In the future financial ecosystem, PayFi will become a key driving force.

Written by: Will A-Wang

Musk's journey is one of stars and seas. Similarly, for the $2 trillion crypto market aiming for mass adoption, the $400 trillion - $600 trillion traditional financial market is also a vast ocean.

We can see some paths, such as the rise of tokenization, but the current migration of early RWA 1.0 assets to the chain, with relatively illiquid models, is not a long-term solution. Even if DePIN can revive the Internet of Things, it still struggles to hit the core.

Thus, we see Web3 payments, which can drive the mass adoption of stablecoins, a core aspect, especially in non-trading scenarios. VISA's stablecoin report tells us: the total supply of stablecoins is about $170 billion, settling assets worth trillions of dollars annually. Approximately 20 million addresses on-chain engage in stablecoin transactions each month. Over 120 million addresses hold a non-zero stablecoin balance on-chain.

Web3 payments can bring advantages of instant settlement, 24/7 availability, and low transaction costs to traditional financial payment networks, but this is far from enough. What we should see is a brand new financial market brought about by PayFi's innovative applications. PayFi, which can integrate Web3 payments, RWA, and DeFi, can help us reach for the stars and seas.

Therefore, this article will first introduce what PayFi is, and its relationship with Web3 payments, DeFi, and RWA, and then look at how Solana, which proposed PayFi, is gradually building its PayFi ecosystem.

1. What is PayFi

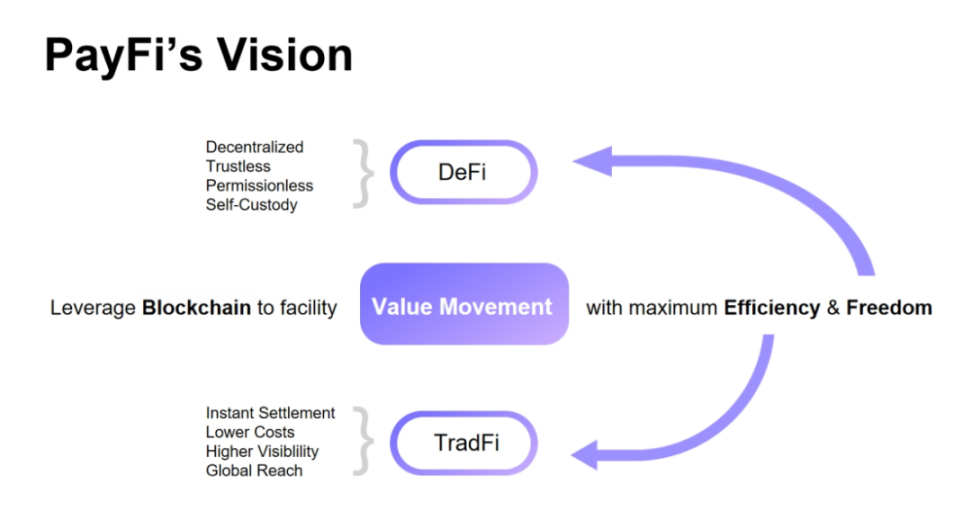

PayFi, or Payment Finance, refers to an innovative application model that combines payment functions with financial services based on blockchain and smart contract technology. The core of PayFi is to use blockchain as a settlement layer, combining the advantages of Web3 payments and decentralized finance (DeFi) to promote the efficient and free flow of value.

The goal of PayFi is to realize the vision of the Bitcoin white paper, building a peer-to-peer electronic cash payment network that does not require a trusted third party, while fully leveraging the advantages of DeFi to create a brand new financial market, including providing new financial experiences, constructing more complex financial products and application scenarios, and ultimately integrating a new value chain.

PayFi was first proposed by Lily Liu, the chair of the Solana Foundation, at the 2024 Hong Kong Web3 Carnival. In her view, PayFi is a new financial market built around the time value of money (TVM). These are difficult or impossible to achieve in traditional finance.

In this brand new PayFi financial market, not only can Web3 payments achieve efficiency improvements over traditional finance—instant settlement, reduced costs, transparency, and global reach—but it can also realize decentralization, permissionless access, asset ownership, and personal sovereignty based on decentralized finance.

2. The Relationship Between PayFi, Web3 Payments, DeFi, and RWA

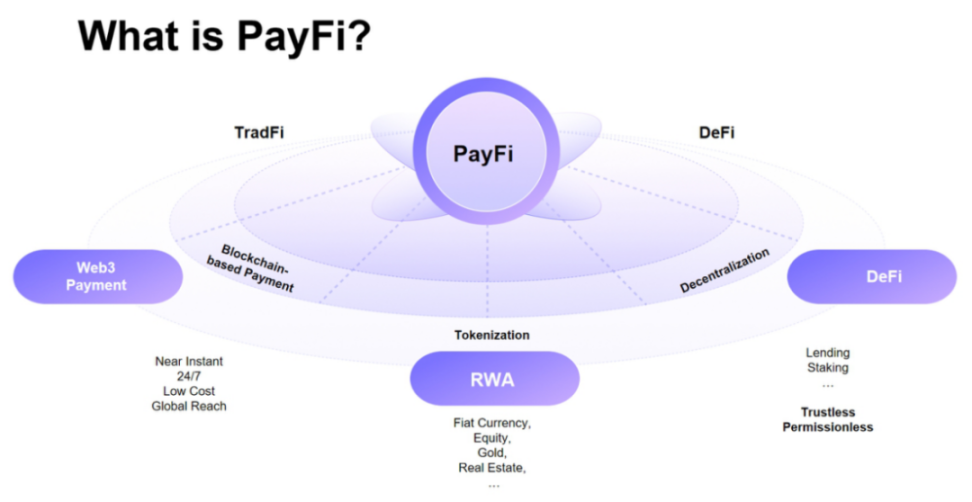

PayFi is not entirely equivalent to Web3 payments. Although Web3 payments have achieved many efficiency improvements over traditional finance based on blockchain technology, PayFi is a further construction, expansion, and deepening based on Web3 payments, further introducing DeFi to build a brand new financial market.

PayFi is not entirely equivalent to DeFi. The essence of payment is based on the exchange of value in the real world—money exchanged for goods/services. Therefore, PayFi is more about the processes of sending and receiving digital assets and settlement, rather than the mainstream trading behaviors of DeFi. Additionally, only by seamlessly connecting Web3 payments with DeFi through blockchain and smart contract technology can we create payment-related financial derivative services, such as lending and wealth management.

PayFi is not entirely equivalent to RWA. Here, RWA has two layers of meaning. The first layer is asset tokenization, meaning that only by tokenizing assets on-chain can we achieve seamless value transfer on the blockchain and use smart contracts to construct trading and settlement processes, such as the tokenization of dollars—stablecoins.

The second layer is RWA fundraising, which provides liquidity support for financing needs in PayFi scenarios. This is what Lily Liu described: "PayFi is a new financial market created around the time value of money. This on-chain financial market can realize new financial paradigms and product experiences that traditional finance cannot achieve."

Therefore, PayFi is not an innovative independent concept but an innovative application that integrates Web3 payments, DeFi, and RWA. This model not only covers the payment and trading of digital assets but also encompasses financial activities such as lending, wealth management, and investment. Through blockchain and smart contract technology, PayFi not only makes global financial payment activities faster and cheaper but also reduces friction and costs in traditional financial payment services.

3. The Significance and Value of PayFi

Literally, PayFi is not fundamentally different from GameFi or SocialFi, but the true significance of PayFi lies in promoting the application of digital assets in real-world scenarios.

Positively, PayFi can facilitate the migration of Web2 groups to Web3, such as how traditional financial payment companies can leverage blockchain technology to gain a larger market share and avoid missing the wave of the times.

Conversely, the Web3 community can use Payment as a vehicle to leverage blockchain technology to address the pain points of the traditional financial system, achieving new financial paradigms and product experiences that traditional finance cannot realize.

Currently, Web3 payments are still in a relatively early stage of basic services and primitive states, primarily using digital currencies as payment mediums in scenarios such as cross-border remittances, OTC, and Payment Cards. This semi-centralized approach struggles to connect with the on-chain DeFi ecosystem, and the scenarios are relatively limited.

However, with the development and promotion of PayFi, this value transfer method based on blockchain and smart contract technology can accelerate the integration of Web3 payments and DeFi financial services, making digital assets more practical and efficient in daily transactions and more complex financial environments.

The emergence of PayFi can resolve the situation where traditional finance and crypto finance "live together for thirty years until the building collapses." In the future global financial ecosystem, PayFi will undoubtedly become a key driver for crypto to achieve mass adoption.

Raymond, co-founder of PolyFlow, has a deeper understanding of PayFi: "What PayFi addresses is not the apparent issues that Web3 payments need to solve, such as the challenges of cross-border fund transfers and low financial inclusion, but rather the most fundamental issue: effectively separating the information flow and capital flow of transactions, allowing everyone to form a consensus on the capital flow on the blockchain's unified ledger, thus enhancing the efficiency of the entire Web3 industry and promoting true mass adoption."

4. Why Solana for PayFi

In response to this question, Lily Liu provides the answer: "Solana possesses three major advantages: high-performance public chain, capital liquidity, and talent mobility." These advantages create a barrier that other competitors find difficult to cross at this stage.

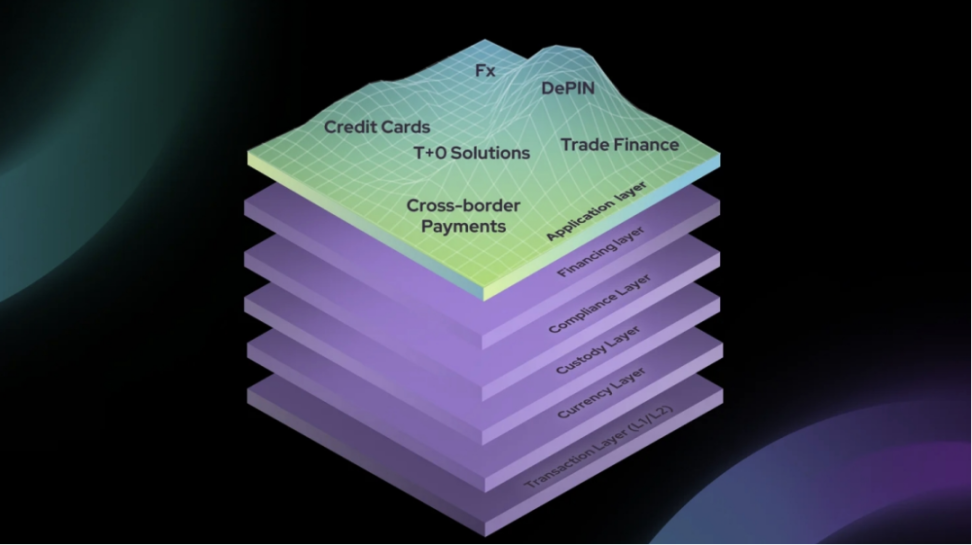

Additionally, we can look at it from the perspective of the PayFi Stack: What kind of infrastructure does PayFi need?

4.1 Blockchain Settlement Layer (Transaction Layer)

As the underlying infrastructure for settlement, although there are many blockchain settlement networks to choose from, Solana undoubtedly stands out. High throughput, low cost, fast settlement, and further performance improvements brought by the Firedancer upgrade can facilitate the rapid implementation of PayFi projects.

4.2 Currency Layer

In addition to the efficiency and smoothness of the underlying settlement network, there also needs to be sufficient liquidity support, especially stablecoins as on-chain trading mediums. We can see Solana's collaborations with Ondo Finance, Visa, Circle, and Stripe, as well as the launch of PYUSD in June this year.

According to DeFilama data, in August this year, the volume of PYUSD on Solana accounted for 64% of the market share, while Ethereum only accounted for 36%. Since 2023, the on-chain stablecoin volume has gradually increased from $1.8 billion to the current $3.6 billion, mainly including USDC, USDT, PYUSD, and USDY.

4.3 Asset Custody Layer (Custody Layer)

Asset custody is crucial in finance (on-chain/off-chain). For blockchain-based PayFi, considerations include ensuring the security of smart contracts, private key management, and compatibility with traditional finance and DeFi.

On-chain asset custody is key to achieving personal sovereignty. Not your Key, Not your Coin.

4.4 Compliance Layer (Compliance Layer)

It is well known that only by conducting user compliance checks can we further promote the healthy development of the financial payment ecosystem and services. Fundamentally, this requires ensuring that all transactions and capital flows comply with KYC/AML/CTF requirements while adapting to local legal regulations.

4.5 PayFi Application Layer (Application Layer)

Based on the aforementioned foundational layers, practical PayFi applications can be supported.

We can see at this year's BreakPoint event in Singapore that Solana has already built numerous application scenarios for the consumer end through its infrastructure, with its Consumer sector forming a trend of collective operation, possessing construction reserves far exceeding those of other public chains.

According to @ZKwifgut, the payments at the BreakPoint event included:

- Payment Scenarios: online shopping, social e-commerce, offline events, gaming

- Payment Medium: PayPal PYUSD, merchandise can be purchased on-site; MakerDAO bridging StableCoin to Solana via Wormhole; SOL debit card by Sanctum; Fusewallet virtual Visa card; Kast bank card;

- Payment Gateway: using StableCoin for shopping through Shopify Blinks; accepting StableCoin payments for booking flights and hotels based on Helio Pay/Solana Pay;

- Supply Side of Goods: consumer-grade hardware such as mobile phones / SIM cards / watches, event tickets, merchandise, e-commerce products (integrating Shopify), gaming items, etc.

- Payment Hardware: Solana official second-generation mobile phone Seeker; sports watch Showtime.

Solana is also actively laying out the B-end market. By raising funds through RWA, it provides liquidity support for payment scenarios in cross-border trade and supply chain finance.

Compared to Ethereum's positioning as an "asset chain," Solana is solidifying its position as a "payment chain," currently seen as the optimal solution for blockchain in consumer retail and payment-related products and services. In the words of @ZKwifgut:

PayFi and DeFi are the two legs of Solana's vast crypto ecosystem, and so far, no other ecosystem has such a clear strategy: building an On-chain Economy through DeFi and moving towards mass adoption through PayFi.

(Solana Breakpoint 2024 is ongoing)

(Solana Breakpoint 2024 is ongoing)

5. In Conclusion

In the long term, the entire Web3 industry is shifting towards off-chain and real consumption scenarios, which has become a major trend. Whether it is "making DeFi great again" or "leading Crypto towards mass adoption," these slogans often mentioned in the market can finally be realized through PayFi.

This time, the wolf has truly come.

Blockchain and smart contract technology can make traditional payments faster and cheaper than ever before, but these use cases that help traditional markets reduce costs and increase efficiency are more about capturing value in the traditional payment B-end, which is good, but not what you and I desire.

PayFi can truly bridge the traditional financial market and the crypto financial market, and through the rise of stablecoins, accelerate the integration of payment and financial services, not just reducing costs and increasing efficiency, but creating an entirely new financial market. In this market, you have me, and I have you.

In the future financial ecosystem, PayFi will become a key driving force.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。