In the past few days, both the US stock market and the cryptocurrency market have been dazzled by MSTR. In the latest wave of Bitcoin's market movement, MSTR not only led the rally but also maintained a premium growth over Bitcoin for a period of time afterward, with its price soaring from around $120 one or two weeks ago to the current $247.

Regarding MSTR's explosive growth, most interpretations in the market still revolve around "leveraged Bitcoin." However, this seems insufficient to explain why MSTR's premium suddenly surged despite the fundamentals of "issuing bonds to buy Bitcoin" remaining unchanged. After all, MicroStrategy has been buying Bitcoin for many years, and such a surge in premium has never been seen before.

In fact, the recent surge in MSTR's premium, aside from "issuing bonds to buy Bitcoin," can also be attributed to another secret weapon of MicroStrategy, which has had a tremendous impact on MSTR's fundamentals and has even been referred to by many analysts as MicroStrategy's "infinite money printer," making MSTR "more valuable the more it sells."

Leveraged Bitcoin? A Common Topic

MicroStrategy, as a company focused on business intelligence software, adopted an aggressive strategy starting in 2020: raising funds through bond issuance to purchase Bitcoin. This strategy began in August 2020 when the company announced the conversion of $250 million in treasury reserve assets into Bitcoin. The main motivation behind this strategy was to address challenges posed by declining cash returns and the depreciation of the dollar due to global macroeconomic factors.

To further expand its Bitcoin holdings, MicroStrategy financed itself through long-term bonds in the capital markets in earlier years. These bonds typically have long maturities, most maturing in 2027-2028, with some even being zero-coupon bonds. This allowed the company to maintain low financing costs over the next few years and quickly use the bond financing obtained to purchase Bitcoin, directly adding it to the company's balance sheet.

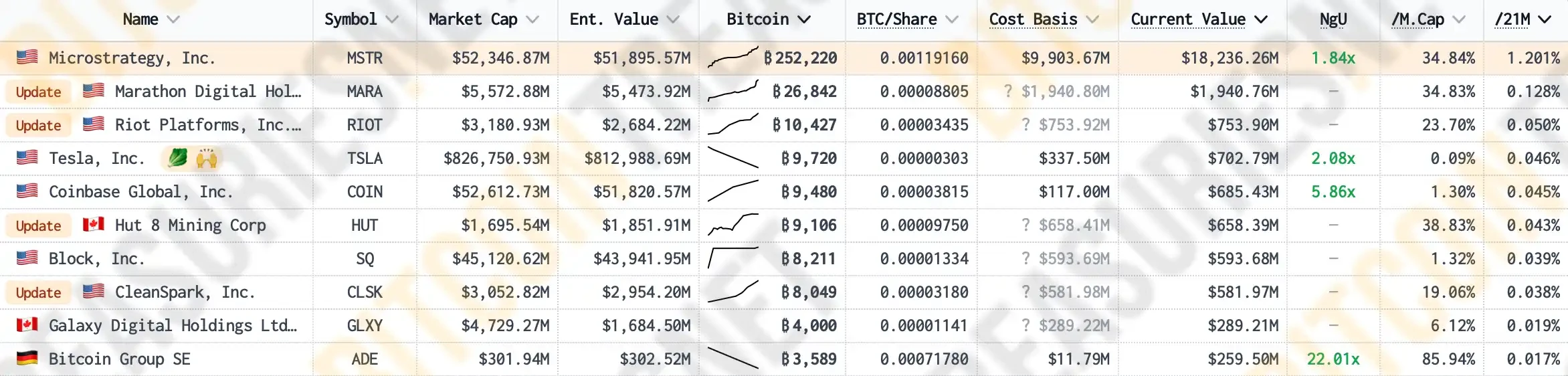

According to data from Bitcoin Treasuries, as of now, MicroStrategy holds 1.2% of the total circulating supply of Bitcoin, making it the publicly listed company with the most Bitcoin globally, far surpassing Bitcoin mining companies like Marathon, Riot, and leading cryptocurrency trading platform Coinbase, which are more "crypto-native" in their business operations.

By financing through bond issuance, MSTR has continuously increased its Bitcoin holdings, which not only increases the number of Bitcoins on its balance sheet but also creates a significant upward pressure on Bitcoin's market price. As the proportion of Bitcoin in MSTR's portfolio continues to rise, the correlation between the company's stock market value and Bitcoin's price further strengthens. According to MSTR Tracker, the correlation coefficient between MSTR's stock price and Bitcoin's price recently surged to 0.365, setting a historical high.

This correlation makes investors willing to buy MSTR's stock while being optimistic about Bitcoin, further driving up the company's market value. Of course, after four years of market and time testing, MSTR's "leveraged Bitcoin effect" has long been a common topic; whenever MSTR's price rises, people always use the logic of "issuing bonds to buy Bitcoin" to explain it.

However, in the recent Bitcoin market, MSTR's market price not only rose ahead of Bitcoin but also maintained an increasingly high premium over Bitcoin for a period afterward. This has left many investors puzzled: why did the premium suddenly spike when the fundamentals remained unchanged?

Premium Issuance: "More Valuable the More It Sells," MSTR's Cheat Code

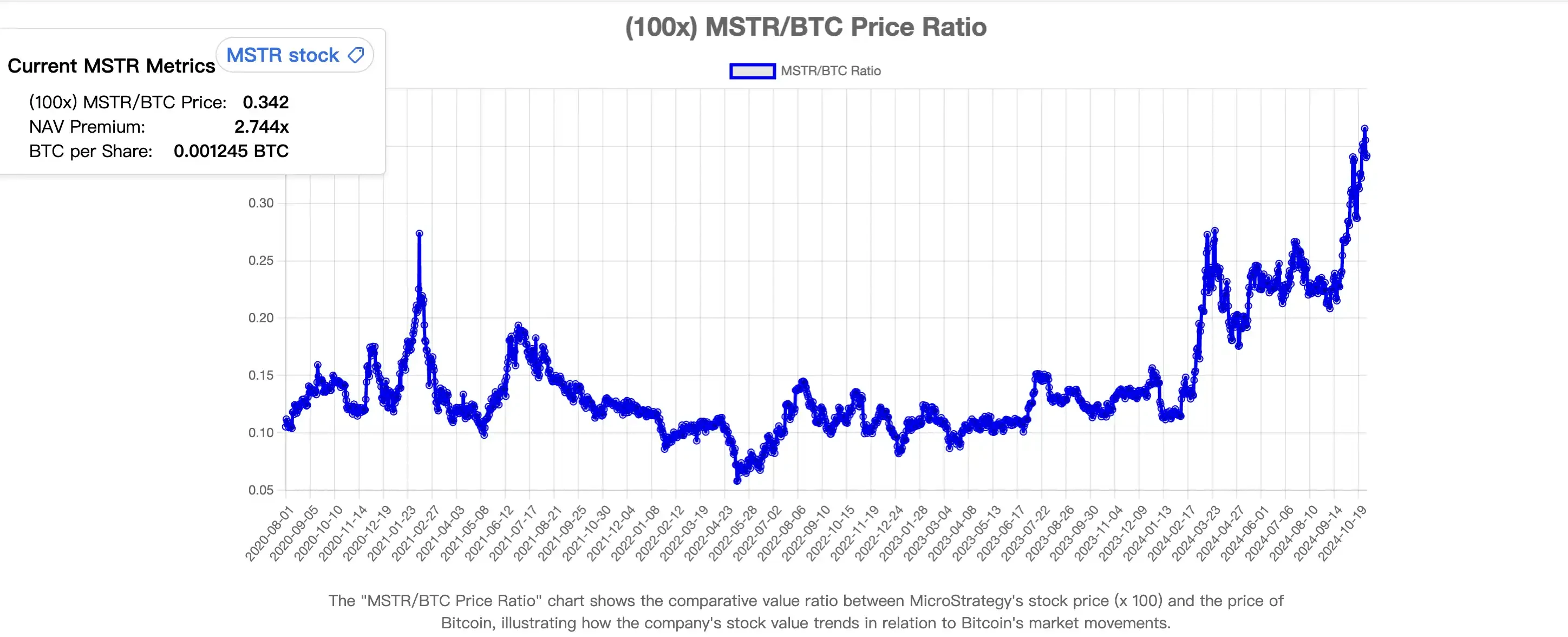

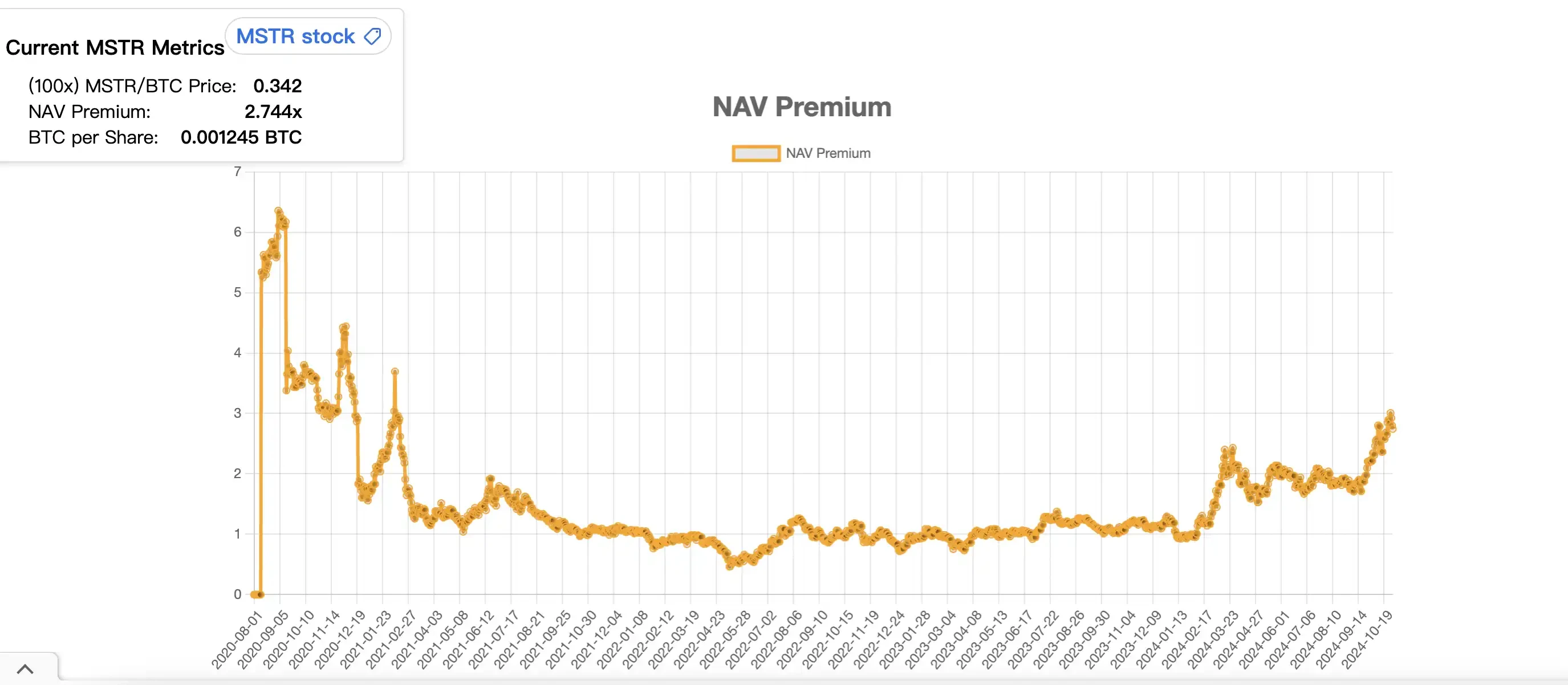

First, let's take a look at how exaggerated MSTR's recent premium has been. According to MSTR Tracker, MSTR's premium over Bitcoin experienced a surge between February and March this year, rising from about 0.95 to 2.43 before falling back to around 1.65. The second rapid increase began just before the recent rise in Bitcoin's price, growing from 1.84 to a peak of 3.04, currently maintaining around 2.8.

It can be seen that although MicroStrategy has been accumulating Bitcoin over the past four years, its NAV (Net Asset Value) premium has not shown significant growth, remaining at a 1:1 ratio for a long time.

So what exactly caused MSTR's premium to surge rapidly? Did the fundamentals of MicroStrategy's "issuing bonds to buy Bitcoin" change?

The answer is: yes. This change in fundamentals is called "premium issuance." Since the latter half of last year, MicroStrategy has adopted a new method of buying Bitcoin, which involves issuing and selling its own MSTR stock to purchase more Bitcoin. This "selling stock to buy Bitcoin" strategy may sound foolish at first, as it could hurt the stock price and even threaten MSTR's market positioning as "leveraged Bitcoin."

However, upon closer analysis of its logical chain, one can find that this new "selling stock to buy Bitcoin" model is essentially MSTR's super flywheel and MicroStrategy's infinite money printer.

First, it is necessary to explain the concept of "Net Asset Value premium" (NAV). Since MSTR holds a large amount of Bitcoin through bond issuance, and the market has strong expectations for Bitcoin's future price increase, the value of MSTR's stock often exceeds the value of the Bitcoin it holds. This premium is referred to as "Net Asset Value premium," reflecting the market's expectations for the company's future expansion of Bitcoin holdings and serving as a support point for MSTR's continuous stock issuance to purchase Bitcoin.

On the other hand, when Bitcoin's price rises, MicroStrategy's market value also increases accordingly, which compels various index funds to increase their purchases of MSTR based on weight considerations, further driving up its price and market value.

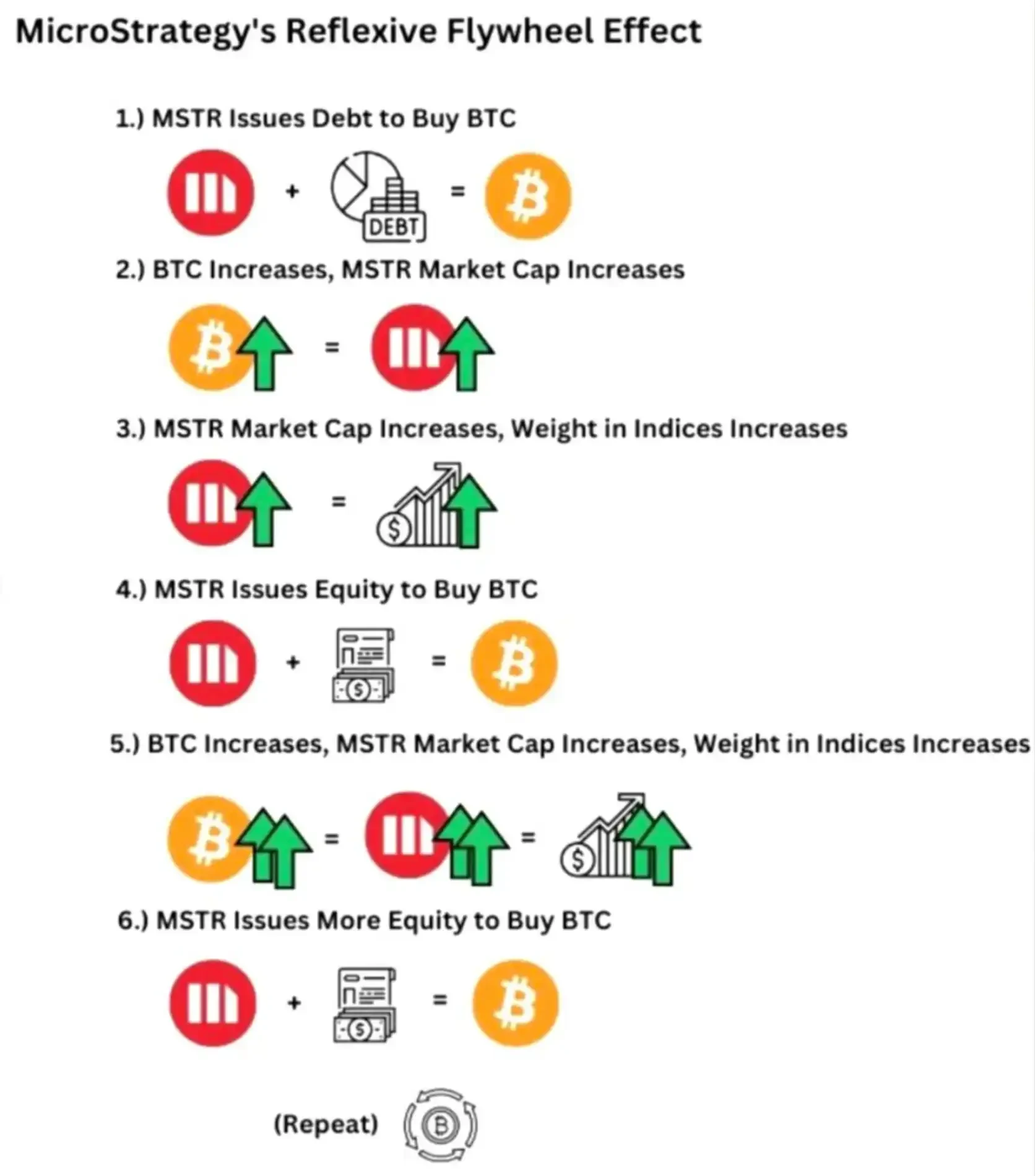

At this point, due to the existence of the "Net Asset Value premium," MSTR can begin its "premium issuance" operation. By continuously issuing stocks, it can obtain more funds to purchase Bitcoin, driving up Bitcoin's price, and the rise in Bitcoin further enhances the company's market value and financing capacity, allowing this cycle to continue. This strategy creates a "Reflexive Flywheel Effect."

In MicroStrategy's "Reflexive Flywheel Effect," the most ingenious point is that the issuance of new shares does not negatively impact MSTR's price; instead, it makes MSTR more valuable.

When MicroStrategy issues new shares to purchase Bitcoin, the newly issued shares are typically traded at a price higher than their net asset value. With this premium, MicroStrategy can acquire more Bitcoin than what each share of MSTR truly represents when selling each share.

For example, if we calculate the correlation coefficient between MSTR and Bitcoin, 36% of the value of each MSTR share symbolizes the Bitcoin backed by the company. Without any premium, when MicroStrategy sells MSTR, it can only exchange for 36% of Bitcoin from the market. However, currently, MSTR's premium over Bitcoin is around 2.74, meaning that every time MicroStrategy sells one share of MSTR, it can exchange for about 98% of Bitcoin.

This means the company can use funds higher than the net asset value of Bitcoin to increase its Bitcoin holdings, thereby expanding its Bitcoin position on the balance sheet. The core of this strategy is that MSTR enhances the speed and scale of its Bitcoin holdings through high premiums, and this speed far exceeds the previous "issuing bonds to buy Bitcoin" speed.

Once the flywheel is in motion, the increasingly high market value of MSTR is also included in the investment scope of US stock indices, attracting more incremental funds and generating more net asset value premiums. Part of the reason for MSTR's decoupling from BTC in the third quarter is also due to the market pricing in that MSTR would be included in the Nasdaq 100 index, bringing in a large amount of passive fund inflow.

US stock index investors will be "forced" to invest in MSTR, returning to the reflexive flywheel, leading to a greater net asset value premium, enabling MSTR to raise more funds to increase its Bitcoin holdings, driving up Bitcoin's price, and enhancing the market's optimistic expectations for MSTR. The company's weight in the index may increase, triggering further buying demand from index funds, forming a self-reinforcing positive feedback loop, overall creating a pressure flywheel for index buying.

From a larger time dimension, the amount of BTC equivalent held by each MSTR shareholder is continuously increasing, which not only enhances the market's recognition of MSTR as a "Bitcoin alternative investment tool" but also raises the pricing expectations for MSTR.

"There Will Be More MSTR in the US Stock Market"

In the past few weeks, MicroStrategy CEO Michael Saylor has become increasingly high-profile, proclaiming on various podcasts and news programs that "there will be more MSTR in the US stock market" and that "MSTR's mechanism is simply an 'infinite financial silver printing malfunction.'"

Saylor believes that MSTR's "reflexive flywheel" model has strong capital operation potential. This model not only continuously accumulates Bitcoin but also maintains its growth through financing and rising stock prices, demonstrating how a publicly listed company can leverage asset premiums and capital market financing capabilities for long-term expansion. This model is not merely a traditional "buy and hold" strategy but an active way to utilize capital market advantages to expand the balance sheet. This mechanism has the potential to become a model for other companies to emulate, especially in resource-intensive or capital-intensive industries. In fact, many companies have emerged that mimic MSTR to engage in partial asset operations.

Currently, this seemingly "left foot stepping on the right foot" model appears to be quite feasible. According to current data, MSTR issues $2.713 worth of stock for every $1 spent on Bitcoin purchases. Many believe that it is leveraging heavily to go long on Bitcoin to significantly "outperform" Bitcoin, but in reality, MSTR is in a very healthy position. It is estimated that MSTR only faces liquidation risk if Bitcoin's price falls below $700.

At present, this mechanism seems to be operating smoothly, with MSTR continuously increasing its BTC holdings. However, as this mechanism becomes more widely used, it will undoubtedly cause US stock indices to be influenced more by cryptocurrency assets and their related derivatives. This mechanism acts like a rope, binding the cryptocurrency market and the US stock market together, leading to profound changes in the market. For the cryptocurrency market, it undoubtedly introduces a large amount of liquidity from US stock funds (mainly absorbed by BTC), while for the US stock market, it seems to exacerbate volatility risks.

According to Saylor's (the founder of MSTR) vision, by the year 2050, the price of Bitcoin will reach $500,000 per coin. He hopes that by then, MSTR will become a trillion-dollar company, better applying itself in promoting the deeper integration of cryptocurrency into people's lives. Whether this seemingly "refined version of a Ponzi scheme" model can operate until that time may require subsequent market validation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。