE), but this time it was not given to the rich; instead, checks were sent directly to every citizen. The poor indeed received cash in their bank accounts. Clearly, Jamie Dimon, CEO of JPMorgan, profited significantly from the fees on government transfers… He is referred to as America's Li Ka-shing, and you cannot avoid paying him fees. The poor are poor because they spend all their money on goods and services, and during this period, they indeed did so. With the velocity of money circulation significantly increasing, economic growth surged. That is to say, $1 of debt generated more than $1 of economic activity. As a result, the ratio of U.S. debt to nominal GDP miraculously decreased.

However, inflation intensified because the growth in the supply of goods and services could not keep up with the increase in purchasing power obtained through government debt. The wealthy holding government bonds were dissatisfied with these populist policies. These wealthy individuals experienced the worst total returns since 1812. In retaliation, they sent out Federal Reserve Chairman Jay Powell, who began raising interest rates in early 2022 to control inflation, while the general public hoped for another round of stimulus checks, but such policies were prohibited. U.S. Treasury Secretary Yellen intervened to offset the impact of the Federal Reserve tightening monetary policy. She drained the Fed's reverse repurchase facility (RRP) by shifting debt issuance from long-term bonds to short-term notes. This injected nearly $2.5 trillion in fiscal stimulus into the market, primarily benefiting those holding financial assets; the asset market thus thrived. Similar to after 2008, the government relief for these wealthy individuals did not generate actual economic activity, and the U.S. debt to nominal GDP ratio began to rise again.

Did Trump's incoming cabinet learn lessons from recent U.S. economic history? I believe they did.

Scott Bassett, widely regarded as Trump's pick to replace Yellen as U.S. Treasury Secretary, has given many speeches on how he would "fix" America. His speeches and columns detail how to implement Trump's "America First Plan," which bears a striking resemblance to China's development strategy (which began in the 1980s under Deng Xiaoping and continues to this day). This plan aims to promote the return of key industries (such as shipbuilding, semiconductor factories, automotive manufacturing, etc.) through government-provided tax credits and subsidies, thereby boosting nominal GDP growth. Eligible companies will be able to obtain low-interest bank loans. Banks will once again actively lend to these operational companies, as their profitability is guaranteed by the U.S. government. As companies expand their operations in the U.S., they will need to hire American workers. Ordinary Americans receiving higher-paying jobs means increased consumer spending. If Trump restricts immigration from certain countries, these effects will be even more pronounced. These measures stimulate economic activity, and the government collects revenue through corporate profits and personal income taxes. To support these plans, government deficits need to remain high, and the Treasury raises funds by selling bonds to banks. Since the Federal Reserve or lawmakers have suspended the supplementary leverage ratio, banks can now re-leverage their balance sheets. The winners are ordinary workers, companies producing "qualified" products and services, and the U.S. government, whose debt to nominal GDP ratio decreases. This policy is equivalent to super quantitative easing for the poor.

Sounds great. Who would oppose such a prosperous era for America?

The losers are those holding long-term bonds or savings deposits, as the yields on these instruments will be deliberately suppressed below the nominal growth rate of the U.S. economy. If your wages cannot keep up with higher inflation levels, you will also be affected. Notably, joining unions is becoming popular again. "4 and 40" has become the new slogan, meaning a 40% raise for workers over the next four years, or a 10% raise each year, to incentivize them to keep working.

For those readers who consider themselves wealthy, don't worry. Here’s an investment guide. This is not financial advice; I am simply sharing what I do in my personal investment portfolio. Whenever a bill passes and allocates funds to a specific industry, read it carefully and then invest in stocks of those industries. Instead of putting money into government bonds or bank deposits, consider buying gold (as a hedge against financial repression for the baby boomer generation) or Bitcoin (as a hedge against financial repression for the millennial generation).

Clearly, my portfolio prioritizes Bitcoin, other cryptocurrencies, and stocks of cryptocurrency-related companies, followed by gold stored in a vault, and finally stocks. I will keep a small amount of cash in a money market fund to pay my Amex bills.

In the remainder of this article, I will explain how the quantitative easing policies for the rich and the poor affect economic growth and the money supply. Next, I will predict how exempting banks from the supplementary leverage ratio (SLR) will again make unlimited quantitative easing for the poor possible. In the final section, I will introduce a new index to track the supply of bank credit in the U.S. and show how Bitcoin has outperformed all other assets when adjusted for bank credit supply.

Money Supply

I have a deep admiration for the high quality of Zoltan Pozar's Ex Uno Plures series of articles. During my recent long weekend in the Maldives, I read all of his works while enjoying surfing, Iyengar yoga, and fascia massage. His work will frequently appear in the remainder of this article.

Next, I will present a series of hypothetical accounting entries. On the left side of the T-account are assets, and on the right side are liabilities. Blue entries indicate value increases, while red entries indicate value decreases.

The first example focuses on how the Federal Reserve's bond purchases through quantitative easing affect the money supply and economic growth. Of course, this example and the subsequent ones will be slightly humorous to add interest and appeal.

Imagine you are Powell during the U.S. regional banking crisis in March 2023. To relieve the pressure, Powell heads to the Racquet and Tennis Club at 370 Park Avenue in New York City to play squash with a billionaire old friend. Powell's friend is very anxious.

This friend, whom we will call Kevin, is a seasoned financial professional, and he says, "Jay, I might have to sell my house in the Hamptons. All my money is in Signature Bank, and clearly, my balance exceeds the federal deposit insurance limit. You have to help me. You know how hard it is for a rabbit to stay in the city for a day in the summer."

Jay replies, "Don't worry, I'll take care of it. I will initiate $2 trillion in quantitative easing. This will be announced on Sunday night. You know the Fed always has your back. Without your contributions, who knows what America would look like? Just imagine if Trump regained power because Biden had to deal with a financial crisis. I still remember Trump stealing my girlfriend at Dorsia in the early '80s; it was infuriating."

The Federal Reserve created a Bank Term Funding Program, which is different from direct quantitative easing, to address the banking crisis. But allow me to add a bit of artistic flair here. Now, let’s see how $2 trillion in quantitative easing affects the money supply. All numbers will be in billions of dollars.

The Federal Reserve purchased $200 billion in government bonds from Blackrock and paid for it with reserves. JP Morgan acted as an intermediary in this transaction. JP Morgan received $200 billion in reserves and credited Blackrock with $200 billion in deposits. The Federal Reserve's quantitative easing policy allowed banks to create deposits, which ultimately became money.

Having lost the government bonds, Blackrock needed to reinvest this capital into other interest-bearing assets. Blackrock's CEO, Larry Fink, typically collaborates only with industry leaders, and at this moment, he is quite interested in the tech sector. A new social networking application called Anaconda is building a user community to share user-uploaded photos. Anaconda is in a growth phase, and Blackrock is eager to purchase their bonds worth $200 billion.

Anaconda has become an important player in the U.S. capital markets. They successfully attracted a male user base aged 18 to 45, who became addicted to the app. As these users reduced their reading time in favor of browsing the app, their productivity significantly declined. Anaconda financed stock buybacks through debt issuance for tax optimization, allowing them to avoid repatriating overseas retained earnings. Reducing the number of shares not only boosted the stock price but also increased earnings per share, as the denominator decreased. Consequently, passive index investors like Blackrock were more inclined to buy their stocks. The result was that the elites, after selling their stocks, found an additional $200 billion in their bank accounts.

The wealthy shareholders of Anaconda had no immediate need for this capital. Gagosian hosted a grand party at the Miami Basel Art Fair. At the party, the elites decided to purchase the latest artworks to enhance their reputation as serious art collectors while also impressing the beauties at the booth. The sellers of these artworks were also individuals from the same economic class. The result was that the buyers' bank accounts were credited, while the sellers' accounts were debited.

After all these transactions, no actual economic activity was created. The Federal Reserve, by injecting $2 trillion into the economy, effectively only increased the bank account balances of the wealthy. Even financing for an American company did not generate economic growth, as these funds were used to inflate stock prices without creating new job opportunities. $1 of quantitative easing resulted in a $1 increase in the money supply but did not bring about any economic activity. This is not a reasonable use of debt. Therefore, from 2008 to 2020, the ratio of debt to nominal GDP during the period of quantitative easing rose among the wealthy.

Now, let’s look at President Trump's decision-making process during COVID. Back in March 2020: at the onset of the COVID outbreak, Trump's advisors suggested he "flatten the curve." They advised him to shut down the economy, allowing only "essential workers" to continue working, typically those who maintain operations at low wages.

Trump: "Do I really need to shut down the economy because some doctors think this flu is serious?"

Advisor: "Yes, Mr. President. I must remind you that primarily older individuals like yourself are at risk of complications from COVID-19. I also want to point out that if they get sick and need hospitalization, treating the entire population over 65 will be very expensive. You need to lock down all non-essential workers."

Trump: "This will lead to an economic collapse; we should send checks to everyone so they won't complain. The Federal Reserve can buy the debt issued by the Treasury, which will fund these subsidies."

Next, let’s use the same accounting framework to analyze step by step how quantitative easing impacts ordinary people.

Just like in the first example, the Federal Reserve conducted $200 billion in quantitative easing by purchasing government bonds from Blackrock using reserves.

Unlike the first example, this time the Treasury was also involved in the flow of funds. To pay for the economic stimulus checks from the Trump administration, the government needed to raise funds by issuing government bonds. Blackrock chose to purchase government bonds instead of corporate bonds. JP Morgan assisted Blackrock in converting its bank deposits into reserves at the Federal Reserve, which could be used to purchase government bonds. The Treasury received deposits similar to a checking account in the Federal Reserve's General Account (TGA).

The Treasury mailed out stimulus checks to everyone, primarily to the vast ordinary populace. This led to a decrease in the TGA balance, while the reserves held by the Federal Reserve correspondingly increased, becoming the bank deposits of ordinary people at JP Morgan.

Ordinary people spent all their stimulus checks on new Ford F-150 pickup trucks. Ignoring the trend of electric vehicles, this is America; they still love traditional gasoline vehicles. The bank accounts of ordinary people were debited, while Ford's bank account saw an increase in deposits.

When Ford sold these trucks, they did two things. First, they paid workers' wages, transferring bank deposits from Ford's account to the employees' accounts. Then, Ford applied for a loan from the bank to expand production; the issuance of the loan created new deposits and increased the money supply. Finally, ordinary people planned to go on vacation and obtained personal loans from the bank, as the economic situation was good and they had high-paying jobs, the bank was happy to provide loans. The bank loans to ordinary people also created additional deposits, just like when Ford borrowed money.

The final deposit or money balance was $300 billion, which is $100 billion more than the $200 billion initially injected by the Federal Reserve through quantitative easing. This example shows that quantitative easing for ordinary people stimulated economic growth. The stimulus checks issued by the Treasury encouraged ordinary people to buy trucks. Due to the demand for goods, Ford was able to pay employee wages and apply for loans to increase production. Employees with high-paying jobs obtained bank credit, enabling them to consume more. $1 of debt generated more than $1 of economic activity. This is a positive outcome for the government.

I want to further explore how banks can infinitely finance the Treasury.

We will start from step 3 above.

The Treasury began issuing a new round of economic stimulus funds. To raise these funds, the Treasury financed through bond auctions, with JP Morgan as the primary dealer using its reserves at the Federal Reserve to purchase these bonds. After selling the bonds, the Treasury's balance in the Federal Reserve's TGA account increased.

Just like in previous examples, the checks issued by the Treasury would be deposited by ordinary people into JP Morgan's accounts.

When the Treasury issues bonds purchased by the banking system, it transforms otherwise useless Federal Reserve reserves into deposits for ordinary people, which can be used for consumption, thereby driving economic activity.

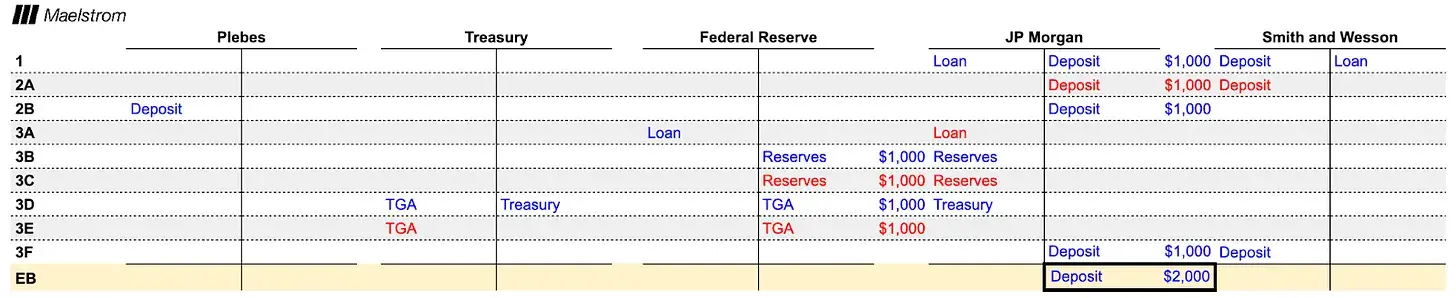

Now let’s look at another T-account example. What happens when the government encourages businesses to produce specific goods and services through tax breaks and subsidies?

In this example, the U.S. ran out of bullets while filming a Gulf War action movie inspired by Clint Eastwood's Westerns. The government passed a bill promising to subsidize ammunition production. Smith & Wesson applied for and received a contract to supply ammunition to the military, but they could not produce enough bullets to fulfill the contract, so they applied for a loan from JP Morgan to build a new factory.

After receiving the government contract, JP Morgan's loan officer confidently lent $1,000 to Smith & Wesson. This loan created $1,000 in funds out of thin air.

Smith & Wesson built the factory, generating wage income, which ultimately became deposits at JP Morgan. The funds created by JP Morgan turned into deposits for those most likely to consume, namely ordinary people. I have already explained how ordinary people's consumption habits drive economic activity. Let’s adjust this example slightly.

The Treasury needs to issue $1,000 in new debt through an auction to fund the subsidy to Smith & Wesson. JP Morgan participates in the auction to purchase the debt but does not have enough reserves to pay for the debt. Since there are now no negative consequences to using the Federal Reserve's discount window, JP Morgan uses its Smith & Wesson corporate debt asset as collateral to obtain a reserve loan from the Federal Reserve. These reserves are used to purchase the newly issued Treasury debt. The Treasury then pays the subsidy to Smith & Wesson, which again becomes deposits at JP Morgan.

This example illustrates how the U.S. government encourages JP Morgan to create loans through industrial policy and uses the assets formed by those loans as collateral to purchase more U.S. Treasury debt.

The Treasury, the Federal Reserve, and banks seem to operate a magical "money-making machine" that can achieve the following functions:

Increase financial assets for the wealthy, but these assets do not generate actual economic activity.

Inject funds into the bank accounts of the poor, who typically use this money to consume goods and services, thereby driving actual economic activity.

Ensure the profitability of certain companies in specific industries, allowing them to expand through bank credit, thus driving actual economic activity.

So, are there any limits to such operations?

Of course, there are. Banks cannot create funds indefinitely because they must prepare expensive equity for every debt asset they hold. In technical terms, different types of assets have risk-weighted asset costs. Even "risk-free" government bonds and central bank reserves require equity capital expenditures. Therefore, at some point, banks cannot effectively participate in bidding for U.S. Treasury bonds or issuing corporate loans.

The reason banks need to provide equity for loans and other debt securities is that if a borrower defaults, whether a government or a corporation, someone has to bear the loss. Since banks choose to create money or purchase government bonds for profit, it is reasonable for their shareholders to bear these losses. When losses exceed a bank's equity, the bank will fail. A bank failure not only causes depositors to lose their deposits, which is already bad, but from a systemic perspective, it is worse because the bank cannot continue to expand the credit volume in the economy. Since the fractional reserve banking system requires continuous credit issuance to function, a bank failure could cause the entire financial system to collapse like a house of cards. Remember—one person's asset is another person's liability.

When a bank's equity credit runs out, the only way to save the system is for the central bank to create new legal tender and exchange that currency for the bank's bad assets. Imagine if Signature Bank only lent to Su Zhu and Kyle Davies of the now-defunct Three Arrows Capital (3AC). Su and Kyle provided the bank with false financial statements, misleading the bank's judgment about the company's financial health. They then withdrew cash from the fund and transferred it to their wives, hoping to shield those funds from bankruptcy liquidation. When the fund went bankrupt, the bank had no assets to recover, and the loans became worthless. This is a fictional scenario; Su and Kyle are good people, and they wouldn't do such a thing ;) Signature made significant campaign contributions to Senator Elizabeth Warren, who is a member of the U.S. Senate Banking Committee. With political influence, Signature convinced Senator Warren that they deserved to be saved. Senator Warren contacted Federal Reserve Chairman Powell, requesting that the Fed exchange 3AC's debt at face value through the discount window. The Fed complied, allowing Signature to exchange 3AC's bonds for newly issued dollars to address any deposit outflows. Of course, this is just a fictional example, but the implication is that if banks do not provide sufficient equity capital, ultimately, society as a whole will bear the consequences of currency devaluation.

Perhaps there is some truth in my assumption; here is a recent news article from The Straits Times:

The wife of Zhu Su, co-founder of the collapsed cryptocurrency hedge fund Three Arrows Capital (3AC), successfully sold her mansion in Singapore for $51 million, despite the court freezing some of the couple's other assets.

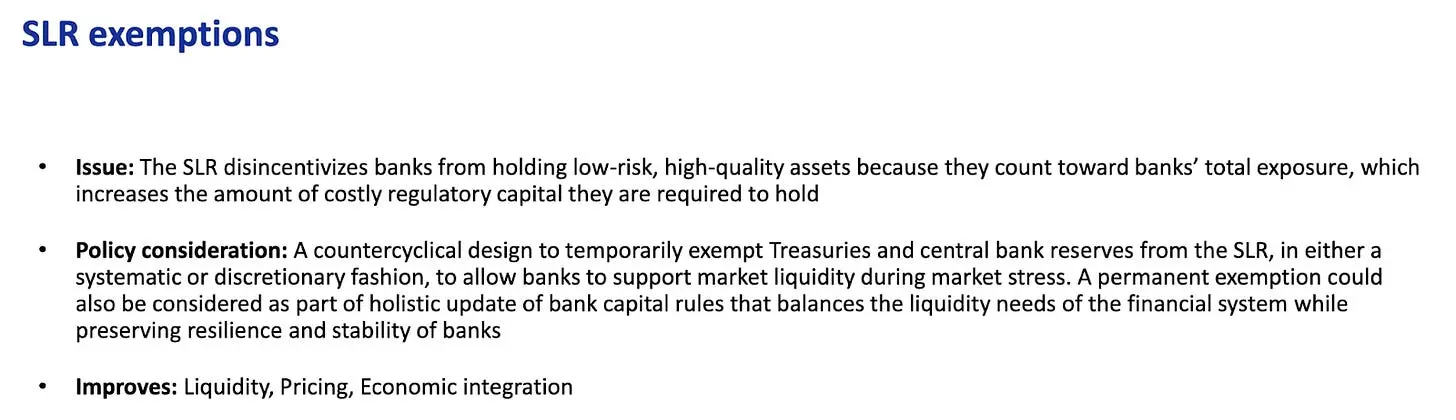

Assuming the government wants to create unlimited bank credit, they must modify the rules so that government bonds and certain "approved" corporate debts (e.g., investment-grade bonds or debts issued by specific industries like semiconductor companies) can be exempt from the Supplementary Leverage Ratio (SLR) restrictions.

If government bonds, central bank reserves, and/or approved corporate debt securities are exempt from SLR restrictions, banks can purchase these debts in unlimited quantities without incurring expensive equity. The Federal Reserve has the power to grant such exemptions, and they did so from April 2020 to March 2021. At that time, the U.S. credit markets were frozen. To encourage banks to re-engage in government bond auctions and provide loans to the U.S. government, the Fed took action because the government planned to issue trillions of dollars in stimulus funds without sufficient tax revenue to support it. This exemption had a significant effect, leading banks to purchase large amounts of government bonds. However, the cost was that when Powell raised interest rates from 0% to 5%, the prices of these bonds plummeted, leading to the regional bank crisis in March 2023. There is no such thing as a free lunch.

Additionally, the level of bank reserves also affects banks' willingness to purchase government bonds at auctions. When banks feel that their reserves at the Federal Reserve have reached the Minimum Comfortable Reserve Level (LCLoR), they will stop participating in auctions. The specific value of LCLoR is only known in hindsight.

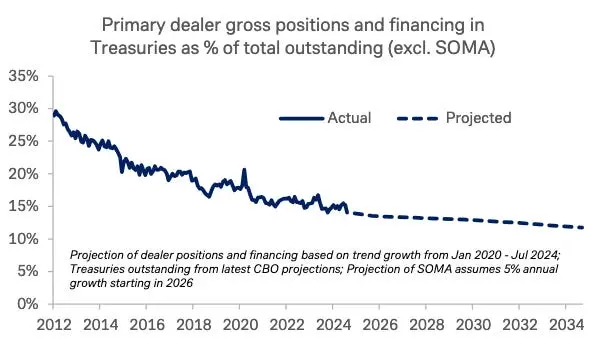

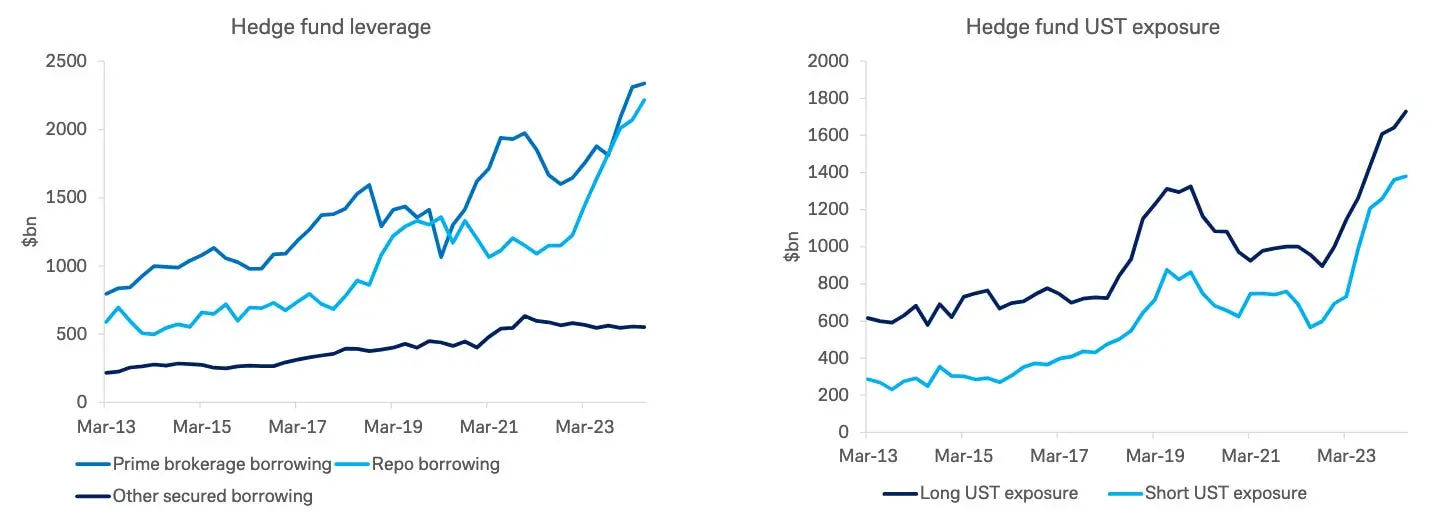

This is a chart from a presentation on Financial Resilience released by the Treasury Borrowing Advisory Committee (TBAC) on October 29, 2024. The chart shows that the proportion of government bonds held by the banking system relative to total outstanding debt is decreasing, approaching the Minimum Comfortable Reserve Level (LCLoR). This raises concerns because as the Federal Reserve conducts quantitative tightening (QT) and surplus country central banks sell or cease investing their net export earnings (i.e., de-dollarization), the marginal buyers in the government bond market become unstable bond trading hedge funds.

This is another chart from the same presentation. It shows that hedge funds are filling the gap left by banks. However, hedge funds are not substantial buyers of funds. They profit through arbitrage trading, buying cash government bonds at low prices while shorting government bond futures contracts. The cash portion of the trade is financed through the repo market. A repo transaction involves exchanging assets (like Treasury bills) for cash over a period at a certain interest rate. The pricing in the repo market when using government bonds as collateral for overnight financing is based on the available capacity of commercial banks' balance sheets. As balance sheet capacity decreases, repo rates will rise. If the financing cost of government bonds increases, hedge funds can only buy more when government bonds are cheap relative to futures prices. This means that the auction prices of government bonds need to fall, and yields need to rise. This is contrary to the Treasury's goals, as they want to issue more debt at a lower cost.

Due to regulatory constraints, banks cannot purchase enough government bonds or provide financing for hedge funds' government bond purchases at reasonable prices. Therefore, the Federal Reserve needs to exempt banks from SLR again. This would help improve liquidity in the government bond market and allow unlimited quantitative easing (QE) policies to be applied to productive sectors of the U.S. economy.

If you are still unsure whether the Treasury and the Federal Reserve recognize the importance of relaxing bank regulations, TBAC explicitly pointed out this need in slide 29 of the same presentation.

Tracking Indicators

If Trumponomics operates as I have described, then we need to focus on the potential for bank credit growth. From previous examples, we understand that quantitative easing (QE) for the wealthy is achieved by increasing bank reserves, while quantitative easing for the poor is achieved by increasing bank deposits. Fortunately, the Federal Reserve provides both of these data points for the entire banking system weekly.

I created a custom Bloomie index that combines reserves and other deposits and liabilities (BANKUS U Index>). This is my custom index for tracking the quantity of U.S. bank credit. In my view, this is the most important indicator of money supply. As you can see, sometimes it leads Bitcoin, as in 2020, and sometimes it lags behind Bitcoin, as in 2024.

However, what is more critical is the performance of assets when the supply of bank credit is shrinking. Bitcoin (white), the S&P 500 index (gold), and gold (green) have all been adjusted by my bank credit index. The values are normalized to 100, and it can be seen that Bitcoin's performance is the most outstanding, having risen over 400% since 2020. If you can only take one measure to hedge against fiat currency devaluation, it is to invest in Bitcoin. The mathematical data is indisputable.

Future Directions

Trump and his economic team have made it clear that they will pursue policies that weaken the dollar and provide necessary funding to support the return of American industry. With the Republican Party controlling the three major branches of government over the next two years, they can advance Trump's entire economic plan without obstruction. I believe the Democrats will also join this "money printing party," as no politician can resist the temptation to distribute benefits to voters.

The Republicans will first pass a series of bills encouraging manufacturers of key goods and materials to expand production domestically. These bills will be similar to the CHIPS Act, Infrastructure Act, and Green New Deal passed during the Biden administration. As businesses accept government subsidies and obtain loans, bank credit will grow rapidly. For those skilled in stock picking, investing in publicly traded companies that produce products needed by the government could be considered.

Ultimately, the Federal Reserve may relax policies, at least exempting government bonds and central bank reserves from SLR (Supplementary Leverage Ratio). At that point, the path for unlimited quantitative easing will be clear.

The combination of legislatively driven industrial policy and SLR exemptions will trigger a surge in bank credit. I have already shown that the velocity of funds from this policy is much higher than the traditional wealthy quantitative easing approach of the Federal Reserve. Therefore, we can anticipate that the performance of Bitcoin and cryptocurrencies will be at least as outstanding as during the period from March 2020 to November 2021, if not better. The real question is, how much credit will be created?

The COVID stimulus measures injected about $4 trillion in credit. This time, the scale will be even larger. The growth rate of defense and healthcare spending has already outpaced the growth rate of nominal GDP. As the U.S. increases defense spending to respond to a multipolar geopolitical environment, these expenditures will continue to grow rapidly. By 2030, the proportion of the population aged 65 and older in the U.S. will peak, meaning that healthcare spending will accelerate from now until 2030. No politician dares to cut defense and healthcare spending, or they will quickly be ousted by voters. All of this means that the Treasury will continuously inject debt into the market just to maintain normal operations. I have previously shown that the combination of quantitative easing and government bond borrowing has a velocity of money greater than 1. This deficit spending will enhance the nominal growth potential of the U.S.

In the process of encouraging the return of American businesses, the cost of achieving this goal will reach trillions of dollars. Since the U.S. allowed China to join the World Trade Organization in 2001, it has actively transferred its manufacturing base to China. In less than thirty years, China has become the global manufacturing center, producing high-quality products at the lowest cost. Even companies that plan to diversify their supply chains outside of China to supposedly lower-cost countries find that the deep integration of numerous suppliers on China's east coast is highly efficient. Even if countries like Vietnam have lower labor costs, these companies still need to import intermediate products from China to complete production. Therefore, relocating supply chains back to the U.S. will be a daunting task, and if it must be done for political reasons, the costs will be exorbitant. I mean that it will require providing up to trillions of dollars in cheap bank financing to shift production capacity from China to the U.S.

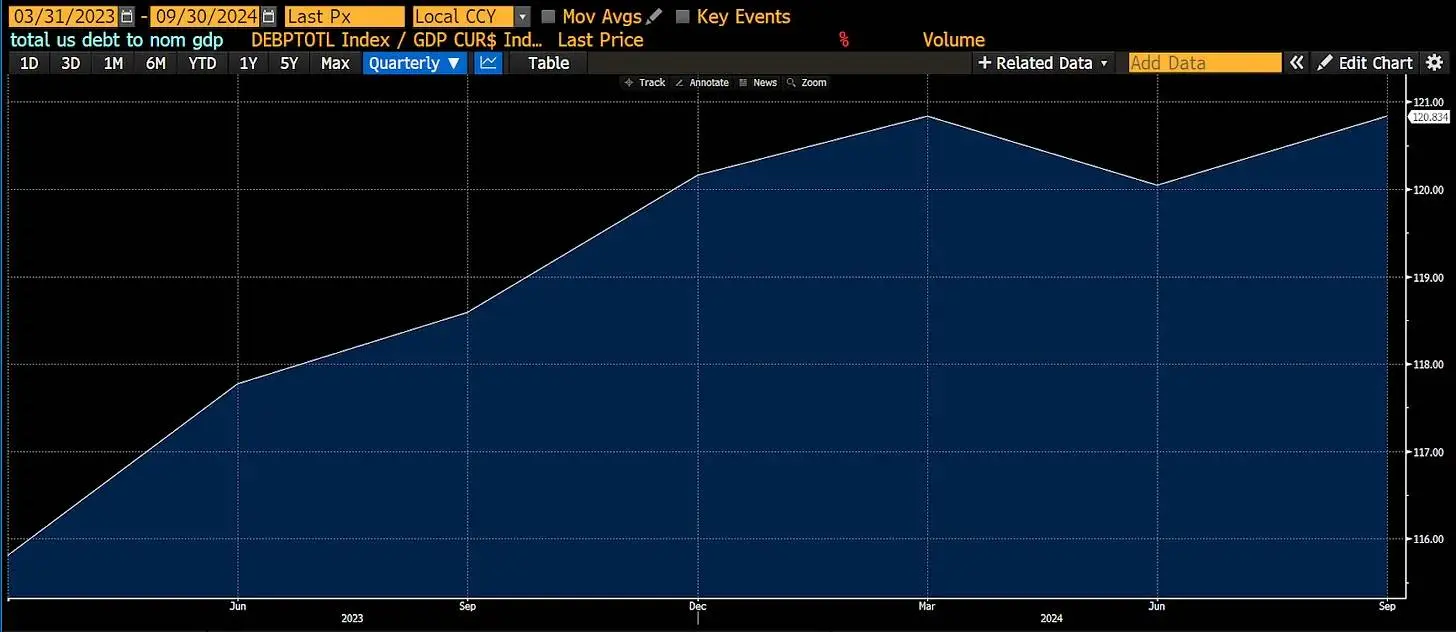

Reducing the debt-to-nominal GDP ratio from 132% to 115% cost $4 trillion. Assuming the U.S. further reduces this ratio to 70% as of September 2008, then according to linear extrapolation, it would require creating $10.5 trillion in credit to achieve this deleveraging. This is why Bitcoin's price could reach $1 million, as prices are determined at the margin. As the circulating supply of Bitcoin decreases, a large amount of fiat currency worldwide will compete to seek safe-haven assets, not just from the U.S., but also from investors in China, Japan, and Western Europe. Buy and hold for the long term. If you are skeptical about my analysis of the impact of quantitative easing for the poor, just look back at the history of China's economic development over the past thirty years, and you will understand why I refer to the new Pax Americana economic system as "American capitalism with Chinese characteristics."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。