In July, Base, this "digital American West," welcomed a major player: SynFutures. As of today, SynFutures has accumulated $26 billion in trading volume on Base, accounting for more than half of the market share in the Base ecosystem's PerpDEX track.

Recently, SynFutures launched the Perp Launchpad platform on Base, pioneering a brand new perpetual contract issuance model.

However, before deconstructing this new toy, we must understand a harsh reality: in the current market environment, the growth of PerpDEX is encountering bottlenecks, and leading players like dYdX, Hyperliquid, GMX, and SynFutures have already divided the profitable perpetual contract varieties among themselves. What remains is either trading volume that is too meager to sustain or has become an arbitrage tool due to low pricing efficiency.

In this context of a segmented track, SynFutures has chosen to take a different approach to gain new growth space.

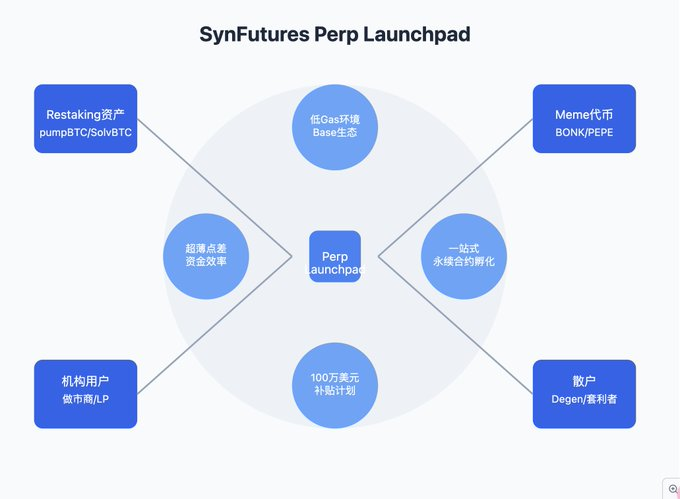

1. Innovation of Perp Launchpad: A One-Stop Perpetual Contract Launcher

Perp Launchpad provides liquidity depth and price discovery channels for the Restaking and Meme tracks through ultra-low Gas environments, ultra-thin spread capital efficiency, and $1 million subsidies, attempting to capture incremental users primarily composed of on-chain Degens, and create a http://Pump.fun for the PerpDEX track.

With just one token, a perpetual contract trading pair can be launched without permission.

The biggest highlights of this model are:

-- Lowering the entry threshold for the perpetual contract market

-- Quickly establishing depth through LP incentive mechanisms

-- Achieving rapid deployment by leveraging Base's low Gas advantages

Taking Lido as an example: the wstETH/ETH perpetual contract was launched only 2 months ago and has achieved:

-- Cumulative trading volume: $260 million

-- Peak TVL: $918,000 -- On-chain transaction count: 132,000

-- User count: 1,955+

2. Investor Perspective: New Sources of Income and Risk Management Tools

For on-chain Degens, SynFutures offers threefold income opportunities:

-- LP market-making income (annualized up to 50%+) -- Revenue sharing with partner communities

-- Expectations for future token airdrops and point rewards

At the same time, it can help on-chain Degens manage Restaking assets and Meme coin risks.

However, caution is advised:

-- The liquidity of the perpetual contract market often exhibits strong cyclicality

-- The price discovery process for newly launched trading pairs may bring significant volatility

-- LP market-making faces the risk of impermanent loss

3. A New Toy for Restaking Enthusiasts

SynFutures has chosen to collaborate with leading Liquid Staking players like Lido, providing a new monetization channel for Restaking assets to some extent. We can foresee:

-- More Restaking assets will be introduced to the perpetual contract market

-- The liquidity of LRT tokens will be further enhanced

-- New Restaking derivative play may emerge

Data from SynFutures reveals an interesting phenomenon: BTC Restaking assets are becoming the new favorites in the perpetual contract market.

The performance of pumpBTC/ETH and SolvBTC/ETH perpetual contracts is particularly impressive:

-- pumpBTC/ETH 24h trading volume: 429.3K, TVL size: 12M

-- SolvBTC/ETH 24h trading volume: 341.8K, TVL size: 5M

The TVL size of these two trading pairs is approaching that of mainstream pairs like ETH/USDC. Why is this phenomenon occurring?

-- The BTC Restaking track is in high demand, and funds need hedging tools

-- The price correlation between native BTC and ETH provides a natural pricing benchmark for these trading pairs

-- Increased competition among Restaking protocols has generated more speculative demand

4. Long-Tail Status of Meme Coin Perpetual Contracts

Surprisingly, Meme coin perpetual contracts have performed relatively average and have not received the same market enthusiasm as spot meme coins, with data not looking very good:

-- BONK/USDC perpetual contract: 24h trading volume 7.7K, market-making depth 405.3K

-- PEPE perpetual contract: Average daily trading volume fluctuates between 5K-10K, market-making depth remains in the range of 300K-500K

-- Other Meme tokens perform even worse

Possible reasons for this phenomenon include:

-- The combination of high leverage and high volatility poses too high a risk, deterring traders

-- The speculative nature of the Meme coin spot market often leads to imbalanced perpetual rates, which are unfriendly to traders

-- The probability and magnitude of impermanent loss are relatively high, requiring LPers to control risk exposure

Conclusion

SynFutures' innovation essentially reshapes the issuance paradigm of perpetual contracts. It is no longer limited to mainstream assets but opens the derivatives market for any token.

The innovation of SynFutures not only lowers the issuance threshold for perpetual contracts but, more importantly, it opens up an important value discovery channel: from "blue-chip assets" like Restaking to "retail favorites" like Meme coins, all can find their market pricing here.

This inclusive strategy, while risky, may be the necessary path for perpetual contracts to enter the mainstream market. After all, in a bear market, sometimes the craziest ideas can create the greatest value.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。