Next Space invited HighFreedom, a former macroeconomic analyst at a brokerage, to share his trading strategies, insights on the macro economy, and predictions for the future of the cryptocurrency market. With years of trading experience, HighFreedom has a deep understanding of Bitcoin, altcoins, and their relationship with traditional financial markets. This conversation also covered the growth path of novice traders and how to build a systematic trading logic.

All text is for sharing purposes only and does not constitute any investment advice.

TL;DR

I. About Trader HighFreedom

1) What is your trading strategy?

Make money from direction, that is, during a bull market, by holding Bitcoin and not selling, earning from the overall market rise.

Make money from volatility, by controlling leverage, establishing a Bitcoin-based long position when the BTC price falls into a suitable range, and staking Bitcoin to lend out some funds when the price is right, then closing the Bitcoin-based long position to increase Bitcoin holdings when the price rises.

2) Why did you form such a trading strategy?

After experiencing several cycles, HighFreedom believes this strategy aligns better with his risk preference and capital management strategy, effectively avoiding the risk of missing out and reducing holding costs.

In the high-risk, high-drawdown environment of the crypto market, it essentially achieves similar results to high buy-low-sell-high strategies in spot trading. The advantage of the Bitcoin-based long strategy is that it can avoid missing the main upward wave in a bull market, while the downside is that it is leveraged long, which carries liquidation risks, so it is crucial to manage leverage risk effectively.

3) The logic of the trading strategy

Core logic: Combine directional gains with volatility gains, avoiding missing the overall market rise while further increasing Bitcoin holdings through volatility operations. Especially during bull markets, timely use of volatility tools to optimize positions.

Risk avoidance: By using a Bitcoin-based long strategy, HighFreedom reduces the risk of premature selling and missing the market, especially in cases of sudden rapid price increases.

4) Expected returns

Long-term returns: During bull market cycles, this strategy can achieve overall returns of 3 to 5 times.

Drawdown management: HighFreedom expects drawdowns to be controlled at around 20%-30%, with extreme cases possibly reaching 40%.

5) Considerations for implementing the trading strategy

Control leverage: Strictly control leverage levels during trading, especially when prices are high or market volatility is significant. It is generally recommended to keep leverage within 50% to ensure a large safety margin.

Timing: Bitcoin-based longs require choosing the right market timing; this strategy is most suitable for oscillating markets within a bull trend. It is not applicable during rapid upward waves, as the cost of leveraged longs can be very high (for example, in March this year, the funding rate for long BTC even exceeded an annualized 70%), making the strategy less effective, especially in low liquidity conditions.

II. Macroeconomics, US Stocks, and the Crypto Market

1) Why should "crypto people" understand the macroeconomic situation in the US, and what should be the core focus?

HighFreedom believes there are two types of trading entities in the market: on-market participants and off-market participants. On-market participants are usually veterans in the crypto space, often holding more coins than cash, focusing on crypto cycles, popular sectors, on-chain data, and other indicators. In contrast, off-market participants typically enter the market through channels like spot ETFs, characterized by having more cash than coins, viewing Bitcoin as a risk asset, and flexibly entering and exiting based on market liquidity. In the early stages of the market, participants were mainly on-market crypto individuals, and the market was small, so only technical indicators and candlestick patterns needed to be monitored. However, as the market developed, off-market traders' funds began to flow in, significantly impacting the market, thus necessitating attention to US stocks and the overall macroeconomic situation. Similar to how BTC has finally been recognized and married into the wealthy family of US stocks after years of effort.

The US stock market has a pyramid-like structure, from the bottom layer of money market funds and government bonds to the top layer of high-risk, high-reward dream companies, with risk and return increasing step by step. HighFreedom believes Bitcoin's risk and return positioning can roughly be aligned with Russell 2000 and ARKK, possessing certain fundamentals and growth potential, making it a form of digital gold. Altcoins, on the other hand, carry higher risks, similar to high-risk stocks in the US market (like GME and AMC).

2) How to judge the direction of the current altcoin market through US stock logic?

HighFreedom believes that when Bitcoin's price rises to a certain level, some funds in the market may shift towards higher-risk altcoins, triggering an altcoin rally.

The performance of altcoins fundamentally depends on overall market liquidity. If high-risk stocks in the US market, such as ARKK, GME, and AMC, perform well, it indicates ample liquidity, and the altcoin market may also see an upward trend. However, current liquidity is tight, which may suppress the performance of the altcoin market.

He believes the recent market has experienced a deleveraging process both on-market and off-market. The deleveraging on July 4 was mainly a process of on-market deleveraging in the crypto space, while the deleveraging on August 5 was related to off-market (mainly US stocks) funds, which has little to do with the crypto space itself. However, a macro reversal is expected, potentially leading to a new bull market cycle in the fourth quarter. Nevertheless, there are still differing opinions and controversies in the market regarding the future extent of the rally.

3) What steps should novice traders take to learn trading?

Basic learning: HighFreedom suggests novice traders obtain CFA Level 1 certification to systematically learn the fundamentals of financial markets and master key skills such as macroeconomic analysis and industry analysis.

Deliberate practice: Pay attention to market dynamics daily, analyze the reasons behind token price movements, and cultivate market sensitivity and trading intuition. At the same time, learn risk management, especially how to control leverage in volatile markets.

Multi-dimensional analysis: In addition to fundamental analysis of financial markets, attention should also be paid to on-chain data and the fundamentals of different cryptocurrencies, building one's own trading logic and system.

4) What is the Stop Doing List?

Overusing leverage: When trading on-chain, leverage levels must be strictly controlled. The cyclical effects of on-chain trading are significant, especially regarding the behavior of large holders.

Over-relying on indicators: With the emergence of spot ETFs, the effectiveness of on-chain indicators may be weakened, and investors need to continuously adapt to new market logic and changes. In the long run, if macroeconomic logic changes, the indicators investors focus on should also change accordingly.

III. Recommended Traders

1) Fu Peng: From Northeast Securities, has profound insights into US dollar assets, excels in systematic analysis, and enjoys sharing insights.

2) Arthur@CryptoHayes: Has in-depth knowledge of the US macro economy; although the language in his articles can be complex, his viewpoints are valuable for reference.

3) Victor@VictorL1024: A fund manager, veteran in the crypto space, early miner, with unique perspectives on the market.

4) Bperson sunong@BensonTWN: A veteran from the last bull market, providing key cyclical indicators that are helpful for trading.

Dialogue Record

FC

Today we have HighFreedom with us. Initially, we wanted to build an investment research system within our fund. We have been looking to talk to people who have previously worked in brokerages or traditional financial institutions and have experience in research to learn how to build this system. That's how we got to know each other. We have chatted a couple of times, and since we come from different perspectives, it has been quite rewarding. So today, we would like to ask you to share your views on the entire market and some thoughts on the future. We believe this is the main purpose of this dialogue. How about you start with a brief introduction about yourself, and then we can move on to the next part?

HighFreedom

Sure, sounds good. Host, good evening everyone. Thank you for the invitation today. I have been listening to your weekly dialogues with friends, and I find the quality quite high. My background is that I worked as a macroeconomic analyst at a brokerage. In 2016, while studying in Singapore, I was introduced to cryptocurrency. So, I have been in this market for about seven to eight years. You could say I am a notorious crypto trader or a cryptocurrency investor. Today, I am here to discuss how this market seems very different from when I first joined in 2016 and 2017, as well as from 2021. So, I would like to chat with everyone about this. Is that okay?

FC

Could you first talk about your trading logic? What does your trading strategy look like?

HighFreedom

Sure. I believe everyone has different risk preferences, acceptable profit-loss ratios, and capital positions. Let me share my situation. After several bull markets, I find that the best operating logic for me is to earn two types of money during a bull market. The first is directional money. Directional money means you clearly know you are in a bull market. Earning directional money is simple: just hold onto Bitcoin, regardless of whether it goes up or down. The second is volatility money. A straightforward approach to volatility money is that when I think the price has risen enough, I sell some of my spot holdings and wait for a dip to buy back, continuously doing this to lower my holding costs. This Bitcoin-based logic suits me better, which is to earn from volatility.

Considering all directions, I think if the price drops to a good position during a bull market, I will go long based on Bitcoin. When the price returns, I will close that portion of the position. This way, during the bull market, I am doing one thing: making my Bitcoin holdings increase, aiming to sell at a good price near the market peak. That's basically my thought process. So, it is more of a Bitcoin-based logic.

Another question is why make it so complicated, with both Bitcoin-based longs and contracts. The thing is, everything has its pros and cons. The advantage is that there is no so-called risk of missing out. Because after experiencing several market changes, you realize that this market is like this. You clearly know the bull market hasn't ended and is still running, but if you unload some spot holdings, the risk of missing out is quite significant. The market's rise, based on historical data, can achieve a 20% to 30% increase in just one to two weeks. This is especially true for Bitcoin, so sometimes if you unload leverage and some spot holdings, it can be quite awkward, and you might miss out suddenly. After holding for a long time and experiencing a lot of fluctuations, it suddenly rises. So, in short, the best operating logic for me is to go long based on Bitcoin, earn as much directional money as possible, and if I can earn from volatility, I will; if not, I will just hold. That's the situation.

You mean that when you go long based on Bitcoin, you find a relatively low point and just keep opening long positions, right?

HighFreedom

Yes, for example, recently when it dropped to around 50,000, the lowest was about 48,888. In the crypto market, after the spot price drops, it might slowly stabilize. If I have, say, one Bitcoin when the price is at 52,000, 53,000, or 54,000, I can use that Bitcoin as collateral to borrow, say, 0.5 Bitcoin. This way, the leverage is around 50%, and the liquidation price would be around 20,000. Once the price goes up, I can gradually close the position, and one Bitcoin might turn into, say, 1.05 Bitcoin, allowing me to earn a bit from the volatility. That's the operational logic—going long based on Bitcoin. Most people use USDT for long positions, but I prefer to use Bitcoin as collateral.

FC

I understand. If that's the case, what do you think is a suitable capital size for this kind of operation?

HighFreedom

I think if you want to reach a million level, it might be easier, but it also depends on everyone's expected returns in this market. If you hope to achieve a hundredfold return, then I think this operation is completely unsuitable. This operation is more like taking Bitcoin during a bull market when you feel bored and have nothing to do, and when a good opportunity arises, you definitely want to go long to increase your Bitcoin holdings. So, if you look at it this way, for example, if you go long at 50,000 with 50% leverage and it rises to 60,000, that's a 20% increase, and the money we earn is 20% of that 50%.

After a series of operations, your entire position could change from one Bitcoin to 1.1 Bitcoin, which is a ten percent increase. So, I think it really depends on everyone's expectations. Even if I have 100 dollars, I can do this kind of operation. However, those with 100 dollars might not just think that a two to three times return from a bull market is enough; it might not be enough at all. That's the situation.

FC

Got it. What do you expect your returns to be?

HighFreedom

I think over one cycle, the worst-case scenario might be three to four times, while the best-case scenario could be four to five times. High returns are certainly what everyone desires, but in my case, it's hard to say. To supplement alpha, you can only use small positions, while you need to maintain a large position to secure beta. Speaking of drawdowns, since my operation involves leverage, if the leverage is set at a midpoint and the market accelerates downward, my net worth will decline rapidly, with the maximum drawdown possibly controlled around 40%. This is the worst-case scenario I hope to avoid. However, after several cycles, experienced traders generally manage to open positions at reasonable levels, so it's not too extreme. I think a drawdown of 20-30% is something I'm used to, and it's not a big deal. That's how it is.

FC

Understood. If someone wants to adopt your trading strategy, what key skills do you think are necessary, aside from timing?

HighFreedom

I think the primary skill is controlling leverage. After eight years of experience, I believe this is the most important point. Because later we might also discuss that, looking at various assets around the world, the crypto market consists of high-risk or ultra-high-risk assets that can bring you several times or even dozens of times returns. But at the same time, the drawdowns are also very significant. Friends who experienced the last cycle might remember situations like March 12; if you were long Bitcoin with 2x leverage and the position was wrong, you could get wiped out, especially if you went all-in. Logically, going long Bitcoin with 2x leverage should be something crypto people would consider conservative, but in extreme situations, you could still get wiped out. So, I feel that controlling risk is crucial. For example, if I have 100 Bitcoins, I would only open a position of about 40% at most. In extreme situations, if I feel the position is very good, I might go up to around 50%, ensuring a very low liquidation price. I think that's the most important thing.

Secondly, this strategy has its limitations. As you may have heard, essentially, going long based on Bitcoin means borrowing coins from the market. In a cooler market, the annualized return for Bitcoin-based positions on Binance might be around 7%, 8%, or 9%, which I think is completely acceptable. However, when it reaches the peak of a bull market, like in March this year, going long Bitcoin with leverage becomes less suitable. Because at that time, the funding rate for long Bitcoin on Binance had already exceeded an annualized 60% to 70%, which is extremely high. When the market is sideways, the cost is too high to bear. So, I think one needs to control the position size and liquidation price, and also consider when to enter the market. Doing this kind of operation during a hot market is generally not feasible. That's about it.

FC

I understand. Because I have discussed a lot offline about your understanding of traditional markets, or the emergence of ETFs. You have also mentioned many changes in our industry, so I think we can talk about the specific logic of your trading strategy. I believe the first factor affecting prices in this cycle is the on-market and off-market factors, right? I think we can start discussing this.

HighFreedom

Sure, no problem. Speaking of this, let me share my growth experience, which also helped me build my own analytical system. In 2016 and 2017, I was still studying in Singapore, and during a dinner gathering, everyone was discussing ESO and the 49 super genesis nodes. I might be mentioning things that new friends haven't heard of, but everyone was very excited back then.

At that time, I felt that the market was relatively small. Basically, only pure crypto people were playing with this stuff, and there were very few funds or people from other markets participating. So, I felt that it was a very primitive market. It was enough to simply look at various technical indicators, candlestick patterns, such as momentum, volume, trading volume, MACD, and so on, including daily charts, EMA, and the Vegas channel. That was basically the situation back then.

Fast forward to the last bull market in 2021, I felt that just looking at these things was not enough. While it was useful, it gradually became insufficient. Because last time, we had limited time, but I have a strong impression of the last bull market. If you participated, you might remember that it had a double top; in April 2021, there was a top around 64,000 to 65,000, which I remember was on April 14. In the second half of the year, there was another top around November, with a spike reaching 69,000. In fact, there was a clear situation: if you looked at the most commonly used data websites, like Glassnode, you would see what happened.

In the first half of 2021, I defined that peak as the spot top, which was a point where long-term holders in the crypto space were continuously selling. However, the peak in the second half of 2021 was basically unrelated to the crypto space; from an on-chain perspective, it didn't have much relevance. The peak in the second half was driven by off-market factors, with a large influx of liquidity at a very high point. The Nasdaq index was also soaring, and dollar liquidity was increasing, which caused Bitcoin to rise as well. So, I simply defined the top in April 2021 as the spot top, while the November peak was the contract top, which was basically driven by off-market contracts without much spot involvement.

So, my feeling is that towards the end of the last cycle, off-market participants began to try to dominate and participate in this market. This time, it is even more evident. A landmark event that everyone might know is that on January 11, after the approval of the US stock market's spot ETF, the Bitcoin market finally built a bridge to the vast river of US stocks.

In fact, after all this discussion, I think the current situation is as follows: there are two types of participants in this market. The first type is called on-market participants, which I believe includes many of you listening now—experienced traders and long-time crypto enthusiasts. The typical characteristics of these people are that they hold a lot of coins. If you look at the current situation with the US spot ETF, it has been around for more than half a year, and it has bought less than 5% of Bitcoin—around 4.7% to 4.8%, which is less than 1 million Bitcoins. About 94% of Bitcoins have already been mined, and if you consider that 20% of Bitcoins have been lost, it can be conservatively estimated that around 60% of Bitcoins are still in the hands of crypto participants. So, the first type of participant in this market is the on-market participant. Another typical characteristic of these people is that they hold a lot of coins but have relatively less money compared to the second type of participants, which are off-market participants who come in through spot ETFs. Their money is compliant money; they are not allowed to buy USDT on Binance and then buy coins. They typically use currencies like USD, HKD, AUD, JPY, etc. The big money in this wave has a typical characteristic: they have a lot of money. These funds, especially actively managed equity funds, can easily reach hundreds of millions or even billions of dollars. These people have a lot of money but relatively few coins. So, I think the current market is composed of these two types of participants.

In this situation, both types of participants are forced to pay attention to each other's perspectives. On-market participants may focus more on the original cycles, on-chain conditions, long-term holders, and short-term holders in the crypto space. In contrast, off-market participants are more likely to define Bitcoin as a risk asset. When liquidity is abundant, they rush in. When liquidity is tight, they retreat, and risk assets tend to decline. So, I think this is also why when we discussed the other day, I felt it was important to look at both on-market and off-market perspectives to gain a more objective and comprehensive view of the overall situation. I hope everyone can understand this.

FC

OK. So, have you looked into the on-market and off-market situations? Especially regarding the new off-market participants, how much are they allocating, or what is their overall allocation logic?

HighFreedom

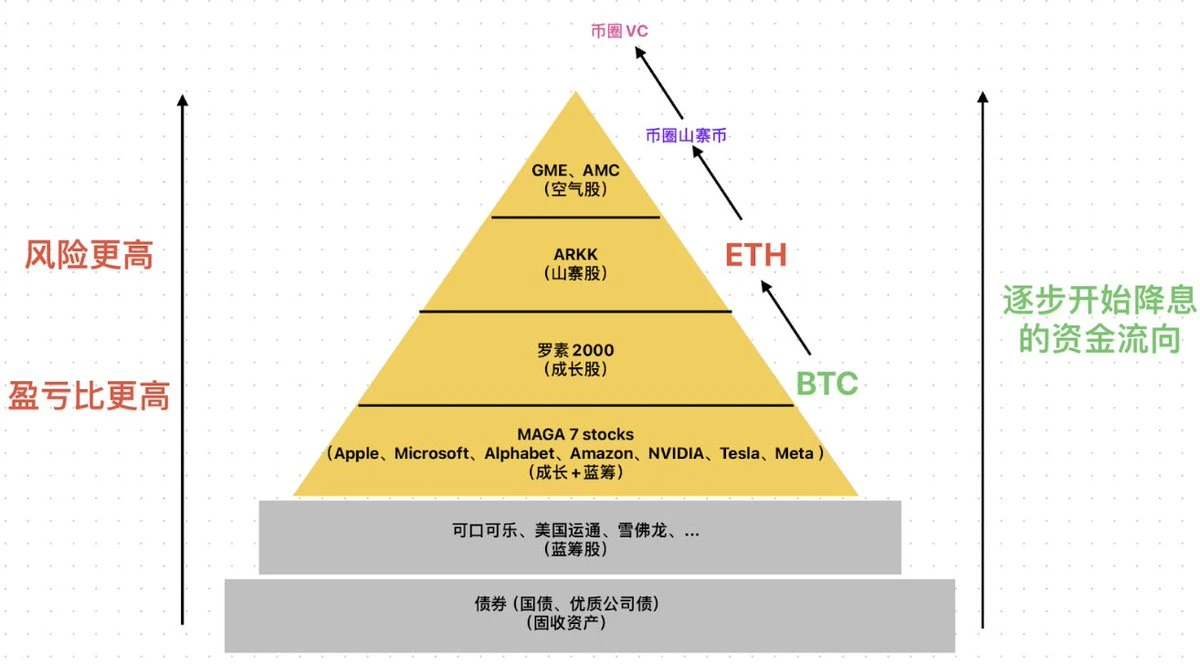

I understand, and I think this point is quite clear. After the launch of the US spot ETF, the definition of Bitcoin now and in the future has become quite clear. Bitcoin can now be defined as a growth-oriented digital gold. If you talk to those off-market participants about layer two, minting inscriptions, or meme coins, they won't understand or care about those things. They only understand and recognize one thing: digital gold, and specifically, a growth-oriented digital gold. This also explains why, in their eyes, Bitcoin is now seen more as a high-risk asset. After all, it has high volatility, and its market cap is still far less than gold, currently accounting for about 7% to 8%. So, it is a growth-oriented asset. Sometimes, people discuss what Bitcoin really is; my understanding is simple: Bitcoin is a growth-oriented digital gold, and at present, it is a risk asset with high growth attributes, but it also carries high risks. In the US stock market, I happened to draw a pyramid the other day.

Speaking of this, let's look at how the funds in the US stock market perceive the world. First, let's visualize a pyramid. I can't project it, so I'll describe it to you. The pyramid looks like this: at the bottom layer, there are assets with very large capital capacity but relatively low returns and low risks, such as various money market funds and some American equivalents of Yu'ebao. They invest in overnight repurchase agreements and short-term government bonds, currently yielding around 5.1%, 5.2%, 5.3%, or 5.4%. This category of money market funds is definitely at the base of the pyramid.

Moving up a layer, we have US Treasury bonds, including short-term, medium-term, and long-term bonds.

Next, we have stocks, which also vary. The lowest tier here includes the types of stocks that Warren Buffett loves, such as Coca-Cola, Unilever, Goldman Sachs, and JPMorgan. Do these companies have any grand dreams? Not really; they are industry leaders with strong profit-making abilities, often referred to as cash cows.

Going up another layer, we find companies with dreams, typically large American tech companies, often referred to as the "mega 7" or the "seven brothers." What characterizes these seven stocks? They have very strong cash flow and solid fundamentals. Companies like Google and Apple are incredibly profitable. However, they also have a certain vision; compared to Coca-Cola, they have aspirations that point towards the future of humanity.

Next, we have the Russell 2000, which consists of 2,000 small companies in the US. Some of these companies are profitable, while others are not, and they come from various industries without strong stable cash flows. However, these companies may have bigger dreams, which is why they are categorized as weak cash flow but strong dream entities.

Moving up another layer, if you recall 2021, the most talked-about figure wasn't Nvidia or Apple; it was Cathie Wood, known as "Woodstock." Her fund, particularly the ARKK fund, became very famous.

What is ARKK? It represents very typical human dream-type enterprises. Under it are sectors like telemedicine, implantable chips, and super nuclear fusion, which may take 50 to 100 years to realize, but they are ambitious visions for the next 10 to 20 years.

Going up another layer, we have the "Roaring Kitty," who recently emerged again. What was he rallying people for? Stocks like GME and later AMC, which are mini stocks in the US market. These are not much different from the meme coins like PEPE and Dogecoin in our crypto space; they lack solid fundamentals.

As I mentioned earlier, the lower you go in this pyramid, the larger the capital capacity, but the lower the risk and returns. Conversely, the higher you go, the smaller the capital capacity, but the higher the potential returns, albeit with greater drawdowns. This structure represents the entire US market. As Bitcoin integrates into this market, we need to consider where it fits in this pyramid. I believe no one can definitively say where it belongs. We are still exploring and figuring it out. However, placing it alongside Apple or Google seems difficult, and putting it in the realm of AMC or GME, which are purely speculative, also seems challenging. I think its position is likely somewhere between the Russell 2000 and ARKK; it has fundamentals, is considered digital gold, and is a good growth asset.

Digital gold has aspirations. But can we say it is purely speculative or worthless? Not at all; it is a valuable asset with certain risks and fundamentals. This is how I believe participants in the US market view Bitcoin. In the last cycle, our perception was different. Market participants viewed Bitcoin as a speculative asset with extremely high risk and volatility, similar to AMC or GME during times of excess liquidity. However, this time, their understanding has changed, and they recognize that Bitcoin is a good asset with fundamentals, a solid digital asset.

Digital gold has not yet fully matured, so discussing this gives us an overall market structure, a pyramid from the off-market perspective. With this understanding, we can move on to the next point, which is quite simple: the less money people have, the fewer dreams they have, leading them to invest in money market funds and short-term US Treasury bonds. If they have a bit more money, they might pursue dreams by investing in large tech stocks. The more money and dreams they have, the higher they can climb.

We might also discuss the issue of interest rate hikes and cuts. I remember a metaphor from a friend that resonated with me. He said it’s like the ebb and flow of rivers and streams. What does that mean? When the tide recedes, the small streams dry up first, and then the water level in the larger rivers drops. Conversely, when the tide rises, the larger rivers fill up first, similar to how in our crypto space, we first see Bitcoin being traded, then Ethereum, and finally altcoins, leading to the emergence of various meme coins. So, I think this is a broad positioning. I want everyone to understand that off-market participants view things this way.

As for Ethereum, it might be positioned even higher. If Bitcoin can be defined between the Russell 2000 and ARKK, which have some dreams and fundamentals, then Ethereum's definition should be even higher.

Moving up another layer, for example, altcoins in the crypto space, their risk level or liquidity overflow must at least reach the heights of stocks like GME or AMC to take off. For those listening who have stock trading software, you can check ARKK and GME while listening.

Look at these two stocks and see when they surged during the last cycle in 2021. You might be surprised to find that their movements closely align with the bull market in the crypto space.

You will see that ARKK, which is a fund, peaked at around 150 to 160, which is quite exaggerated. It surged several times in a short period, and GME also saw massive increases, comparable to the gains of many altcoins in the crypto space.

This illustrates that as off-market participants enter the market with significant capital, you have to engage with them. You need to understand their situation. So, I want to provide you with a useful reference point. Look at the situation with ARKK and GME. If you suddenly notice that these two stocks are soaring, there’s no reason why altcoins in the crypto space wouldn’t also take off. This essentially represents a massive overflow of dollar liquidity. I’ve said quite a bit, but this is the overall logic and framework.

FC

Understood. We’ve discussed this offline a couple of times. Recently, there has been quite a bit of volatility, but if you look at the prices, it’s basically a wide range of fluctuations. Many analyses have been made, such as regarding the yen and expectations. So, what do you think is behind this volatility, and do you believe the upcoming quarter's elections will bring any market movements? What is your logic from a traditional finance perspective?

HighFreedom

I see it this way. Let me recap for you. Today is August 22. I want to review the significant drops in July and the recent drop in August. These events correspond to what we’ve been discussing about on-market and off-market dynamics.

What happened on July 4? There were reports about the German government selling coins and that Mt. Gox was starting to make payouts, etc. That day was significant; I remember it well—it was a Thursday.

What was happening in the US on that day? It was Independence Day, and the markets were closed. The liquidity was very weak; there were no buyers or sellers. If someone wanted to push the market down, they could easily do so. This led to a hard sell-off, and the US stock market, gold, and US Treasury bonds showed little volatility.

So, the drop on July 4 was a very typical case of an on-market decline, a cleansing of leverage within the crypto space. It was a beautiful example of leverage being cleared out, and I observed that the liquidation volume was quite high. After clearing out a lot of leverage, we could see that the major players in the market were either buying spot or increasing their positions in Bitcoin-based longs.

Now, the drop on August 5, I believe, had little to do with the crypto space. That day was a Monday, and the drop was primarily due to all valuable assets in the off-market declining. For example, Nvidia saw its largest drop, if I remember correctly, around 13% to 14%, while Bitcoin itself dropped 17% to 18%. I think that’s already quite significant for Bitcoin. Apple dropped about 7% to 8%, and Google dropped about 8% to 9%. The entire Nasdaq fell nearly 10%, so I think Bitcoin's drop of 17% to 18% was quite reasonable. Therefore, I believe July was a cleansing of leverage on the on-market side, while August was a cleansing of leverage on the off-market side.

Now, let’s discuss what happened in August. This ties back to the pyramid structure I mentioned earlier. Remember that the higher you go in the pyramid, the more speculative those stocks become, and when liquidity increases, their prices rise significantly. Conversely, when liquidity recedes, those stocks tend to drop sharply or languish at a bottom for a long time. Look at GME, AMC, and ARKK; they all exhibit this kind of trend.

So, the drop on August 5 was just a significant decline. I want to review this systematically. People might talk about the carry trade related to the yen and its impact, etc. I want to clarify that if we must identify a cause, my understanding might account for about 20% to a maximum of 30%, but definitely not more than that. There are fundamental underlying reasons for historical events, as well as surface-level direct triggers.

The direct trigger at that time was quite simple: August 5 was a Monday, and the economic data released on August 10 and August 2 was very poor, with unemployment rates far exceeding expectations. This led to a significant increase in expectations for interest rate cuts, causing the yen to appreciate unexpectedly.

The brothers who were borrowing yen to speculate on US stocks were lying there doing nothing, and suddenly their profits were swallowed up by the appreciation of the yen. In this situation, they were forced to start closing their positions painfully, selling off one after another. This is the direct surface reason, a sudden deleveraging. But in reality, I believe the deeper reason for this story needs to be understood from the beginning, which I will define as the starting point.

In March 2020, what happened? Friends in the crypto space will remember that on March 12, there was a significant drop, with Bitcoin falling from $10,000 to around $8,000, then dropping again to the $7,000 range, bouncing back to $8,000, and finally plummeting to a low of around $3,600 or $3,700. However, if you look around, you will find that on March 10, the US stock market began to experience circuit breakers, with the S&P 500 and Nasdaq indices both facing similar situations. Warren Buffett even stated that in his lifetime of investing, he had never seen such a large drop.

So what was the situation? It was quite simple; this person was sick. In March of that year, this individual fell ill. People talked about liquidity issues; the entire pandemic led to a lack of liquidity, causing all valuable assets to drop and resulting in a massive deleveraging across the market. So, this person was sick. Now, treating the illness is straightforward. I want everyone to understand two things: the doctor treating this illness is the central bank, specifically the Federal Reserve of the United States.

Historically, no central bank in any country has escaped these two characteristics. The first is called decision lag. It’s not that I predict you will get sick and take preventive measures. I think you might catch a cold, so I give you something to boost your immune system. No, it’s not like that. It’s only when this person is already sick that they start to think about what actions to take. So, all central banks share this first major characteristic: decision lag.

The second characteristic is the excessive dosage. What does this mean? When you are sick, the medicine prescribed should be just the right amount, say 10 milligrams, but instead, they prescribe you 200 milligrams. So, what happened back then? After this crisis occurred and this person fell ill, the Federal Reserve began to treat the illness, but their decisions were lagging, and the dosage was excessive.

Therefore, when we look back, we can see what types of assets began to take off in 2020. The top of the pyramid we mentioned earlier, whether it was Bitcoin, Ethereum, altcoins, or speculative stocks in the US market like GME and AMC, or fundamentally dream-type stocks, ARKK took off.

Let’s look at ARKK, which is the most typical example. In the first half of 2021, ARKK reached its peak for that year, and throughout 2021, it experienced high volatility but ultimately trended downward. This is a very clear feeling: it’s called the diminishing effect of the medicine. After taking an excessive dose, the first thing to reflect this is that there is too much money in the market. If you tell me to buy Nvidia and double my investment, I find that uninteresting. If you tell me to buy Apple and we make 60%, I think that’s not exciting. I want to play with things that can multiply by five, ten, or a hundred times.

The same situation occurred in the US stock market in 2021. As interest rates gradually increased and the balance sheet was further reduced, quantitative tightening began to actively shrink the previously excessive liquidity. You will find that the overall risk appetite in the market gradually decreased. Eventually, what happened? The market style shifted from AMC and GME rising to ARKK rising, and ARKK basically stopped moving.

Once it started to decline, the market style switched to stocks like the S&P 500, which includes the top 500 stocks in the US market. You will notice that the S&P 500 struggled to rise, and only the S&P 100 was increasing. Later, when the S&P 100 also struggled, it became that only the mega seven stocks were rising. These include Microsoft, Nvidia, Google, and Apple. Eventually, it was found that only Nvidia was rising. This is a very clear indication that the excessive dosage is gradually being withdrawn. The quantitative tightening process is slowly pulling back the excess liquidity, and there will always be a turning point.

At this time, I understand that the fundamental reason for the significant drop on August 5 lies in the continuous retreat of liquidity. Even risk assets with some dreams but basic fundamentals could not rise anymore. Eventually, the market style had to switch, and this often accompanies a severe deleveraging.

Later, what did we find? Friends who speculate on US stocks, especially those involved with Nvidia, were very evident by July. Most of them were highly leveraged, buying various call options. As Nvidia's volatility decreased, these individuals found it uninteresting and began to increase their leverage, which brought them closer to a deleveraging situation.

I also want to recommend something else to you. This is something I think you can keep on your list even if you don’t trade stocks: the VIX, known as the fear index or volatility index. You will see that with the market's sharp declines, adjustments, or significant style shifts, the VIX will quickly rise from a very low point to a high point, indicating that market volatility has increased. After a style switch, how do you know the market has stabilized? You look at the VIX; it will first fall from a very high level and continue to decrease. Secondly, its trading volume will be very low, indicating that no one is trading this anymore.

During the recent months of July and August, what were the fund managers in the US stock market doing? The more stubborn ones were not reducing their positions in Nvidia, Google, or Apple, or the S&P 500. However, they took some of their positions to deleverage and went long on the VIX. These individuals felt that their positions were stagnant and that a market shift might be coming, so they took protective measures by allocating part of their positions to bet on volatility.

In the face of that sharp decline, it was as if all their stocks were losing money and experiencing full drawdowns. However, their positions in volatility made them money. So, at least their overall positions could maintain a break-even situation, essentially buying insurance.

Buying call options on the VIX, engaging in bullish options trading—this is a lot to unpack. To summarize, I think this story is quite simple: this person fell ill, and the story began in March 2020 when this person was basically treated. The significant drop in August 2024 essentially represents that the effect of liquidity has retreated to the point of no return. If it retreats further, where will it go? It will retreat to the next layer, like Coca-Cola or the stocks that Buffett loves to buy, which are pure cash flow stocks. So, I believe this is also a market reversal point, gradually retreating, and soon it will start to rise again, leading to discussions about interest rate cuts.

So, I want to review with you: if you want to understand how the drop on August 5 occurred, you need to trace back to three or four years ago, to the events of March 2020. Then, review the developments in the US financial market, especially the strategic financial market, from March 2020 to August 2024, and you will have a clearer understanding.

In simple terms, for us in the crypto space, I think it’s straightforward. The significant drop on August 5 was a deleveraging in the off-market, which has little to do with the crypto space. Now, both on-market and off-market have been thoroughly cleaned out; that’s basically the situation.

FC

Understood. So, what I want to ask is, what should we reference for the upcoming market trends? What should we think about for the future? What dimensions should we consider? To be honest, I feel like we’ve reached a very boring time, right? I seriously ask myself; I think everyone is no longer pessimistic but rather bored and tired of discussing these matters. Because it seems like we keep circling around the same few questions, right? Ethereum, for example, Ethereum versus Solana, meme coins—there’s no direction, just this kind of sentiment.

HighFreedom

Understood.

FC

If we look at past experiences, this kind of sentiment usually occurs when we are at a bottom range, right? It often accompanies either a bullish market continuing upward or a consolidation phase where people are skeptical but still moving up. So, what indicators should we be looking at below? What should we focus on from your perspective?

HighFreedom

Understood. I think it goes back to the fact that there are two groups of participants in this market: the off-market and the on-market. Let’s first talk about the on-market. I believe the most important indicator for me to watch is the long-term and short-term holders. The situation of long-term holder supply and short-term holder supply. My estimate is that in this bull market, the long-term holders should have sold at least around 2.2 to 2.5 million Bitcoins. Currently, I calculate that they have sold about 700,000 to 800,000, which is roughly one-third of their holdings. The key players with real decision-making power still have about two-thirds of their holdings left; they are still waiting. This is an on-market factor.

As for off-market factors, as mentioned earlier, if the US continues to reduce its balance sheet and shrink liquidity, it will essentially push down to the next layer. The US tech stocks are also struggling a bit, unable to hold up. But now you will notice a slight shift in the market; after a large-scale deleveraging, the Nasdaq has made a slight reversal, returning to around 20,000 points. Essentially, the market in the US stock market will recognize that interest rate cuts are coming. As interest rates are cut, the overall risk appetite in the market will gradually increase.

However, I want to emphasize a small point of knowledge to discuss this matter with everyone. In earlier years, measuring the amount of money in the capital market and the level of risk appetite was quite simple and straightforward: just look at interest rate hikes and cuts.

When interest rates are raised, there’s no money; when interest rates are cut, there’s money, leading to investments in riskier assets. When interest rates rise, I become more conservative, and risk assets decline. However, since the financial crisis in 2008, the US has learned from Japan. Japan was the first to implement quantitative tightening and quantitative easing starting in 2001.

The US began this process at the end of 2008 and the beginning of 2009. At that time, the Federal Reserve Chairman was Ben Bernanke, and they were learning from Japan’s experience with quantitative tightening and easing. What does quantitative tightening mean? In reality, the current financial market is much more complex; it’s no longer as simple as just raising or lowering interest rates to explain things. What is the process? First, they lower interest rates, similar to a doctor treating an illness. I first give you some conservative treatment; you take it and see if it helps. If it doesn’t work and the situation is serious, then we move to the next step: injections or IV drips. Eventually, it may even lead to surgery.

The US quantitative tightening and quantitative easing processes are similar. First, interest rates are lowered; if that solves the problem, then there’s no need to expand the balance sheet afterward. Expanding the balance sheet is quite simple: the central bank prints money to purchase various assets, including mortgages and various US Treasury bonds. So, it’s important to emphasize that it’s not a straightforward sequence of lowering rates, then expanding the balance sheet, then raising rates, and then contracting the balance sheet. It’s not necessarily A to B, then B to C. It starts with A, giving a treatment to see if it works. If it doesn’t, then there’s no need to expand the balance sheet.

So, I want to discuss the topic of interest rate cuts, which has been a hot topic lately. My understanding is that this can be likened to a simple math problem: there’s a water tank with an inflow pipe at the top and an outflow pipe at the bottom. The inflow pipe adds five liters of water per minute, while the outflow pipe removes three liters per minute. Currently, the tank holds 800 liters. The question is, what will happen to the tank in ten minutes? The purpose of this example is to illustrate that the water in the tank represents the so-called dollar liquidity. How does the increase or decrease of the US monetary base (M0) work? What role do interest rate cuts play? Lowering interest rates helps maintain the high pressure in the tank, which was significant under a high-interest environment.

However, after lowering rates, the benefits for risk assets may be limited. What would be truly beneficial? Expanding the balance sheet. But again, we return to the topic: if this person is truly sick and finds that lowering rates doesn’t help, they will take further action. So, returning to the topic, whether there will be a massive bull market in risk assets depends on whether the Americans are seriously ill. However, I believe this is something ordinary people cannot judge, and even Federal Reserve officials cannot accurately assess; the Fed itself is always lagging behind.

So, what can we do? I want to share this logic with you. If the Federal Reserve officials indeed say, “We are sick, and I am about to expand the balance sheet,” then what might happen? Risk assets could collectively plummet, and after that, a large-scale expansion of the balance sheet could replay the story of 2020. However, currently, the probability of this scenario seems low. I lean towards the greater probability being a gradual interest rate cut, where inflation is not high, and the economy is not collapsing, leading to stable inflation and a healthy economy, allowing for a gradual decline. This would definitely be beneficial for risk assets.

Therefore, I think there are several practical indicators to watch. You can look at the Russell 2000, which should be searchable under the code RUT, or the BlackRock fund called RWM. Add ARKK, GME, and AMC to your watchlist. You don’t need to buy these assets, but you should monitor them. If you start to see these assets rising, it would indicate that the overall risk appetite in the US stock market is gradually increasing, and people are starting to invest in these assets. This is the most direct thing to observe off-market.

As for interest rate cuts, balance sheet expansion or contraction, and dollar liquidity, the issuance of ultra-short, medium, and long-term government bonds, I think these are too complex for most ordinary investors. There’s little significance in watching these; just focus on the risk appetite in the US stock market.

Now, I want to address what I believe are the two main concerns for holders. The first is about Bitcoin, and the second is about altcoins. I think Bitcoin is quite simple and clear; it is a growth-oriented digital gold. When did Bitcoin’s market cap surpass that of gold? It was in November 2021 when Bitcoin reached $69,000, and its market cap was 11% of gold’s market cap, which was a historical high. In every bull market, Bitcoin’s market cap tends to climb higher. Each bull market sees Bitcoin’s market cap relative to gold’s market cap increase. Especially in this round, all the new funds coming in from off-market are simply buying into the digital gold narrative.

So, if you are extremely conservative, you should at least wait until Bitcoin’s market cap reaches a certain level. I’ve been discussing this with my friends; recently, everyone has been feeling down after months of sideways movement and volatility, thinking the bull market is over. I believe my judgment is that a new wave of upward movement is yet to begin. Don’t give up before dawn; manage your leverage and mindset. Because first and foremost, Bitcoin is simple; it’s a digital gold asset. Currently, Bitcoin’s market cap is only about 7% to 8% of gold’s market cap, and it hasn’t reached the previous peak. Shouldn’t we give it a little chance? At the very least, it should reach the previous peak before you exit. Based on gold’s market cap of $17 trillion, that would put Bitcoin’s price around $100,000. If you have a bit of ambition, shouldn’t we aim a little higher? Perhaps Bitcoin’s market cap could reach 15% to 20% of gold’s market cap.

This leads to the next topic: how do we estimate these things? It’s about looking at the counterparties. I believe the biggest counterparties in this market are all traditional financial institutions in the US. For example, state government funds from all 50 states; currently, three states have begun to accumulate Bitcoin. The fastest is Wisconsin, the birthplace of the Republican Party, with a fund size of about $150 billion to $160 billion, planning to allocate 1% to 2%. What I want to emphasize is that these people are our true friends in the crypto space because they are real holders; they may hold their purchases for five or ten years without selling.

What is our enemy? Currently, the inflow into spot ETFs since January 11 has been around $16 to $17 billion. From the quarterly disclosures, you can see that about 80% of the holdings are retail investors. The real friends, these institutions, are still on their way; they haven’t boarded the train yet. They have many internal processes to go through before buying these products. They need to understand what Bitcoin is, report to their bosses about Bitcoin, and communicate with regulators about whether they can buy Bitcoin. This product also has a 90-day observation period, among other factors.

So, I want to say, don’t rush. The counterparties in this round, the sophisticated term is counterparties, but in simpler terms, the ones picking up the pieces, are still on their way. They haven’t figured it out yet. Some early movers have started buying, like Goldman Sachs using its own funds, and some banks in the US are also starting to buy with their own money. These are the counterparties in this round, and they are just beginning. Therefore, I believe the off-market situation is quite optimistic; they are early, but for them, buying risk assets may not be feasible during the most challenging final stages of quantitative tightening. For example, in the middle of the second quarter, when quantitative tightening is at its peak, interest rate cuts are about to begin, and quantitative tightening is coming to an end.

They will gradually start buying these assets. So, I hope for something simple: I wish they could act faster because everyone is starting to feel the pressure. I think the off-market situation is optimistic, while on-market, we just need to look at the blockchain. Those big players, the whales, long-term and short-term holders, still have a lot of assets they haven’t sold; they are also waiting. So, I think we should be patient; I’m not worried about Bitcoin at all.

Now, let me share my views on altcoins. The first question is, are there altcoins? I believe there definitely are. Why? It’s simple; just look at who holds Bitcoin. At least around 60% of the coins are in the hands of crypto enthusiasts. When Bitcoin reaches $100,000 or $150,000, these long-term holders will inevitably want to speculate on altcoins.

I’ve always believed that the crypto space is never short of stories; it’s just about whether these stories can meet the right historical timing to ignite a positive cycle. What does this mean? Looking back over the past year, or rather, the past six months, the hype around inscriptions and layer twos has fizzled out, with only a few billion dollars generated. Those heavily invested in these areas are now suffering significant losses and are constantly trying to create new stories. They are in the final stages of quantitative tightening, and assets like AMC, GME, and ARKK have been struggling for a long time; it’s normal for these stories not to take off.

So, are there altcoins? It’s simple: when 60% of Bitcoin holders want to speculate on altcoins, they will create some stories, whatever they may be, and push forward. The only point for discussion is how strong the altcoin movement will be. I think there are two scenarios. If Bitcoin rises to, say, $120,000 to $130,000 or $140,000, and you see the Russell 2000, GME, and others soaring, even surpassing previous highs, then altcoins in the crypto space could skyrocket. This is similar to the summer of 2021 compared to the winter of 2021, where summer was about DeFi and winter was about NFTs and the metaverse.

This is the first optimistic scenario, but I think the probability of this happening is relatively low. It goes back to the point that if this person doesn’t take a strong action or doesn’t take a strong medicine, it’s hard for this situation to occur. I think this might be why there are no altcoins; perhaps people are considering these factors. This is the first scenario.

The second scenario, which I think has a higher probability, is that Bitcoin can rise to $120,000 to $130,000 or $140,000. I believe this is achievable. However, if at that time the Russell 2000, GME, and AMC are still struggling, and the overall market cap of stablecoins is not excessively high, then the growth of altcoins may be quite limited.

But I believe altcoins do exist; the vast majority of Bitcoin is in the hands of crypto enthusiasts. If we look at it from another angle, the vast majority of Bitcoin is in the hands of traditional institutional investors in the US stock market. They don’t understand layer twos, let alone inscriptions, DeFi, or AI; they don’t comprehend these concepts, and they don’t participate, which is problematic. The height of Bitcoin’s price has little to do with altcoins; they are not connected at all. Therefore, I believe there will still be altcoins; it’s just a matter of magnitude. Of course, expressing this viewpoint may lead to criticism or backlash, but I believe we are currently at the bottom of the bottom. Whether it’s Bitcoin or altcoins, I think we are at the bottom of the bottom. Everyone should look for suitable targets to invest in. Even a few months ago, if you wanted to invest in altcoins, you would have seen GME and AMC struggling, making it difficult to invest, as there was little money to drive them up.

However, I believe that now, the better altcoins may have reached the positions they were in at the beginning of 2021 or early 2024, while the weaker altcoins have already reached the positions they were in during the bear market of 2022 or 2023, essentially at the starting point before the surge in September or October. I think this is a time when a reversal is gradually approaching. Finally, the tide has retreated to the point of no return, and interest rate cuts are about to begin, leading to a rising tide. You are holding a highly risky asset, hoping for a rising tide, wishing that the tide will rise into your small stream or tributary. Therefore, I don’t think we should be overly pessimistic.

Some of my friends think we are in a bear market, but I believe the bull market is not over, and I hope I won't be proven wrong. I also hope to verify this soon. We are now in the middle of the third quarter, and I think around the fourth quarter, we should be at the bottom of the bottom. The leverage both on and off the market has been thoroughly cleaned up. Moreover, the entire macro environment is starting to reverse, transitioning from a tide receding to a tide rising. The only point of contention is how high this tide will rise, which I think needs to be discussed clearly.

FC

Let's set the title like this: "The Bull Market Returns in Q4." You’ve basically answered my questions already. However, I suddenly want to add a question. Since you have been in the brokerage industry for quite a while, as a trader, what do you think is the proper growth path for entering a brokerage or the financial market? What should one learn first and then what next?

HighFreedom

Let me think. I particularly recommend that everyone take the CFA Level 1 exam; push yourself to do it. If you register for the early bird, I don’t know how much it costs now, but it used to be around $700 to $800. There are ten subjects in total, and the CFA stands for Chartered Financial Analyst. This is a set of financial courses from abroad, consisting of three levels: CFA Level 1, CFA Level 2, and CFA Level 3. If you work in a traditional financial institution as an analyst, you need to take this exam.

Why do I want to talk about this? It might not matter if you studied math, music, sports, or physics in school. It’s okay if you haven’t studied finance; the CFA is specifically designed for this purpose. You don’t need to take Levels 2 and 3; I think that’s completely unnecessary if you’re not working in this field. However, it’s worth taking Level 1 because it essentially gives you an opportunity to study what is akin to a Master of Finance. Studying abroad for a Master’s in Finance costs tens of thousands of dollars, and the courses are not much different from the CFA. Ironically, many students focus on passing the CFA while studying.

What is the CFA? It consists of ten subjects and provides a comprehensive and systematic understanding of the foundational knowledge of the entire financial system. It serves as a framework. Once you have this framework, you can extend your learning to other areas. It’s simple; you will be speaking the same language as others in the field. Sometimes I feel a bit silly recommending that everyone take a certification exam, but I think it’s very useful. That’s why I encourage my friends to spend this money; it’s not too expensive, a few hundred dollars. Only by doing this can you force yourself to learn; otherwise, the material can be quite dry and overwhelming, especially since it’s all in English. Having an exam compels you to study; otherwise, you might just dabble for a couple of days and then set it aside and never look at it again. So, I think this is quite beneficial.

You see, not everyone working in brokerages has a finance background. Many people, for example, who analyze the Huawei supply chain, originally studied electronic mechanical manufacturing. Those looking at TMT or technology might have studied computer science; people from various fields are present, but they all generally take the CFA because this body of financial knowledge has been around for hundreds of years and is quite rigid.

FC

It seems like you are channeling Teacher Hong Hao; you sound like his spokesperson.

HighFreedom

Then let him give me some advertising fees.

FC

What do you think the CFA is? What is orthodox once we enter? This is quite interesting. Many of my friends often ask me, especially earlier this year, what should I do if I want to enter this industry? What should I learn? Some smart friends ask about your industry rankings. This is quite interesting.

I have some friends doing this; they check the top three tokens by price increase every day and analyze why they are rising. I do this every day too; I take a look at who is at the top of the gainers list and look for reasons for the increase. I think this helps develop muscle memory, as I might recognize similar situations in the future.

HighFreedom

That might help.

FC

As a trader in a system like yours, what should their deliberate training be?

HighFreedom

I see, I’m getting some ideas here. Let me explain this thought. In financial institutions, there are two groups of people doing research, the so-called analysts. The first group looks at the fundamentals, focusing on macroeconomic factors. They are often referred to as macro analysts or total analysis, or they might look at fixed income and government bonds, focusing on the macro direction. This is one group.

The second group looks at specific industries. I look at electronics, you look at consumer goods, and someone else looks at manufacturing; these are industry analysts. I feel like the crypto space is similar. In the crypto space, you have macro analysts; I think tools like Glassnode are important. Regularly checking Glassnode and understanding its key indicators is crucial for grasping the macro situation in crypto.

Going a level deeper, I think it involves the alpha in the crypto space, various new tracks, and directions. What are these tracks? What is the market cap? What is the token unlocking situation? These on-chain conditions can be observed through tools like Dingyong and a few others that focus on small tokens. I think this corresponds to how brokerages operate: one group looks at macro conditions, while another focuses on various industries. I believe it’s the same here; in the crypto space, there are those who look at Bitcoin on-chain data, and then there are those who analyze small tokens and seek excess returns. I feel there are these two groups of people, each with their own focus. So, one set corresponds to the on-chain data for Bitcoin, while the other set looks at the fundamentals and unlocking situations for small tokens.

FC

Right, I understand. OK, let’s move to the final segment about growth. I want to know who you recommend as a trader you particularly like, who you follow closely, and why?

HighFreedom

Does this have to be limited to the crypto space, or can it be from various fields?

FC

As long as it helps you, it’s fine.

HighFreedom

OK. I’ll recommend a few people. The first is definitely Fu Zong, a guy from Northeast Securities named Fu Peng. He also does media and is quite active. I think his views and analyses on dollar assets are systematic and insightful. He also enjoys sharing. I won’t start a debate; I think Fu Zong is quite capable.

The first person I recommend is Fu Peng. The second person I feel is A Sir; I think he has a relatively clear understanding of the macro situation in the US. However, he tends to write extremely long articles filled with American slang, which can be a bit challenging to read, but I think his insights are valid. For example, in March or April, he mentioned that liquidity might decline in April and that the market might move sideways. Recently, he has been optimistic about the future, suggesting that if Bitcoin breaks $75,000 in September, October, or November, it could be significant. I think A Sir is the second one.

Another person is a friend of mine who is a fund manager. He has his own Twitter account but doesn’t post much because he’s a bit lazy. I often consult him on various issues; his name is Victor. Victor is also an old crypto enthusiast. He started as a miner and has been in the space ever since. I’ve added notifications for these people, so whenever they post something, I check it out immediately. There’s also a well-known trader from the last cycle named Person Song, who runs a website. I think he provides useful insights on key cyclical indicators and major cycles.

FC

Got it, sounds good. Everyone can follow these recommendations; we will publish a written version. Hearing you explain it again today has helped me review and learn new things. I think for those who engage in cyclical trading, the most important thing is to find a hobby.

HighFreedom

Yes, it can be quite boring.

FC

Most of the time, there’s no need to take action.

HighFreedom

Exactly.

FC

I think those who engage in on-chain trading also need to find a good psychologist. The dopamine rush comes too quickly, and when it’s time to leave, it can be hard to accept; it’s not easy. Traders are often highly sensitive individuals. I think that’s it. HighFreedom, do you have any final thoughts on today’s discussion?

HighFreedom

Let me think. Right, there’s one more thing you ask every interviewee about: the so-called stop doing list.

FC

I initially heard you mention stop-loss strategies; you can elaborate on that.

HighFreedom

I think on-chain data is very important, especially for Bitcoin. You can see very clear cyclical effects. However, I want to discuss something that is useful for this round; everyone doesn’t need to worry. But in the future, it may have a significant impact. You see, on-chain cyclical traders accumulate coins and then sell them when the bull market arrives; it’s quite straightforward. But on-chain, these behaviors are visible, and it’s important because they have pricing power. The coins are in their hands. As we mentioned earlier, about 60% of holders are these individuals. They don’t trust any exchange; if they have 10,000 Bitcoins, they won’t store them on OKEx or Binance; they keep them in their cold wallets.

So, I want to say that these on-chain individuals have very strong pricing power. Because the people with a large number of coins are on-chain, not on exchanges. However, their behaviors can be observed on-chain.

But what’s the issue? As more and more spot ETFs buy Bitcoin, it might reach around 20% to 30%. You will find that it’s like returning to an exchange environment, where it’s all about Coinbase cold wallet custody addresses. At that point, on-chain data may not be as effective. I think this is something everyone should consider, but I believe it’s a long-term issue that we shouldn’t worry about in the short term. Secondly, I think regarding the on-market situation, when will it become ineffective? I have a set of judgment logic here, such as dollar liquidity, interest rate cuts, and balance sheet expansion or contraction. Of course, the US might come up with a new logic, and if they stop quantitative tightening and easing, we might have to learn again and adapt. But I think this is also something we might not see in the short term. So, I believe these are two points; I don’t have anything else to add.

FC

I understand. Here’s a challenge for you: predict the price of Bitcoin on December 31. No pressure; this is not investment advice.

HighFreedom

You’re putting me on the spot, haha. I think let’s set it at $100,000; that’s the number I’ll go with.

At least it touched 100,000; whether it can guarantee 100,000 is hard to say, but it has touched 100,000.

FC

How much did you lose? Not too much, let's bet.

HighFreedom

You want to be the counterparty.

FC

Of course, I think it won't reach 100,000, so I'll be your counterparty. Besides just sending a red envelope, we can also do a lottery later.

HighFreedom

Or we can do it this way: if it reaches 100,000, you treat me to a meal; if it doesn't reach 100,000, I treat you to a meal, and that's it.

FC

That doesn't involve everyone; I’ll treat you alone, right? If I lose, I think we should bet on something auspicious, right? I’ll think about how much it will be, and I’ll let you know. If I lose, I’ll send it to your fans and help you with a lottery.

HighFreedom

Sure, 666, 888, and those kinds of numbers.

FC

Right, we are using U as the unit.

HighFreedom

No problem, no problem.

FC

That works.

HighFreedom

May I ask a question as the guest? Why do you think it won't reach 100,000?

FC

I haven't really thought about this because I don't like to guess prices, to be honest. But I think if you ask me to look at the exit now, from my perspective, I believe that, how should I put it, I might expect a return of about 50% to 100%. I'm not talking about BGC; I'm talking about Ethereum and others. I think it’s about there. Because I think if we assume we exit in the middle to late stage of a bull market, at that time, you can do many things. For example, you can use U to invest in new projects, use U for quantitative trading, or arbitrage. I think all of these could yield around 12% annually, right? I believe that the win rate might be higher than just holding coins; that’s my thought.

HighFreedom

But as time goes on, there might be other operations, and the risk-reward ratio might be better. It’s not necessarily the best choice to just hold spot.

FC

I think that’s my mindset. Because I know that around 70,000, many people around me sold off a wave.

HighFreedom

That’s just practice.

FC

You can think of it as the first distribution of a long weekend.

HighFreedom

Right? Yes, it was very obvious on-chain in March, with a large amount of distribution, even 3/1.

FC

From the on-chain perspective, recently, Galaxy has been consistently dollar-cost averaging, and many institutions are also doing the same.

HighFreedom

Yes.

FC

It’s quite interesting. OK, then we’ll reveal it on December 31.

HighFreedom

OK, sounds good.

FC

Everyone can quickly click to follow. I’ll try to make sure to ask this question to everyone who comes in the future.

HighFreedom

Sure, I’ll be there. Alright.

FC 01:16:07

From the on-chain perspective, recently, Galaxy has been consistently dollar-cost averaging, and many institutions are also doing the same.

HighFreedom

Yes.

FC

It’s quite interesting. OK, then we’ll reveal it on December 31.

HighFreedom

OK, sounds good.

FC

Everyone can quickly click to follow. In the future, I’ll ask this question to everyone who comes in.

HighFreedom

Sure.

FC

Thank you, everyone. Our recording is on Xiaoyuzhou, in a program called "Dialogue with Traders," so you can check it out. Basically, that’s it. If anyone has good trader recommendations, I’m a bit short on them right now. Thank you all, thank you. We’ll end here today.

HighFreedom

Alright, bye-bye.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。