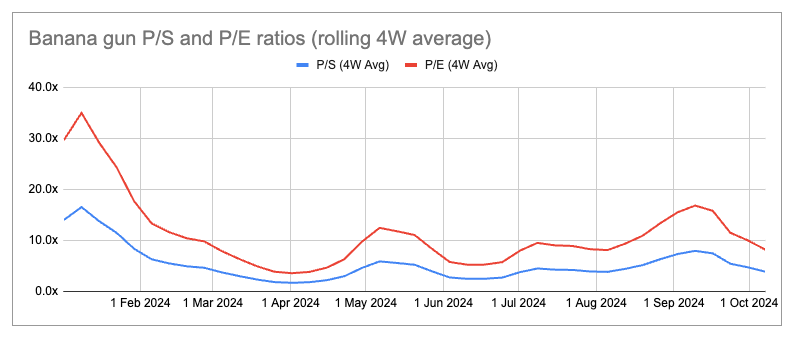

- Despite significant growth momentum and structural advantages, the price-to-sales ratio (P/S) of $BANANA is only 4 times, indicating a conservative valuation.

Author: ML

Translation: ShenChao TechFlow

Executive Summary

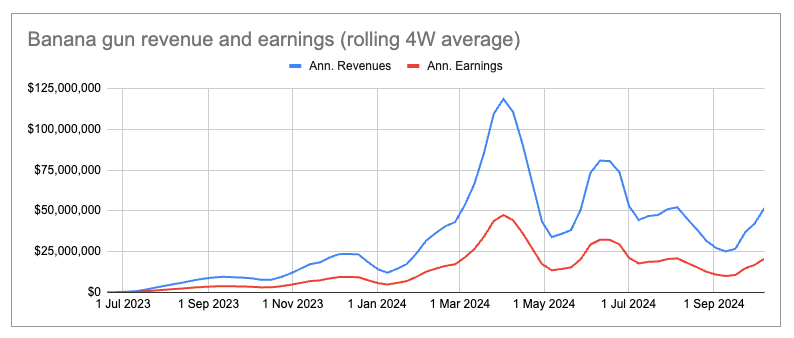

According to 4-week rolling average data, the annualized revenue of Banana Gun (BG) is approximately $52 million, of which about $21 million belongs to token holders (annual yield of 17%).

Despite significant growth momentum and structural advantages, the price-to-sales ratio (P/S) of $BANANA is only 4 times, indicating a conservative valuation.

The issue of fully diluted valuation is not severe: in the foreseeable future, $BANANA is unlikely to experience supply shocks due to team and financial allocations.

The potential for vertical integration presents huge opportunities, with annual revenue and profits potentially tripling.

Upcoming new products will further strengthen BG's competitive advantage and position it more favorably in market competition.

Although there are risks related to the market, competition, and regulation, these risks have been effectively managed.

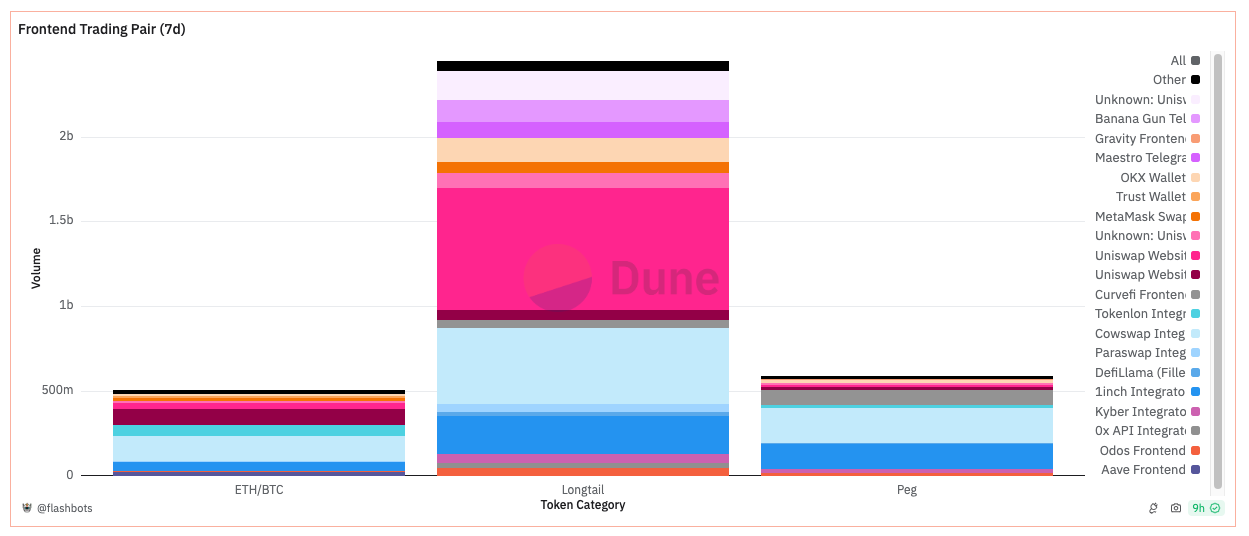

The Frontend Battle

Source: Flashbots

In the past 7 days, frontend trading platforms on Ethereum generated approximately $36 billion in trading volume (annualized to $185 billion). Among this, long-tail assets (i.e., non-ETH/BTC or pegged assets) accounted for 69% of the trading volume share (about $24.5 billion). The top trading platforms by volume include some familiar names: Uniswap (despite frontend fees), Cowswap, and 1inch. However, BG also generated about $129 million in trading volume, accounting for approximately 5% of long-tail asset trading volume.

I recently read an article written by Mason discussing the privatization of order flow and how the surge of altcoins has driven the development of TG bots. As this asset class continues to expand, traders are becoming more sophisticated, constantly seeking ways to enhance trading speed and avoid MEV. Users of these bots are typically less sensitive to price and place greater importance on speed and convenience. Despite high fees of 0.5% to 1% on trades, we still observe a significant increase in the usage of TG bots.

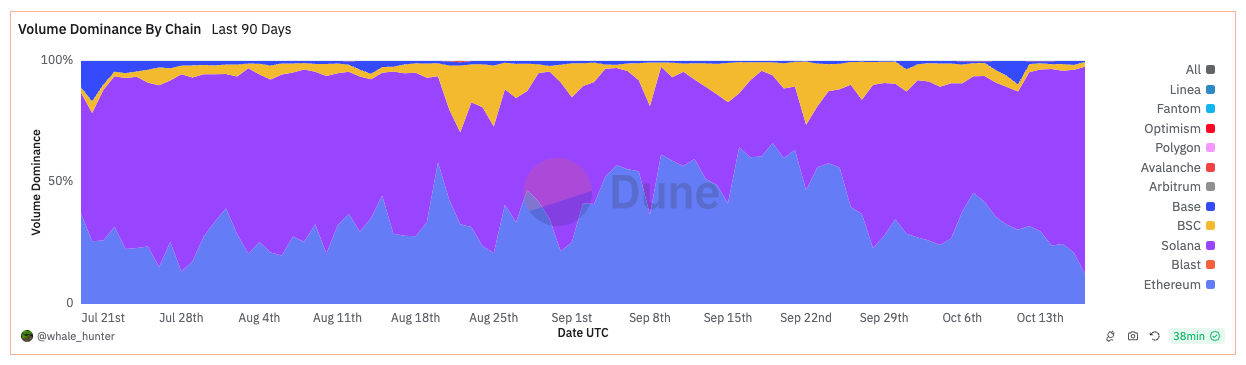

Source: whale_hunter

Analyzing the market dynamics of TG bots, we find that 98% of trading volume is concentrated on Ethereum and Solana. In the past 7 days, Trojan led in trading volume (reaching $325 million), primarily due to its dominance on Solana, while BG and Maestro had trading volumes of $167 million and $142 million, respectively.

Although BG's release on SOL is close to Trojan's, I believe Trojan's advantage mainly comes from a more effective referral program (tiered reward system) and airdrop activities. BG has rooted itself in the Ethereum ecosystem and formed its own community, closely related to its origins. Notably, Maestro, which once dominated Ethereum, is gradually losing market share, partly due to the presence of the $BANANA token and the high success rate of BG's sniping operations (which will be detailed later).

Here are four important conclusions:

The importance of building relationships with end users is increasing;

As users mature, enhancing trading speed and execution efficiency is becoming a trend;

Using TG bots for altcoin trading has become the norm;

Users of TG bots are often driven by incentives (such as token holder status, referral programs, rebates, and airdrops).

BG's Revenue Model and User Acquisition Strategy

BG generates revenue by charging a 0.5% fee on manual buy/limit orders (Ethereum only) and a 1% fee on all other supported chain sniping or trading. According to 4-week average data, BG's weekly revenue is approximately $993,000 (annualized to $52 million). Of this, 40% of the revenue is distributed to token holders, excluding the financial treasury, CEX balances, and half of the team tokens. Among the circulating 3.4 million tokens, only 2.9 million are eligible to share in the revenue, with an annual yield of about 17% at the time of writing.

To enhance user loyalty, the team has designed a rebate program that rewards users with $BANANA for trading on the bot. The actual $BANANA rebate is calculated based on the dollar value of fees paid and a discretionary multiplier. This program is partially supported by financial buybacks, reducing reliance on token issuance.

In-Depth Understanding of $BANANA's Token Economics

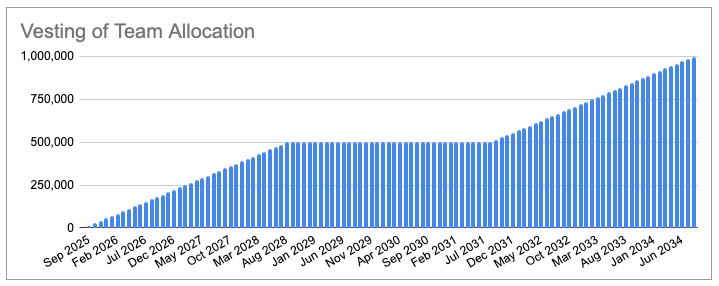

The team holds 10% of the token supply, with the first batch unlocking on September 14, 2025, and the remaining portion unlocking on September 14, 2031. Both batches of tokens will undergo a linear unlock over three years starting from the unlock date. The team is willing to accept such a long unlock schedule because half of their tokens are eligible for revenue distribution—this is a fair arrangement for them, which requires an incentive mechanism. This demonstrates the team's high confidence, as they can only benefit when BG is profitable, thus avoiding the need to profit by selling tokens.

Conclusion: The team's incentive mechanism aligns with the interests of token holders.

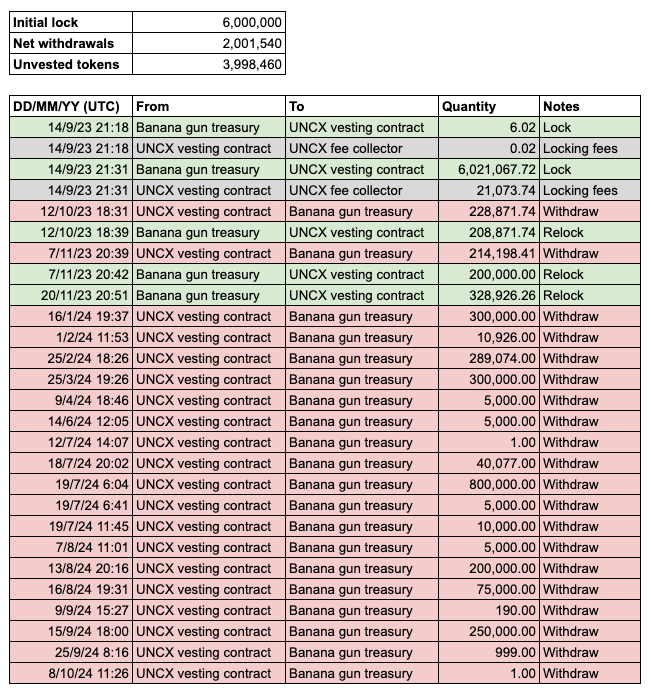

It is worth noting that the initial financial treasury held 60% of the token supply (lock transaction can be found here), but after burning about 15% of the supply, the documentation was revised to 45%. According to the original plan, 250,000 tokens were to be unlocked monthly for two years. Although by plan, the unlocked tokens from the financial treasury should reach 3.25 million by October 2024, the actual net token amount withdrawn from the unlock contract so far is only 2 million.

It is evident that, considering BG's substantial revenue, continuing to drive product adoption does not need to rely on the release of tokens.

Perspective

BG's order flow holds enormous revenue potential.

Source: whale_hunter

As previously mentioned, BG benefits from an increasing number of people opting for privatized execution and quick listings. According to Felipe's research, BG has won about 88% of the sniping orders, creating a natural monopoly in this niche market. This is partly due to the "high bribery culture" surrounding the release of highly anticipated projects (see the query above).

Source: Arkham (Banana Gun's main trading counterpart ranked by capital outflow)

From BG's profile on Arkham, it can be seen that users paid nearly $100 million in priority fees (bribes) for sniping orders, most of which flowed to titan. This is somewhat strange, as titan is a relatively new participant (joined in April 2023) in the building space and does not have the historical record of existing players like beaverbuild.

Upon deeper analysis, it is found that although the number of blocks built by titan is only half that of beaverbuild, its generated profits exceed those of beaverbuild. This suggests that there may be some sort of "exclusive order flow arrangement" between BG and titan, which is not necessarily a bad thing.

Source: libMEV (data since the merge)

The key is… what if BG keeps the order flow to itself? If they choose to become block builders, BG's annual revenue could easily triple overnight (assuming $ETH is $2.6K).

Imagine a world where $BANANA holders can earn an annual yield of about 51%, with these earnings coming from frontend and block building revenues.

We May Not Experience Supply Shocks

We are quite familiar with the team strategies surrounding major unlocking events and supply surpluses. In the case of $BANANA, the locked supply will not enter the market until September 2025 (when the financial and team allocations will begin to be released linearly).

I have ample reason to believe that the selling pressure from the treasury and team will be minimal for the following reasons:

- BG is highly profitable, and if they decide to become block builders, they can significantly increase their revenue.

Strong revenue allows them to support growth and operations without selling unlocked treasury tokens.

The underutilized treasury tokens further support this view.

- The culture and belief of the BG community are based on the vision of BG becoming a self-sustaining cash cow (e.g., long-term team lock-up periods, team revenue sharing).

- The team understands that a large sale of unlocked tokens would undermine the community's culture and belief in the long-term vision, severely impacting sustained growth and adoption. If the team chooses to re-lock their team and treasury tokens upon unlocking next year, I would not be surprised.

If this happens, I expect the re-locked team tokens to be included in the revenue sharing pool (after all, this is their right).

Strong Narrative and Fundamentals

Source: Brent

BG is a unique platform with both short-term positive factors and strong fundamentals. Recently, discussions about whether funds will include meme coins in their core portfolios have garnered attention. Here are my thoughts:

- If funds decide to invest in meme coins, they are likely to choose blue-chip coins due to scale and liquidity constraints.

Although they are unlikely to use tools like BG, this is beneficial for the overall meme coin market (driving prices and market sentiment up).

This will encourage an increase in micro and small-cap meme coins, thereby increasing user activity on tools like BG to seize these opportunities.

- If funds are unwilling to invest directly in meme coins but still want to get involved in this space, purchasing projects like $BANANA as an alternative to meme coins makes sense. This is similar to the strategy of "selling shovels during a gold rush," suitable for funds that focus on theory and fundamentals.

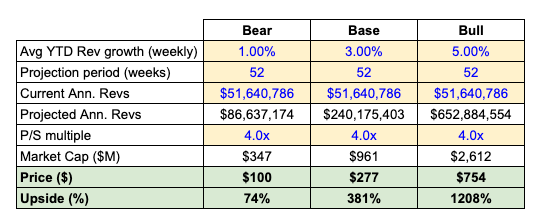

Regarding fundamentals, $BANANA attracts investors who prefer reasonably valued quality assets. By using a 4-week rolling average to smooth the data, BG's annualized revenue (earnings) reaches $52 million ($21 million), with a price-to-sales ratio and price-to-earnings ratio of 4 times and 8 times, respectively. This is below the average level of comparable projects (decentralized exchanges are the closest category).

Their annualized revenue and earnings show approximately 4.5% growth per week in the data so far this year. Interestingly, since January 2024, the price-to-sales and price-to-earnings ratios have decreased from 12.5 times and 26.5 times, respectively. This multiple compression is partly due to the weakening growth prospects of ETH and SOL, but I believe $BANANA will regain a higher valuation because:

Investors will focus on large applications that can "control the entire tech stack" (such as Aave, Uniswap, Ethena, etc.).

There are some upcoming growth catalysts (to be discussed in the next section) that the market has yet to price in regarding their potential uplift to revenue and earnings.

New Growth Drivers

Several anticipated catalysts include:

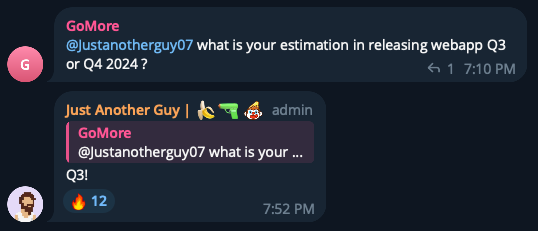

Webapp (expected to launch in Q3 2024): A browser trading terminal optimized for professional users, providing an on-chain trading experience similar to centralized exchanges.

White-label products: BG will integrate with dextools (and possibly other platforms) to increase order flow (more frontends mean better distribution).

Others: App store (like moonshot), more blockchain support, increased use cases for Banana points, etc.

I believe the future of TG trading bots is cross-platform, and having a user-friendly complex webapp will lower the barrier for users to adopt these tools. Additionally, white-label products will be an effective way to acquire more order flow, potentially converting users into loyal BG platform users.

These initiatives create strong differentiation in a relatively homogeneous market, and I believe BG is on the right path to continue growing its market share.

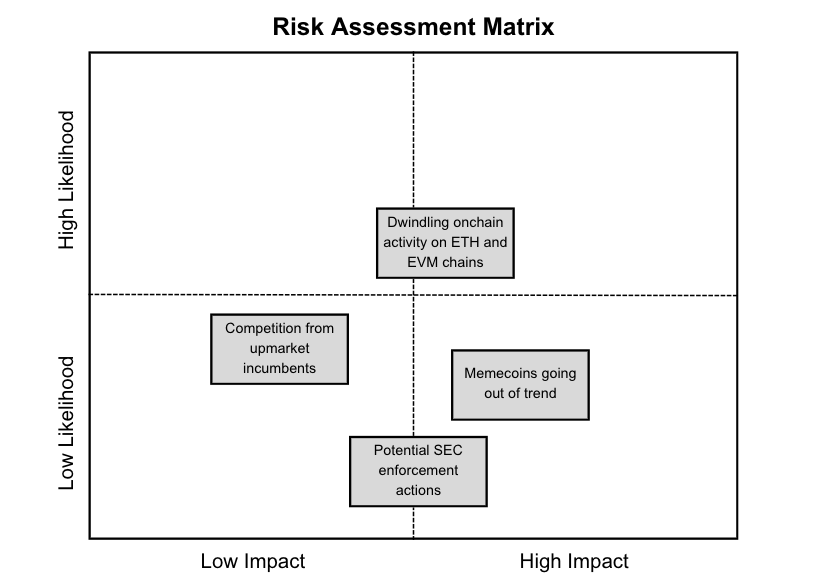

Risks

On-chain activity on ETH and EVM chains is decreasing

Since the beginning of 2024, activity on the SOL chain has surpassed that on ETH. As this trend may continue in the future, it is not favorable for BG. Although BG has already established some influence on SOL, it still faces fierce competition from rivals like photon, bonkbot, and trojan. However, I believe the upcoming webapp and app store will have uniqueness and effectively mitigate risks.

Competition from Existing Enterprises in the High-End Market

While projects like Uniswap Labs focus on increasing trading volume in the high-end market (i.e., intent-driven execution of large orders), we cannot ignore the potential competitive threats that may arise if BG grows too quickly. However, considering that trading volume in micro-assets constitutes a small proportion of overall on-chain trading volume, the likelihood of this scenario should be low.

Meme Coins May Lose Market Heat

Source: DefiSquared

Every bull market cycle has its themes, and we have seen speculative rises and falls in subcategories like DeFi, L1, and NFTs. So far, the hot topic of this cycle has been meme coins, which have greatly benefited BG. But nothing is eternal—if the market finds new speculative hotspots, meme coins may lose their appeal. However, I believe this scenario will not occur in the short term.

Regulatory Risks: Potential Enforcement Actions by the SEC

Since 2023, the SEC has filed lawsuits against over 40 crypto companies, accusing them of violating securities laws. However, the SEC typically targets platforms and exchanges with high token trading volumes and securities characteristics, such as Crypto.com, Robinhood, Consensys, Uniswap, Kraken, and Binance. While this risk cannot be ignored, considering BG's relatively small operational scale, the likelihood of this risk materializing is low.

Simple Valuation Analysis

I will describe my bear, base, and bull market scenarios based on the following assumptions:

Bear Market: New competitors from existing enterprises in the high-end market (like Uniswap) enter, on-chain activity on ETH decreases, and Trojan continues to dominate SOL market share, leading to a significant decline in growth.

Base Case: Growth slightly below the 4.5% seen so far this year, maintaining current market share on ETH and SOL, with no shitcoin frenzy emerging on supported chains (excluding ETH/SOL).

Bull Market: BG becomes a block builder, growth plans succeed, BG becomes the market leader across all chains, and some shitcoin frenzy emerges on supported chains (excluding ETH/SOL).

Note: To avoid excessive speculation, I have not considered the expansion of price-to-sales multiples.

Conclusion

Banana Gun ($BANANA) offers an attractive opportunity in the rapidly evolving trading bot market. BG demonstrates growth potential at reasonable prices, with advantages in privatized order flow, trading speed, robust fundamentals, no supply surplus, and attractive valuations. Additionally, a series of upcoming catalysts will help it stand out in the trading bot space. Despite regulatory and competitive risks, these risks are manageable and have been effectively mitigated given BG's current scale. Although challenges exist in the market, BG's innovative strategies and strong fundamentals indicate the potential for outstanding performance in the foreseeable future.

Disclaimer: The information in this research report is for reference only and should not be considered financial advice. The author may hold or trade the assets discussed in this article and may benefit from price increases. This report does not guarantee its accuracy, completeness, or timeliness, and investing involves risks, including the potential loss of principal. Readers should independently verify all information before making any investment decisions. The author, publisher, and related parties are not responsible for any losses, damages, or expenses resulting from the use of this information. This report does not comply with specific regulatory requirements, may contain third-party information of unknown reliability, and includes forward-looking statements based on assumptions that may not be realized, and does not constitute an offer to buy or sell securities. By accessing this report, you agree to these terms.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。