This article will take Berachain, Initia, and Injective as examples to focus on three key aspects that address the limitations of existing token economics and promote sustainable design.

Author: Eren

Compiled by: Deep Tide TechFlow

Key Points

Currently, there are many L1 projects in the market dedicated to specific missions, such as high-performance EVM, optimized Rollup execution environments, or IP tokenization, which propose and promote new L1 solutions. Among these projects, which ones can achieve sustainable growth and become the next generation of L1 blockchains? This article explores token economics, which is as important as technical capabilities and community in Layer 1 projects.

When designing L1 token economics, three aspects need to be emphasized: 1) mechanism design, 2) alignment with architecture, and 3) value capture. Based on these principles, ecosystem participants should prioritize their own interests while promoting network growth through collective economic behavior. The economic model should match the unique technical architecture of L1 and ensure that tokens can capture value as network activity increases.

L1 token economics that meet these key points include Berachain (PoL), Initia (VIP), and Injective (Burn Auction). These projects actively adjust token economics at the network level, proposing unique token economic solutions by regulating the supply and demand of tokens, adjusting the interests among participants, or designing new economic models for the technical architecture.

1. Introduction: The Transformation of Layer 1 Token Economics

Recently, projects that have received significant attention and investment, such as Berachain, Monad, Story Protocol, Initia, and Movement, share a common feature: they are all upcoming Layer 1 (L1) blockchains. These projects choose to develop their own L1 solutions rather than building Layer 2 (L2) on Ethereum or developing a single protocol. This strategy allows them to build unique ecosystems through specific functionalities and economic models. Each project enters the market with a specific mission, such as high-performance EVM, optimized Rollup execution environments, or IP tokenization, proposing and promoting new L1 solutions.

The question is: among these projects, which ones can achieve sustainable growth and become the next generation of L1 blockchains? In the evaluation, a key factor that is as important as technical capabilities and community participation is the robustness of their token economics.

Source: Foundations of Cryptoeconomic Systems

L1 blockchains can be likened to a country. The L1 network corresponds to the country, the ecosystem protocols constitute the local economy, and users or communities are the participating entities. In this framework, tokens serve both as economic incentives and reserve currencies, organically connecting various economic units.

In this context, what role does token economics play in the "country" of L1 blockchains? As an economic system, token economics incentivizes network participants to actively engage in activities to ensure the network operates actively. At the same time, it maintains the stable value of tokens by regulating supply and demand.

Therefore, the design of token economics is akin to a country's economic system. When designing an economic system, a country considers geographical conditions, industrial structure, political systems, and culture. Similarly, the token economics of an L1 blockchain must reflect its technical architecture, Dapp ecosystem, governance model, and community characteristics.

However, many L1 blockchains that emerged during the ICO boom from 2017 to 2019 did not consider their unique network characteristics and instead adopted one-size-fits-all token economics. This has led to the emergence of some "billion-dollar zombie blockchains," which, despite high valuations, have not achieved significant accomplishments.

In contrast, recent trends in token economics show a more refined approach. These approaches include directly regulating the supply and demand of tokens at the network level, introducing token economics suitable for the technical architecture, and clearer role assignments to coordinate the interests of validators, protocols, and users. This article will use Berachain, Initia, and Injective as examples to explore this trend, focusing on three key aspects that address the limitations of existing token economics and promote sustainable design.

2. The Flaws of the Token Flywheel and Its Three Pillars of Solution

2.1 Basic Overview of Tokens and Token Economics

2.1.1 The Role of Layer 1 Tokens

"Why do we need tokens?" While tokens are effective tools for blockchain projects, the answer to this question is not always obvious. However, for L1 networks, the demand for tokens is clearer, as they are used at the core level to reward validators and pay network fees. The native tokens of L1 primarily serve three functions:

Reserve Currency: Users need to pay network fees with native tokens when using block space. For blockchains that embed L2, when L2 uses the main chain as a data availability (DA) layer, native tokens are also used to pay for storage costs.

Incentive Tool: Validators receive block rewards in the form of native tokens after honestly verifying the legitimacy of transactions. Additionally, unique L1 features like unified liquidity are also incentivized through native token rewards.

Unit of Value: The native tokens issued by L1 directly or indirectly represent the value created by L1. Market participants trade tokens like $ETH based on their assessments of Ethereum's business performance and market position.

2.1.2 The Role of Layer 1 Token Economics

While tokens have their specific roles, the function of token economics lies in controlling the flow of tokens. This concept is often narrowly understood as adjusting supply through burn mechanisms or adopting specific token distribution methods (such as maximum supply, distribution ratios, unlocking plans, etc.). However, in our discussion, token economics encompasses not only these mechanisms but also the incentive systems that coordinate participant interests, the actual use of tokens, and revenue distribution models—essentially forming a complete economic system based on tokens.

In this context, the core role of token economics is to establish a system that incentivizes participants to take expected actions, thereby ensuring the normal operation of the L1 network. Specifically, it encourages behaviors beneficial to the network, such as enhancing security or providing liquidity, through the design of reward structures. For the reward system to be effective, the rewards must hold sufficient value to attract contributors. Therefore, token economics must also include mechanisms to regulate token supply and demand to maintain the value of rewards.

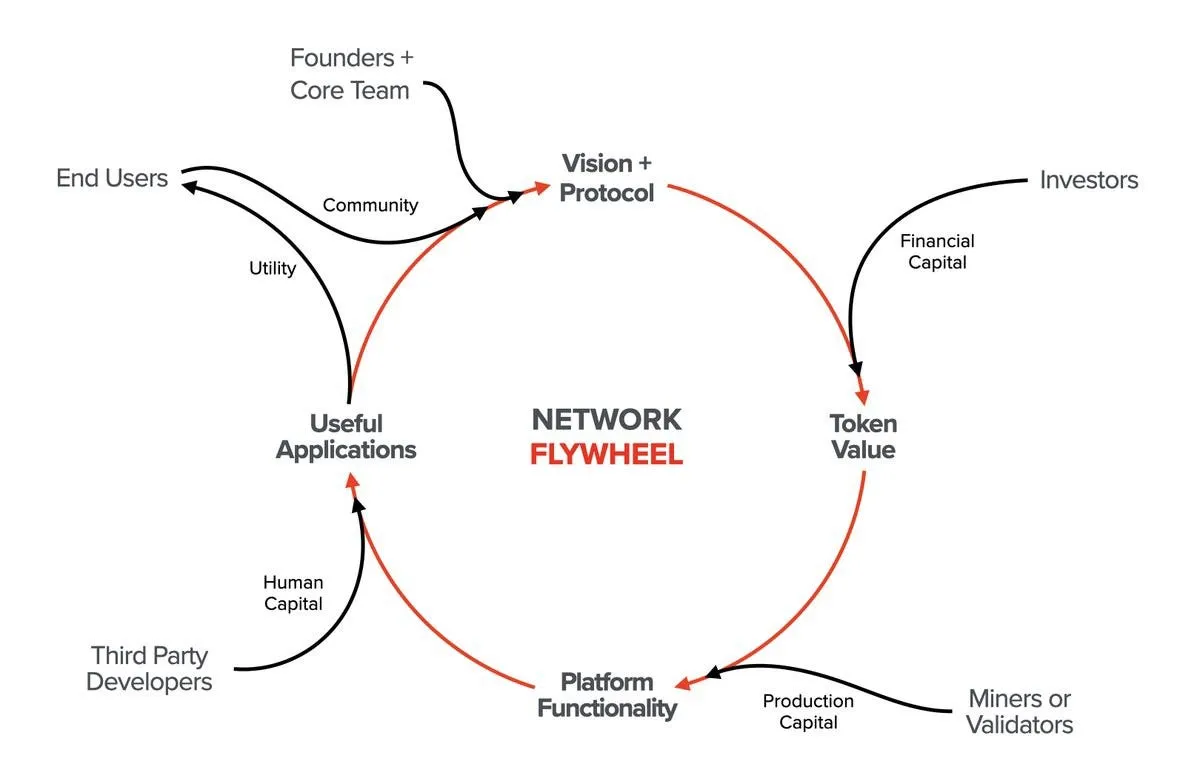

2.2 The Circular Growth Structure Created by Token Economics: The Token Flywheel is the Ultimate Goal

Source: X(@alive_eth)

Well-designed token economics can generate a flywheel effect, allowing value to circulate within the network and promoting its natural growth. This model assumes that the interactions between validators (responsible for blockchain security), developers (building applications), and users (forming the community) construct a circular growth structure. Through "network effects," these interactions achieve economies of scale, accelerating the expansion of the network. Let’s trace the implementation process of the flywheel effect from the ground up:

After the core team presents a new vision to the market, initial capital is used to complete the infrastructure of the L1 network, generating token value in private or public markets.

As the value of tokens increases, validators exchange support for the network's supply side for token rewards. For example, validators earn block rewards by verifying transactions, thereby providing security and functionality to the network.

Once the functionality and security of the L1 network stabilize, developers begin to join and build valuable applications.

These applications provide real value to end users, thereby driving demand for tokens. In this process, the community formed around users gradually becomes supporters of the L1 network.

As network activity increases and the community grows, the demand for tokens also rises. Tokens serve not only as reserve currencies for paying network fees but also as units representing the value of the network. Therefore, market demand for tokens is also increasing.

With the increase in token demand, validators have a stronger incentive to support the security and functionality of the network. This improves the network's security and development environment, further encouraging developers to create more useful applications that provide more value to users. This process, in turn, enhances token demand, strengthens the incentive mechanism, improves network security and functionality, promotes application development, makes the community more active, and ultimately forms the flywheel effect.

Once the flywheel effect is initiated, the L1 network can achieve self-sustaining growth. At this point, the development of the network no longer relies entirely on the core team's push but accelerates autonomously through token incentives. This flywheel effect fully leverages the potential of token economics and is often regarded as the ultimate goal pursued by all token economics.

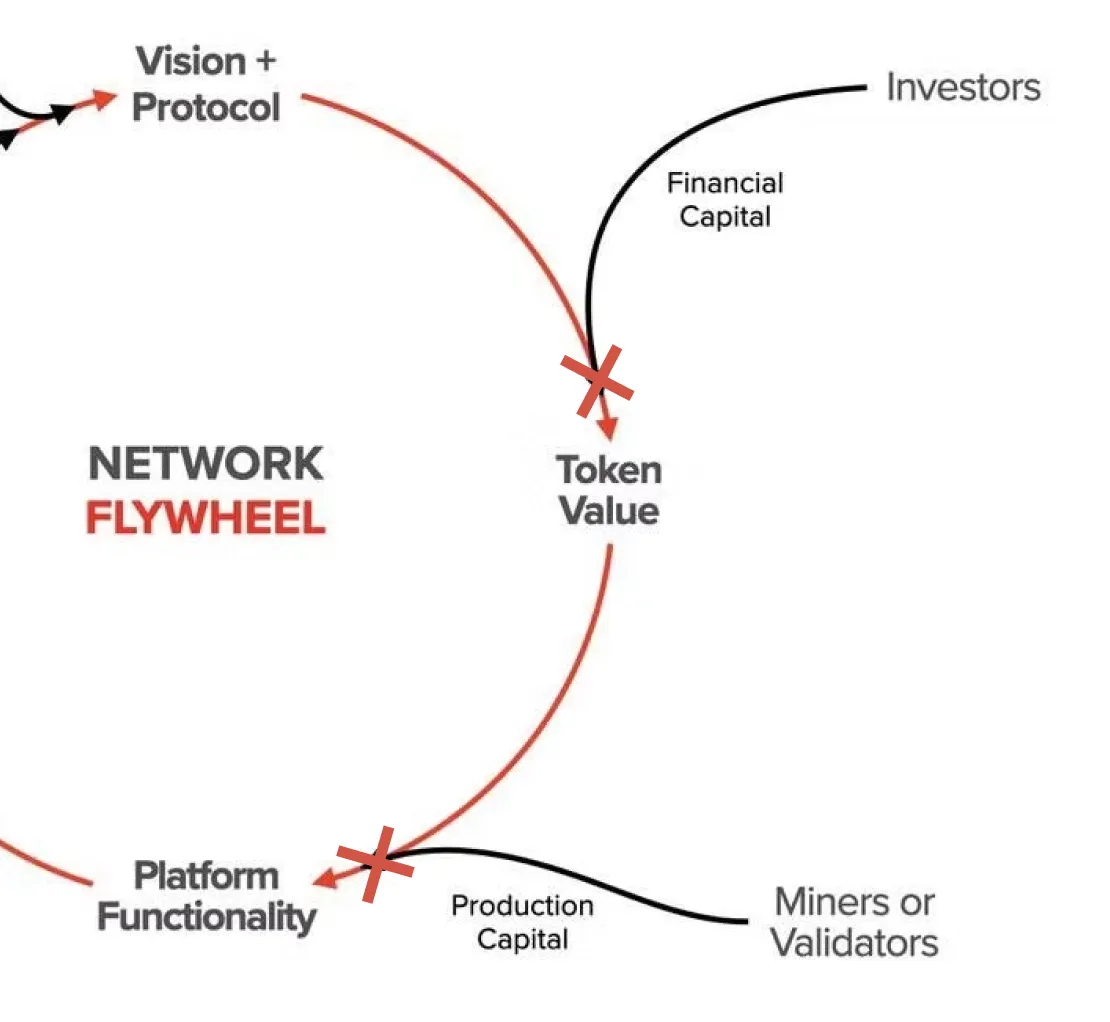

2.3 Three Challenges to the Token Flywheel: No, the Token Flywheel is Just a Conceptual Label

Source: X(@alive_eth)

The flywheel model is based on certain assumptions when constructing a circular growth structure. It posits that as network activity increases, token demand will also grow in tandem, laying the foundation for enhancing the incentive mechanisms for ecosystem contributors. At the same time, it assumes that higher incentives will encourage validators to contribute to the ecosystem in various ways, thereby creating an environment conducive to developing more useful applications. We need to question these seemingly obvious assumptions. Many existing L1 networks encounter difficulties in building sustainable token economics, often lacking key elements in three areas:

2.3.1 Are the incentives of all participants truly aligned?

There are various types of participants in an L1 network, each with different interests in the ecosystem. If the structure to coordinate these complex interests for growth collapses, the flywheel effect will cease. Specifically, we need to question whether validators will indeed contribute to the ecosystem in other ways as described by the flywheel model when token demand increases and the interests of participants are enhanced.

The interests of validators are closely tied to the growth of the ecosystem. Their block rewards are distributed in the native tokens of L1, so an increase in token demand and value is beneficial for them. Additionally, as the application ecosystem attracts more users and increases transaction volume, network congestion may worsen, thereby enhancing the incentives for validators. Most L1 networks, such as Ethereum's PoS network, adopt a gas fee mechanism, where validators can earn higher fees during network congestion. However, the lack of a direct mechanism at the network level requiring validators to contribute to the ecosystem results in a loose relationship between validators and the protocol or users. The lack of a direct link between enhanced validator incentives and ecosystem activity leads to insufficient motivation for contributions to the ecosystem. Conversely, when individual stakers cannot obtain significant rewards, users or protocols lack clear methods or incentives to enhance economic security. The low governance participation rates commonly seen across all L1 ecosystems indicate that individual users lack a clear motivation to actively participate in network consensus. In other words, there is no direct connection between the interests of validators and those of other ecosystem participants.

2.3.2 Does increased network activity lead to increased token demand?

It is difficult to determine whether the increase in network activity, driven by the emergence of applications and an increase in users, will necessarily lead to an increase in token demand. If there is no inherent or strong structure linking network activity to the demand for native tokens, then network activity and token demand may not align. As will be discussed in detail later, Ethereum currently faces a situation where L2 activity is increasing, but the factors driving $ETH demand are low. Like Ethereum, every blockchain network has its unique technical architecture, and thus, token economics should effectively reflect these architectural characteristics.

2.3.3 How do tokens achieve value capture?

While this question is similar to the previous one, we can explore it from another angle: how do tokens achieve value capture? Assuming the flywheel model can operate ideally, will the growth in token demand due to network activity necessarily lead to an increase in token value? Clearly, an increase in token demand does not directly equate to an increase in token value. Setting aside market speculation (which is often unrelated to the fundamental growth of the ecosystem), simple calculations indicate that token demand must exceed the supply of newly issued tokens for value to increase. Therefore, there needs to be a mechanism to increase token demand or reduce supply when the network is active. However, this mechanism is sometimes overlooked or fails to operate effectively, leading to the inability to realize the feedback loop of "network activation → increased token demand → increased token value."

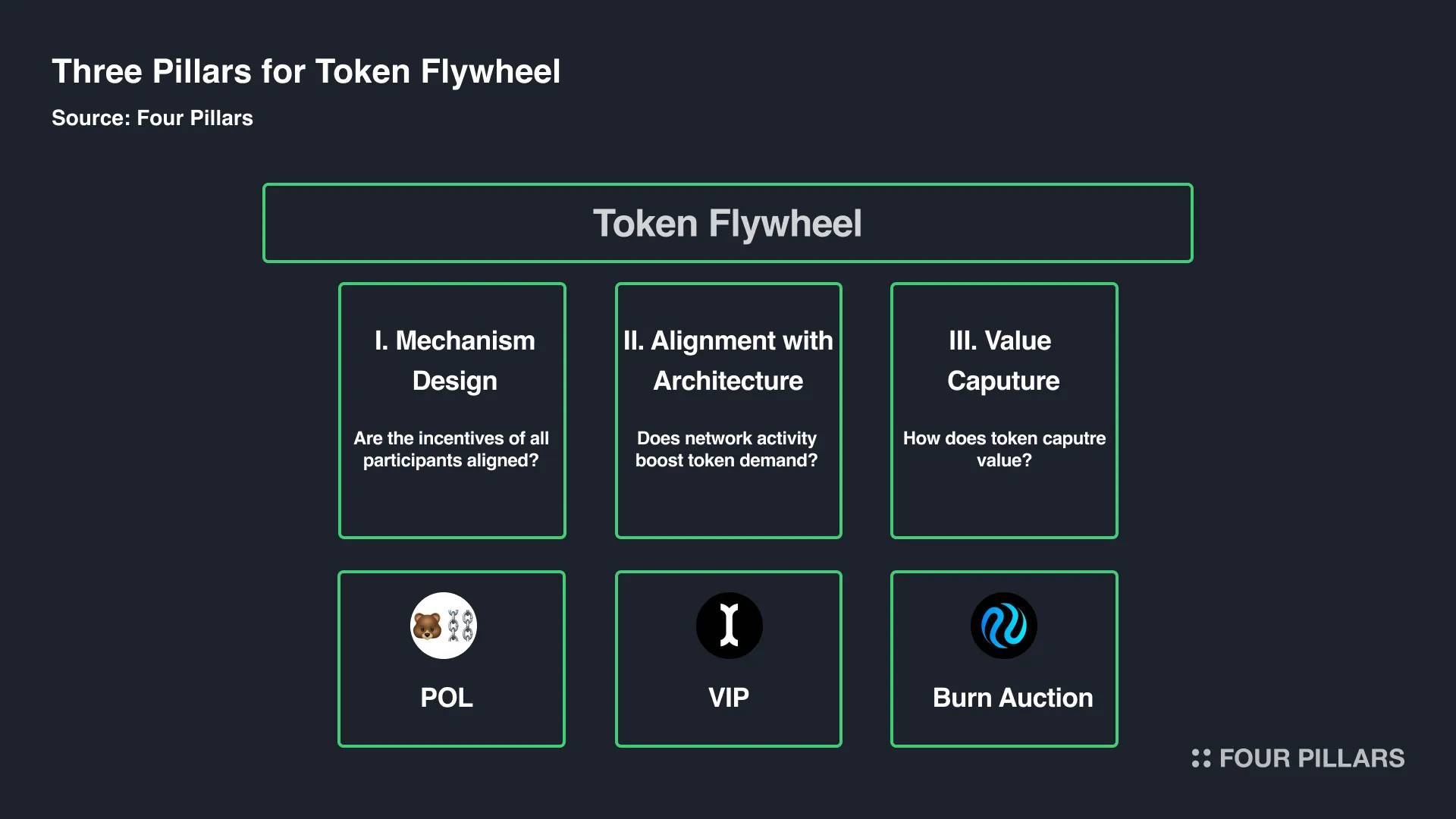

2.4 Correcting the Token Flywheel: Three Pillars

To summarize the content so far, L1 tokens serve as the reserve currency of the network, act as tools for incentivizing contributions, and represent the unit of value created by the network. L1 can coordinate the interests of ecosystem participants through the construction of token economics, functioning as an economic system that ensures the active operation of the network through tokens and incentive mechanisms. Well-designed token economics have the potential to create a self-sustaining growth of the network through the value generated by token incentives circulating within the network.

However, our ideal token flywheel often does not align with the phenomena observed in actual L1 networks. This is because the positive feedback mechanisms intended to guide participant behavior or value connections have not been effectively realized. Specifically, it is due to a lack of sufficient consideration of whether the incentives of all participants are truly aligned, whether network activity can drive an increase in token demand, and whether value can be accumulated in the tokens.

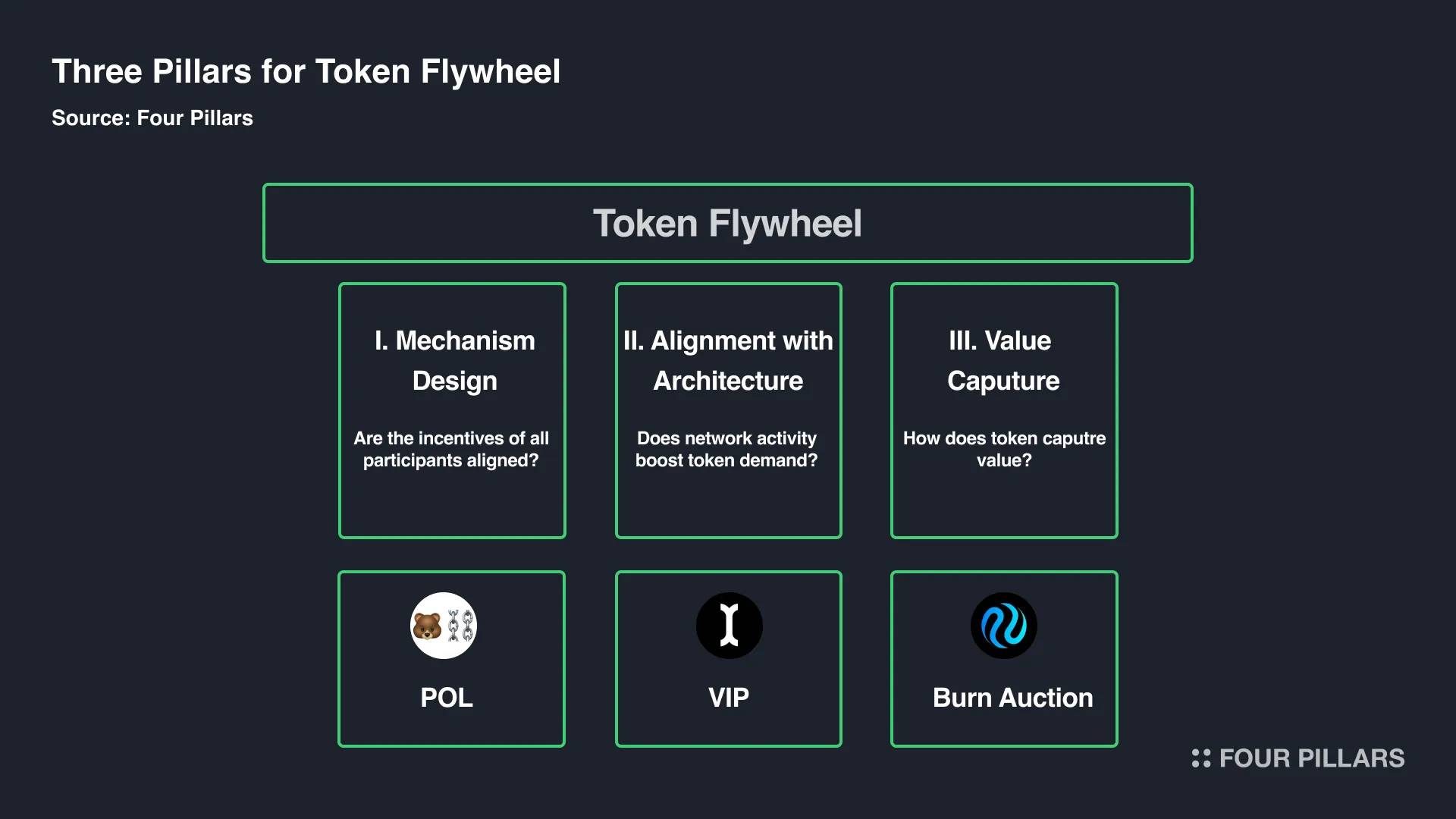

These limitations often lead to a loss of sustainability in token economics for many existing L1 networks. Therefore, when exploring the development direction of the next generation of L1 token economics, we need to analyze these past limitations in greater detail. To this end, we can transform the questions regarding the token flywheel into key points for the design of L1 token economics: I. Mechanism Design, II. Consistency with Architecture, III. Value Capture. In the next section, we will continue to explore the limitations of existing token economics and their causes through case studies, while clarifying these key points.

I. Are the incentives of all participants truly aligned? → Mechanism Design

II. Does increased network activity lead to increased token demand? → Consistency with Architecture

III. How do tokens achieve value capture? → Value Capture

3. Lessons Learned from Millennial L1 Networks

Due to the complexity of token economics, analyzing token economics cases from a single factor may lead to a one-sided understanding of the phenomena. However, as a method for exploring sustainable token economics, attempting to identify the limitations encountered in existing cases and learning from them is an effective approach. We can concretize the three pillars supporting the flywheel of token economics by analyzing the following aspects: 1) the challenges Bitcoin faces in mechanism design, 2) the inconsistency between architecture and token economics in Ethereum, and 3) the structural limitations of Arbitrum tokens in failing to effectively capture network value.

3.1 Pillar I - Mechanism Design: Bitcoin

Bitcoin has been one of the most innovative inventions since the advent of blockchain and has also become an important asset in traditional financial markets. However, there is a significant gap between Bitcoin's original intent and its current role. As Bitcoin gradually evolves into an asset, its initial incentive mechanism design is no longer suitable for its current function, raising concerns about the future sustainability of Bitcoin's security incentives. This reality is reshaping Bitcoin's development roadmap. Let us delve into the case of Bitcoin, focusing on its mechanism design, which can be summarized as "how much reward to provide, how to provide the reward, and what behaviors are desired from participants."

3.1.1 Bitcoin Token Economics: The Premise of Halving

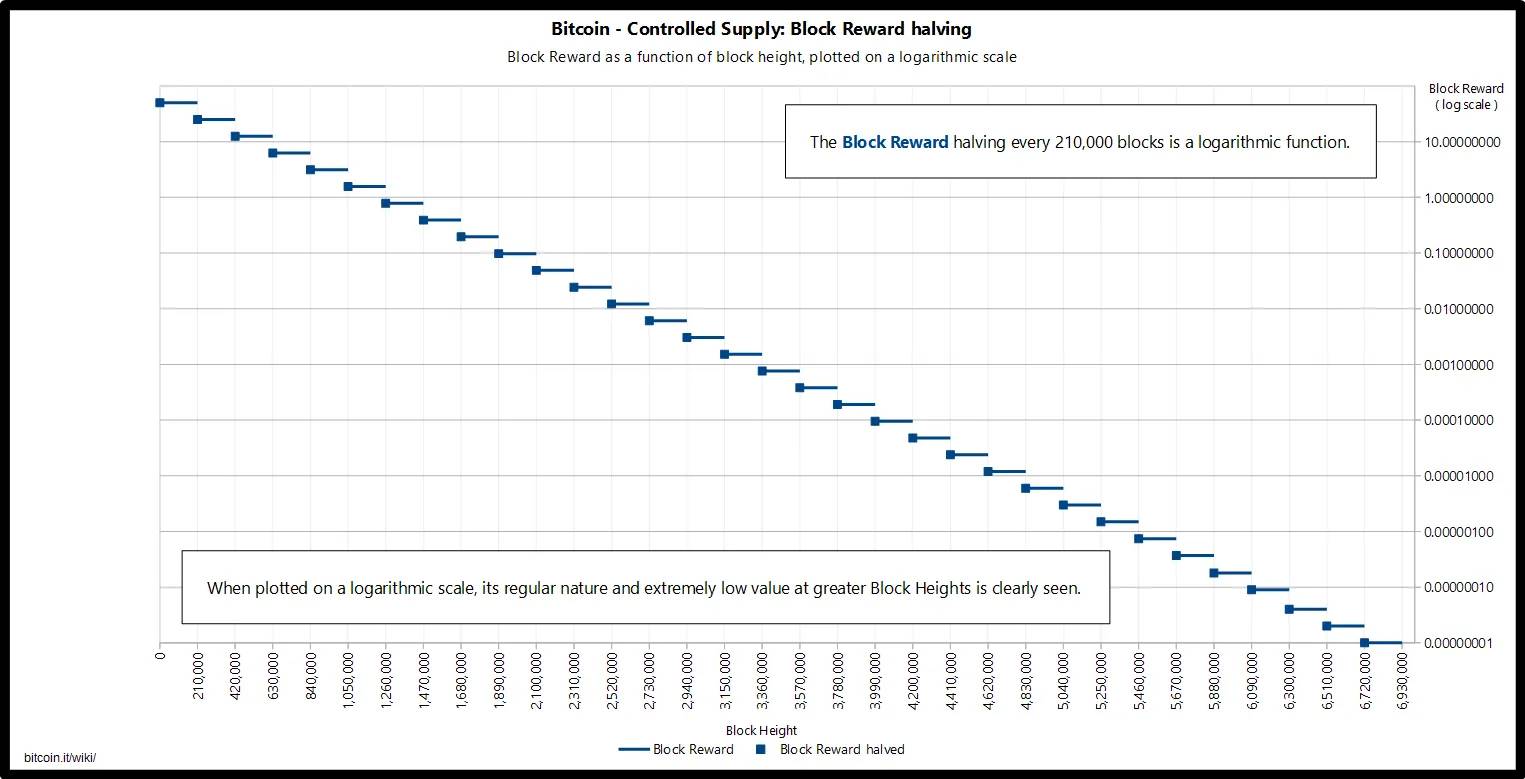

The mechanism of Bitcoin can be summarized as follows: it combines network security with node incentives by rewarding miner nodes that generate valid blocks under the PoW (Proof of Work) consensus algorithm. Nodes participating in the network must compete to compute hash values, consuming computational power to obtain block rewards and add valid blocks to the longest chain. For malicious nodes, attacking the network requires controlling more than half of the PoW computational power. This is extremely difficult to achieve in practice, and even if successful, attackers would lose motivation, as the attack would lead to a decrease in Bitcoin's value, resulting in their own losses. Through this mechanism, Bitcoin achieves Byzantine Fault Tolerance (BFT) and operates as a decentralized currency system through node consensus without relying on third-party trust.

Source: Bitcoin Wiki

Thus, the block rewards received by miner nodes are crucial for maintaining Bitcoin's decentralization and security, as they incentivize nodes to act honestly and actively participate in the Proof of Work process. However, a deeper analysis of Bitcoin's reward mechanism reveals that to limit inflation, block rewards are halved approximately every four years, eventually ceasing altogether. Consequently, miners will increasingly rely on transaction fees rather than inflationary block rewards.

This halving reward mechanism is designed based on the assumption that Bitcoin will ultimately become a payment currency, with transaction fees completely replacing miner rewards. Unlike its current role as a "store of value" (SoV), Bitcoin's original goal was to replace centralized electronic payment systems. However, it is well-known that Bitcoin faces scalability issues as a payment currency, while solutions like USDC or USDT have become effective alternatives for payment currencies.

To address these challenges, some have proposed that Bitcoin needs to adjust its strategy, summarizing its mining incentive solutions as follows. One possible scenario is that as Bitcoin supply decreases, its scarcity naturally increases, which may resolve related issues. Ultimately, as Bitcoin truly becomes a store of value, its value may rise significantly, providing sufficient incentives for block generation even without mining rewards. Another solution is to develop Bitcoin into a programmable asset and network through projects like BTCFi or Bitcoin L2. This approach aims to make Bitcoin more productive.

3.1.2 The Importance of Mechanism Design Revealed by Bitcoin

Although discussions about Bitcoin's scalability continue, the potential future lack of miner incentives, which contradicts the original token economics design, raises key questions about Bitcoin's sustainability. If mining rewards eventually cease, it is possible that no one will be willing to invest computational power to obtain the rights to generate blocks, which could lead to Bitcoin transactions being unable to be recorded on the blockchain. Therefore, the market has begun to focus on how to gradually increase transaction fees to replace mining rewards, making Bitcoin a more productive asset. This task has become a significant driving force for attracting developers and expanding the Bitcoin ecosystem.

The case of Bitcoin highlights the importance of mechanism design in token economics, specifically "how to provide rewards, how much to provide, and what behaviors are desired from participants." Here, mechanism design refers to setting specific contexts and incentives that encourage participants in token economics to take actions that maximize their returns. Mechanism design is also known as "reverse game theory." While game theory predicts how individuals make strategic decisions to align with their interests, reverse game theory designs optimal mechanisms that allow individuals to pursue their interests while collectively achieving a certain goal. In other words, it ensures that validators responsible for network security, protocols, and users can maintain the smooth operation and sustainable development of the L1 network while pursuing maximum benefits.

3.2 Pillar II - Architectural Alignment: The Case of Ethereum

Architectural alignment can be understood as whether the technical structure of a blockchain is compatible with the economic model it relies on. L1 networks adopt various technical architectures, from consensus algorithms to transaction computation structures, as well as the existence of L2. For example, some L1 networks have specific goals, such as the Monad blockchain achieving high-performance EVM networks through parallel transaction processing, or the Story network focusing on IP tokenization, all of which require unique technical architectures. However, is merely adjusting the architecture sufficient? As the architecture changes, the types of participants in the network and their interests also change, necessitating an optimization of the economic model to adapt to the new architecture. From this perspective, we can explore whether the architecture and token economics are aligned. The recent challenges Ethereum has faced regarding the sustainability of its token economics provide a multi-faceted case study on this topic.

3.2.1 Ethereum's Token Economics: The Dependency of Layer 2 on Ethereum

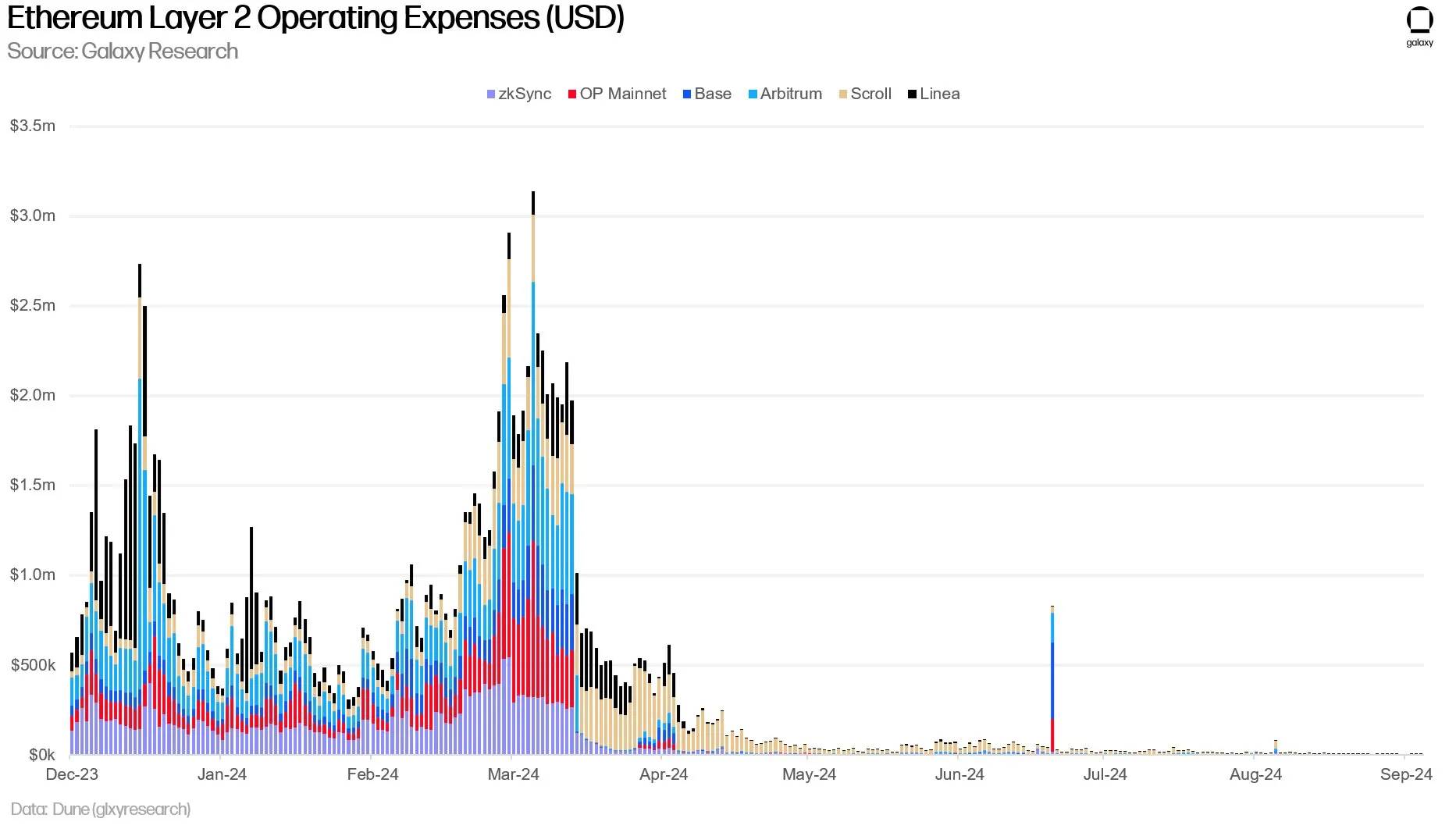

Source: X(@glxyresearch)

Ethereum has built the largest ecosystem in the blockchain network, relying on its strong liquidity and active developer community. However, recent concerns have arisen regarding Ethereum's economic model, primarily because the value of L2 is not reflected in the Ethereum main chain and $ETH. The root of the problem lies in the significant reduction of DA (data availability) fees paid by L2 when uploading transaction data to Ethereum after the EIP-4844 update. This has led to a decrease in demand for $ETH as a gas token. In other words, as the fees paid by L2 to Ethereum decrease, Ethereum's revenue diminishes, and a crucial demand factor for $ETH disappears, leading to the viewpoint that "L2 is economically parasitic on Ethereum."

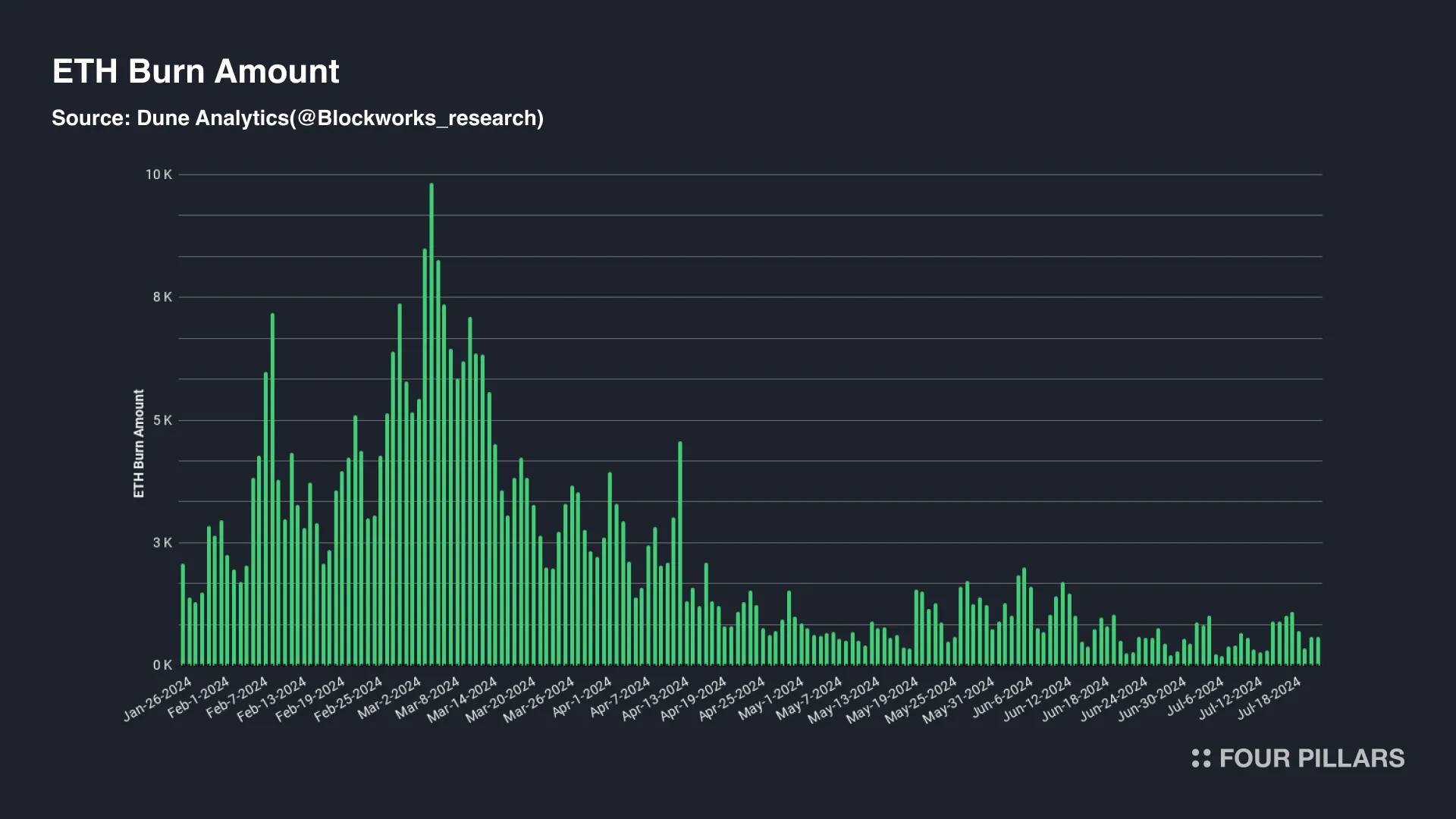

Source: Dune(@blockworks_research)

To gain a deeper understanding of the context, Ethereum divides gas fees into base fees determined by network congestion and priority fees set by users. The priority fees are paid as rewards to validators, while the base fees are burned. Therefore, when Ethereum's total base fees exceed the newly generated block rewards, a sufficient amount of $ETH is burned, keeping the total $ETH supply in a deflationary state. The circulating supply of $ETH in the market continues to decrease, which is seen as the foundation supporting the demand for $ETH as an asset.

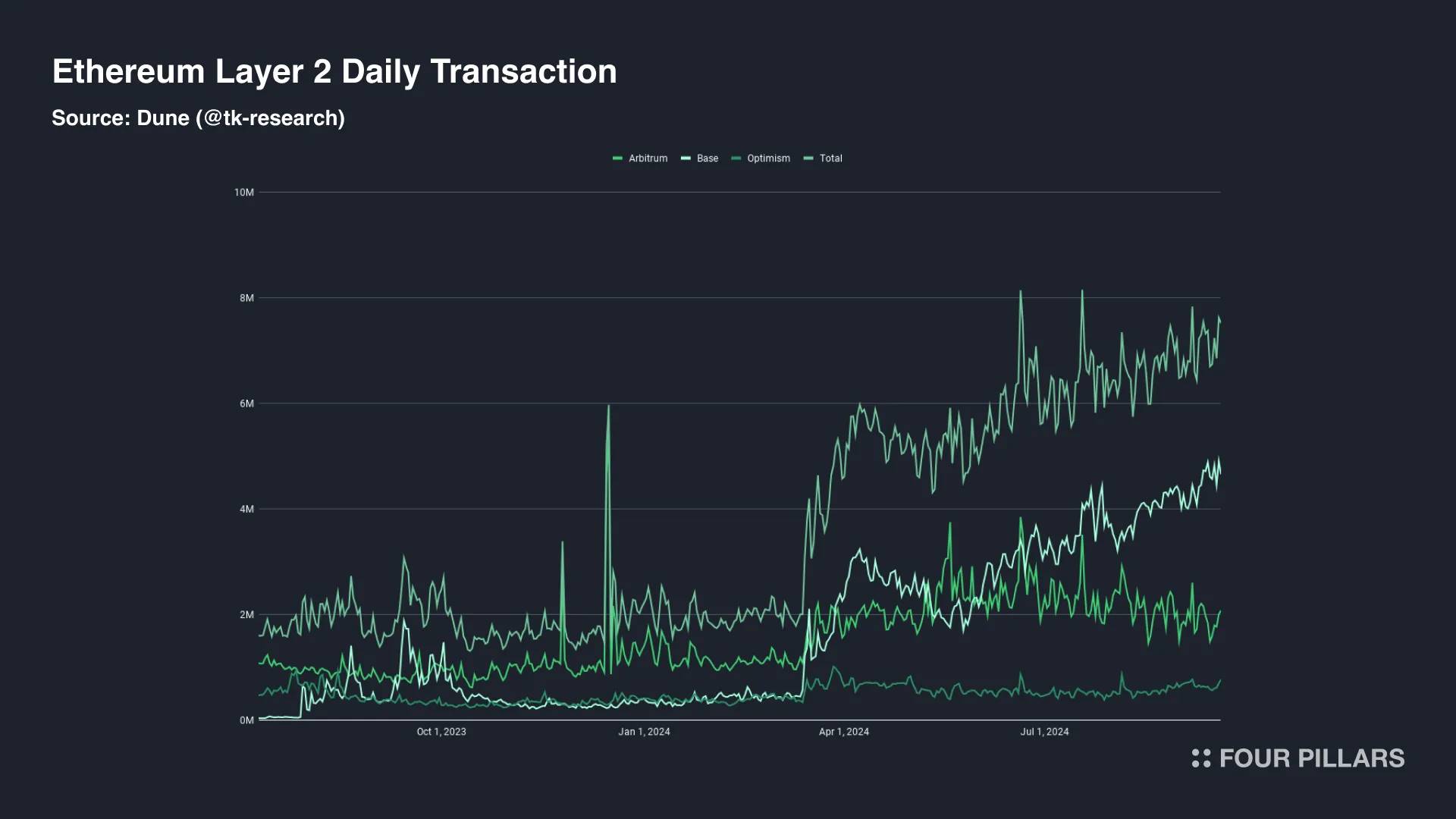

Source: Dune(@tk-research)

However, Ethereum's long-term goal is to develop a L2-centric roadmap, which prompted the EIP-4844 update to reduce sorting costs and enhance L2 scalability. Since this update, the situation has changed. The significantly increased L2 transactions and active addresses indicate that end users can now transact through L2 applications with lower network fees, no longer relying on Ethereum. On the other hand, structurally, Ethereum is at a "disadvantage" compared to L2. Despite L2 activity, Ethereum's average gas fees have dropped to 1 Gwei, leading to an inflationary state for $ETH supply. This has sparked criticism that L2 is economically parasitic on Ethereum.

3.2.2 The Importance of Alignment Between Architecture and Economic Model as Demonstrated by Ethereum

Ethereum continuously upgrades its architecture to compensate for the main chain's scalability shortcomings through L2. This raises the question: given the significant improvement in Ethereum's scalability and the increase in L2 activity, has it not successfully achieved its goals? Ethereum has announced a rollup-centric development roadmap aimed at achieving a highly scalable blockchain environment while maintaining sufficient decentralization. Therefore, since the EIP-4844 update, the reduction in L2 operational costs and the increased convenience for end users may align with Ethereum's architectural upgrade goals.

However, the case of Ethereum illustrates that problems arise when the technical architecture does not match the economic model, even during this transitional phase towards an L2-centric roadmap. Although L1 has made architectural improvements to achieve its goals, and user experience and activity have improved, the connection between the value generated by this activity and the economic model has broken. The scalability of L2 has not effectively translated into economic benefits for Ethereum. Proposals like EIP-7762 suggest increasing L2 blob fees, which may lead to a regression in L2 scalability, indicating a mismatch between Ethereum's architectural and economic growth curves.

This indicates that token economics cannot be considered separately from the architecture of L1. If an L1 has clear problems to solve and goals to achieve, its technical architecture should be constructed as a methodology to achieve these goals. Then, there should be a token economics design that matches this architecture. Such issues are more likely to arise in modular blockchains that may lead to economic fragmentation. Besides Ethereum, the Cosmos IBC ecosystem also generates different application chains based on its unique technical architecture, but it remains a decentralized ecosystem without forming a value chain that economically integrates these application chains into a unified economic system. In other words, as the architecture evolves, if the participants in the ecosystem have unique interests, an optimized economic model is also needed.

3.3 Pillar III - Value Capture: Arbitrum

Value capture refers to the mechanism by which tokens derive value from the network. Even if network activity is very active, a mechanism that can directly adjust the supply and demand of tokens is still needed to enhance the fundamental demand for tokens. The lack of a close connection between Arbitrum and $ARB has led to the inability of the token to effectively capture value, which fully illustrates the importance of the value capture mechanism.

3.3.1 Arbitrum's Token Economics: L2 Token as a Meme Token

Arbitrum is currently the most active among all L2 networks, with its ecosystem hosting about 700 protocols and processing approximately 5 million transactions weekly. However, despite the high level of network activity, $ARB has been criticized as being similar to a meme token due to its lack of utility beyond governance functions. Therefore, it lacks the fundamental demand factors recognized by the market. Although various variables in the market complexly influence token prices, making price fluctuations difficult to explain simply, the mechanisms that encourage market participants to be willing to purchase or hold tokens long-term play a significant role in their value assessment. In fact, the price of $ARB has been on a downward trend, decreasing by 66% since the beginning of the year, and according to IntoTheBlock, currently 95% of $ARB holders are in a state of loss.

To address this issue, Arbitrum DAO recently passed a proposal to introduce staking functionality for $ARB. The core of this proposal is to delegate governance rights through the staking of ARB tokens and strengthen the staking reward system. First, staking $ARB can yield returns from various income sources, such as sequencer fees, MEV fees, and validator fees. Additionally, by introducing liquid staking, $ARB holders can interoperate with other DeFi protocols while maintaining their staked status through $stARB.

This update to the token economics is expected to bring about multiple effects. The Arbitrum DAO treasury has already accumulated $45 million worth of $ETH, but the circulating $ARB used for governance accounts for less than 10%. Therefore, enhancing the motivation for governance delegation through $ARB staking is expected to improve governance security. Another important effect is to incentivize token holders to hold $ARB long-term.

3.3.2 Arbitrum Highlights the Importance of Value Capture Mechanisms

Value capture refers to the accumulation of network value through tokens, which can be achieved by distributing the revenue generated by the network to ecosystem contributors or by directly or indirectly adjusting the token supply. Value capture is crucial not only for L2 or DeFi protocols, as demonstrated by the case of Arbitrum, but also for L1 token economics. Especially for L1 native tokens that serve as incentive mechanisms, tokens must be viewed as rewards with appropriate value to incentivize ecosystem participants to contribute to the network.

The method of capturing value through tokens involves mechanisms that combine network demand with the supply and demand dynamics of tokens. For example, if network revenue is used to buy and burn tokens from the market, the supply of tokens in the market will decrease. Alternatively, network-generated revenue can be directly distributed to stakers. Such value capture mechanisms can create a virtuous cycle by generating fundamental demand factors for tokens or adjusting the number of tokens circulating in the market. This cycle can promote increased L1 activity, thereby enhancing the value of tokens, further incentivizing contributors, and driving further growth in L1 activity.

4. Sustainable Token Economics for Next-Generation Layer 1

By studying existing token economics cases, we have been able to identify three key points for creating a token flywheel. Although it will take a long time for Bitcoin's block rewards to completely disappear, this is not an urgent issue at present. Ethereum and Arbitrum are actively discussing how to address the current challenges, and there is still room for improvement in the future. However, the limitations encountered in existing token economics provide valuable lessons. When an ecosystem lacks incentives, the economic model does not match the technical architecture, or network activity fails to translate into token value growth, the sustainability of token economics may be threatened.

However, meeting these standards is not as straightforward as it seems. The common solution proposed by Berachain, Initia, and Injective is to intervene directly at the network level to adjust the interests of participants or to design token economics that are closely integrated with the technical architecture. Alternatively, they attempt to adjust the supply and demand relationship of tokens through unique mechanisms to overcome previous limitations. This strategy of deeply engaging with token economics at the network level has the potential to effectively fill the gap of the flywheel effect in existing token economics. Next, we will explore how Berachain addresses issues through its complex PoL mechanism design, how Initia plans to connect decentralized Rollup ecosystems through the VIP economic model, and why Injective can maintain the deflationary state of its tokens in the long term.

4.1 Mechanism Design: Berachain's Proof of Liquidity

Mechanism design involves creating a system that allows L1 participants to actively promote the operation and sustainability of L1 while pursuing maximum benefits. Berachain focuses on this area, proposing PoL (Proof of Liquidity) as a consensus algorithm that addresses the issue of misaligned interests by closely integrating the interests and reward systems of ecosystem participants.

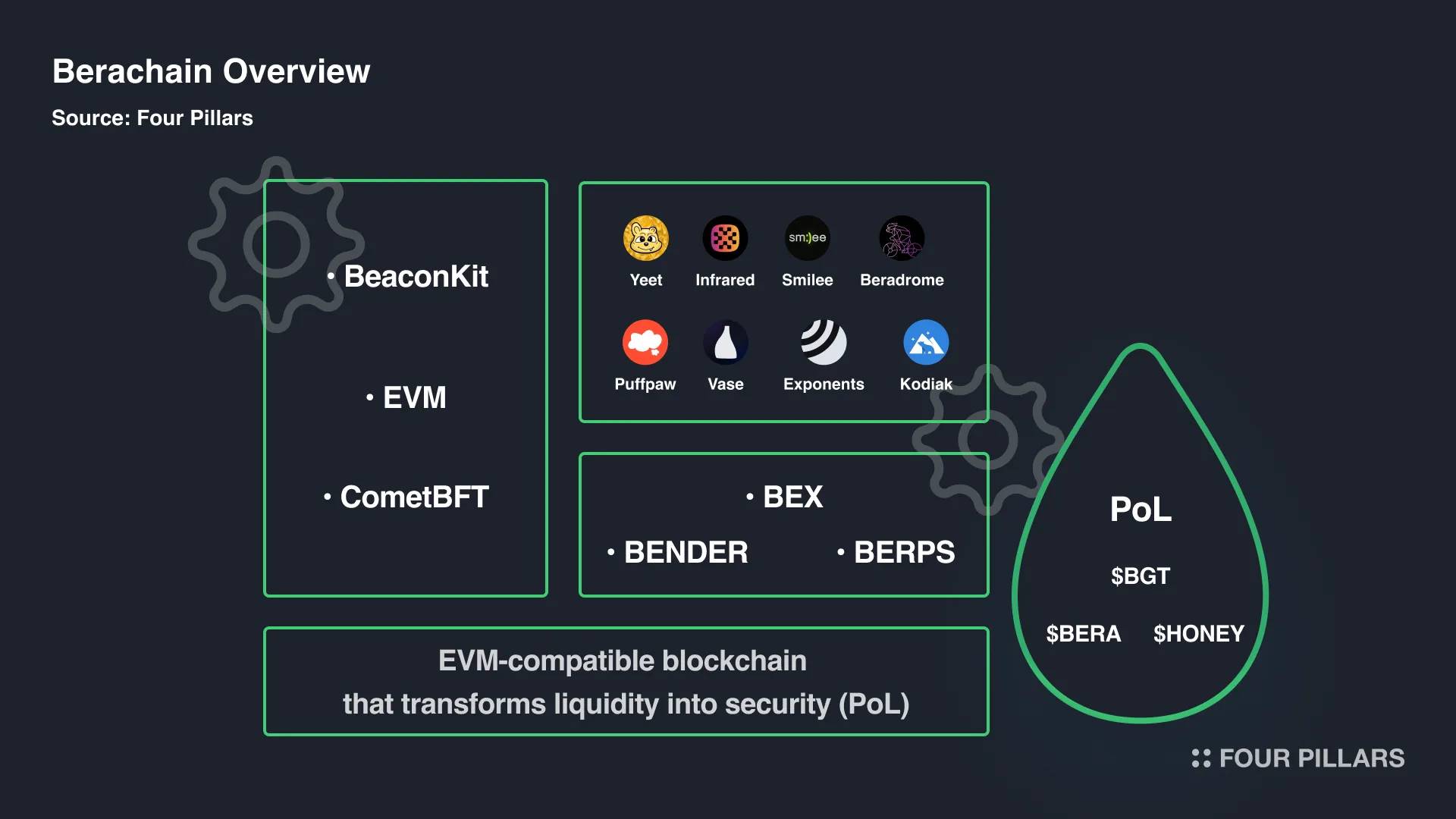

4.1.1 Overview of Berachain

Berachain is an EVM-compatible L1 blockchain built on BeaconKit, which is developed by modifying the Cosmos SDK. Similar to Ethereum's beacon chain structure, Berachain uses BeaconKit to separate the execution layer from the consensus layer, employing ComtBFT as the consensus layer and EVM as the execution layer to ensure high compatibility with the EVM execution environment. With its strong technical capabilities, Berachain has been building its community and development environment for a long time, starting with the NFT project Bong Bears. Therefore, although it is still in the testnet phase, multiple protocols have already launched, showing a high level of community engagement.

4.1.2 Berachain's Token Economics

What makes Berachain unique is its PoL mechanism, which adjusts the interests of participants at the network level. PoL is a specially designed consensus algorithm aimed at stably ensuring liquidity and security while enhancing the role of validators in the ecosystem. It focuses on mechanism design, allowing each ecosystem participant to promote network growth through interdependent relationships while pursuing their own interests. Next, we will explore how Berachain unifies the individual interests of users, validators, and protocols into a common growth point.

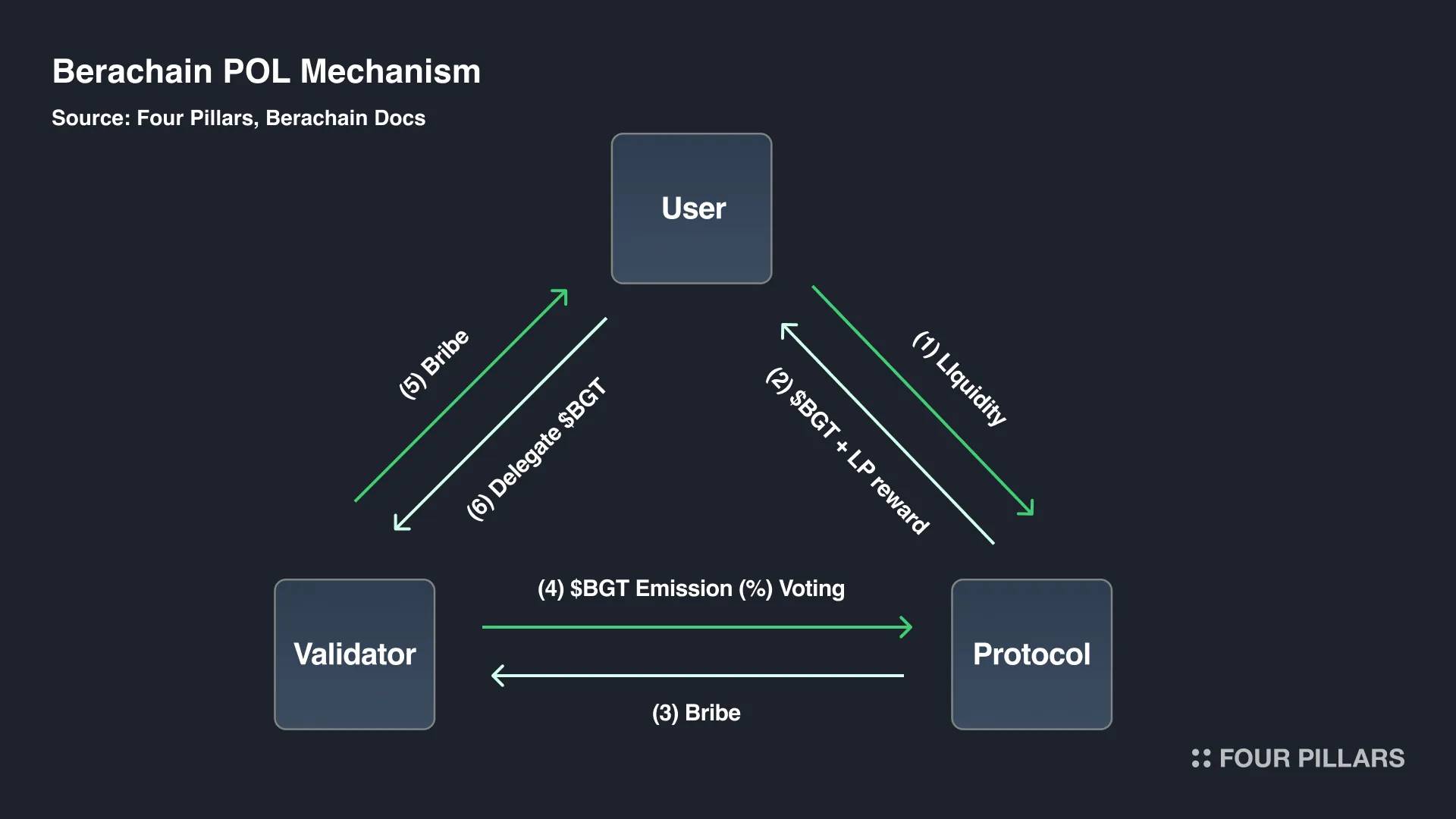

Source: Berachain Docs

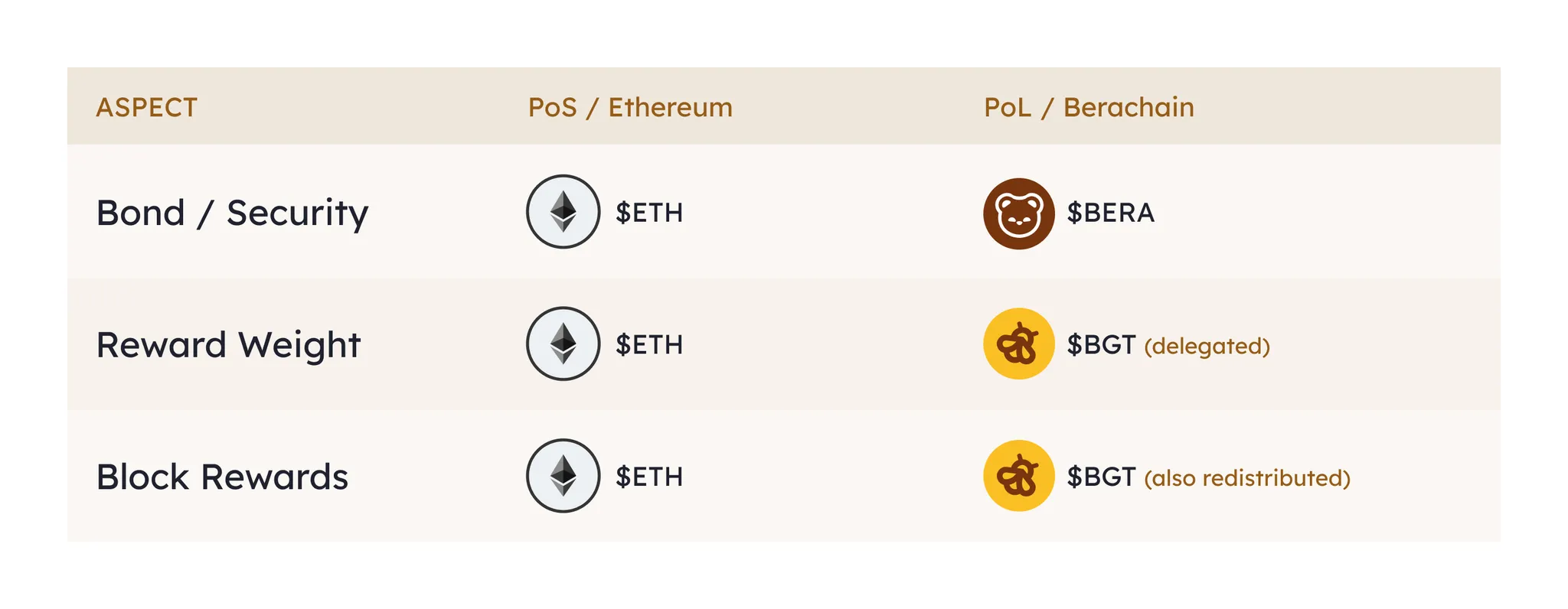

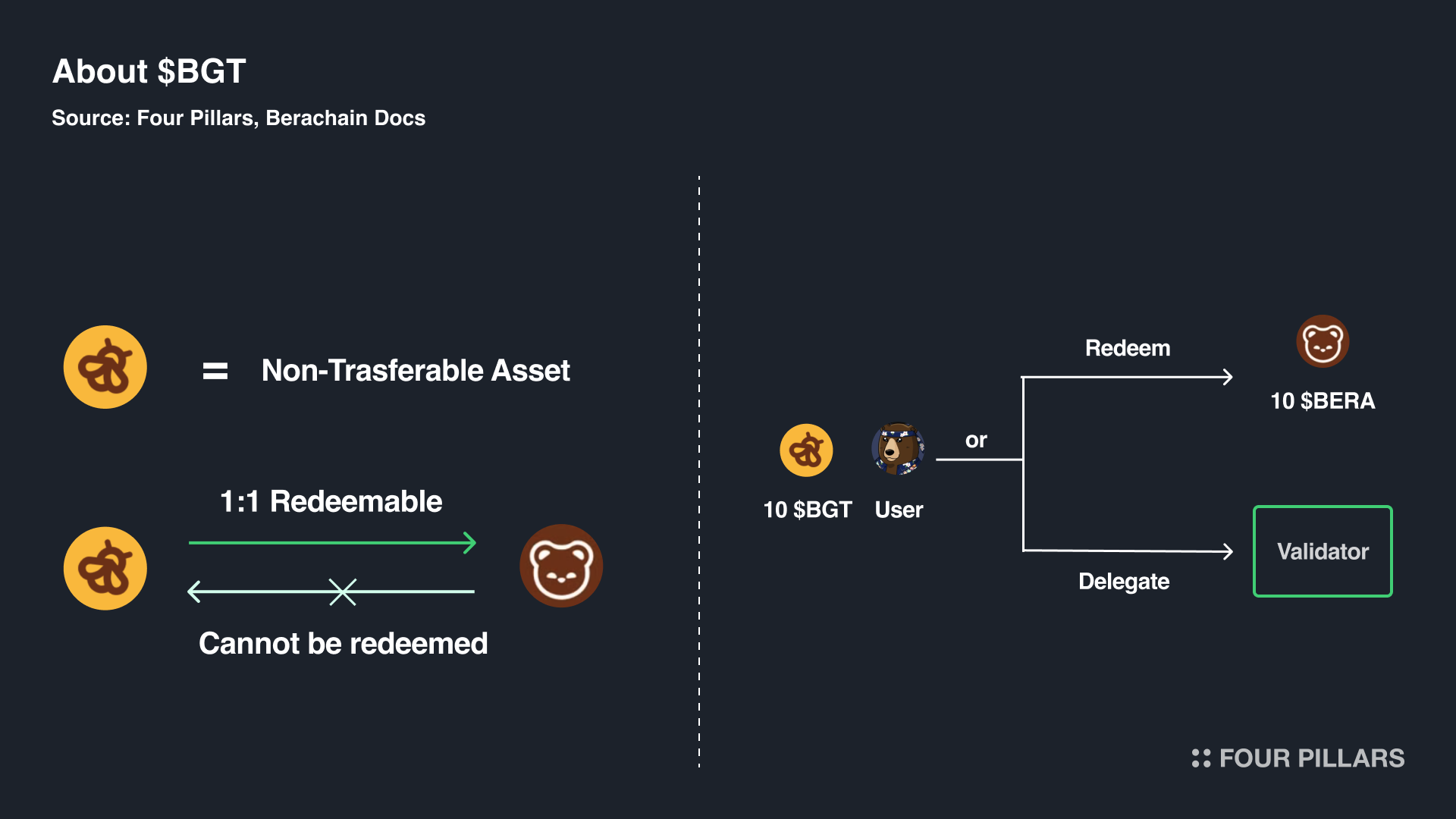

First, Berachain has three tokens: $BERA, $BGT, and $HONEY, each serving different roles in the operation of PoL. $BERA is used as the gas token for paying network fees, $BGT (Bera governance token) serves both as a reward token for providing liquidity and as a governance token that determines the reward ratio. $HONEY is Berachain's native stablecoin, pegged to $USDC at a 1:1 ratio. While Berachain adopts a triple-token economic model, to simplify the discussion of the PoL participation structure, we will focus on $BERA and $BGT. Understanding Berachain's mechanism design requires special attention to the unique functions of $BGT.

BGT is a reward token that users can earn by providing liquidity to whitelisted liquidity pools (whitelist reward treasury), as determined by governance. BGT is provided in a non-tradable form in accounts, and while $BGT earned as a reward can be exchanged for $BERA at a 1:1 ratio, the reverse exchange ($BERA → $BGT) is not possible. Therefore, providing liquidity is the only way to obtain $BGT.

BGT is allocated to specific liquidity pools. Users who obtain $BGT have two options: they can either exchange $BGT for $BERA to realize value or delegate it to validators for additional rewards. These additional rewards refer to the incentives flowing from the protocol to users through validators, which we will elaborate on later.

The reason Berachain separates the gas token and governance token into $BERA and $BGT is to ensure both liquidity and security within the ecosystem. In L1 networks using a single token, staking tokens to enhance PoS security limits the number of tokens available for liquidity in the ecosystem. Therefore, Berachain aims to resolve the inconsistency between network liquidity and security by requiring users to provide liquidity to obtain $BGT for security. Additionally, by allowing validators to allocate the issuance ratio of $BGT, it enhances the alignment of interests among ecosystem participants, increasing the interdependence between validators, protocols, and users.

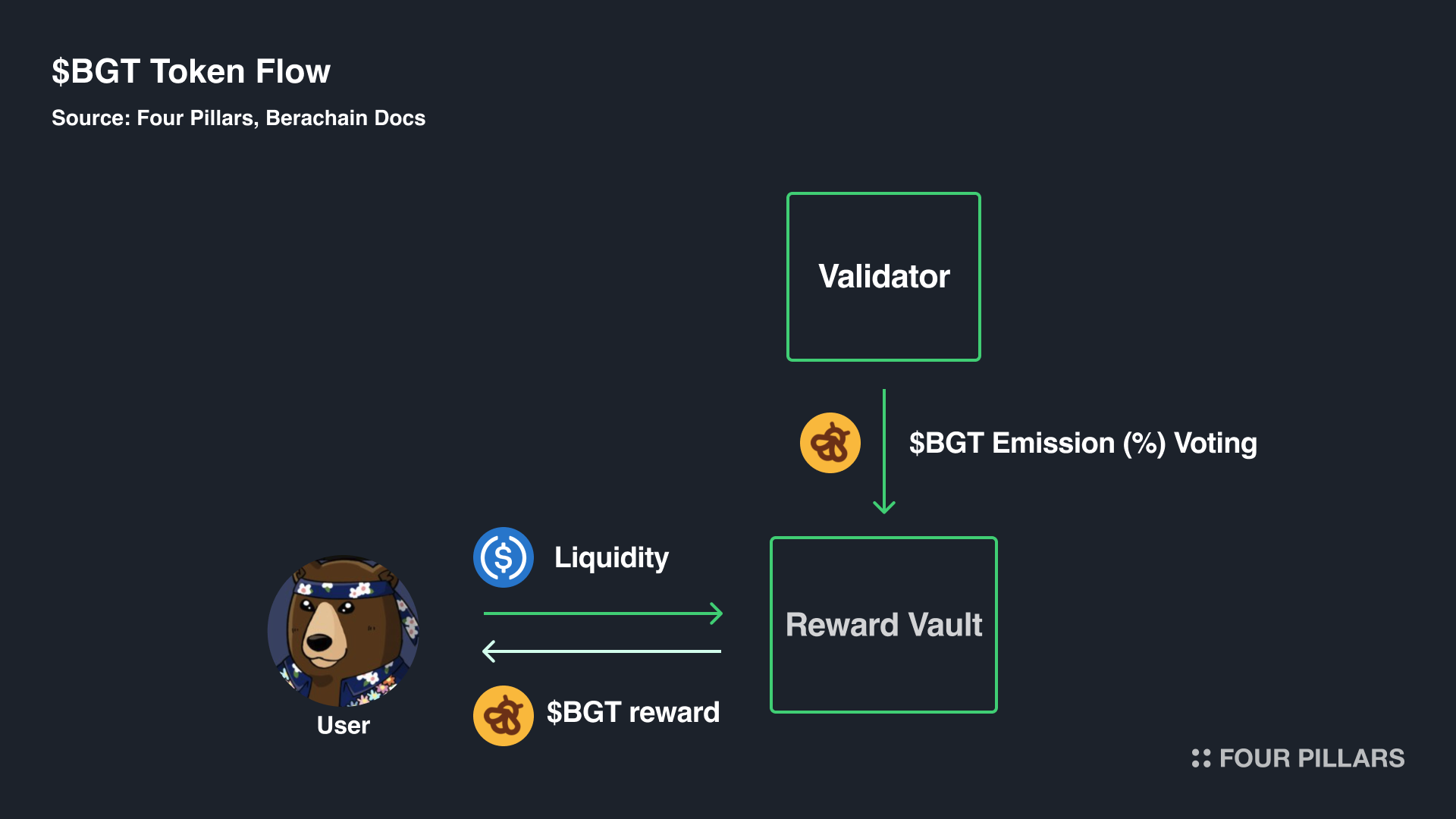

Now that we understand the basic principles of PoL and the roles of $BERA and $BGT, let’s look at how ecosystem participants interact under this mechanism design. Following the flow from (1) to (6), we will track the movement of $BGT, liquidity, and incentives to understand how ecosystem participants interact under specific interests.

User ↔ Protocol

(1) Liquidity: Users deposit funds into their chosen whitelisted liquidity pools. The protocol utilizes these liquidity pools to provide users with a smooth trading environment.

(2) $BGT + LP Rewards: When users provide liquidity to the whitelisted pool, the protocol rewards them with $BGT and liquidity provision rewards. In this process, the protocol needs to strive for a higher issuance ratio of $BGT to attract users to choose their liquidity pools.

Protocol ↔ Validators

(3) Incentives: Validators have governance rights to determine the issuance ratio of $BGT for liquidity pools. Therefore, the protocol provides incentives to validators to encourage them to vote for their liquidity pools.

(4) $BGT Issuance Voting: Unlike other L1s, Berachain's validators do not receive L1 tokens as network validation rewards directly based on inflation rates. Instead, they earn network validation rewards through incentives provided by the protocol (excluding any priority fees that may occur irregularly). Therefore, to obtain sufficient incentives from the protocol, they need to strive for more $BGT to enhance their governance power.

Validators ↔ Users

(5) Incentives: Validators need users to delegate the $BGT obtained through liquidity provision to them to gain stronger governance power. To achieve this, they need to return the incentives obtained from the protocol to users or provide additional rewards to increase the amount of delegated $BGT.

(6) Delegating $BGT: Users delegate $BGT to validators in exchange for the incentives they provide.

4.1.3 Token Economics Direction of Berachain's Mechanism Design

In summary, Berachain, through the PoL mechanism, aims to ensure both liquidity and security within the ecosystem while addressing the issue of misaligned interests among validators. Unlike traditional single-token models, Berachain uses $BERA for liquidity and $BGT for governance, resolving the trade-off between liquidity and security. By allowing validators to earn rewards through incentives and granting them the power to determine the issuance of $BGT, it strengthens the interdependence among validators, protocols, and users.

Of course, as the complexity of the mechanism increases, the learning curve for users will also become steeper. Therefore, it is essential to closely monitor whether the interactions around PoL can proceed smoothly after the mainnet launch. However, Berachain's token economics demonstrates complexity in mechanism design, providing an important direction for L1 token economics by addressing the issue of inconsistent incentives among participants.

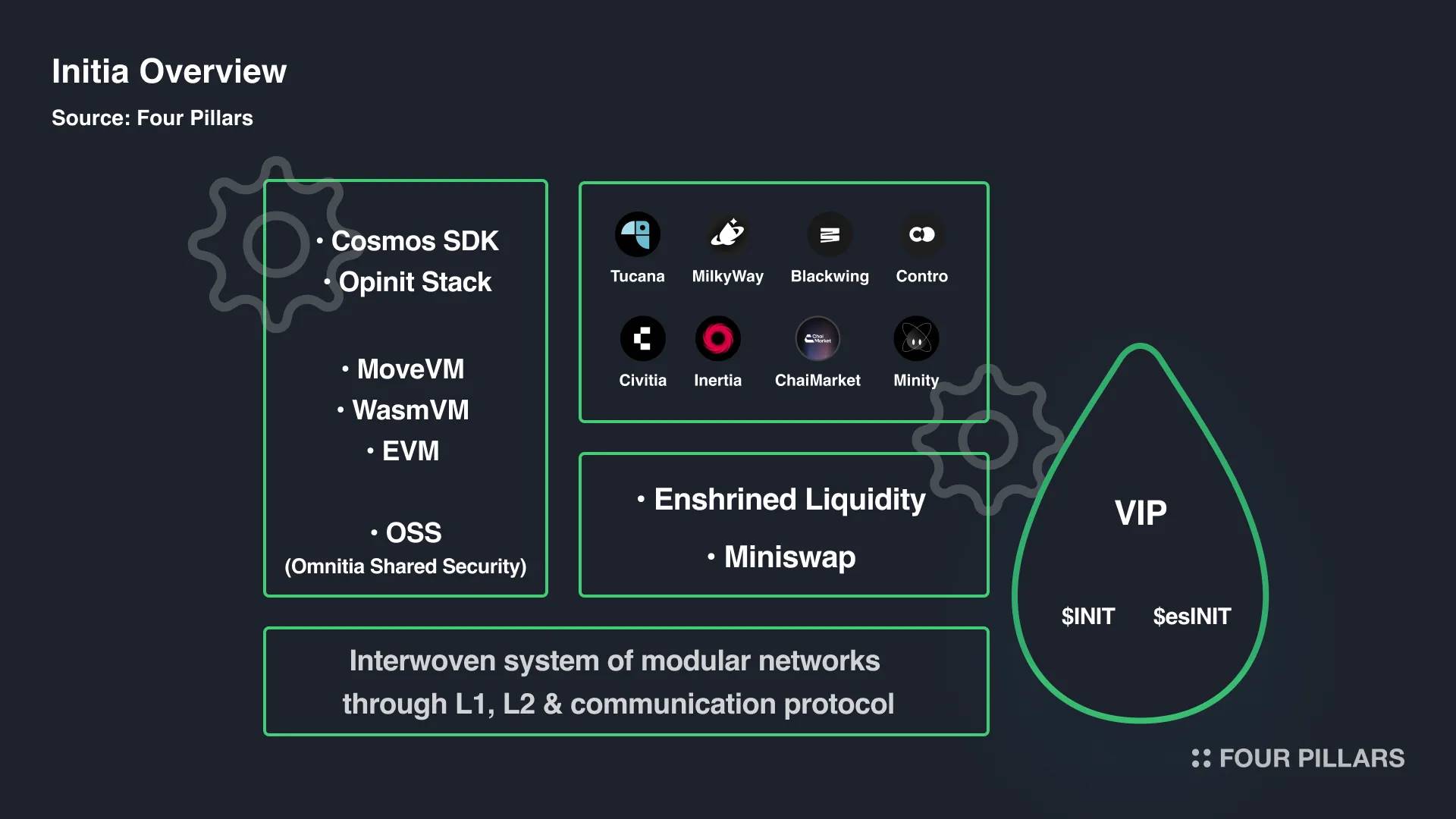

4.2 Consistency with Architecture: INITIA and VIP

Initia aims to address the potential inconsistencies that may arise between architecture and economic models when the architecture aligns with the network direction. It focuses on the fragmentation challenges within the existing Rollup ecosystem. Upholding the mission of "interwoven Rollups," Initia is dedicated to building an ecosystem where L2 Minitia is distributed around Initia and closely connected on both economic and security levels. To achieve this goal, Initia attempts to connect the potentially fragmented Rollup ecosystem economy through its unique VIP token economics.

4.2.1 Overview of Initia

Initia is a Layer 1 blockchain based on Cosmos, supported by MoveVM, designed to serve as the settlement layer for a Layer 2 Rollup called Minitia. Initia (L1) and Minitia (L2) are interconnected in terms of economy and security, forming an integrated ecosystem known as Omnitia. Therefore, various functions of Initia are aimed at strengthening the connection with Minitia L2. For example, in terms of security, if fraud occurs in Minitia, Initia's validating nodes will intervene alongside Celestia to resolve disputes and reconstruct the final valid state. In terms of liquidity, it operates a liquidity center called Enshrined Liquidity at the L1 network level, which Minitia can utilize for routing functions, supporting users in seamless asset movement and exchange between Minitia.

4.2.2 Initia Token Economics

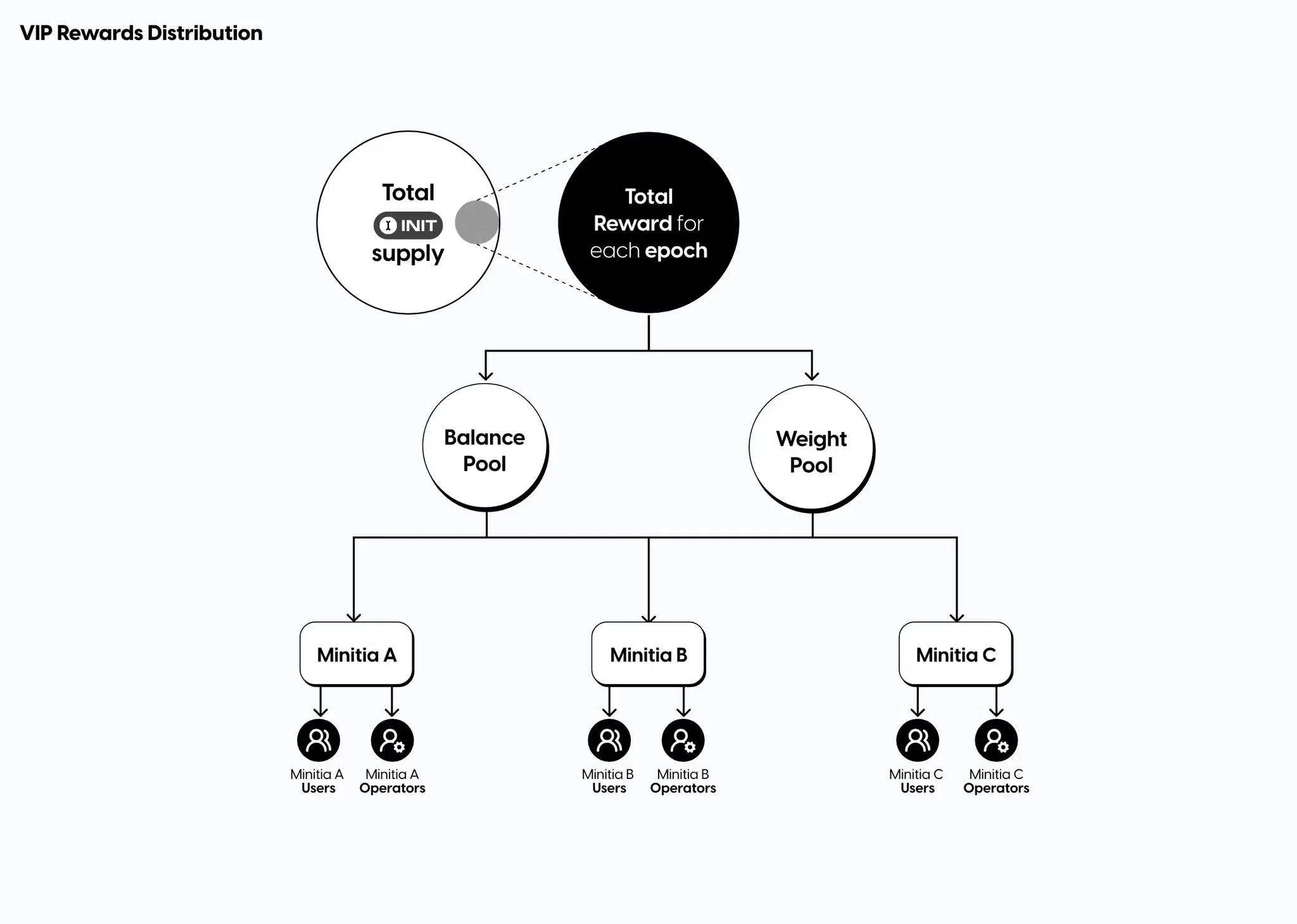

Initia's design focuses on a close connection with Minitia L2, for which it has launched the VIP (Vested Interest Program) mechanism to establish economic ties. The goal of VIP is to make $INIT the foundational currency of the Initia ecosystem and a key component of all L2s. Through this mechanism, $INIT serves as the economic link connecting Initia and Minitia, continuously expanding the use cases of $INIT. The VIP process can be divided into three main steps: 1) Allocation, 2) Distribution, 3) Unlocking.

1) Allocation

Source: Introducing VIP

First, 10% of the initial supply of $INIT is designated as VIP funds. These funds are allocated to eligible Minitia and users every two weeks. VIP rewards are distributed through two pools: the Balance Pool and the Weight Pool. Rewards from the Balance Pool are allocated proportionally based on the amount of $INIT held by Minitia. In contrast, rewards from the Weight Pool are distributed to Minitia based on the weights set through metric voting in L1 governance. In other words, L1 stakers determine the reward share each Minitia should receive through metric voting. Thus, the Balance Pool encourages Minitia to hold more $INIT and expand the use cases of $INIT in their applications, while the Weight Pool creates new use cases for the $INIT token through metric voting and incentivizes validators, users, or bribery protocols like Votium and Hidden Hand to actively participate in L1 governance.

2) Distribution

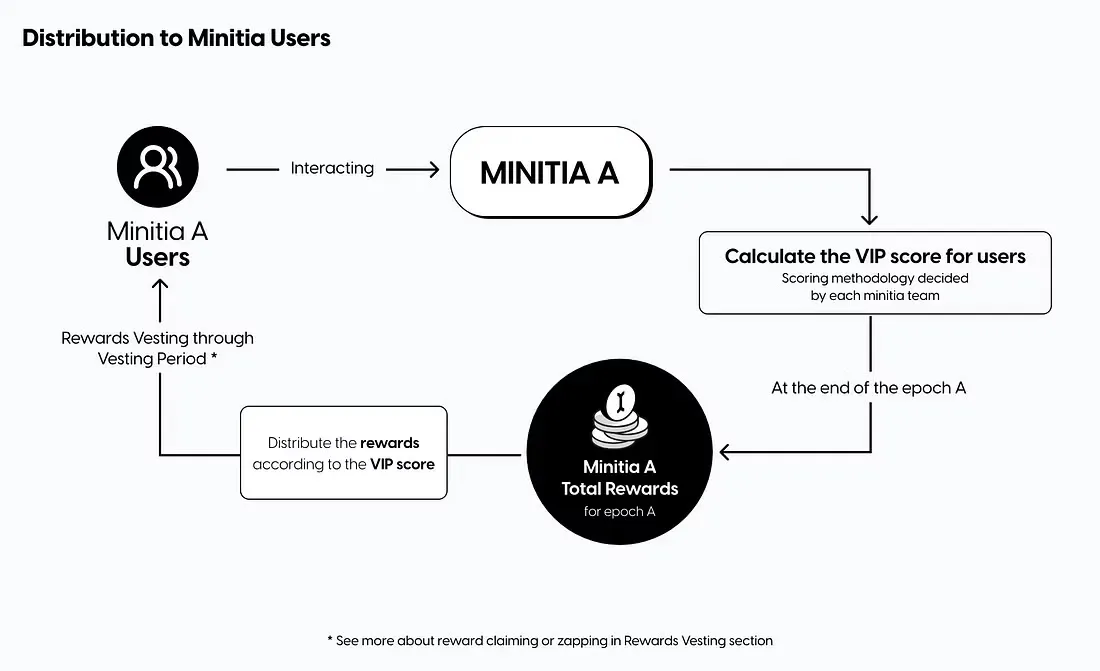

Source: Introducing VIP

Rewards allocated to Minitia are issued in the form of $esINIT (escrowed INIT), which is initially non-transferable. Recipients of $esINIT are divided into operators and users. Operators refer to the project teams responsible for operating Minitia. These teams can utilize $esINIT in various ways, such as using it as development funds to support Minitia's growth, redistributing it to active users in Minitia, or staking it on Initia L1 to vote for themselves in future metric voting.

On the other hand, $esINIT issued as user rewards is provided directly based on the user's VIP score. The VIP score is calculated based on various key performance indicators (KPIs) set by Minitia, aimed at encouraging user interaction on Minitia. For example, Minitia can set VIP score criteria, such as the number of transactions generated by users through Minitia within a specific period, transaction volume, or lending scale, to incentivize users to perform specific actions.

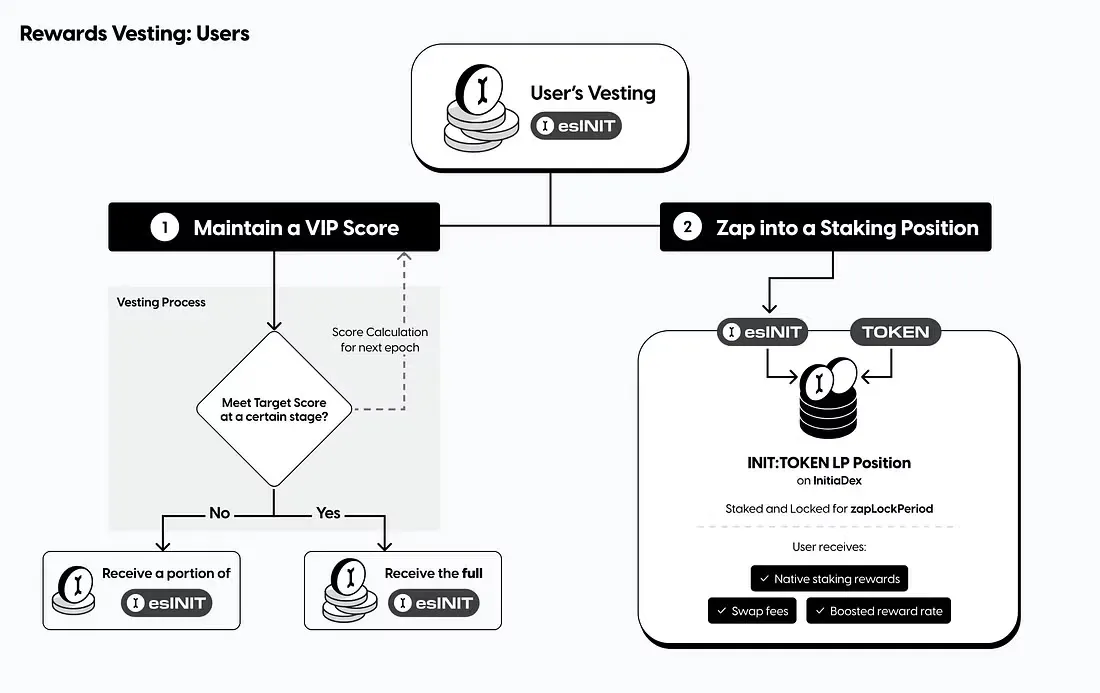

3) Unlocking

Source: Introducing VIP

As mentioned earlier, when rewards are issued to users based on VIP scores, $esINIT is issued as a non-transferable escrowed token. Therefore, users need to go through an unlocking process to realize the $esINIT they have obtained. In this process, users can choose two ways to maximize their benefits. The first is to maintain their VIP score over multiple cycles, thereby unlocking $esINIT as transferable $INIT. During the period of maintaining the VIP score, users can accumulate more points in Minitia, which helps improve user retention for Minitia. The second way is to deposit $esINIT as liquidity into Enshrined Liquidity to earn deposit rewards.

4.2.3 Token Economics Direction Proposed by Initia's VIP

In summary, VIP is Initia's token economics strategy aimed at economically connecting L1 and L2 and creating sustained demand for $INIT. In the 1) Allocation phase, it increases the use cases of $INIT and encourages governance participation through mechanisms such as the Balance Pool and Weight Pool with different allocation methods to activate the ecosystem. In the 2) Distribution phase, it aligns the interests of Minitia and users by allowing Minitia to utilize VIP scores to guide specific user behaviors. Finally, in the 3) Unlocking phase, it promotes user retention or direct contributions to the Initia ecosystem through liquidity provision.

Through this process, Initia aims to prevent economic fragmentation within the Minitia ecosystem while creating multiple use cases for $INIT, thereby stimulating the fundamental demand for the token. With the rise of modular blockchain infrastructure, economic fragmentation of ecosystems is seen as a long-term issue that requires balancing the advantages of modular development environments with the challenges they bring. In this regard, the VIP proposed by Initia provides a meaningful direction for token economics design in future modular ecosystems.

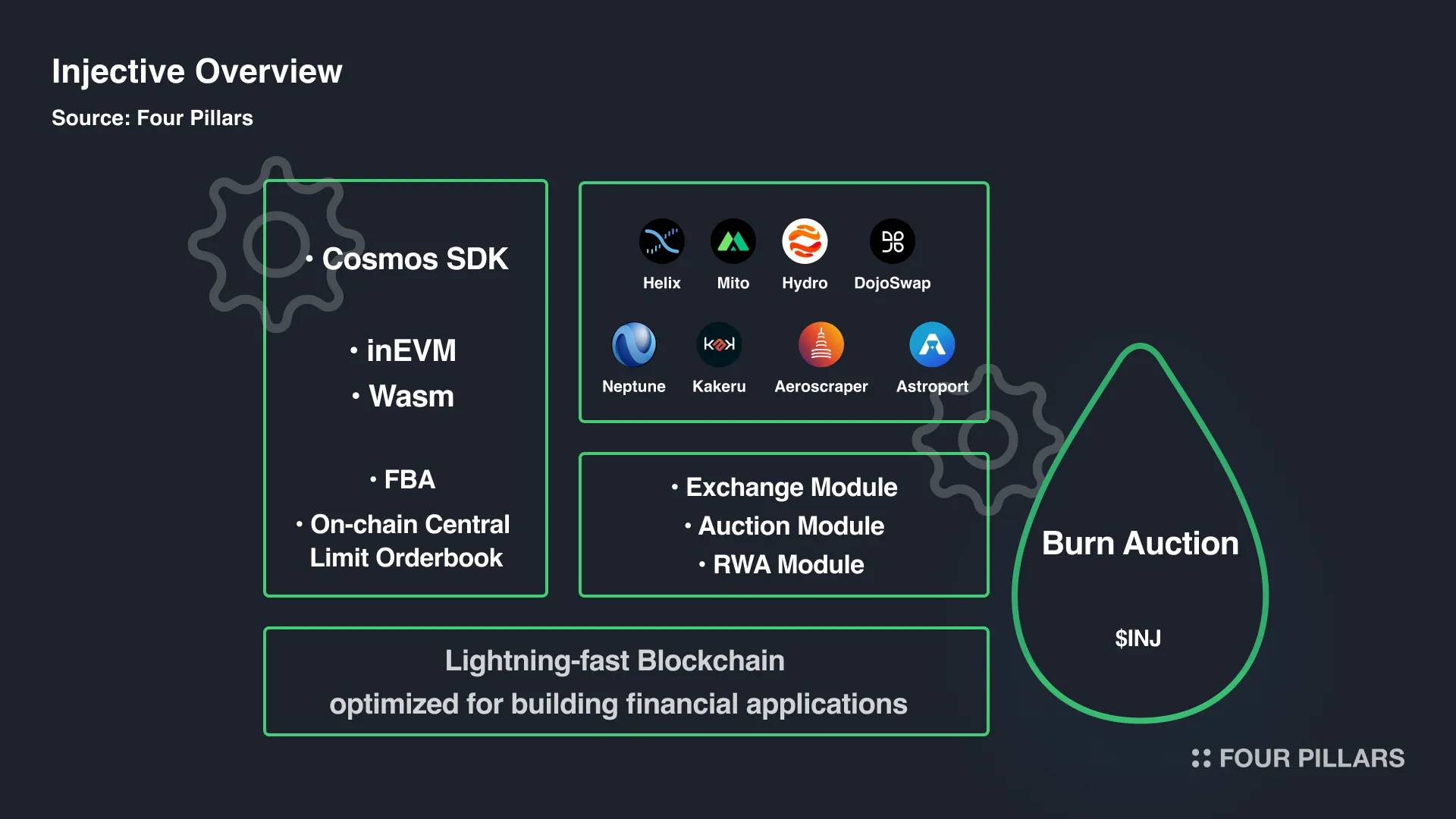

4.3 Value Capture: Injective and Destruction Auctions

Unlike Berachain and Initia, which have yet to launch their mainnets, Injective has been making its mark in the market since 2018. However, it continuously refines its token economics through updates like INJ 3.0 and Altaris, establishing a unique deflationary token economics system based on its destruction mechanism. Therefore, when discussing value capture in L1 token economics, I believe Injective is a case worth paying attention to, and thus I will introduce it here.

4.3.1 Overview of Injective

Injective is an L1 blockchain built on the Cosmos SDK and a custom consensus mechanism based on TendermintBFT, optimized for financial applications ranging from spot trading to perpetual futures trading and RWA. As a finance-focused L1 blockchain, it provides a high-performance environment with over 25,000 TPS to support high-frequency trading and employs on-chain order matching models like FBA (Frequent Batch Auctions) to prevent MEV in capital-efficient trading. Additionally, Injective offers plug-and-play modules as part of its development resources. In particular, by using the trading module, users can easily handle order book operations, trade execution, and order matching processes, leveraging Injective's built-in shared liquidity to create a financial service environment that does not require additional liquidity attraction.

4.3.2 Injective Token Economics

Source: X(@Injective)

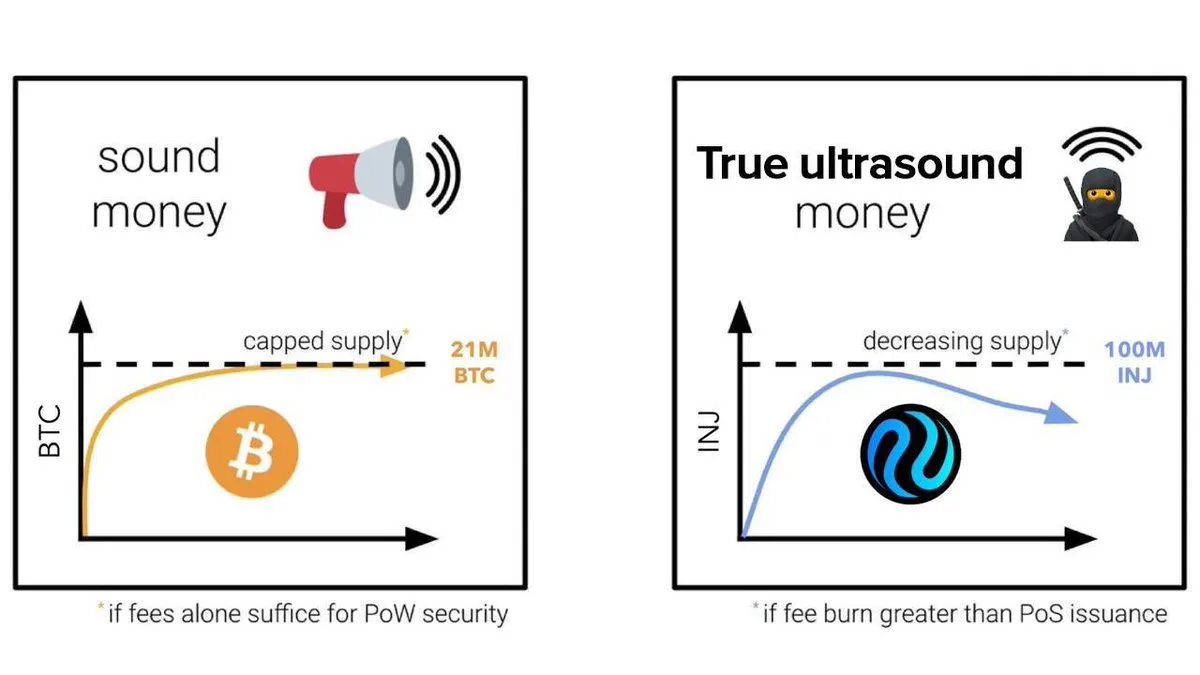

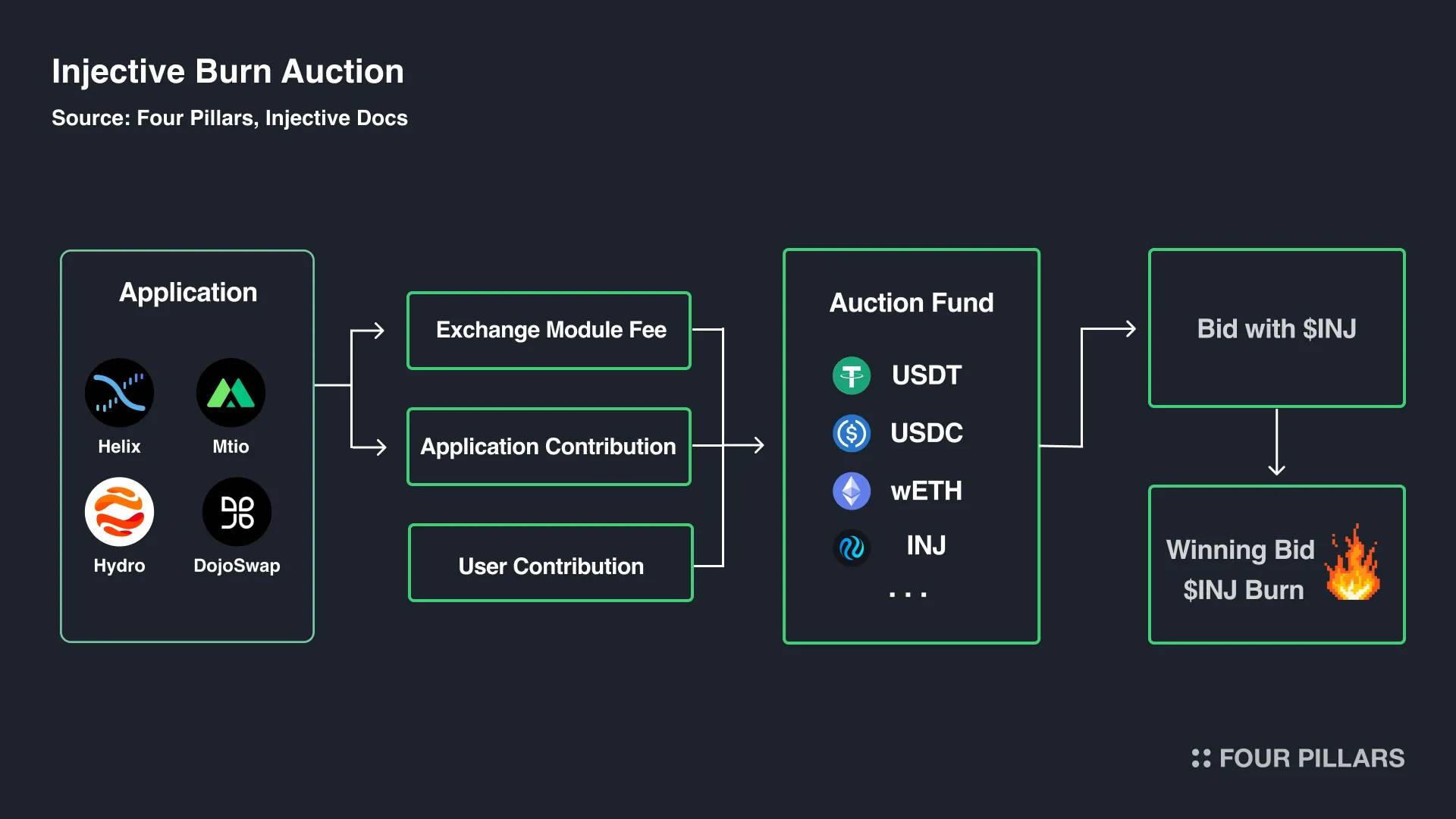

Injective is known for its economic model that achieves token deflation through destruction auctions, a mechanism designed to reduce the circulating supply of $INJ in the market. The process of destruction auctions is as follows: when assets accumulate in the auction fund through a portion of the revenue from the Injective application or direct contributions from individual users, these assets are auctioned off, and bidders can bid using $INJ. At the end of the auction, the successful bidder exchanges their $INJ used for bidding for tokens from the auction fund, while the $INJ used for bidding is destroyed, thereby reducing the total token supply. Injective conducts such auctions weekly, and as of October 2024, has destroyed 6,231,217 $INJ through auctions, amounting to approximately $142 million.

The destruction auction program is conducted through the auction module, which is responsible for handling bids, determining winners, and the destruction of $INJ, and it works in conjunction with the trading module. First, the assets in the auction fund are collected through three avenues. The first avenue is to transfer a portion of the revenue into the auction fund using the trading module's application. The second avenue allows applications that do not use the trading module to transfer a certain amount or percentage of fees into the auction fund. Finally, individual users can also contribute funds directly to the auction fund.

The assets in the auction fund are primarily accumulated in the form of USDT, USDC, or $INJ, and anyone can participate in the auction using $INJ. Participants have the opportunity to acquire assets from the fund at slightly discounted prices, for example, winning assets worth $100 with $INJ valued at $95, which naturally sparks bidding competition. Ultimately, the successful bidder exchanges their bidding $INJ for tokens from the auction fund, while the $INJ used for bidding is destroyed.

4.3.3 Token Economics Direction Proposed by Injective's Destruction Auctions

Injective's destruction auctions create a mechanism for bidding that increases the amount of $INJ destroyed as the trading volume of the trading module increases through accumulated fees. Therefore, as trading activity on Injective increases, the circulating supply of tokens in the market decreases, allowing the tokens to capture value from the network. Thus, Injective closely ties the growth of its ecosystem to the enhancement of token economic value through its destruction mechanism and plans to continue strengthening its growth-driven token destruction mechanism in the future.

While most blockchains have mechanisms to destroy a certain percentage of network fees, few L1 networks can adjust token supply as intuitively as Injective. In particular, since most blockchains, aside from Bitcoin and Ethereum (mainnet), are developed under the premise of low gas fees, the token destruction mechanism based on network fees shows limitations when it comes to large-scale destruction. Injective is also committed to achieving near-zero transaction fees, with an average transaction fee recorded at $0.0003 per transaction. In this context, the destruction auction, which can achieve large-scale destruction while maintaining low gas fees, aligns with the user environment that future L1 networks seek, making Injective a noteworthy use case in this regard.

5. Looking Ahead: Why We Should Focus on the Token Economics of Next-Generation Layer 1

5.1 Shifting Perspectives: What is the Ideal Layer 1?

So far, we have analyzed the limitations of existing token economics and some improved cases, identifying potential development directions for next-generation token economics. Notably, Berachain, Initia, and Injective exhibit a common trend: they enhance token economics by implementing unique mechanisms at the network level. Each project leverages its advantages in mechanism design, architectural alignment, and value capture to build unique token economics.

So, what constitutes ideal L1 token economics? Is there an absolute token economics framework that can drive the token flywheel? To answer this question, we view token economics as an integrated system that involves not only the tokens themselves but also the mission that L1 aims to solve, the technical architecture, and the behavioral patterns of ecosystem participants. Through this process, the key insight we gain is that token economics itself is merely a concept. Its value is reflected in the actual interactions between various elements of the L1 network and its participants.

Therefore, we need to shift our perspective from "What is ideal token economics?" to "What constitutes an ideal L1, and what role does token economics play in it?" From this perspective, I believe a highly potential L1 is an ecosystem where its mission, architecture, protocols, and token economics can organically combine and generate synergies.

A clear mission

A technical architecture designed to faithfully achieve that mission

An ecosystem filled with protocols and applications that are optimized for the network's development environment or architecture, which can be described as "only possible on this particular chain"

Thus, able to provide differentiated value to users

In this list, token economics is not listed separately; rather, it acts as a lubricant that facilitates the smoother operation of architecture and protocols. Analyzing the L1 networks we discussed today through this framework leads to the following conclusions:

5.2 Overview of Berachain, Initia, and Injective

Berachain has designed a unique consensus algorithm called PoL to create an EVM-compatible L1 network that converts liquidity into security and has developed an EVM-compatible framework called Polaris. Based on this, several projects have emerged, such as Infrared, which liquidates non-tradable assets $BGT; Smilee Finance reduces the risks that PoL needs to focus on liquidity provision by hedging impermanent loss; and Yeet Bonds allows protocols to autonomously acquire liquidity through bond products (i.e., protocols own liquidity), thereby minimizing the resources required for liquidity initiation (such as liquidity mining and bribery) and enabling autonomous voting to ensure the issuance of $BGT. When these components are combined with Berachain's PoL goals and means, as well as the triple token economics of $BERA, $BGT, and $HONEY, we can expect the formation of a unique ecosystem where validators, protocols, and users can develop and grow together.

Initia is an L1 network designed for "interwoven Rollups," aimed at addressing fragmentation issues in modular blockchains. To this end, it has built various architectures to enhance the connection between Initia and Minitia, including the Opinit Stack (a framework for building Rollups based on Initia), Enshrined Liquidity to ensure Minitia's liquidity, and the OSS (Omnitia Shared Security) framework for Minitia's fraud proofs. Based on Initia's architecture, Minitia, which focuses on modular infrastructure, is continuously emerging, including Tucana, an intent-driven DEX that integrates modular network liquidity, and Milkyway, which aims to provide restaking services based on Initia. Here, the VIP token economics is expected to create a virtuous economic cycle, where Minitia accumulates value created in Initia, while Initia enhances Minitia's activity.

Injective has a technology architecture optimized for financial applications, perfectly embodying its goal of being "a blockchain built for finance." It is based on a high-performance blockchain environment capable of handling high-frequency trading and supports a plug-and-play modular design. These modules can be used to develop financial applications, including the Exchange Module that provides a shared order book and shared liquidity, as well as modules for auctions, oracles, insurance, and RWA. Many financial applications and products have been developed on Injective, leveraging these diverse modules. The on-chain order book exchange Helix uses the Exchange Module to provide a trading environment comparable to centralized exchanges (CEX), while the case of launching a tokenized index for Blackrock's BUIDL fund through Injective's built-in RWA oracle perfectly demonstrates the idea of "only possible on Injective." In this context, Injective's token economics combines the growth of the ecosystem with the enhancement of token value through the burning auction mechanism, driving the emergence of more innovative applications.

From the above analysis, it is evident that these projects have the conditions to achieve synergistic development in the components of L1 networks and token economics. Of course, since Berachain and Initia have not yet officially launched, we need to closely monitor the potential interactions that may occur within the ecosystem from a long-term perspective. In particular, these two chains are designing quite complex token economics, which requires careful evaluation from multiple angles to effectively reduce the learning difficulties users may face and ensure that the token economics can perform as expected in practical applications.

At the same time, Injective's token economics particularly relies on the activation of the application ecosystem, which is its most critical prerequisite. Currently, Injective averages 2-3 million daily transactions, with a cumulative trading volume of $39.2 billion, demonstrating its high activity level and maintaining a stable $INJ burn rate. Looking ahead, actively promoting the active use of financial products and applications, especially those that leverage the unique characteristics of the financial professional chain, such as the BUIDL index or the 2024ELECTION perpetual market, will continue to play an important role in maintaining Injective's unique deflationary model in its token economics.

5.3 Fundamentals Matter: The Importance of Token Economics

Is the crypto industry still just a "narrative game" lacking substantive content? Recent market trends suggest otherwise. With the RWA market size reaching $12 billion driven by large institutions like BlackRock and Franklin Templeton, the participation of traditional financial institutions is accelerating, and market participants are beginning to focus not only on short-term market narratives but also on the actual profitability and revenue distribution mechanisms of protocols like Uniswap and Aave. In this context, the importance of fundamentals in the crypto industry is becoming increasingly prominent.

As fundamentals become more important, token economics clearly becomes a core criterion for assessing the fundamentals of L1 networks. Based on our discussion in this article, token economics can be evaluated by examining whether network activity effectively drives token demand, whether ecosystem participants actively interact around the token, and whether these interactions promote the growth of the network. Furthermore, token economics should not only exist as a concept but also play a practical role in the synergistic interactions with various components of the network, which will become an important framework for judging the fundamental value of L1 networks in the future.

In this context, the reason we focus on Berachain, Initia, and Injective today is that they attempt to break through the limitations of existing models by directly engaging in token economics at the network level. Injective maintains a unique token economics that enhances token value through its deflationary mechanism, while Berachain's PoL and Initia's VIP provide a new blueprint for L1 token economics in innovative ways. In a situation where many past L1 projects remain stagnant and become "zombie chains," I believe that the simple conceptual token flywheels have had little effect. Instead, whether these new approaches can truly establish sustainable ecosystems and achieve the ultimate goal of token flywheels will be an important observation point determining the future development of L1 token economics.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。