This "free money" game ultimately benefits only a few.

Written by: Dr_Gingerballs, Crypto Kol

Translated by: zhouzhou, BlockBeats

Editor’s note: This article analyzes the unusual impact of the Federal Reserve's interest rate cuts on bond yields, with the core argument being: In the current environment, a rate cut by the Federal Reserve will lead to a decrease in short-term rates, but due to the massive scale of debt and deficits, the market demands higher yields on long-term government bonds to maintain portfolio balance. Additionally, the operations of the Federal Reserve and the Treasury inadvertently transfer public wealth to asset holders, and an economic recession will exacerbate this issue.

The following is the original content (reorganized for readability):

Tomorrow is a key day for the Federal Reserve, with many expecting a 25 basis point rate cut. After the last 50 basis point cut, bond yields rose significantly, which did not surprise me. So, why would a rate cut by the Federal Reserve in 2024 lead to an increase in bond yields?

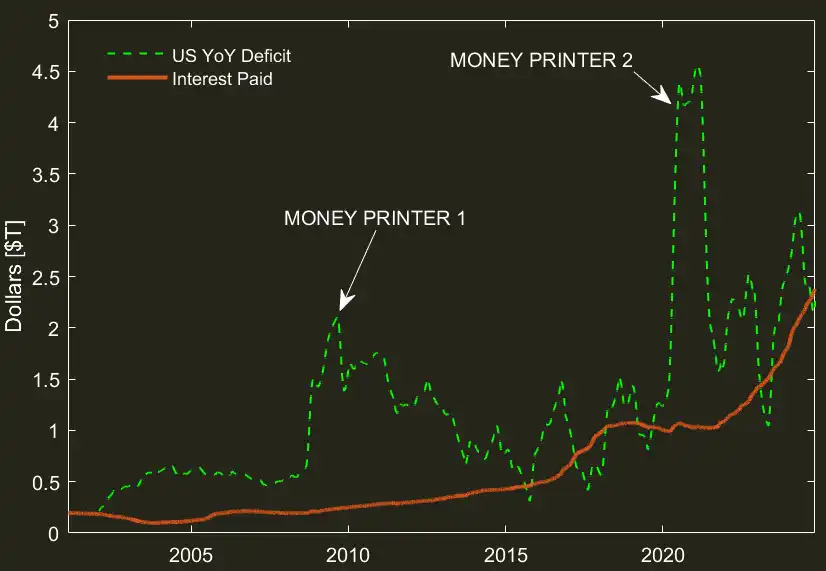

To be concise, I designed a chart to illustrate my point most clearly. The chart shows the annual growth rate of the U.S. deficit and the total interest paid on existing government debt (data directly from the Treasury website). Note that before 2008, the U.S. debt-to-GDP ratio remained between 40-60%, which meant that the private sector (banks) could significantly increase the money supply relative to the public sector, and funds could be used to purchase new debt without worrying about an excessive proportion of government bonds in their portfolios. In fact, issuing government bonds for the market to hold high-quality assets is beneficial.

However, in 2008, the Federal Reserve's "original sin" occurred, and Pandora's box was opened. Faced with a sharp decline in tax revenue, the government spent a large amount of money, and the Federal Reserve monetized it through quantitative easing (QE). People worried this would trigger inflation, but unexpectedly, inflation did not materialize. This laid the foundation for the government's consequence-free massive spending. Thus, the Federal Reserve could buy our debt, keep interest rates low, and avoid inflation penalties? "Free money"!

The government indeed spared no effort in spending. From 2009 to 2013, debt rose from 60% of nominal GDP to 100% and remained at that level until 2020. Many forgot that we had already experienced some inflation issues before the pandemic, and the Federal Reserve was raising rates at that time. By exporting inflation overseas, the benefits we gained gradually disappeared. In hindsight, we have been stepping into a dangerous situation.

In 2020, a new money printing plan began, further confirming the end of our free money era. After the Federal Reserve monetized these expenditures, inflation soared rapidly. No more QE without triggering inflation.

So, what did the Federal Reserve do? They stopped printing money while the Treasury continued to issue debt. This means the Federal Reserve no longer buys these government bonds, which must now be absorbed by the private sector.

Skipping some details, essentially, the Federal Reserve and the Treasury created an environment where they reward debt holders by raising short-term rates and concentrating all debt at the short end. This is good for government bond holders because they can purchase this additional debt, gain cash flow, and bear lower term risk. This equals "more free money."

It is worth mentioning that this free money is a process of transferring wealth from the public to asset holders (the rich). The Federal Reserve raising rates and the Treasury lowering term risk is intentionally directing funds from the poor to the rich. The deficit is borne by everyone, while the interest on government bonds benefits only a few.

But there is a problem. The Treasury must issue a large amount of debt, which means it must be purchased by the private sector (since the Federal Reserve will not take the inflation risk by buying it). However, the private sector wants to maintain a specific bond ratio in its portfolio. The only way to avoid government bonds gradually taking over the entire portfolio is through interest payments.

This leads to the crux of my chart. In an environment where portfolio allocation determines valuation, portfolio allocation is relatively rigid, and overall, bond holders will only buy more bonds if they receive cash flow compensation. The result is that the interest payments on existing debt must balance with the rate of new debt issuance.

The conclusion is simple: interest payments on government bonds must equal the rate of new debt issuance. Currently, the deficit growth is about 6%-7% of nominal GDP, so bond yields must rise to 6%-7% to achieve balance. But remember, if the private sector grows fast enough, some of that money creation can be used to lower bond yields.

Now, back to the Federal Reserve. In an environment where interest cash flow is king, what happens if the Federal Reserve lowers the short-term government bond rates that the Treasury focuses on? Short-term interest payments will drop significantly. So, to maintain portfolio allocation, what will the market do? It will demand higher long-term rates.

Therefore, the first effect of a Federal Reserve rate cut is inevitably to push rates up elsewhere to meet the cash flow needs of bond holders. So we are in a strange world where rate cuts cool the economy (the economy relies on long-term rates), while rate hikes stimulate the economy.

I fully expect the Federal Reserve to cut rates tomorrow, while I also anticipate that the long end of the yield curve will continue to rise, as bond holders will demand returns from their portfolios. Paradoxically, an economic recession will only exacerbate this issue, as the private sector cannot naturally absorb these bond issuances. In contrast, a thriving economy would keep rates at reasonable levels.

I do not envy those who have just been elected into this predicament, as I can almost guarantee they know nothing about these situations. Everything seems fine until it suddenly becomes very bad.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。