In 2023, Arthur Hayes and former BitMEX Head of Business Development Akshat Vaidya co-founded the investment firm Maelstrom Capital, with Vaidya serving as the Chief Investment Officer. Maelstrom is set up as Hayes's family office, funded by Hayes himself, which means there is no need to deal with LPs (after all, it's all Hayes's money), and there is no rush to allocate capital to earn management fees, allowing for sufficient "patience." This also showcases the different investment styles between family offices and VC firms.

Hayes stated, "We want to look for truly quality projects; this is not a 'spray and pray' game (referring to a scattergun investment approach followed by hoping for success), because we don't have external LPs (after all, it's our own money, so we need to be cautious)." At a time when the current market is maturing but still lacks a clear path forward, BlockBeats had the privilege of interviewing Maelstrom's co-founder Akshat Vaidya to discuss the development of family offices in the crypto space and their market perceptions.

During the interview, BlockBeats asked whether Maelstrom would participate in the current hot market trend of buying meme coins. Akshat responded that they do not directly engage in meme coin trading but instead invest in the infrastructure that supports the creation and dissemination of meme coins, indirectly capturing the value brought by the meme coin phenomenon.

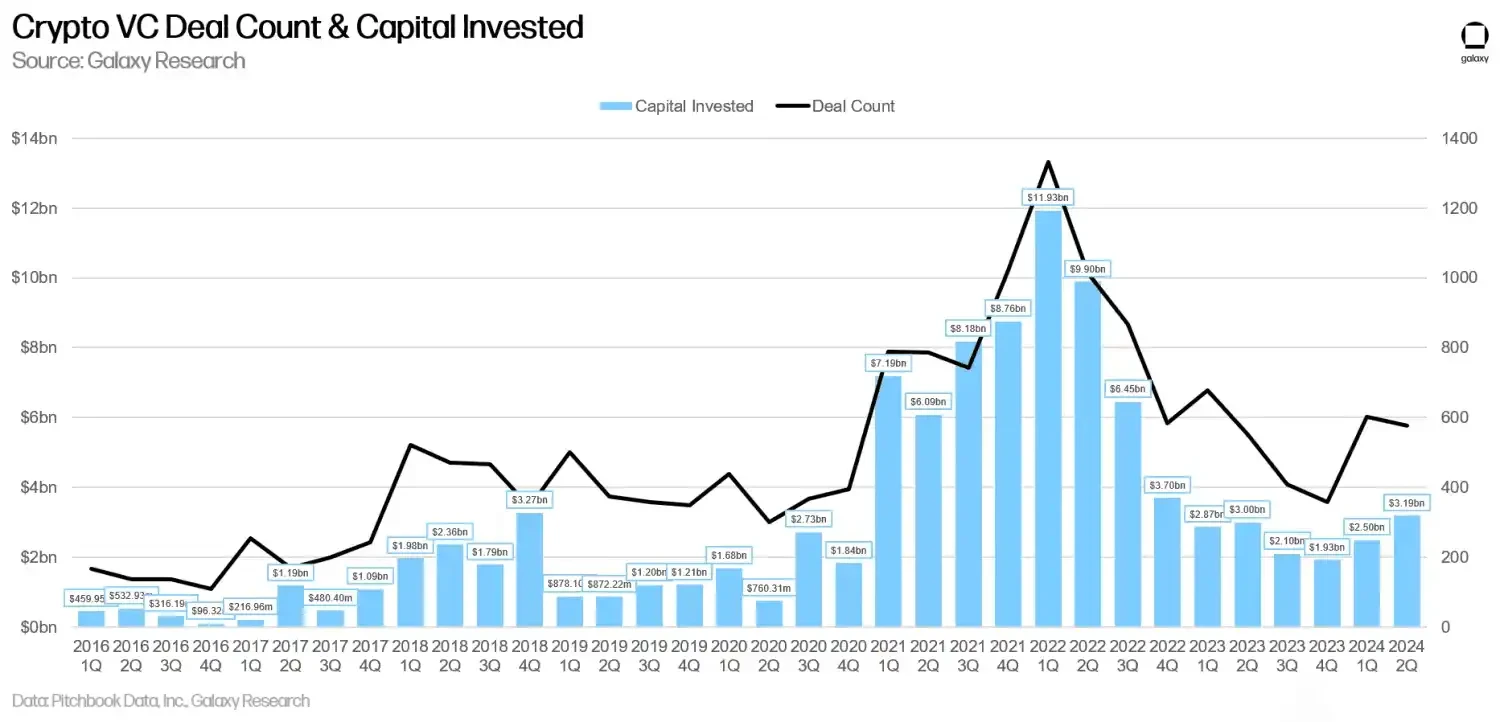

Contrary to the common belief that crypto infrastructure is overly saturated, Maelstrom's main investment portfolio still targets infrastructure companies. Both Hayes and Akshat believe that during this phase of the cycle, infrastructure is meaningful, stating, "Everyone is looking forward to user scaling, but the market does not yet have enough infrastructure to support such a large user base."

Here is the original interview:

BlockBeats: How did you meet Arthur Hayes?

Akshat: I started buying Bitcoin in 2013, around the time Arthur was starting to create BitMEX. By 2019, BitMEX had become the largest cryptocurrency trading platform in the world by annual trading volume (in nominal dollars), and I decided to leave the traditional finance industry to fully immerse myself in the crypto space. At that time, I was living in Chicago and working at a mid-sized private equity firm.

At a Maelstrom event, Akshat is in the center; image source: X

I remember I stumbled upon a job posting for a "BitMEX Ventures Investment Associate," which specified "Hong Kong applicants only." Nevertheless, I submitted my application and eventually succeeded in the interview, which is how I first met Arthur. After joining BitMEX, I initially worked under several levels of Arthur, gradually promoted to become the Head of Business Development and M&A for the company.

BlockBeats: Why did you choose to leave BitMEX to work with Arthur Hayes on this family fund?

Akshat: In the summer of 2022, I discussed the future direction of BitMEX Ventures with Arthur and proposed a concept called the "Centennial Portfolio." I envisioned creating an investment fund that leverages Arthur's unique advantage as one of the youngest billionaires in the world—time—to invest in future technologies and scarce assets, including water rights and cryptocurrencies. He was very interested in the idea but suggested we start on a smaller scale, focusing on our area of expertise—cryptocurrencies.

Arthur Hayes's influence on Maelstrom's operations

BlockBeats: How much capital does Maelstrom currently manage? What are the main responsibilities of the Chief Investment Officer?

Akshat: We do not publicly disclose our assets under management (AUM), but based on our publicly available portfolio, it is not difficult to estimate a rough figure. I am responsible for proposing investment strategies, executing trades, and managing Maelstrom's venture capital portfolio. In 2022, the team consisted only of Arthur and me. Now, I lead a full-time team of six traders, investors, and researchers, and we expect to further expand the team in the next bear market.

BlockBeats: How does a family fund in the crypto space operate differently from a VC?

Akshat: As one of the most influential builders in the crypto space, Maelstrom can provide operational support to its portfolio companies that is difficult for other investors to offer. Many funds excel in investment decision-making, but very few are led by individuals who have successfully built profitable unicorns in the crypto space.

In contrast, VCs typically have an obligation to deploy capital, so they are more likely to lower investment standards to ensure funds can be put to work. This is also why they often perform worse than family offices.

Additionally, venture funds charge their LPs a 2% management fee, so they are incentivized to continuously raise larger funds to maximize management fee income. Family offices do not have this incentive mechanism, allowing them to focus more on finding high-quality investment opportunities, conducting thorough due diligence, negotiating better investment terms, and providing substantial assistance to portfolio companies.

BlockBeats: How much influence does Arthur Hayes and his ideas have on your investment decisions?

Akshat: Our investment team operates independently, with Arthur as the final decision-maker responsible for approving or rejecting each investment. His macro theories are one of the important references for us in formulating investment strategies. In terms of portfolio management, Arthur is more involved. Once we invest in a company, Arthur becomes a supporter of that company, and his influence permeates the entire portfolio.

The advantages of combining CeFi and DeFi, indirectly benefiting from meme coin trends

BlockBeats: From Maelstrom's portfolio, your investments in the DeFi space are particularly prominent. What is the logic behind this?

Akshat: CeFi has always been seen as a bridge from traditional finance to DeFi. In the long run, we believe that capital formation and value capture will gradually shift towards permissionless decentralized systems. However, in the short term, the combination of CeFi and DeFi can leverage the strengths of both. For example, Ethena is a typical case.

BlockBeats: Ethena is a project that Arthur is particularly optimistic about, but it has recently faced community skepticism due to its underwhelming price performance. What do you think is the biggest issue Ethena is currently facing? What can or should the team and community do to turn the situation around?

Akshat: All value investors understand that less than six months is insufficient to evaluate any serious investment, whether in the cryptocurrency space or elsewhere. While this does not constitute investment advice and everyone should conduct their own research, overall, investing in profit-generating protocols like Ethena that focus on real applications is more akin to a long-term layout in the venture capital stage rather than a get-rich-quick scheme.

Based on on-chain and off-chain data, Ethena has been very successful in finding initial product-market fit and has become one of the fastest-growing decentralized finance products in history. Since its launch at the beginning of this year, its user base, TVL, and partnerships have continued to grow, and the product mechanism has operated as expected in different scenarios (such as this summer's market correction).

The team is focused on creating long-term value. Recently, Ethena announced a partnership with traditional financial giant BlackRock to launch a new UStb product, which will be used alongside the existing USDe. Ethena will become the only issuer 100% supported by BlackRock's BUIDL, and through this stablecoin, it will expand collateral options, allowing CEX partners to choose to launch USDe, UStb, or both simultaneously, which will help drive the realization of long-term value.

BlockBeats: Arthur often promotes some meme coins on X, and more and more meme trading tools are making meme trading gradually become a major active market in the Chinese community. What do you think is the main development trend of meme coins? Will Maelstrom consider investing in meme projects?

Akshat: We view meme coins as a cultural phenomenon and would never underestimate anything that can bring attention to the crypto space, attracting engineers and resources. However, as a venture capital fund focused on building infrastructure for a permissionless future, Maelstrom does not directly engage in meme coin trading. Instead, we invest in the infrastructure that supports the creation and dissemination of meme coins, indirectly capturing the value brought by the meme coin phenomenon. Arthur personally is keen on meme coin trading, and if you want to understand his views on specific meme coins, you can follow his X account.

BlockBeats: There is currently strong resistance in the market towards the concept of "VC coins." What do you think is the problem with "VC coins" from Maelstrom's perspective?

Akshat: The incentive mechanism of VC funds drives them to continuously raise more capital because they profit in two ways: a 2% management fee and a 20% performance share. Most VC funds perform even worse than simple passive investment strategies, making the 2% management fee one of the most "secure" income sources for VC fund managers. This leads them to primarily aim to raise larger funds, even if there are no suitable capital deployment opportunities.

In the crypto space, VC funds typically repeat similar operational patterns:

1) Relying on the success of founders, industry leaders, or investors in small-scale investments to raise VC funds;

2) Investing in early-stage projects, even when high-quality investment opportunities are limited;

3) Inflating valuations in each round of financing and pushing tokens to list on CEXs at inflated valuations;

4) Quickly raising a new round of funding, using unrealized performance records to fundraise. Although the funds may appear to perform well on paper, this is mainly due to key projects being listed by CEXs like Binance at valuations of 30 to 50 times, while these tokens have not fully circulated. Once they do circulate, token prices often drop by 50%-75% or even more.

Ultimately, the ones bearing the losses are retail investors and the limited partners of VC funds. This is also one of the reasons I prefer the family office model, as the incentive mechanisms of family offices align completely with the interests of the shareholders (in the case of Maelstrom, that is Arthur).

BlockBeats: Recently, more and more people in the industry have started discussing fundamentals such as project profitability and sustainability. Do you agree with this new line of thinking in the industry? In your view, has the crypto industry reached a stage where it must explore profit models? Will Maelstrom's investment strategy and thinking change as a result?

Akshat: Investing in early-stage crypto projects is essentially no different from investing in early-stage startups, whether it's your uncle's laundromat, a friend's consumer application, or a VC-backed tech service company. Before deciding whether to invest in a project, comprehensive due diligence must be conducted to assess various factors, including the founding team, product, roadmap, business model/revenue model, legal strategy, operational status, competitive landscape, token value accumulation mechanisms, and token economics.

Will there be another bull market?

BlockBeats: The Federal Reserve has recently begun a rate-cutting cycle. Do you think this could be a key catalyst for a new round of crypto bull markets? What impact might the recent situation in the Middle East have on the crypto industry?

Akshat: Personally, I believe we may face two risks in the coming months that could lead to a rise in short- to medium-term inflation:

Regulatory agencies returning to loose monetary policy;

Supply-side disruptions (such as escalating wars in the Middle East affecting oil supply chains and strikes by U.S. port workers).

If U.S. economic growth remains strong, regulators will have straightforward tools to address rising inflation. However, if the U.S. economy slows down, the Federal Reserve may find itself in a dilemma between tightening policies to control inflation or loosening policies to stimulate economic growth. In this scenario, speculative crypto assets (like meme coins and early projects) may perform worse than digital gold (like Bitcoin) and mature crypto products with actual protocol revenue and cash flow.

BlockBeats: Many people believe that from the perspective of industry innovation and fundamentals, cryptocurrencies do not seem ready for a new bull market. Do you agree with this view? What do you think will be the main driving forces of the new cycle?

Akshat: The growth process of the crypto industry is similar to that of the human genome, a child, or a developing country, gradually maturing through phases of rapid growth. I started investing in cryptocurrencies in 2013 and have experienced multiple cycles:

The 2013/2014 cycle was the stage where Bitcoin found its initial market fit as a store of value (prior to this, Bitcoin was still proving to core users that its decentralized P2P trading system was viable);

The 2017/2018 cycle focused on exploring the potential of smart contracts after Ethereum and other smart contract networks achieved initial success;

The 2021/2022 cycle was about smart contracts (especially Ethereum) finally finding their first real application scenario (DeFi);

The 2023/2024 cycle will focus on expanding DeFi infrastructure (L1, L2, money markets, etc.), far beyond the initial use cases.

I believe the upcoming cycle will be driven by several key factors:

The integration of traditional finance (TradFi) with crypto technology;

Governments around the world beginning to view crypto as a strategic priority;

The development of decentralized physical infrastructure networks (DePIN).

Currently, there are numerous preliminary experiments underway in the DePIN field, and success is just a matter of time. This will attract more users, investors, engineers, and new application scenarios into the crypto space. As DePIN matures, crypto technology will integrate into people's lives in ways beyond our imagination.

Additionally, there are many long-term catalytic factors, simply listed as follows:

The entry of traditional financial giants and the gradual recognition of cryptocurrencies in global investment portfolios;

The emergence of the wealthiest generation with the highest financial and crypto literacy (Generation Z and young people) entering the workforce;

The first millennials interested in cryptocurrencies beginning to inherit wealth from the previous generation;

The accumulation and gradual intensification of long-term risks within the existing monetary system.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。