FDV is not a Meme.

Author: 0xLouisT

Compiled by: Deep Tide TechFlow

In Greek mythology, Icarus and his father Daedalus crafted wings with feathers and wax to escape the trap of King Minos. Daedalus warned his son, "Fly too low, and the ocean will wet your wings; fly too high, and the scorching sun will melt them."

But Icarus was intoxicated by the thrill of flying and soared higher and higher, forgetting his father's warning. The heat of the sun melted the wax that held his wings together, and Icarus fell into the sea. The moral of this story is that excessive arrogance often leads to self-destruction.

In the current cycle, I see astonishing similarities with the story of Icarus. Just as Icarus was drawn to the exhilaration of flight, many crypto projects are also lured by the temptation of high valuations. In both cases, they have led to their own destruction due to unsustainable promises and exaggerated valuations.

Why has this FDV frenzy occurred?

What are the reasons behind this frenzy of low circulation and high FDV? Several factors are at play:

Anchoring Effect: This cognitive bias influences decision-making, relying on the initial reference point. If founders believe their project is worth $1 billion, they may launch with a $10 billion FDV, setting a benchmark in the market's mind. Even if the token drops by 90%, it will still return to the founder's perceived fair value.

Venture Capital Valuations: The surplus of venture capital in 2021/2022 led to the inflation of private valuations. VCs paid excessively high prices in each funding round, while the public market was not interested in these high valuations. As no project is willing to conduct a Token Generation Event (TGE) at a valuation lower than the last round of private funding, they are forced to seek ways to launch at higher valuations.

Incentives and Treasury: A $100 billion FDV on paper boosts the project's treasury, enabling it to attract top talent, provide token incentives, offer ecosystem subsidies, and establish partnerships—driving growth with a significant paper value.

Supply Distribution: After ICOs and actions by the U.S. Securities and Exchange Commission (SEC), distributing tokens to the community has become more challenging. Airdrops and community incentives often cannot allocate a meaningful proportion of tokens at launch, which remains a major challenge for the industry.

OTC Sales and Hedging: High launch prices facilitate cash outflows through discounted OTC sales or hedging positions using perpetual contracts (perps), although conducting large-scale trades is difficult.

Cognitive Success: This reflects our way of thinking. Higher valuations create an illusion of success, attracting people to seemingly successful projects, and everyone wants to be involved.

How did all this initially happen?

If you create a token A with a supply of 1 billion and pair it with 1 USDC in a Uniswap pool, the nominal value of token A is $1, thus its FDV is $1 billion. This valuation is entirely artificial; the actual value of the token is very limited.

The same applies to high FDV tokens, where the actual circulating supply is only a small fraction of the total supply. After the initial selling pressure from airdrops subsides, most of the supply is held by liquidity providers and whales who can influence market prices. Therefore, a $10 billion FDV can be achieved with just tens of millions of dollars.

Issues related to high FDV

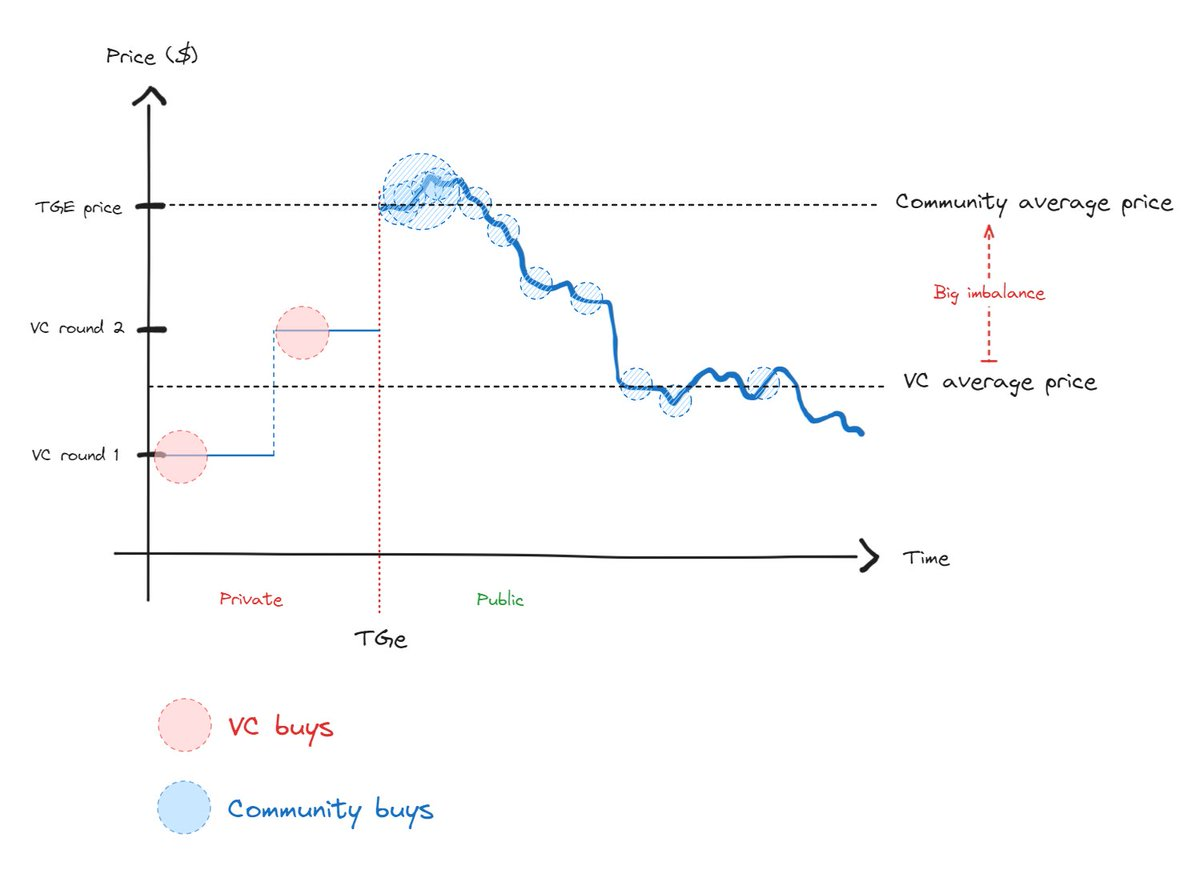

This high FDV leads to significant imbalance in cost structure and supply distribution between TGE buyers and private investors (see figure). This excessive imbalance exacerbates the ongoing tension between these two groups until market prices return to a reasonable level.

TGE buyers incur immediate losses after purchase, while VCs are incentivized to sell after their holdings unlock. When community buyers realize this trend, they stop buying, explaining the recent sharp decline in interest in new tokens.

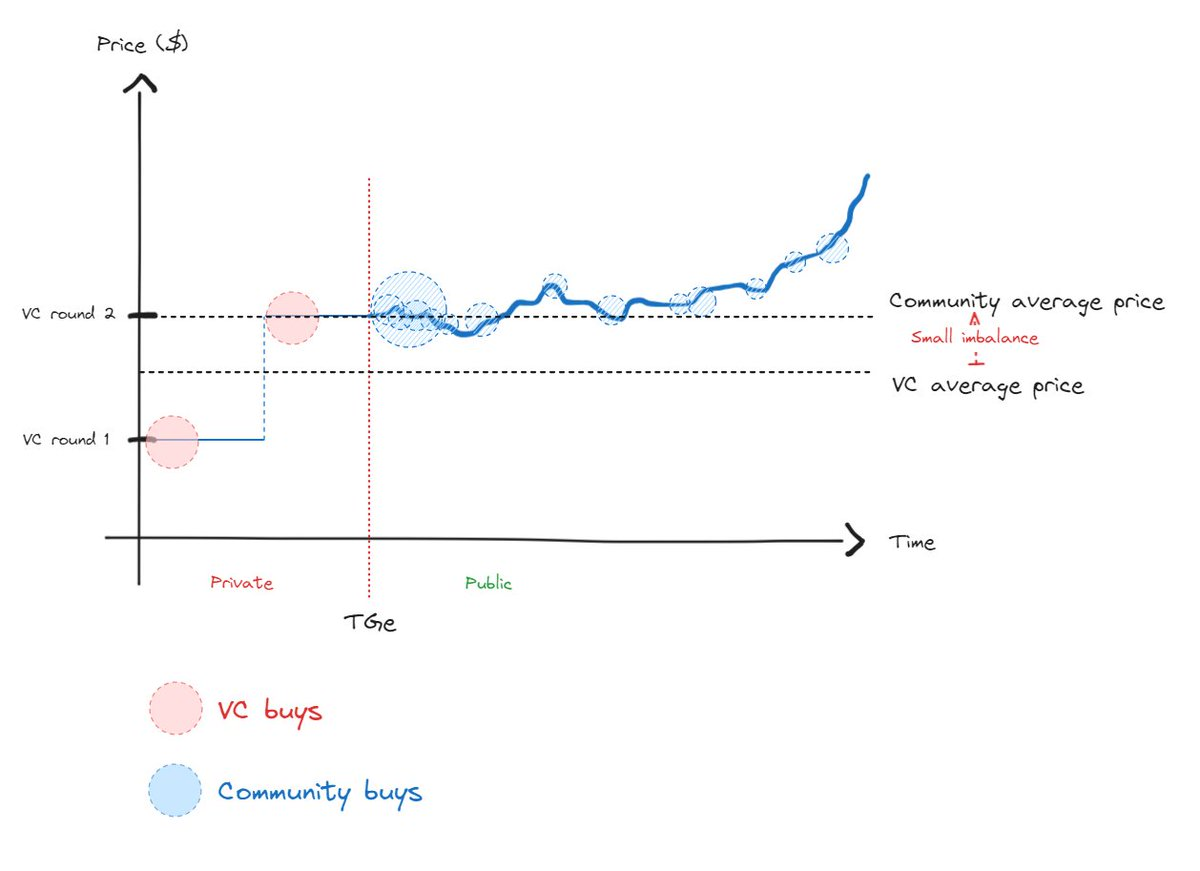

A healthier situation would show less imbalance between community and VC prices, promoting genuine price discovery (see below).

In an efficient market, price discovery is inevitable. While you can artificially influence price discovery in the short term, this only delays the return of prices to their true value. However, the development path of the market is interconnected, so a sustained downward trend is much more painful than reaching equilibrium directly.

Conclusion

An important subtlety in the myth of Icarus is to remind people not to fly too low. Just as Icarus was warned that flying too low could weaken his wings, issuing tokens with too low valuations may inhibit growth potential. This could hinder partnership opportunities, make talent retention difficult, and impact overall success. Issuing tokens before the project is mature enough is equally important to avoid high FDV situations.

Key Points

FDV is not a Meme: Avoid issuing tokens at high FDV. Just like Icarus, attempting to manipulate the market with inflated valuations is likely to backfire in the long run. High FDV tokens are a warning signal for retail investors—they typically avoid or even short assets with inflation risks.

Prudently Raise Venture Capital: Raise funds only when necessary and aligned with growth strategies. Choose venture capital firms you want to work with, rather than just selecting the highest valuation. Avoid accepting unsustainable valuation pressure.

Avoid Premature Token Issuance: Do not issue tokens solely because of achieving high FDV in the private market. Ensure there are clear signs of market appeal and product fit before issuing tokens.

Token Distribution: This is a topic worthy of separate discussion, but to facilitate effective price discovery, circulating supply should be maximized when issuing tokens. The target should be at least 20% to 50% of the total supply, rather than just 5%. However, the current regulatory environment may make this circulating supply target difficult to achieve.

Engage with Liquidity Providers: Liquidity providers are mature investors who take on project risk after TGE, so they play a crucial role in price discovery, rather than venture capitalists.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。