Two Core Elements of the Angel Round: Signals and Insights.

Author: Ishita Srivastava

Translation: Deep Tide TechFlow

Fundraising is not easy—whether you are a first-time founder or an experienced builder, it feels like navigating a storm without a map. This article can easily lead you into a negative mindset, but today we will stay positive.

Figure: Founders navigating in DeFi/Venture Capital liquidity pools

In the first part, we will delve into the basics of angel investors and venture capital in the cryptocurrency space. Understanding what drives their investment decisions is crucial to grasping why they accept or reject deals.

We will discuss their primary goals when selecting investments, how they handle deals, and the three major criteria used to evaluate potential investments.

Next, we will explore common failure points, combining personal experiences and insights from second-time founders in this rugged field. Ultimately, I hope to provide you with knowledge to view fundraising with a clearer perspective and better prepare for the challenges it brings.

Let’s go, friends, we can do this.

Your Angel Investors

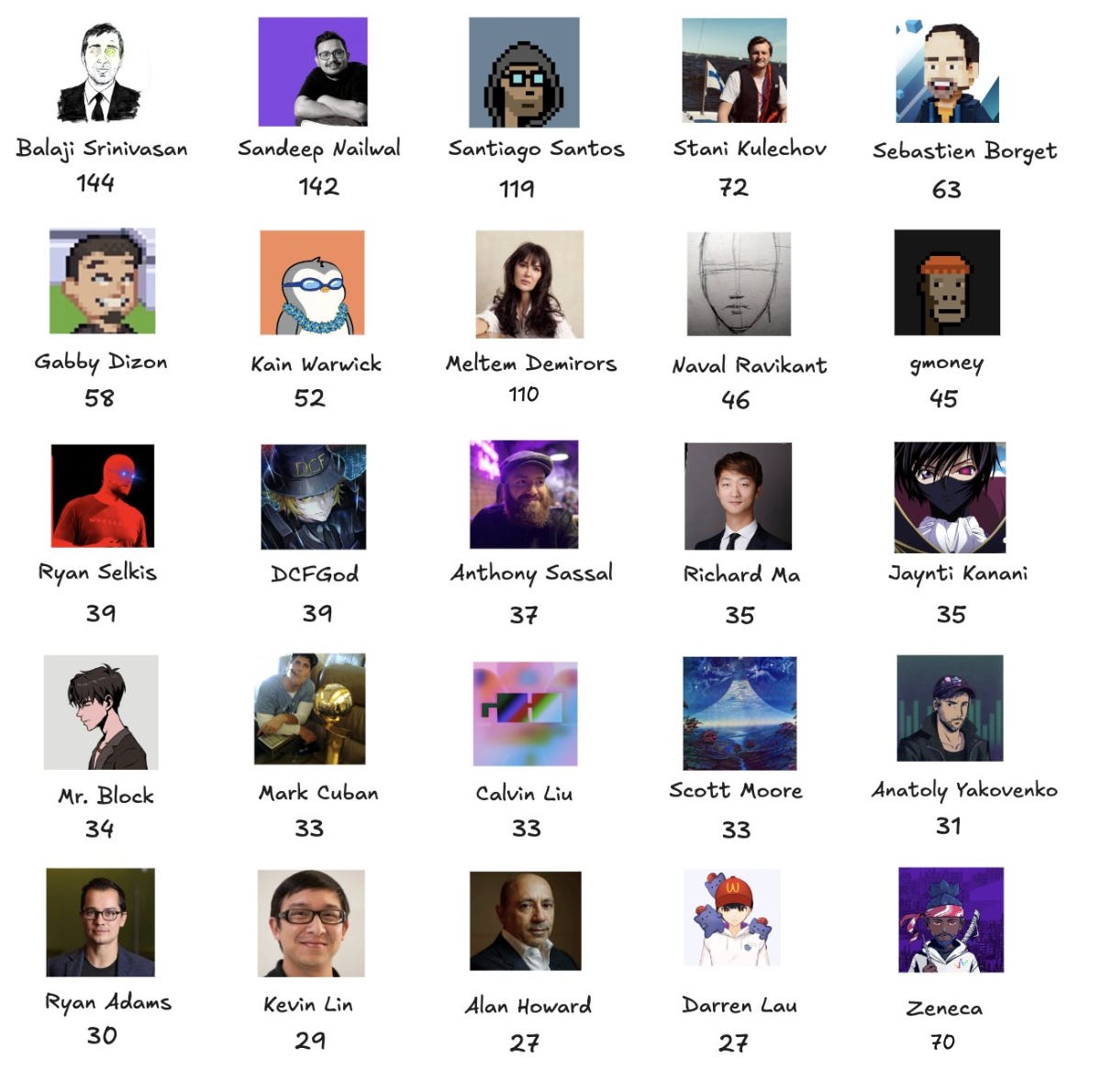

Founders often raise their first angel round funding from Twitter friends and Discord communities. In this process, building the equity structure is crucial. Founders often bring in angels who are loud but lack substantial support, and when introductions or meaningful feedback are needed, they are nowhere to be found. The harsh reality is: If someone has completed over 150 deals in the past year, they may not be the reliable signal you need.

Figure: Top-ranked angel investors by number of deals, source: Rachit

What Drives Angel Investment?

Angel investment heavily relies on networking. Some angel investors, like the founders of Polygon, support ecosystem projects; while others, like GMoney and Zeneca in the NFT space, operate within specific circles of influence. However, return on investment (ROI) remains the primary driver for most angel investors.

There is a small group of frustrating angel investors who invest merely for signals—hoping to get into hot equity structures for more investment opportunities. While I don’t hold them in high regard, if used properly, they can still help build some connections. This leads us to the two core elements of the angel round: signals and insights.

Signals vs Insights

Signals are industry-specific. In Solana DeFi, gaining support from Mert or Anatoly is a success. In gaming, getting backing from Ellio Trades shows a deep understanding of the field. But gaining support from the head of the Avalanche ecosystem for a ZK project? That might not be as useful.

On the other hand, insights can compress months of work into weeks—like experts such as DCF God sharing TVL strategies. At the angel stage, you need both signals and insights, but understand that your equity structure may consist of 90% signals and 10% insights.

Building the Equity Structure and Due Diligence

Finding the right angel investors not only enhances credibility but also lays the groundwork for subsequent rounds that are riskier and offer higher returns.

You are giving away ownership at the best price, so you must clarify the added value each angel brings to the equity structure and know how to leverage it effectively. Core angels will use their networks to help you refine the equity structure. Most angel rounds are high-risk, high-reward—they can lead you to major primary funds or may fail. These investments heavily rely on networks, and due diligence (DD) at this stage is often quite simple—a straightforward presentation is usually enough to get started.

The smartest founders will open their rounds to Series A, allowing valuable stakeholders to join at a significant discount. Venture capital firms typically don’t mind this “backdoor” approach, as it increases the overall value of the company.

Once you have refined your equity structure with early-stage angels, you enter a larger arena: venture capital. In the next section, we will explore how venture capital firms operate.

Venture Capital

In this section, we will explore from the perspective of investors. Who leads these investors, what do limited partners (LPs) expect in terms of return on investment (ROI) from funds, and how does the venture capital circle operate? We will also delve into why venture capital firms choose their investment strategies, the usual processes for deal handling, and why ROI remains the primary driver for most investment decisions.

Limited Partners: The Top of the Liquidity Chain

Figure: The big boss

At the top of the liquidity chain are the limited partners (LPs) who provide capital to venture funds. In the crypto space, these LPs are often early cryptocurrency adopters, including investors, operators, and miners who made wealth in previous cycles. After experiencing exponential returns, they now expect quick and substantial returns from venture capital.

In the crypto space, investments are typically token-based, accompanied by vesting schedules, liquidity events, and market cycles that move much faster than traditional equity. Therefore, the expected return cycles are much shorter. The opportunity cost of holding capital in slow, long-cycle projects is high, so LPs demand faster ROI, pushing VCs to invest at a pace that matches market volatility and speed.

Although the pressure from more LPs does not directly translate to the investment team due to many legal separations, the key is that funds know they must satisfy LPs by achieving 1000x returns to raise Fund-3 and Fund-4.

Figure: Venture capital firms raising new funds

Essentially, this dynamic makes venture capital in the crypto space unique: capital is impatient, risks are high, and there is little room for error. Venture capital firms know they must not only outpace competitors but also deliver quickly to meet the growing expectations of limited partners (LPs). However, this dynamic is changing as more mature capital re-enters the space, including from pension funds, family offices, and web2 venture capital firms.

From the Investor's Perspective

An interesting combination has emerged, as this LP capital is often combined with analysts and associates, many of whom are fresh out of college with little operational experience (I was one of them). These analysts are expected to handle over 360 deals a year, covering a wide range of areas from ZK to modular infrastructure.

Figure: A dramatized and simplified view of crypto venture capital in Q2 2023

This toxic relationship driven by rampant speculation between investors and founders has led to a bubble-like fundraising environment. Unfortunately, in this flawed system, the most affected are founders who are not within traditional success circles, such as those outside of Ivy League schools, the Singapore VC network, or London’s web3 running groups. These founders often find themselves at a disadvantage because they a) do not understand how deal processing works in crypto venture capital, b) have limited access to capital deployers, forcing them to pitch based solely on the merits of their ideas with almost no room for error.

This is a harsh reality, but if you are an investor reading this, I strongly encourage you to invite 5 non-traditional proposals each month. We can eliminate this systemic issue in our industry by addressing 5 deals at a time. Now, back to the established agenda.

Deals in Progress

For the investment committee (IC) to approve an investment, the conditions on a Monday morning must be perfect: the deal lead needs to distribute a 20-page investment thesis the previous Thursday (with final edits added on Sunday night), and the chief investment officer’s coffee temperature must be just right.

The first point of discussion is usually the alignment of the investment thesis. The deal must align with the company’s investment strategy in areas like infrastructure, gaming, or the Bitcoin ecosystem. Next, the deal lead presents her investment thesis to the IC—why this is an interesting problem worth solving, what makes this solution unique, why this is the right team to solve the problem, and what kind of returns participating in this round can bring.

Essentially, the deal lead focuses on ROI and risk.

ROI

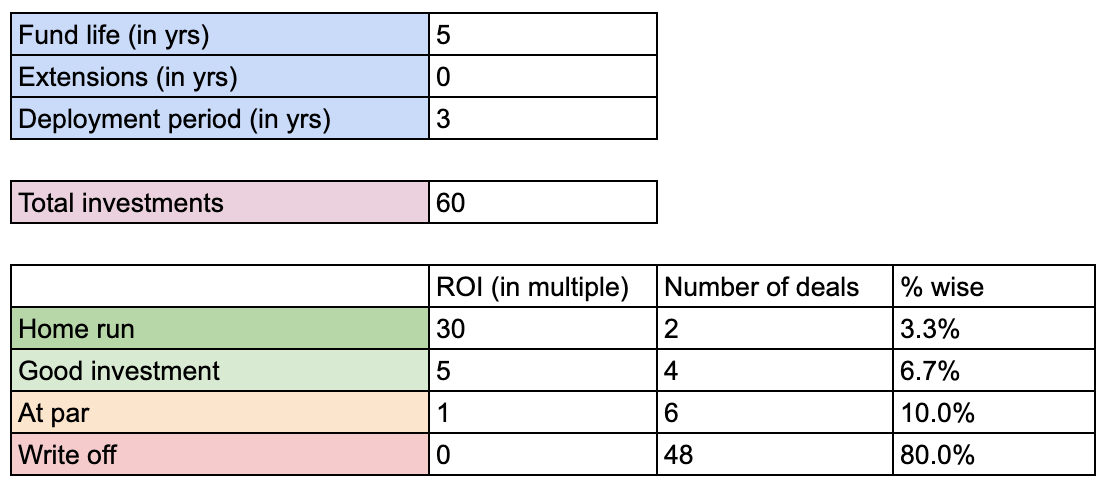

Let’s take a look at a typical portfolio construction to understand what average ROI expectations look like:

A very optimistic portfolio construction in crypto venture capital around 2021

Anyone hoping to get promoted in a venture firm is eager to land that home run deal, while more mature investors are willing to dig for gold with a 1/100 chance. A 30x return is certainly important, but if the risk of a deal is low enough, even a 5x return can be attractive from a portfolio construction perspective.

To illustrate this further, consider: entering a deal at a $25 million valuation with the potential to exit at $250 million offers a better risk-adjusted ROI than joining a hot $1 billion seed round, as the latter has a lower likelihood of achieving a 10x return. However, WLD managed to do this.

In the current cycle, funds are increasingly cautious about investment lock-up periods. A project achieving 60x at TGE but dropping to 2x by the time of fund unlock is far from a successful investment. We see a polarization in this space—either you are raising a $7 million seed round, or you are struggling to scrape together $1 million from third-tier investors, with almost no middle ground existing.

Review

Venture capital firms typically spend about 40 seconds reviewing each investment proposal, so adhering to their investment framework is crucial for survival in the fierce competition of crypto venture capital. Over time, this framework has gradually simplified into a one-liner view for most industries:

There are too many Bitcoin infrastructure projects, and large investors are not interested;

NFTs are considered a product of the last cycle;

DeFi? Most of the infrastructure has already been built. The best investors have a flexible view of various industries and update their positions on problem statements by continuously reading and following thought leaders.

Founders who thoroughly research their competitors are like hidden diamonds in the investment market. For founders, effective insights lie in the fact that by 2024, the investors you face may have seen deals similar to yours and may have even lost money in that space. Your task is not only to explain why previous attempts failed (demonstrating your understanding of the industry) but also to articulate why you are capable of succeeding. Whether through executing insights, customer validation, or technical prowess, you need to redefine the investment return of the project. Each cycle, the benchmarks become increasingly mature.

In my career, I have used a rigorous framework to evaluate deals, but frankly (more often than I would like to admit), strong deal leads and the founder's fit with the problem often influence my decisions.

Rejecting others is always unpleasant.

This is why investors often give generic responses like "the timing is not right" or "it doesn't align with our investment philosophy" when rejecting deals. But here are some real reasons I personally reject deals:

Founder and problem mismatch: If the founder lacks relevant experience, it’s a red flag. For example, a custody business requires enterprise sales experience, so the founder's background must be closely related to the problem.

No competitive advantage: If the project lacks a competitive edge—whether it’s better distribution channels, higher total value locked (TVL), more users, or stronger technical capabilities—it’s hard to gain support. It becomes difficult to pitch the 17th stablecoin when a Stanford PhD in cryptography is already developing a similar solution.

Low return/high-risk industry: Some industries simply cannot provide the returns most funds expect; DAO deals often fall into this category. Similarly, most funds do not invest in gaming projects due to the high risk of failure.

Zero-knowledge issues: Sometimes, an excellent project may not align with our investment philosophy. For instance, I wouldn’t invest in a ZK-intensive project unless it’s led by someone known for thorough technical due diligence.

SAFT > SAFE: Equity investments require more due diligence and are often less flexible than token raises.

Overly transformative founders: Founders who frequently pivot to cater to market trends often lose investors' trust.

Distribution bottlenecks: If Metamask or other large companies develop similar features, your distribution advantage could vanish in an instant. I wouldn’t risk participating in such deals.

Of course, not every rejection is correct. Some projects I rejected later performed exceptionally well. My anti-portfolio is painful, and when I talk to my VC friends, Celestia and Botanix are among the most frequently mentioned missed opportunities.

Fundraising Like a Winner

Many tech-focused founders fear pitching because it feels too much like sales. But it’s unrealistic to survive without this ability. Pitching to investors is a professional skill, and your presentation and data room are like a good pair of running shoes. Sure, you can complete a 5K without running shoes, but why would you?

Yes, definitely create a presentation

As we discussed earlier, investors face an influx of deals. Unless you already have a strong network, having polished sales materials (like presentations and data rooms) will help you find lead or major investors more quickly.

Keep pitching

Another key step is to practice your pitch as much as possible and gather feedback. You need to know your pitch inside and out—you can’t afford to appear awkward in this area. The more people you talk to (whether they are marketers, business developers, or tech people—anyone willing to listen), the more powerful and refined your pitch will become. Demo days and venture capital events are excellent opportunities to test your pitch and receive real-time feedback from diverse audiences.

Additional reading: The Art of Feedback

As I mentioned earlier, people hate saying "no," which is a fundamental psychological phenomenon. Therefore, investors often give vague reasons for rejection. Don’t hesitate to seek more specific feedback from investors you respect. Most may not agree, but those who are confident enough to engage with you will provide valuable insights that can help you truly understand the potential issues with your thesis.

The more enthusiasm, the better

The crypto space is small, and enthusiastic referrals are crucial. Cold DMs are inefficient; I once sent 60 DMs and received only 5 replies. Instead, you should spend time building genuine connections on platforms like Twitter and Telegram—relationships on these platforms are vital. Similarly, submitting pitch materials through websites doesn’t work—99% of the funds I know are either reviewed by interns or, worse, not looked at at all.

Figure: The only important metaverse is the Twitter world

The charm of cryptocurrency lies in the fact that everyone is on Twitter. It’s an open platform where you can leverage it to build real connections. Rushi from Movement is a great example of someone who effectively uses Twitter to bring potential clients to projects. The best approach is through enthusiastic referrals—through people you chat with on Twitter or Telegram, or those you meet at conferences (though I think conferences are quite inefficient). Spending a month being active on Twitter before fundraising is the best way to build relationships with investors. Mutual introductions between founders are ideal, but unfortunately, many people are stingy when it comes to referring investors.

Even my investor friends who entered the field in 2020 and have transitioned to builders in this cycle have faced difficulties in pitching and obtaining referrals. So yes—it is indeed challenging.

Tomorrow Will Be Better

The failure rate of startups is as high as 99%. There are many things that can go wrong—whether it’s poor product-market fit, difficulty in assembling the right team, execution failures, low industry investment returns, or simply being at the wrong time.

However, during the fundraising process, I repeatedly see certain specific failure points. At the execution level, failures often stem from a mismatch between the founder and the problem, insufficient research, inadequate documentation, or a pitch that lacks refinement. Industries with mediocre investment returns, overly saturated markets, and excessive reliance on cold introductions can also quickly lead to deal failures.

What to do after fundraising fails?

This is a difficult question to answer—if investor interest is low, should you continue pushing the project? The answer is: it depends.

Staying flexible during the fundraising process is crucial. If you fail to complete a round of funding or are considering abandoning the project, remember that the design space is still vast. If you can demonstrate growth and learning, good investors will be willing to support you again. Always maintain a learning attitude.

Listen to the opinion of an anonymous source, a second-time founder in the field. He shared this key lesson:

There is a difference between knowing when to stop and truly acknowledging it. In [Project 1], I held on until the end because I believed (and still believe) that the direction of venture capital is wrong—there will ultimately be a market for options and derivatives in decentralized finance (DeFi). But I knew from the start that raising funds would be difficult.

Looking back, the biggest mistake was raising funds on the fly and launching the product during fundraising—this quantified the opportunity before we were truly ready. It’s better to wait until you have enough funds to refine the product before going public. This is a profound lesson.

Ultimately, the path to success for [Project 2] was exactly the opposite: build credibility, attract interest, and close big deals. An investor offered me $2 million to use at my discretion, entirely because my capital structure was clear, and I earned their trust as a serious builder.

— Anonymous, Anonymous Founder

What’s Next?

Experiences in the crypto venture capital field are like a roller coaster. I entered this industry right after graduating from college and witnessed the boom of 2021 in my first year. Since then, my investment standards have continuously evolved. Today, I primarily focus on the founders' ability to handle risks and failures. No due diligence questionnaire (DDQ) can comprehensively cover this, but fortunately, processing countless business plans is no longer my key performance indicator. This freedom allows me to interact more closely with founders, giving me the opportunity to identify those I believe will succeed and invest more time in those relationships.

The fact is, fundraising is often nerve-wracking, more of a struggle than a success. But every failure brings growth. My conversations with founders and investors are now more vibrant and profound because we focus on resilience, adaptability, and the courage needed to push forward.

Ultimately, this journey is always moving forward. Stay resilient and keep going.

Life is interesting, anonymous, don’t be so serious.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。