Author: 0xLoki

I. Definition of USDe: Fully Collateralized Semi-Centralized Stablecoin

Stablecoins can be classified in many ways, such as:

- Fully collateralized and non-fully collateralized;

- Centralized custody and decentralized custody;

- On-chain issuance and centralized institution issuance;

- Permissioned and permissionless issuance;

There may also be some overlap and changes. For example, in the past, we considered algorithmic stablecoins such as AMPL and UST to be stablecoins whose supply and circulation are completely regulated by algorithms. According to this definition, most stablecoins belong to the category of non-fully collateralized stablecoins, but there are exceptions, such as Lumiterra's LUAUSD. Although its minting and burning prices are regulated by algorithms, the protocol treasury provides collateral (USDT & USDC) worth no less than the LUAUSD anchor value, making LUAUSD both an algorithmic stablecoin and a fully collateralized stablecoin.

Another example is DAI. When DAI's collateral is 100% on-chain assets, DAI belongs to the category of decentralized custody stablecoins. However, after the introduction of RWA, some of the collateral is effectively controlled by real entities, transforming DAI into a stablecoin with a mix of centralized and decentralized custody.

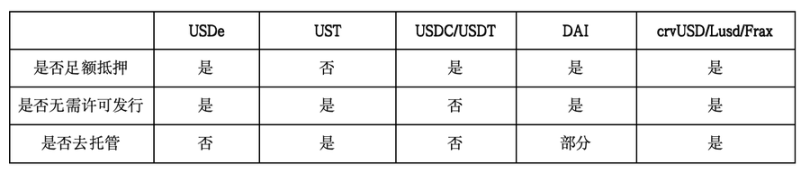

Based on this, we can strip away overly complex classifications and abstract them into three core indicators: whether there is full collateral, whether there is permissionless issuance, and whether there is no custody. In comparison, USDe and other common stablecoins have some differences in these three aspects. If we consider "decentralization" to require both "permissionless issuance" and "no custody," then USDe does not meet these criteria. Therefore, classifying it as a "fully collateralized semi-centralized stablecoin" is appropriate.

II. Collateral Value Analysis

The first question is whether USDe has sufficient collateral, and the answer is obviously yes. As stated in the project documentation, the collateral for USDe is synthetic assets composed of encrypted assets and corresponding short futures positions.

l Synthetic asset value = spot value + short futures position value

l Initially, spot value = X, futures position value = 0, assuming the basis is Y

l Collateral value = X + 0

l Assuming that after a certain period of time, the spot price rises by a dollars, and the futures position value rises by b dollars (a, b can be negative), the position value = X + a - b = X + (a-b), and the basis becomes Y + ΔY, where ΔY = (a-b)

It can be seen that if ΔY remains unchanged, then the intrinsic value of the position will not change. If ΔY is a positive number, then the intrinsic value of the position will rise, and vice versa. In addition, for delivery contracts, the basis is generally negative at the initial stage, and by the delivery date, the basis will gradually become 0 (excluding trading friction), which means that ΔY will inevitably be a positive number. Therefore, if the basis for the synthetic asset is Y at the time of synthesis, the value of the synthetic position on the delivery date will be higher than the initial state.

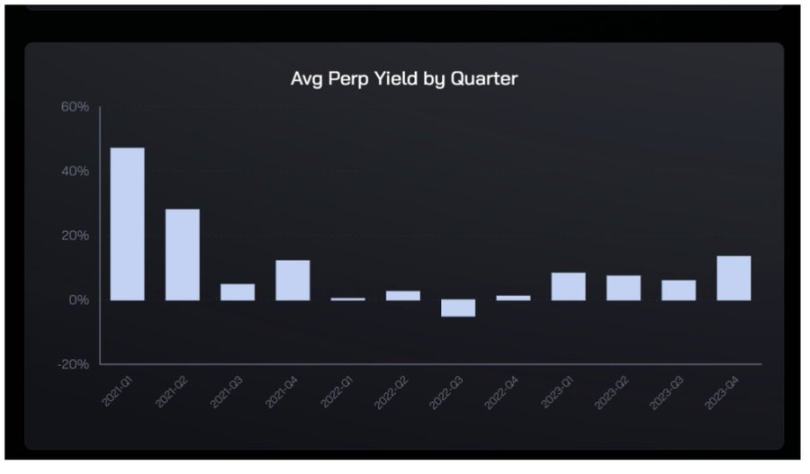

The combination of holding spot and shorting futures is also known as "cash and carry arbitrage." This arbitrage structure itself has no risk (but has external risks). Based on current data, constructing this investment portfolio can generate approximately 18% low-risk annualized returns.

Returning to Ethena, I did not find a precise definition of whether to use delivery contracts or perpetual contracts on the official website (considering the issue of trading depth, the probability of perpetual contracts is higher), but the on-chain address of the collateral and the distribution on CEX have been disclosed.

In the short term, these two methods will have some differences. Delivery contracts will provide a more "stable and predictable" yield, and the yield at maturity will always be positive. Perpetual contracts, on the other hand, are a product with a fluctuating interest rate, and the daily interest rate may also be negative under specific circumstances. However, from experience, the historical return of perpetual contracts' arbitrage is slightly higher than that of delivery contracts, and both are positive:

1) The nature of delta-neutral futures shorting is lending funds, and lending funds cannot maintain a 0 interest rate or negative interest rate for a long time. Additionally, this position stacks USDT risk and centralized exchange risk, so the necessary yield > risk-free yield in USD.

2) Perpetual contracts need to bear variable maturity yields and pay additional risk premiums.

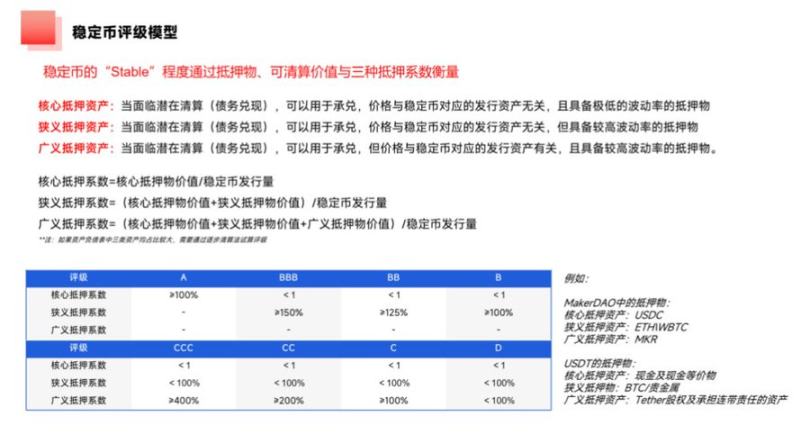

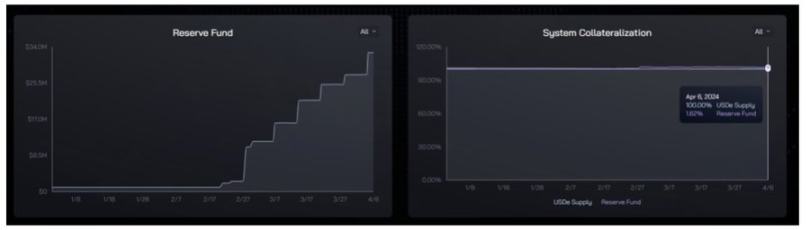

Based on this, it is completely wrong to worry that "USDe" will not be able to meet its obligations or to compare USDe to UST. According to the collateral risk assessment framework introduced at the beginning of the article, the current core/narrow collateral ratio of USDe is 101.62%. After considering the circulating market value of ENA15.7 billion USD, the broad collateral ratio can reach approximately 178%.

The concern about "potential negative rates will cause the collateral of USDe to shrink" is also not a major issue. According to the law of large numbers, as long as the time is long enough, the frequency will inevitably converge to the probability, and the collateral of USDe will maintain a long-term growth rate that converges to the average funding rate.

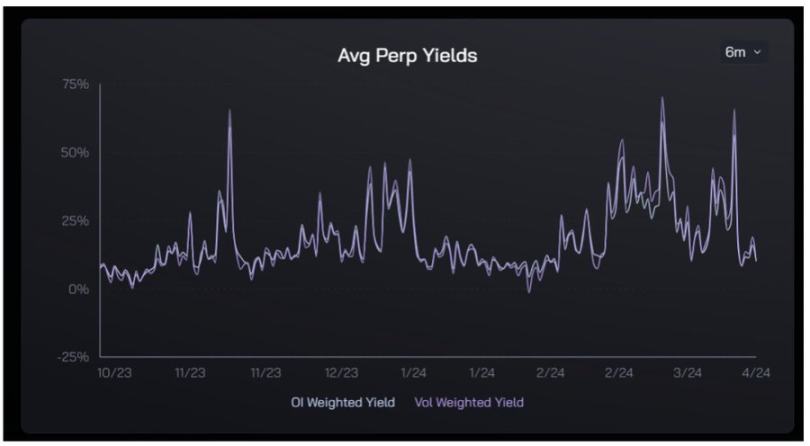

In simpler terms: you can draw a card an infinite number of times from a deck of cards, and if you draw a joker, you will lose 1 USD, but if you draw any of the other 52 cards, you will earn 1 USD. With a principal of 100 USD, do you need to worry about going bankrupt because you draw too many jokers? Looking directly at the data is more intuitive. In the past 6 months, the average contract rate has been below 0% only twice, and the historical success rate of cash and carry arbitrage is much higher than drawing cards from a deck.

III. Where Are the Real Risks?

1. Market Capacity Risk

Now that we have clarified that collateral risk is not worth worrying about, it does not mean that there are no other risks. The most noteworthy risk is the potential limitation of contract market capacity on Ethena.

The first risk is liquidity risk.

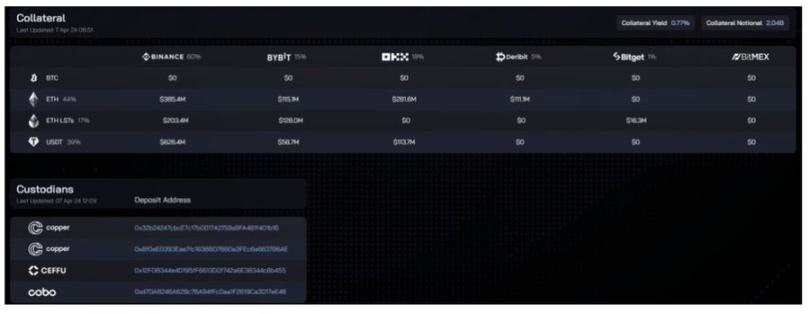

Currently, the circulation of USDe is approximately 20.4 billion USD, of which ETH and LST together account for approximately 12.4 billion USD. This also means that in a fully hedged situation, a short position of 12.4 billion USD needs to be opened, and the required position size is proportional to the size of USDe.

The current position size of Binance's ETH perpetual contract is approximately 30 billion USD, and 78% of the USDT reserve of Ethena is deposited in Binance. Assuming that the utilization of funds is uniform, this means that Ethena needs to open a short position with a notional value of 20.4 billion * 61% * 78% = 9.7 billion USD on Binance, which already accounts for 32.3% of the position size.

If Ethena's position size occupies a disproportionately high proportion on Binance or other derivative exchanges, it will have many negative effects, including:

1) It may lead to increased trading friction; 2) Inability to cope with large-scale redemptions in a short period of time; 3) USDe will push up the supply of short positions, leading to a decrease in the rate, affecting the yield.

Although some mechanized designs may help mitigate risks, such as setting time-based minting/burning limits and dynamic rates (LUNA has introduced this mechanism), the best approach is to not put oneself in danger.

According to this data, the combination of Binance + ETH trading pairs is already very close to the limit of market capacity that Ethena can provide. However, this limit can be surpassed by introducing multiple currencies and multiple exchanges. According to Tokeninsight data, Binance occupies 50.1% of the market share in the derivatives trading market. According to Coinglass data, apart from ETH, the total contract holdings of the top 10 currencies on Binance are approximately three times that of ETH. Based on these two pieces of data, the theoretical upper limit of USDe's market capacity is calculated as follows:

USDe market capacity theoretical upper limit = 20.4 (628/800) * 60% / 4 / 50.1% = 128 billion USD

The bad news is that USDe has a capacity limit, but the good news is that there is still a 500% growth potential before reaching the limit.

Based on these two limits, we can divide the growth of USDe's scale into three stages:

- 0-20 billion: Achieve this scale through the ETH market on Binance;

- 20 billion - 128 billion: Need to expand collateral to mainstream currencies with deep market depth + fully utilize the market capacity of other exchanges;

- Above 128 billion: Need to rely on the growth of the crypto market itself + introduce additional collateral management methods (such as RWA, positions in the lending market);

It should be noted that if USDe wants to truly flip centralized stablecoins, it needs to surpass USDC and become the second largest stablecoin at least. The current total issuance of USDC is approximately 34.6 billion USD, which is 2.7 times the potential capacity limit of USDe in the second stage, posing a significant challenge.

2. Custody Risk

Another point of controversy for Ethena is that the protocol's funds are custodied by third-party institutions. This is a compromise based on the current market environment. Coinglass data shows that dydx's total BTC contract holdings amount to 119 million USD, with only 1.48% on Binance and 2.4% on Bybit. Therefore, it is unavoidable for Ethena to manage positions through centralized exchanges.

However, it should be pointed out that Ethena uses "Off-Exchange Settlement" custody. Simply put, funds managed in this way do not actually enter the exchange but are transferred to a dedicated address for management, usually jointly managed by the grantor (i.e., Ethena), the custodian (third-party custodian), and the exchange. The exchange generates corresponding quotas based on the size of the custodied funds, which can only be used for trading and cannot be transferred. Settlement is then carried out based on the profit and loss situation.

The biggest advantage of this mechanism is that it "eliminates the single-point risk of centralized exchanges" because the exchange never truly controls these funds. At least 2 out of the 3 parties need to sign for the funds to be transferred. Under the premise of a trustworthy custodian, this mechanism can effectively prevent rug pulls by exchanges (such as FTX) and projects. In addition to the services listed by Ethena, Copper, Ceffu, Cobo, Sinohope, and Fireblocks also provide similar services.

Of course, there is a theoretical possibility of misconduct by custodians, but given that CEX still dominates and with frequent on-chain security incidents, this semi-centralization is a local optimal solution rather than a final form. However, APY is not free, and the key question is whether it is worth taking on these risks for the sake of increasing returns and efficiency.

3. Sustainable Interest Rate Risk

USDe needs to be collateralized to earn returns, and since the collateralization rate will not be 100%, the sUSDe yield will be higher than the derivative rate. Currently, approximately 470 million USD of USDe is collateralized in contracts, with a collateralization rate of only about 23%, and the 37.1% nominal APY corresponds to an underlying asset APY of approximately 8.5%.

The current ETH staking yield is approximately 3%, and the average funding rate over the past 3 years is approximately 6-7%. An underlying asset APY of 8.5% is completely sustainable, and whether the 37.1% sUSDe APY can be sustained will depend on whether there are enough applications to bear USDe, in order to lower the collateralization rate and bring higher returns.

4. Other Risks

These include contract risk, liquidation and ADL risk, operational risk, exchange risk, etc. Ethena and Chaos Labs provide more detailed explanations.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。