Original Title: Airdrops in the Barren Desert: Surveying the traits behind 2024’s 11% success rate

Author: Keyrock

Translation: Scof, ChainCatcher

Key Points:

- Difficult to sustain

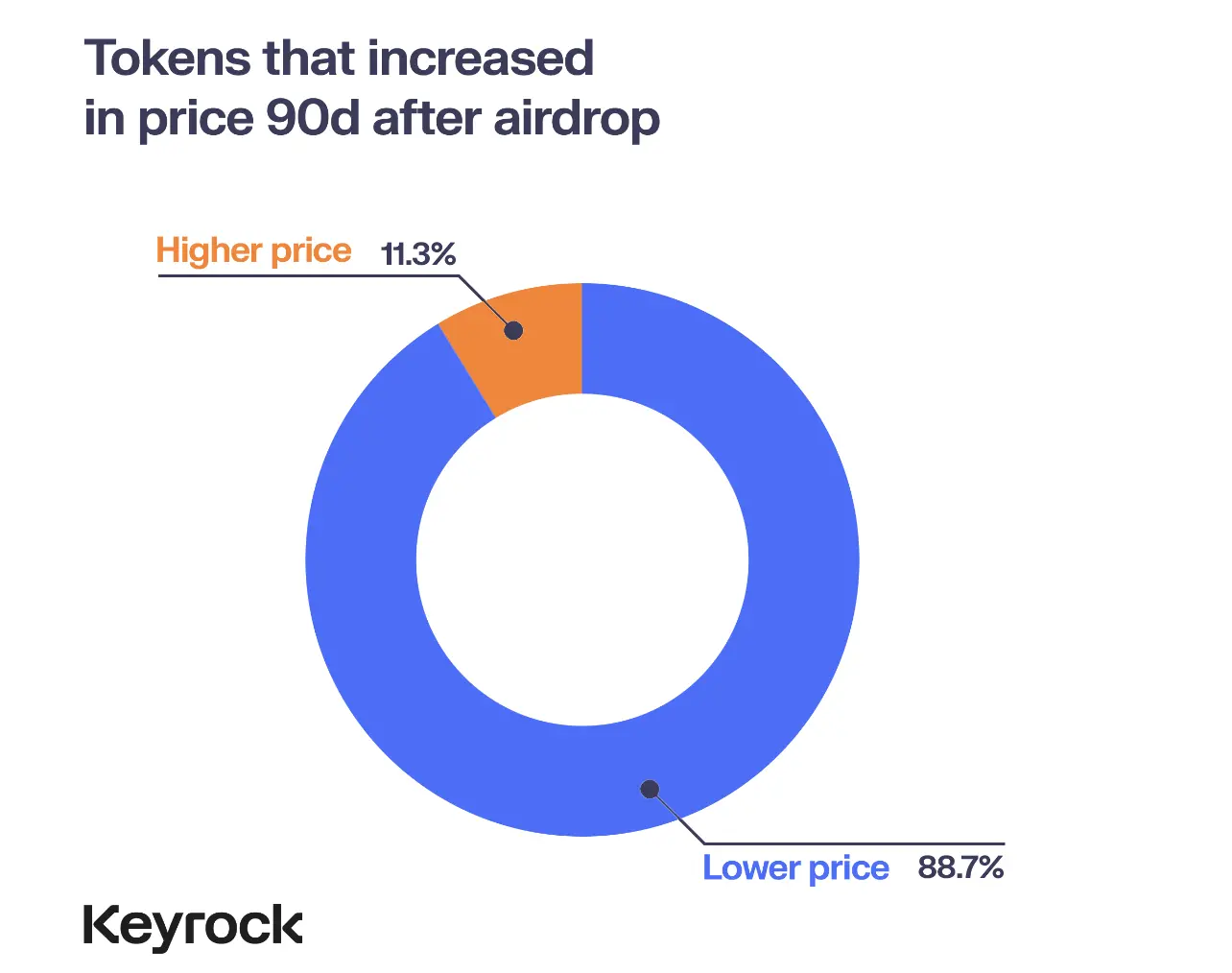

Most airdrops collapse within 15 days. In 2024, despite the initial price surge, 88% of tokens depreciated within a few months.

- Significant fluctuations****

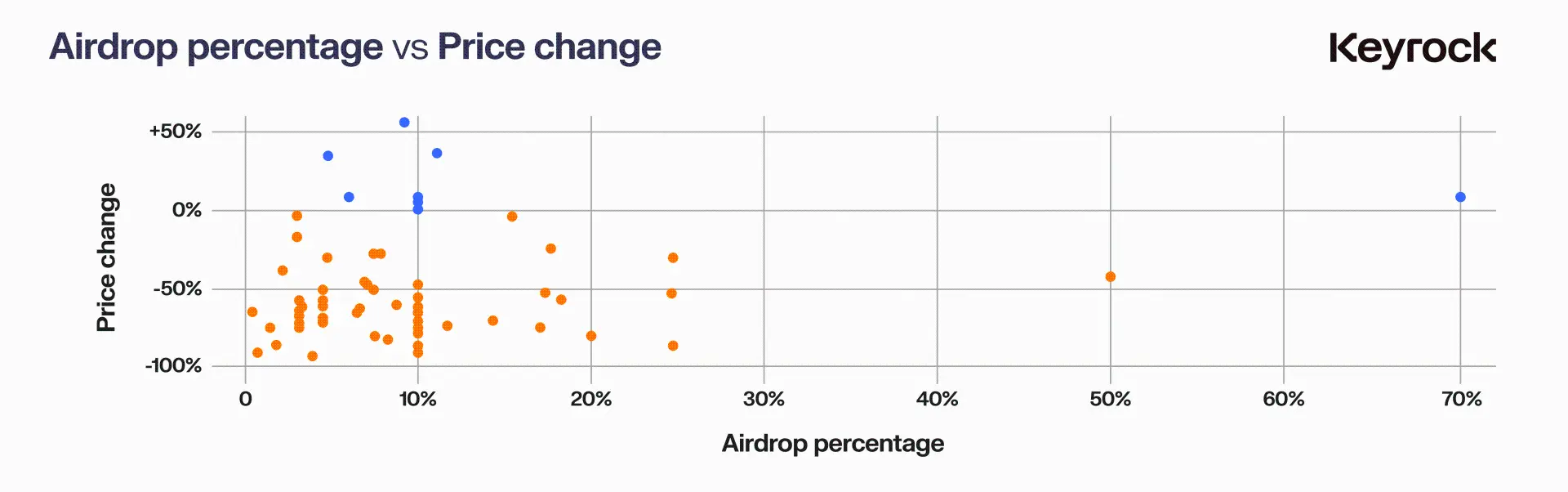

Airdrops distributing more than 10% of the total supply saw stronger community retention and performance. Those below 5% typically faced rapid sell-offs post-release.

- High FDV

Excessively high fully diluted valuation (FDV) inflicts the most damage on projects. High FDV inhibits growth and liquidity, leading to sharp price declines post-airdrop.

- Liquidity is crucial

Without sufficient liquidity to support high FDV, many tokens collapse under selling pressure. Deep liquidity is key to price stability post-airdrop.

- Challenging year

Cryptocurrencies struggled in 2024, with most airdrops taking the hardest hit. For the few successful cases, intelligent allocation, strong liquidity, and realistic FDV were their strategies.

Airdrops: A double-edged sword for token distribution

Since 2017, airdrops have been a popular token distribution strategy used to create early excitement. However, in 2024, due to oversaturation, many projects struggled to succeed. While airdrops still bring initial excitement, most airdrop outcomes resulted in short-term selling pressure, leading to low community retention and protocol abandonment. Nonetheless, some outstanding projects successfully broke this trend, proving that with the right execution, airdrops can still bring meaningful long-term success.

Research Objectives

This report attempts to unravel the mystery of the 2024 airdrop phenomenon—distinguishing winners from losers. We analyzed 62 airdrops across 6 chains, comparing their performance in several aspects: price action, user acceptance, and long-term sustainability. While each protocol has its unique variables, the collective data vividly portrays the effectiveness of these airdrops in achieving their intended goals.

Common** Performance**

When examining the overall performance of 2024 airdrops, most performed poorly post-release. While some saw impressive returns in the early stages, most tokens faced downward pressure on their value in the market. This pattern points to a broader issue within the airdrop model: many users may be there just for the incentives rather than long-term interaction with the protocol.

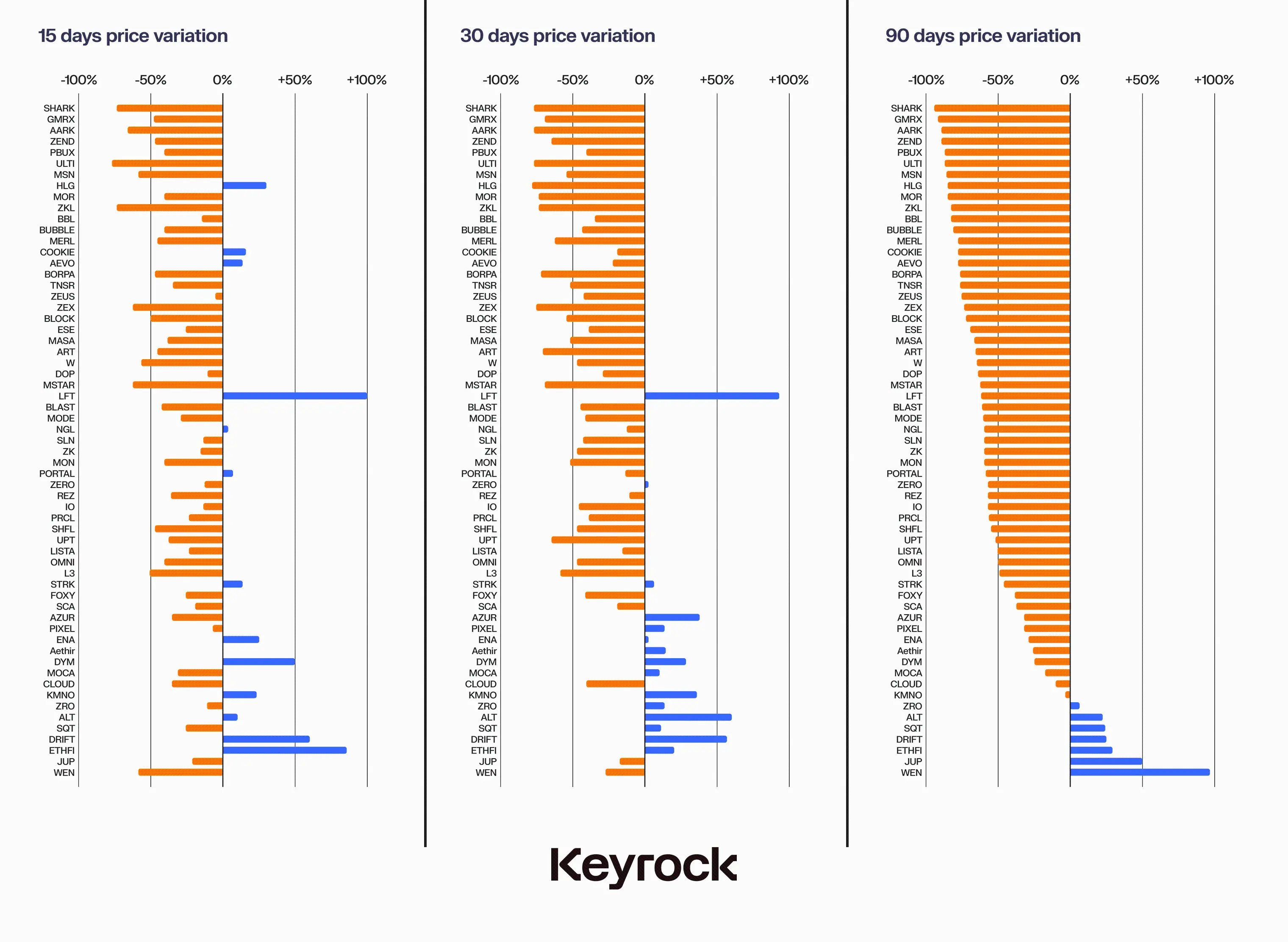

For all airdrops, a key question arises—does the protocol have staying power? Do users continue to see value in the platform once the initial rewards are distributed, or is their participation purely transactional? Our analysis from data across multiple time frames revealed a key insight: for most of these tokens, enthusiasm quickly wanes, typically within the first two weeks.

Overall** Performance**

Observing price trends at 15, 30, and 90 days, it is evident that most price movements occur in the initial few days post-airdrop. Three months later, few tokens were able to achieve positive returns, with only a handful moving against the trend. Nonetheless, it is important to consider the broader context: during this period, the overall performance of the entire crypto market was not favorable, making the situation more complex.

Chain Distribution

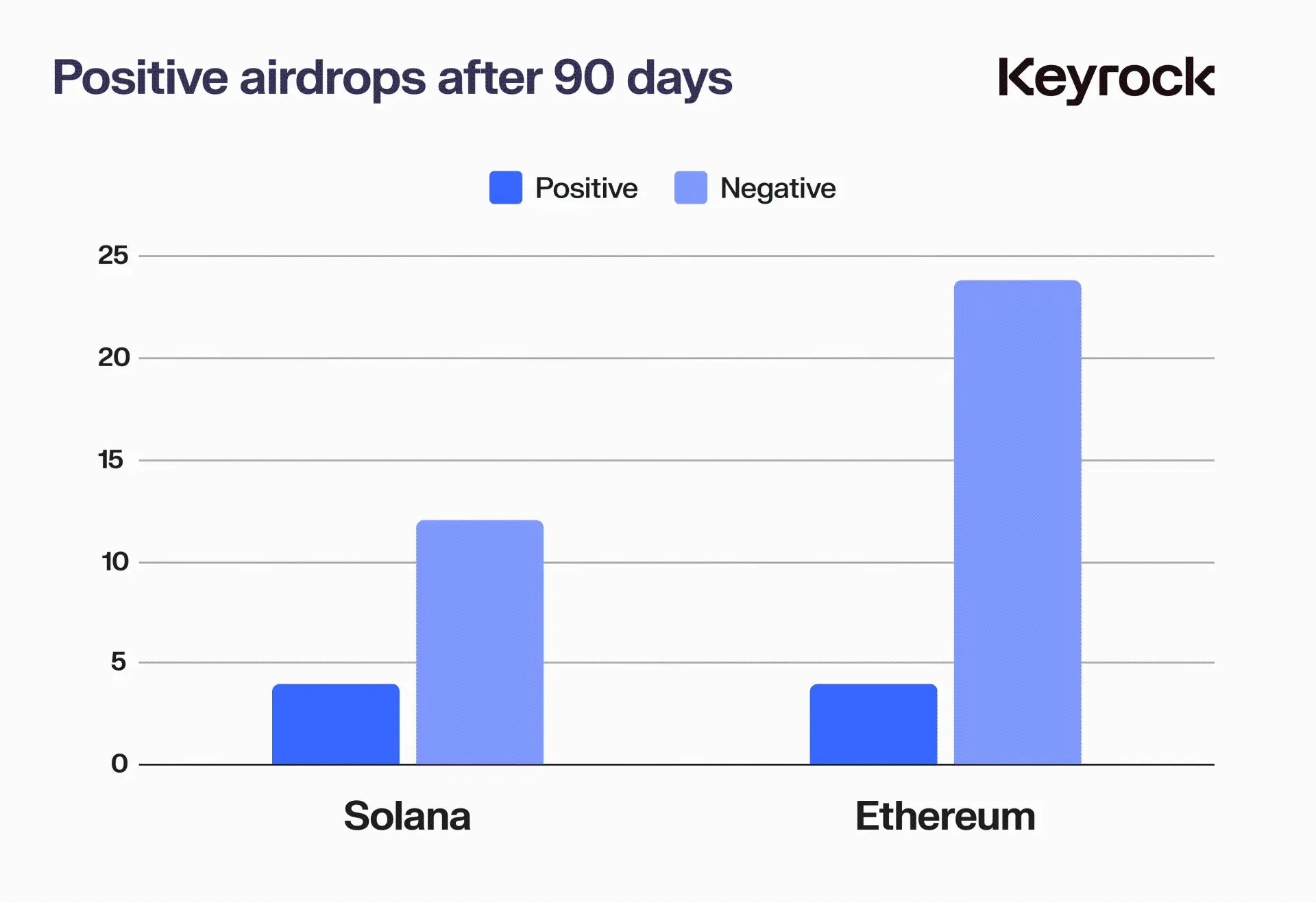

Despite the overall poor performance, not all chains fared the same. Among the analyzed 62 airdrops, only 8 achieved positive returns after 90 days—4 on Ethereum and 4 on Solana. BNB, Starknet, Arbitrum, Merlin, Blast, Mode, and ZkSync had no winners. Solana had a success rate of 25%, while Ethereum had 14.8%.

For Solana, this is not surprising, as the chain has become a favorite in the retail market over the past two years, truly challenging Ethereum's dominance. Moreover, considering many of the other chains we examined are layer 2 chains directly competing with another chain, it is not surprising that only a few winners were retained by the parent chain.

While we did not include Telegram's Ton network, we do want to point out that there have been several successful airdrop cases on the network as enthusiasm and adoption have expanded.

Differences among different public chains (Chain Division)

In other words, if we attempt to separate large chains from their airdrops, would the data change considering the trends of the native tokens of public chains? When we standardize these airdrop prices and compare them with the performance of their respective ecosystems—such as comparing airdrops on Polygon with the price trends of $MATIC, or airdrops on Solana with $SOL—the results are still not optimistic.

Yes, the market has declined, and the highs of 2023 have cooled off, but this is not enough to mask the lackluster performance of airdrops, whether compared to system tokens or general altcoins. These sell-offs are not entirely isolated from the larger narrative, reflecting widespread concerns in the market about short-term prosperity. When something that was considered "established" is declining, no one wants something untested or "new."

Overall, the improvement is at best modest, with Solana and ETH experiencing about a 15-20% decline in some 90-day windows, even at their worst, indicating much greater volatility for these airdrops, and only being connected to the larger narrative rather than in price performance.

Performance based on distribution

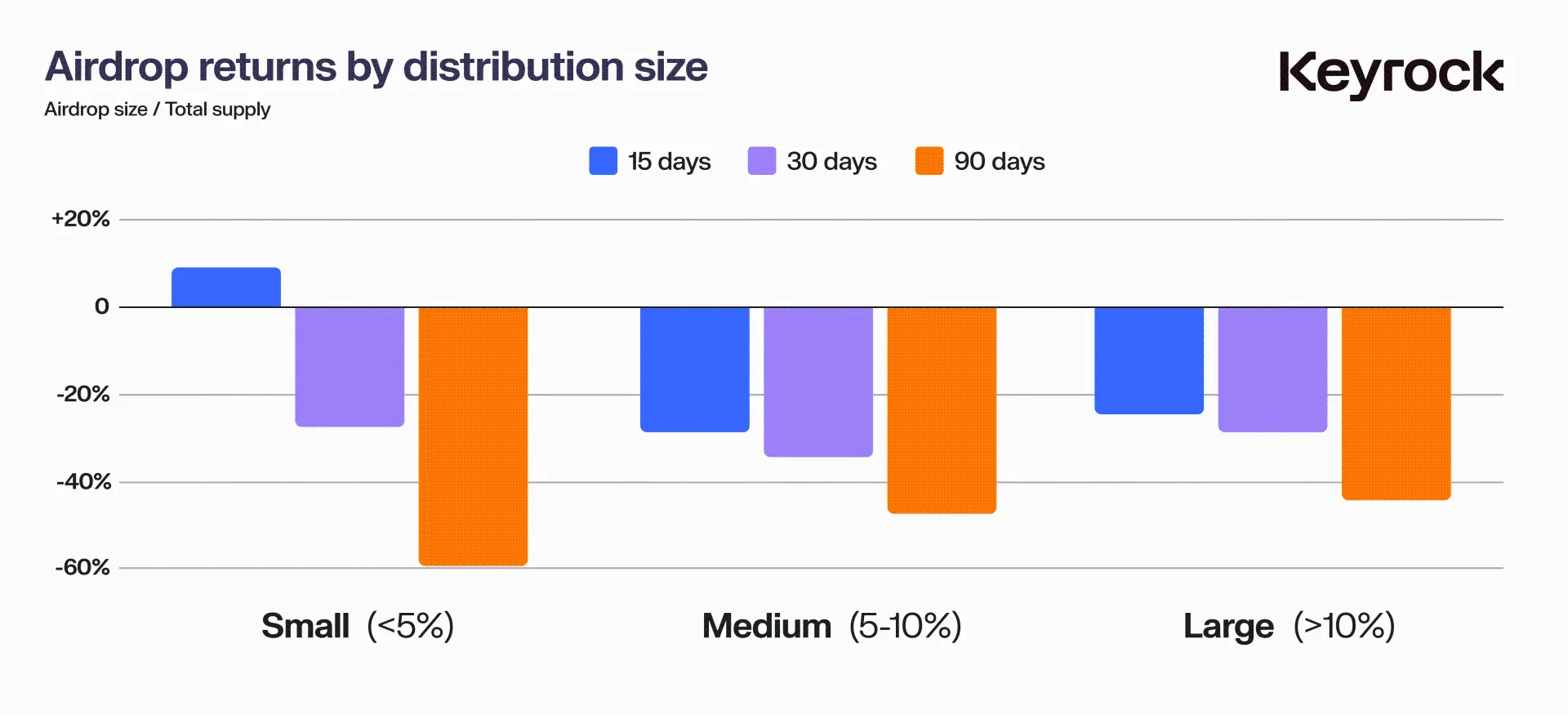

Another key factor affecting airdrop performance is the distribution of the total token supply. The protocol's decision on how much token supply to allocate can significantly impact its price performance. This raises a critical question: is generosity worth it? Or is conservatism safer? Does giving users more tokens lead to better price trends, or does the risk come from giving out too much too quickly?

To break down this issue, we divided the airdrops into three groups:

- Small airdrops: 5% of the total token supply

- Medium airdrops: >5% and ≤10%

- Large airdrops: >10%

Then we examined their performance over three time periods—15 days, 30 days, and 90 days.

In the short term (15 days), smaller airdrops (5%) performed better, possibly because the limited supply created less immediate selling pressure. However, this initial success is often short-lived, and tokens from small airdrops experienced significant sell-offs within three months. This may be due to a combination of factors: the low supply initially suppressed selling, but over time, as the narrative shifted or insiders began selling, the broader community followed suit.

Medium airdrops (5-10%) performed slightly better, balancing supply distribution with user retention. However, large airdrops (>10%) performed best over a longer time frame. These larger allocations, while potentially carrying greater short-term selling pressure risk, seem to foster stronger community ownership. By allocating more tokens, the protocol may empower users, giving them a greater stake in the project's success. This, in turn, can lead to better price stability and long-term performance.

At last, these data indicate that being less stingy with token allocation is worth it. Generous protocols in airdrops tend to cultivate a more committed user base, leading to better results over time.

Distribution Dynamics

Impact of Token Allocation

Our analysis shows that the scale of airdrops directly affects price performance. Small airdrops create less initial selling pressure but often see significant sell-offs within a few months. On the other hand, larger allocations indeed create more volatility in the early stages but lead to stronger long-term performance, indicating that generosity encourages more loyalty and token support.

Linking Distribution to Market Sentiment

Community sentiment is a key factor in successful airdrops, although often elusive. Larger token allocations are often seen as fairer, giving users a stronger sense of ownership and participation. This creates a positive feedback loop—users feel more invested and are less likely to sell their tokens, contributing to long-term stability. In contrast, smaller allocations may initially feel safer but typically lead to short-lived enthusiasm followed by rapid sell-offs.

While it is difficult to quantify the sentiment or "atmosphere" of all 62 airdrops, they remain powerful indicators of sustained project appeal. Signs of strong sentiment include active and engaged communities on platforms like Discord, natural discussions on social media, and genuine interest in the product. Additionally, the novelty and innovation of a product often help maintain positive momentum, as they attract more committed users rather than opportunistic bounty hunters.

Impact of Fully Diluted Valuation (FDV)

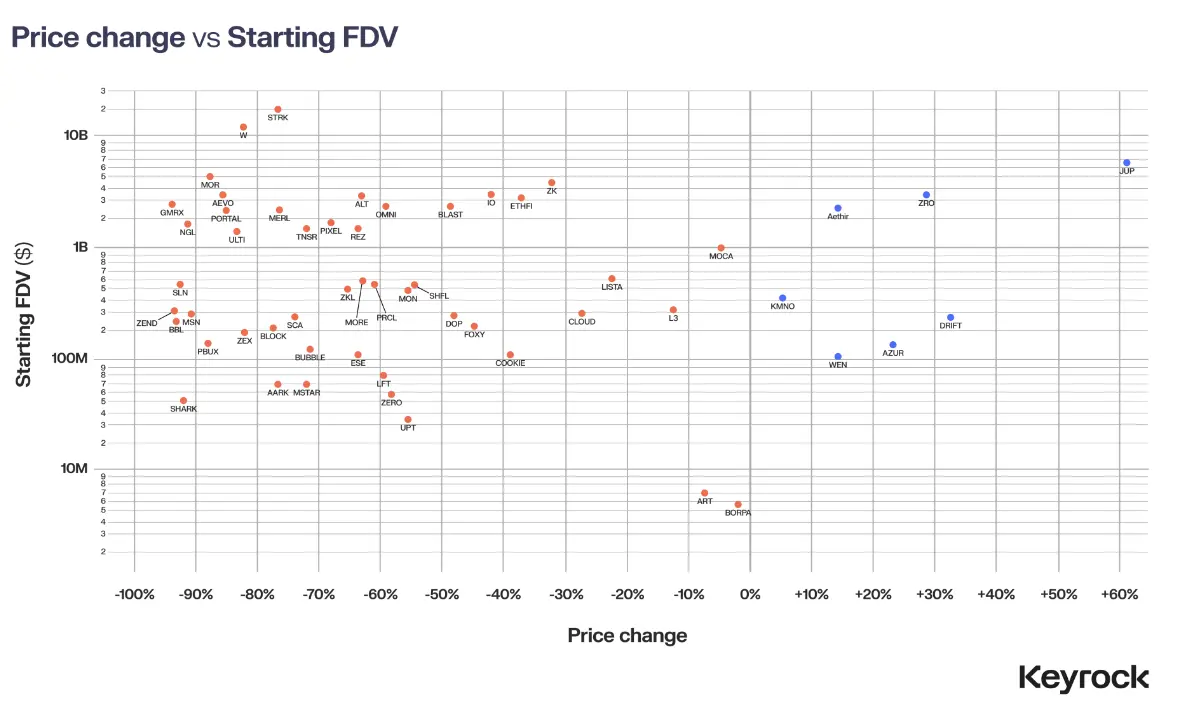

An important area of concern is whether the fully diluted valuation (FDV) of tokens at launch significantly affects their post-airdrop performance. FDV represents the total market value of a cryptocurrency if all possible tokens, including those not yet unlocked or distributed, are in circulation. It is calculated by multiplying the current token price by the total token supply, including circulating tokens and any locked, vested, or future tokens.

In the crypto space, we often see projects with FDVs that seem excessively high compared to their actual utility or impact at launch. This raises a key question: are tokens being punished for inflated FDVs at launch, or does the impact of FDV vary by project?

Our data covers projects launched with a conservative FDV of $5.9 million to a staggering $19 billion— a difference of 3,000 times within the sample of 62 airdrops we analyzed.

As we plot this data, a clear trend emerges: the larger the FDV at launch, the greater the likelihood of a significant price decline.

FDV Relationships

Two main factors are at play here. First is the fundamental market principle: investors are attracted by the perception of upward mobility. Tokens with a lower FDV offer growth potential and the psychological comfort of "early entry," attracting investors and promising future returns. On the other hand, projects with inflated FDVs often struggle to sustain momentum as the perceived upward space becomes limited.

Economists have long discussed the concept of market "space." As Robert Shiller puts it, "irrational exuberance" quickly fades when investors feel limited returns. In the crypto space, when a token's FDV indicates limited growth potential, that exuberance also quickly dissipates.

The second factor is more technical: liquidity. Tokens with large FDVs often lack the liquidity to support these valuations. When significant incentives are allocated to the community, even a small portion of users looking to cash out can create significant selling pressure with no buyers on the other side.

Take $JUP, for example, which launched with a modest FDV of $690 million, supported by a series of liquidity pools and market makers estimated to be worth $22 million on launch day. This gave $JUP a liquidity-to-FDV ratio of only 0.03%. Compared to the 2% liquidity-to-FDV ratio of its meme coin counterpart $WEN, this number is relatively low but relatively high compared to other tokens of the same weight.

In contrast, Wormhole launched with a large FDV of $13 billion. To achieve the same 0.03% liquidity-to-FDV ratio, Wormhole would need $390 million in liquidity across venues. However, even including all available pools, both official and unofficial, and Cex liquidity, our best estimate is closer to $6 million—only a small fraction of the required amount. With 17% of tokens allocated to users, this sets the stage for a potentially unsustainable market value. Since launch, $W has dropped by 83%.

As a market maker, we know that without sufficient liquidity, prices are highly sensitive to selling pressure. The combination of the two factors—psychological demand for growth potential and the actual liquidity required to support large FDVs—explains why tokens with higher FDVs struggle to maintain their value.

The data confirms this. Tokens with lower FDVs experienced less price erosion, while those launched with excessively high valuations suffered the greatest losses in the months following the airdrop.

Overall Winners and Losers

To gain a deeper understanding of some participants, we selected a winner and a significant underperformer from this quarter's airdrops as case studies. We will explore what they did right and where they went wrong, which ultimately shaped their success or failure in the eyes of the community.

Airdrop Season: Case Studies of Winners and Losers

As we delve into the airdrop season, let's examine an outstanding winner and a notable underperformer to reveal the factors that led to their vastly different outcomes. We will explore what these projects did right or wrong, which ultimately shaped their success or lack thereof in the eyes of the community.

Winner: $DRIFT

First up is Drift, a decentralized futures trading platform operating on Solana for nearly three years. Drift's journey has been filled with victories and challenges, including enduring several hacks and exploits. However, each setback forged a stronger protocol, evolving into a platform that has proven its value far beyond a mere airdrop breeding ground.

When Drift's airdrop finally arrived, it was warmly welcomed, especially by its long-term user base. The team strategically allocated 12% of the total token supply for the airdrop, a relatively high percentage, and introduced a clever bonus system that launched every six hours after the initial allocation.

Launching with a modest market value of $56 million, Drift surprised many, especially compared to other virtual automated market makers (vAMMs) with fewer users and less history but higher valuations. Drift's value quickly reflected its true potential, reaching a market value of $163 million—growing 2.9 times post-launch.

The key to Drift's success lies in its fair and thoughtful distribution. By rewarding long-term, loyal users, Drift effectively filtered out new Sybil farmers, nurtured a more genuine community, and avoided the toxicity that sometimes plagues such events.

What Sets Drift Apart?

Heritage and Solid Foundation

- Drift's long history allowed it to reward an existing determined user base.

- With a high-quality, validated product, the team could easily identify and reward genuine power users.

Generous Layered Allocation

- Allocating 12% of the total supply—significant for an airdrop—demonstrates Drift's commitment to its community.

- The staged release structure helped minimize selling pressure, maintaining value stability post-release.

- Crucially, the airdrop was designed to reward actual usage, not just metrics inflated by yield farming.

Realistic Valuation

- Drift's conservative launch valuation avoided the trap of excessive hype, maintaining expected stability.

- Seeded enough liquidity in initial pools, ensuring smooth market operations.

- A low fully diluted valuation (FDV) not only set Drift apart but also sparked broader industry discussions about overvaluations among competitors.

Drift's success was not accidental; it was the result of intentional choices prioritizing product strength, fairness, and sustainability over short-term hype. As the airdrop season continues, it is evident that protocols hoping to replicate Drift's success are best served by focusing on building a solid foundation, nurturing genuine user engagement, and maintaining a realistic view of their market value.

$ZEND: From Hype to Collapse—A Starknet Airdrop Failure

ZkLend ($ZEND) is currently facing significant downturn—its value has plummeted by 95%, with daily trading volume struggling to exceed $400,000. This is a stark contrast for a project that once had a market value of $300 million. More unusually, ZkLend's total value locked (TVL) now exceeds twice its fully diluted valuation (FDV)—an uncommon and not a positive signal in the crypto world.

So, how did a project that surged in the hype around Starknet—a solution aimed at scaling Ethereum through zk-rollups—end up in such an unstable position?

Missed the Starknet Wave, but Didn't Get on Board

ZkLend's concept was not groundbreaking—it aimed to be a lending platform for various assets benefiting from the Starknet narrative. The protocol leveraged the momentum of Starknet, positioning itself as a key participant in a cross-chain liquidity ecosystem.

Premise:

- Generate a farming network where users can earn rewards across different protocols.

- Attract liquidity and users through rewards and cross-chain activities.

However, in execution, the platform ultimately attracted "mercenary" activity farmers—those solely focused on short-term rewards with no commitment to the protocol's long-term health. Instead of nurturing a sustainable ecosystem, ZkLend found itself at the mercy of bounty hunters, resulting in transient engagement and low retention rates.

Backfiring Airdrop

ZkLend's airdrop strategy exacerbated its issues. Without significant product or brand recognition before the airdrop, the token allocation attracted speculators rather than genuine users. This critical mistake—failing to thoroughly vet participants—resulted in:

- A large number of bounty hunters eager to cash out quickly.

- Lack of loyalty or genuine engagement, as participants had no long-term commitment.

- Rapid token value collapse as speculators immediately sold their tokens.

Instead of building momentum and nurturing loyalty, the airdrop created a transient activity surge that quickly dissipated.

Cautionary Tale

ZkLend's experience is a powerful reminder that while hype and airdrops can bring in users, they do not inherently create value, utility, or a sustainable community.

Key Lessons:

- Hype alone is not enough—building real value requires more than just hype around popular narratives.

- Unvetted airdrops can attract speculation and disrupt value, as experienced by ZkLend.

- Excessive valuations for unproven use cases bring significant risks for new products.

Conclusion

If maximizing returns is the goal, selling on the first day is often the best move—85% of airdropped tokens see price declines within a few months. Solana led as a top-tier public chain in 2024, but considering market conditions, overall performance was not as bad as expected. Projects like WEN and JUP stood out as success stories, highlighting that a strategic approach can still yield strong returns.

Contrary to common belief, larger airdrops do not always lead to sell-offs. A token with a 70% airdrop allocation saw positive returns, emphasizing the greater importance of FDV management. Overvaluing FDV is a critical mistake. High FDV limits growth potential, and more importantly, creates liquidity issues—inflated FDV requires significant liquidity to sustain, which is often not available. Without sufficient liquidity, airdropped tokens are susceptible to significant price declines, as there is not enough capital to absorb selling pressure. Projects launched with realistic FDV and a solid liquidity supply plan are better equipped to survive post-airdrop volatility.

Liquidity is crucial. When FDV is too high, it puts immense pressure on liquidity. In cases of insufficient liquidity, large-scale sell-offs can crush prices, especially in airdrops where recipients are eager to sell. By maintaining manageable FDV and focusing on liquidity, projects can create better stability and long-term growth potential.

Ultimately, the success of an airdrop depends not only on the scale of distribution. FDV, liquidity, community engagement, and narrative are all crucial. Projects like WEN and JUP found the right balance, establishing lasting value, while other projects with inflated FDV and shallow liquidity failed to maintain interest.

In a rapidly changing market, many investors make quick decisions—selling on the first day is often the safest bet. But for those focused on long-term fundamentals, there are alwaystokensworth holding.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。