Cryptocurrency ETP will usher in a glorious moment.

Author: Diana Biggs, Partner at 1kx

Translation: Luffy, Foresight News

Exchange Traded Products (ETPs) provide a convenient, regulated, and low-cost way for retail and institutional investors to access a range of underlying investments, including cryptocurrencies.

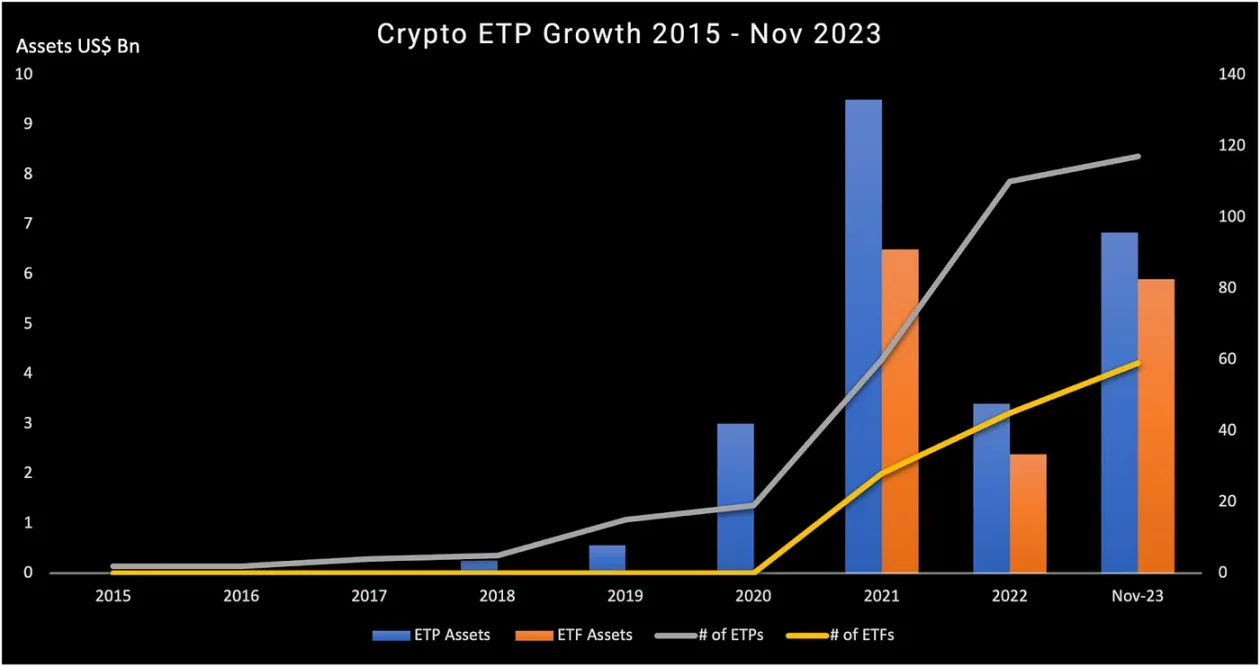

Since the launch of the first Bitcoin tracking product in Sweden in 2015, cryptocurrency ETPs have expanded from Europe to around the world. At the end of 2020, there were only 17 cryptocurrency ETP products, but now there are about 180. With more and more traditional financial institutions joining the ranks of cryptocurrency native companies in issuing ETPs, ETPs not only play a role in expanding investors' access to cryptocurrency opportunities, but also promote the overall acceptance of cryptocurrencies in the global financial market.

This article outlines cryptocurrency ETPs, including the types of products available, operating models, regions, and our focus in this rapidly developing field.

Cryptocurrency ETP Overview

What is a cryptocurrency ETP?

Exchange Traded Products (ETPs) are a type of financial product that is traded on regulated stock exchanges during normal trading hours, tracking the returns of underlying benchmarks, assets, or portfolios.

ETPs are mainly divided into three types: Exchange Traded Funds (ETFs), Exchange Traded Notes (ETNs), and Exchange Traded Commodities (ETCs). ETFs are investment funds, while ETNs and ETCs are debt securities. ETCs track physical commodities such as gold and oil, while ETNs are used for all other types of financial instruments. Since the creation of the first ETF in 1993, ETPs have evolved from tracking products in the stock market to become one of the most innovative investment product categories, providing investors with a range of innovative underlying assets investment opportunities.

Note: Although "ETP" is the general term for such products, the term "ETP" is sometimes also used to refer to debt securities exchange-traded products.

In particular, over the past 20 years, ETPs have continued to grow, with 11,859 products and 23,931 listings on 718 providers in 63 countries/regions and 81 exchanges worldwide, with ETF shares accounting for the largest share, approximately $10.747 trillion, or 98% of the total ETP assets of $10.99 trillion (data from ETFGI, as of the end of November 2023). Ovum Consulting expects the growth of ETFs to accelerate in the coming years, with the market growing at a rate of 13% to 18% annually from 2022 to 2027.

Source: ETFGI

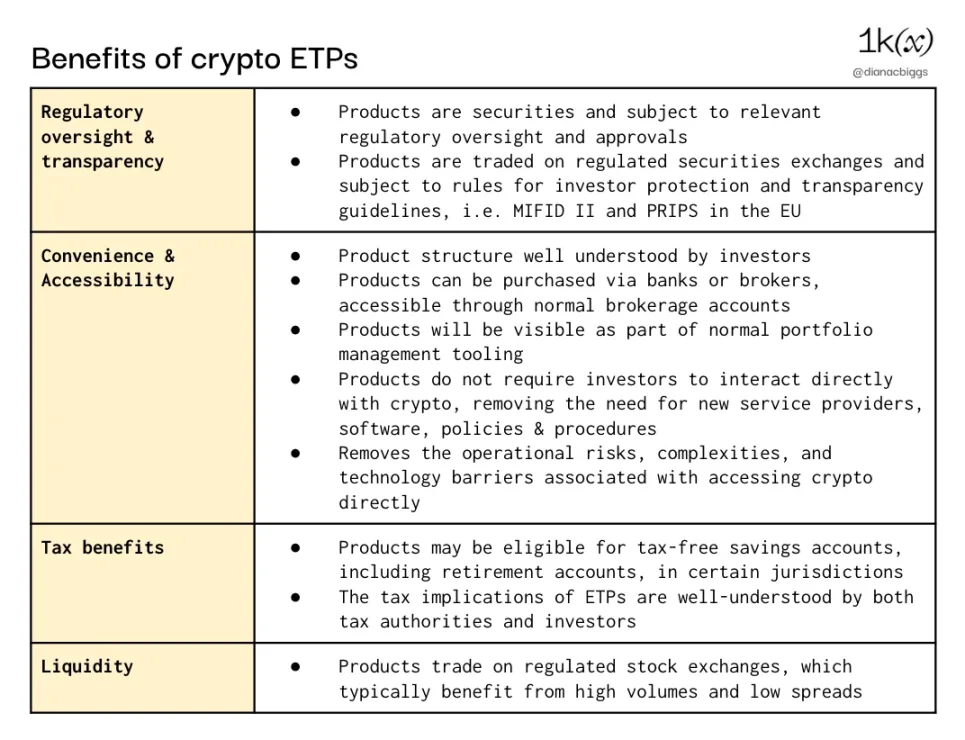

The convenience and accessibility of ETPs have made them a popular tool for opening up new asset classes (including cryptocurrencies) and investment strategies to investors.

The first Bitcoin ETP was launched in 2015 by XBT Provider (later acquired by Coinshares) on the Nasdaq in Sweden. The market's growth has been relatively moderate until the second half of 2020, when the number of products from new cryptocurrency native companies and traditional issuers began to grow strongly, a trend that has continued to this day. In February 2021, Purpose Investment in Canada launched Purpose Bitcoin on the Toronto Stock Exchange, becoming the world's first Bitcoin ETF. Although cryptocurrency ETPs constructed in the form of debt securities still far exceed cryptocurrency ETFs in terms of quantity and assets under management, we expect this situation to begin to change, especially with the opening of the U.S. spot ETF market.

Source: ETFGI

The number of cryptocurrency products has steadily increased, especially in the past three years. According to ETFGI data, as of November 2023, there were 176 cryptocurrency ETFs and ETPs. In the first 11 months of 2023, assets invested in these products grew by 120%, from $5.79 billion at the end of 2022 to $12.73 billion at the end of November 2023.

Why choose cryptocurrency ETPs?

The idea of cryptocurrency ETPs may seem counterintuitive to those in the native cryptocurrency field: ETPs introduce intermediaries, while the goal of cryptocurrency technology is to eliminate intermediaries. However, as easily understandable and regulated investment products, ETPs provide more opportunities for a wider audience of investors to access cryptocurrencies, who may not have access to this asset class for various reasons. For example, retail investors may lack the tools, time, risk tolerance, and expertise to invest directly in cryptocurrencies. ETPs, structured like traditional securities, are open to institutional investors, who may be limited to investing in these types of tools, or may avoid holding cryptocurrencies directly for regulatory, compliance, technical, or other reasons.

Compared to directly purchasing cryptocurrencies, ETPs also have potential drawbacks and considerations (not all investors will consider these as drawbacks). These include the fact that the fees for cryptocurrency ETPs have been much higher than those for other ETPs (although these fees have been declining with increased competition), limited trading access time compared to the 24/7 cryptocurrency market, counterparty and exchange rate risks, and settlement times.

Note: Examples of geographical restrictions include European cryptocurrency ETPs typically not being registered under the U.S. Securities Act of 1933, and therefore cannot be offered to U.S. investors; the UK FCA prohibits the sale of cryptocurrency ETPs to retail investors.

Product Structure

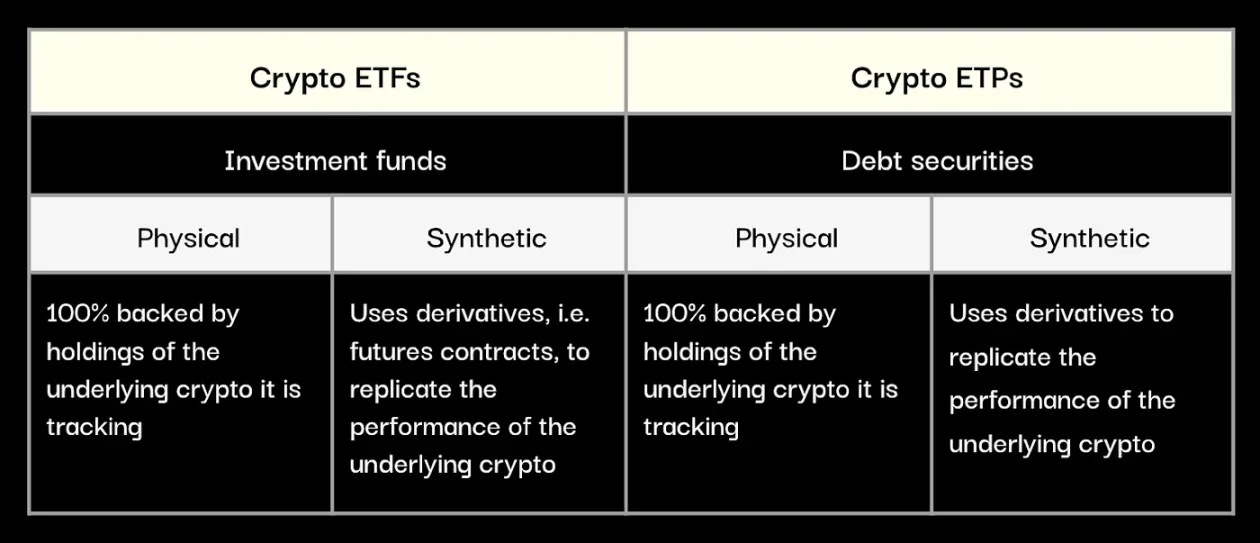

Broadly speaking, cryptocurrency ETPs are divided into two product categories and types: ETFs and ETPs, as well as physical assets and synthetic assets.

Cryptocurrency ETF Structure

The structure of ETFs is a fund, with ETF holdings in fund shares. Funds are legally separated from their issuing entities through trusts, investment companies, or limited partnerships to protect investors' holdings in the event of bankruptcy of the parent company/issuer. ETFs typically need to comply with additional rules and transparency requirements, depending on their jurisdiction; for example, ETFs registered in the EU and sold to EU investors typically need to comply with UCITS (Undertakings for Collective Investment in Transferable Securities) regulations, which bring diversification requirements, such as no more than 10% of the fund's total assets in a single asset.

Most cryptocurrency ETFs today are either spot or futures products. Spot ETFs have direct ownership of the underlying cryptocurrency assets and are guaranteed by independent custodians. For futures ETFs, the issuer does not hold the underlying cryptocurrency, but purchases futures contracts for the assets. Therefore, these products do not directly track the spot prices of the underlying assets, and are generally considered to bring greater complexity and costs, as well as less transparency and intuitiveness for investors.

Cryptocurrency ETP Structure

Cryptocurrency ETPs (in this case, the term refers to products other than ETFs) are structured as debt securities. Although their structural requirements are not as strict as ETFs, their disclosure requirements are very similar.

Physical cryptocurrency ETPs are collateralized debt contracts, with 100% backing provided by the holdings of the underlying cryptocurrency they track. The cryptocurrency assets are purchased and held by an independent third-party custodian under the supervision and control of a designated trustee, who represents the rights and interests of the ETP holders and is responsible for organizing redemptions in the event of the issuer's bankruptcy.

Synthetic ETPs are uncollateralized debt contracts, meaning the issuer does not need to hold the assets being tracked by the product, but instead uses derivatives and swaps to track the assets (exact structures and terms may vary). Therefore, synthetic ETPs carry greater counterparty risk, as there is no legal requirement for the products to be fully backed by the underlying physical assets. XBT Provider (and Valour) are two issuers of cryptocurrency ETPs that provide synthetic products.

Overall, most cryptocurrency ETPs in the market are physical ETPs, as many investors prefer the transparency and reduced counterparty risk provided by this structure.

Cryptocurrency Product Issuers

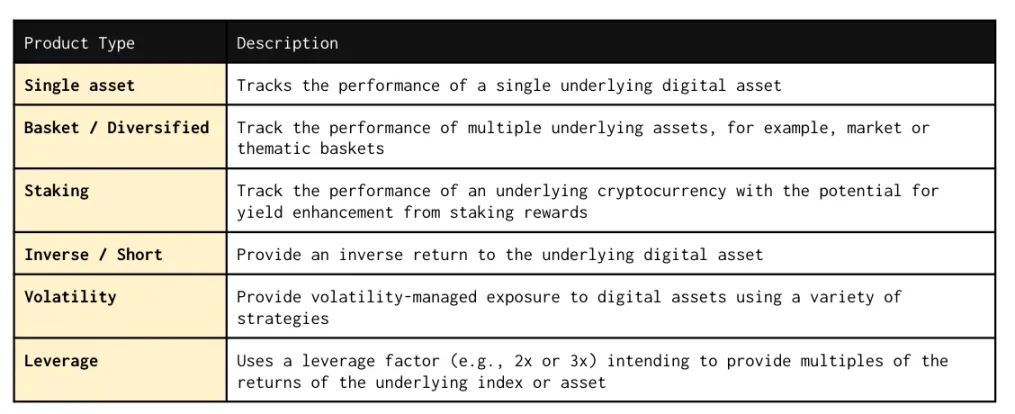

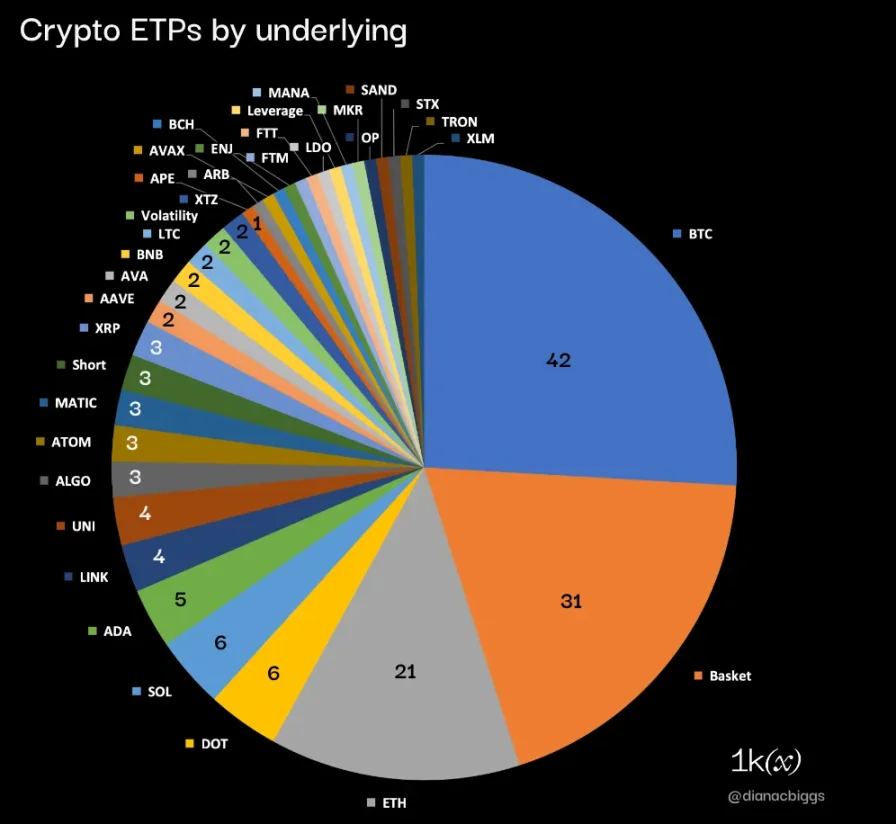

Cryptocurrency ETPs initially started with tracking single digital assets, but now the range of cryptocurrency ETPs available in the market also includes asset baskets, staking, shorting, leveraged products, and some indices designed to manage volatility.

In terms of underlying assets, according to recent data compiled by BitMEX Research, excluding stocks and over-the-counter funds, of the 162 cryptocurrency ETPs, Bitcoin, Ethereum, and basket products account for 58%, while the remaining 42% are long-tail single digital assets, as well as short, volatility, and leveraged products.

Data for 162 cryptocurrency ETPs (excluding stocks and over-the-counter funds); Source: BitMEX Research, 1kx Research

Of these 162 products, 121 are ETPs and 41 are ETFs, with 16 being futures ETFs and 11 awaiting the launch of a spot Bitcoin ETF. There are currently a total of 14 staking products (meaning investors can benefit from the yield of the staked assets): 13 ETPs and 1 ETF.

Largest Products by Assets Under Management (AUM)

The largest cryptocurrency ETP by Assets Under Management (AUM) is the ProShares Bitcoin Strategy ETF, a U.S. futures ETF product, which held assets of $1.68 billion as of January 2, 2024. As shown in the table below, of the top 14 cryptocurrency ETPs ranked by asset size, 9 track Bitcoin (64%); the remaining five track Ethereum (3), Solana (1), and BNB (1).

Source: BitMEX Research, 1kx Research

Of these 14 products, 4 are registered in Switzerland (all issued by 21Shares), 3 in Canada, 2 in Jersey, 1 in Germany, 1 in the United States, and 1 in Liechtenstein.

Among the top 14 products ranked by asset size, 4 are ETFs, with 3 being spot and 1 being futures; the remaining 10 are ETPs, with eight being physical asset ETPs and two being synthetic asset ETPs.

Product Innovation

The launch of new cryptocurrency ETPs needs to consider several limiting factors, including regulatory and stock exchange requirements and permissions, liquidity requirements, investor demand, and the accessibility of public price data and trading pairs. As more participants enter the market seeking to gain market share and differentiate themselves, and as regulatory bodies, service providers, and investors' understanding and acceptance of this asset class improve, we see issuers and index providers continuously innovating their products.

Cryptocurrency ETP Operating Models

The process of creating ETPs starts with the issuer (the investment company or trust issuing the product), who drafts a prospectus for approval by regulatory authorities. These may vary by jurisdiction, but generally, the documents need to include detailed information about the issuer, director identities and financial statements, product and scheme design, an overview of the underlying assets, expected markets and service providers, a comprehensive overview of potential risks, asset valuation (NAV) and NAV calculation methods, and detailed information about fees and redemption processes.

After obtaining regulatory approval and successfully engaging necessary service providers, the issuer must apply for listing on the required stock exchange. Rules about which types of products and underlying assets are eligible for listing vary by exchange.

The operating model and scope of service providers may vary by product type, jurisdiction, and the issuer's scheme design. An overview of the typical model is as follows:

In the primary market, the issuer exchanges product shares with Authorized Participants (APs) in exchange for the underlying cryptocurrency assets ("physical") or cash equivalents, and delivers the underlying cryptocurrency assets to or from a designated custodian as needed. Depending on the structure, transfer agents and trustees may be involved in clearing collateral and transferring funds.

While APs manage primary market creations and redemptions, market makers provide liquidity in the secondary market, ensuring continuous and efficient trading.

Investors buy and sell products in the secondary market, typically placing orders through banks or brokers, who execute orders directly or through other intermediaries on relevant stock exchanges.

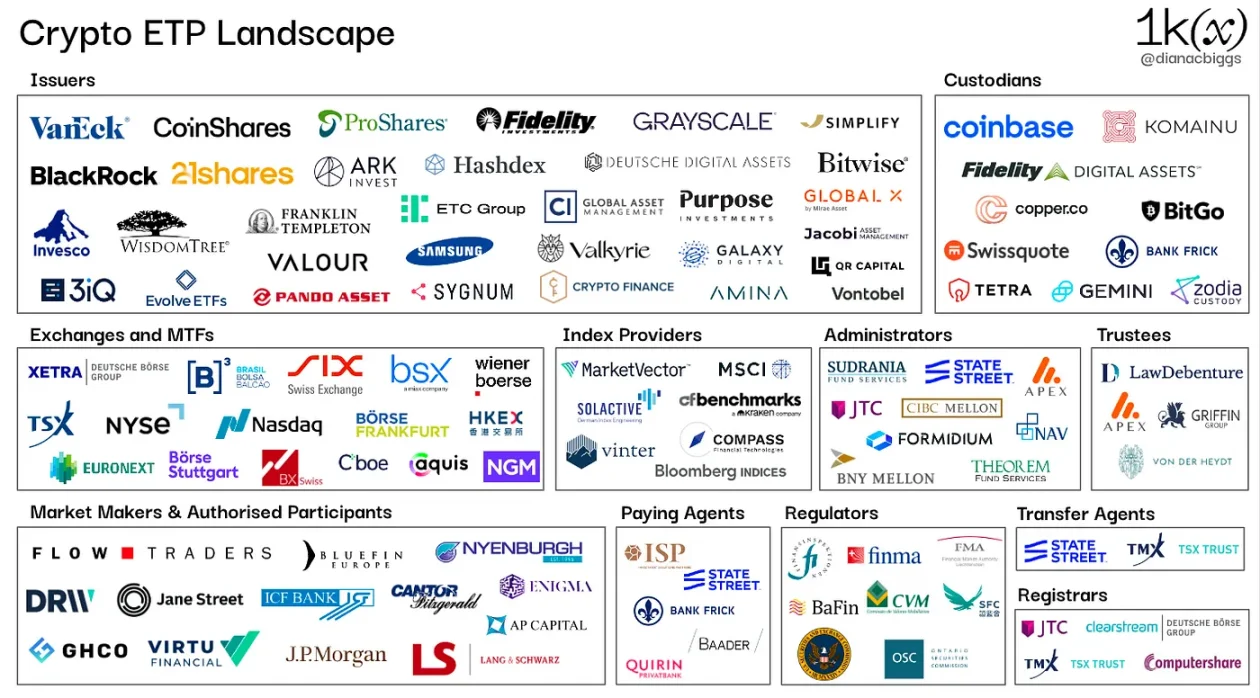

Stakeholders and Service Providers

Issuers

Issuers are responsible for the overall design and creation of ETPs, coordinating and managing relevant intermediaries throughout the product lifecycle. Regulatory oversight of issuers varies by jurisdiction. Regulatory authorities assess issuers during the prospectus approval process, as do stock exchanges during the listing process, with requirements that may include corporate governance, capital requirements, and regular audits. Issuers typically establish independent special purpose vehicles (SPVs) to issue products. Initially, most cryptocurrency ETP issuers were native cryptocurrency companies, such as Coinshares, 21Shares, 3iQ, Hashdex, and Valour, but in recent years, an increasing number of traditional financial companies have joined, including WisdomTree, Fidelity, Schroders, VanEck, and Franklin Templeton and BlackRock, pending approval from the U.S. Securities and Exchange Commission.

Custodians

Custodians hold the underlying cryptocurrencies behind physically backed ETP products. The custodial institutions used by ETP issuers include Coinbase, Fidelity Digital Assets, ital Assets, Komainu, BitGo, Copper, Swissquote, Tetra Trust, Zodia Custody, and Gemini.

Market Makers

Market Makers (MM) are liquidity providers hired by the issuer to provide bid and ask quotes on exchanges according to agreed terms, ensuring necessary liquidity for the ETP. Market makers mainly include Flow Traders and GHCO.

Authorized Participants

Authorized Participants (usually banks or brokers) have the right to create and redeem product shares directly with the issuer on a daily basis. They deliver the underlying assets or cash equivalents to the issuer in exchange for newly created ETP shares, or return shares to the issuer in exchange for the underlying assets or cash. Participants' interest in cryptocurrencies, especially assets other than BTC and ETH, may vary due to factors such as regulatory uncertainty and market conditions. Active Authorized Participants in cryptocurrency ETPs include Flow Traders, GHCO, Virtu Financial, DRW, Bluefin, and Enigma Securities. JPMorgan, Jane Street, and Cantor Fitzgerald & Co were recently designated as Authorized Participants in the U.S. spot Bitcoin ETF filings.

Index Providers

Index providers are responsible for creating, designing, calculating, and maintaining the indices and benchmarks tracked by ETPs, providing transparency and reliability to issuers and investors. In some jurisdictions, index providers are regulated, such as in the European Union under the Benchmarks Regulation (BMR). Active index providers in cryptocurrency ETPs include MarketVector Indexes, CF Benchmarks (acquired by Kraken in 2019), Vinter (a native crypto index provider), Bloomberg, and Compass.

Exchanges and Multilateral Trading Facilities (MTF)

The willingness of exchanges and MTFs to list cryptocurrency ETPs depends on local regulations and regulatory approval of the issuer's prospectus. This becomes a business decision for exchanges and MTFs, depending on the issuer's and product's eligibility requirements. This typically involves an assessment of parameters such as liquidity of underlying assets, compliance, public pricing information, and risk mitigation. Rules for which types of products can be listed vary by exchange, for example, Xetra in Germany only lists asset-backed ETPs, while six Swiss exchanges have specific rules for eligible cryptocurrency underlying assets.

Trustees

Trustees are responsible for safeguarding assets and representing the interests of ETP holders or investors. Their specific roles and responsibilities may vary depending on the specific structure and legal arrangements of the ETP. Active trustees in cryptocurrency ETPs include Law Debenture Trust Corporation, Apex Corporate Trust Services, Bankhaus von der Heydt, and Griffin Trust.

Administrators

Administrators support the overall operational management of ETPs. Their services may include accounting, regulatory compliance, financial reporting, and shareholder services. Active administrators in cryptocurrency ETPs include Brown Brothers Harriman, JTC Fund Solutions, CIBC Mellon Global Securities Services, Theorem Fund Services, NAV Consulting, Formidium, and BNY Mellon.

Other Service Providers

Other service providers that may play a role in ETP planning and the product lifecycle include but are not limited to paying agents (responsible for registering new ETP units and obtaining ISINs from local institutions), transfer agents (used to maintain records of shareholders and other duties), calculation agents (used to calculate the net asset value of underlying assets), and registrars (used to maintain shareholder records). These different roles and responsibilities may overlap or be undertaken by different parties depending on the product type, issuer, and jurisdiction.

Explanation of Fees

ETPs charge management fees, also known as expense ratios or underwriting fees, to cover the costs of managing and operating the product. These fees are calculated annually as a percentage of the holdings and deducted from the net asset value on a daily or regular basis. Many early cryptocurrency ETPs were able to charge fees as high as 2.5%, while the typical range for ETP fees is between 0.05% and 0.75%. As alternative products charge as low as 0%, cryptocurrency ETPs charge 2.5% of AUM, indicating the stickiness and first-mover advantage of these products.

We expect fees to become a key differentiating factor for new products in the future, as demonstrated by current U.S. spot ETFs. The first companies to announce fees were Invesco, Galaxy, offering fee waivers for the first six months and the first $5 billion in assets, and Fidelity offering a 0.39% fee. As of January 8, other issuers' announcements confirmed that the fee war has indeed begun.

Source: James Seyffart, January 8, 2024

Region

Europe

Cryptocurrency ETPs originated in Europe, with the first Bitcoin product launched in Sweden in 2015 by XBT Provider, tracking synthetic assets. In Europe, cryptocurrency ETP issuers benefit from a single market, as once an ETP prospectus is approved by a regulatory authority in one European country, the product can also be listed in other member states (referred to as a "passport" prospectus). The SFSA in Sweden remains a popular choice for the approval of cryptocurrency ETP prospectuses. Germany is another jurisdiction that has approved cryptocurrency ETP prospectuses, and cryptocurrency ETPs have good accessibility on various exchanges, such as Deutsche Boerse, Boerse Stuttgart Group, and other leading exchange groups.

ETPs still dominate as the product type in Europe, and the lack of true cryptocurrency ETFs in Europe is largely due to the UCITS (Undertakings for Collective Investment in Transferable Securities) regulations. Overall, most European ETFs comply with UCITS regulations to benefit from the pan-European passport, allowing these ETFs to be sold to retail investors in other EU member states in addition to the registration country. However, UCITS rules and requirements are currently incompatible with single-asset tracking products such as Bitcoin ETFs. For example, UCITS diversification requirements include not allowing any single asset to exceed 10% of the fund, and the underlying assets must be eligible financial instruments. In June 2023, the European Commission tasked the European Securities and Markets Authority (ESMA) with investigating the need to update UCITS rules and focus on cryptocurrency assets. However, the purpose of this seems to be to determine whether more rules and investor protection are needed, rather than expanding the eligible product types. The deadline for ESMA's opinion is October 31, 2024.

Switzerland

In 2016, Switzerland became the second jurisdiction, after Sweden, to approve and list cryptocurrency ETPs. Bank Vontobel launched an ETP tracking Bitcoin on the SIX Swiss Exchange. Subsequently, the world's first cryptocurrency index product was launched in Switzerland in November 2018. This was a physically backed basket ETP consisting of Bitcoin, Ethereum, Ripple, and Litecoin, issued by 21Shares. SIX Swiss Exchange has specific rules for cryptocurrency underlying assets, including the requirement that "when applying for temporary trading permission, the cryptocurrency must be one of the 15 largest cryptocurrencies measured by USD market value," and according to our research, this cryptocurrency is widely used as an underlying asset in products on all global exchanges. BX Swiss, the Swiss securities exchange, also allows products with cryptocurrencies as underlying assets, with rules requiring the underlying assets to belong to the top 50 cryptocurrencies by market value.

United Kingdom

In October 2020, the Financial Conduct Authority (FCA) in the UK banned the sale, marketing, and distribution of any crypto derivatives to retail investors. Many cryptocurrency ETPs are listed on the Aquis Exchange in the UK, but are only available for purchase by professional investors.

Canada

Canada was the first country to approve a Bitcoin ETF, with the first product launched in February 2021 by Purpose Investments on the Toronto Stock Exchange (TSX), followed closely by an Ethereum ETF. In October 2023, 3iQ launched a physically backed Ethereum ETF with staking rewards included in the fund, a first in North America. Other Canadian cryptocurrency ETF issuers include Fidelity Investments Canada, CI Global Asset Management (CI GAM) in partnership with Galaxy, and Evolve Funds.

Brazil

Brazil followed Canada closely. The Brazilian Securities and Exchange Commission (CVM) approved the first Bitcoin ETF in the Latin American region in March 2021. Brazilian cryptocurrency ETF issuers include cryptocurrency asset management companies Hashdex and QR Capital, as well as Itaú Asset Management in partnership with Galaxy.

United States

To date, only cryptocurrency futures ETFs have been approved by the SEC and made available to investors. ProShares launched the first Bitcoin futures ETF on October 19, 2021, becoming one of the largest funds in history and attracting over $1 billion in funds in the first few days of trading.

Two years later, on October 2, 2023, ProShares, VanEck, and Bitwise launched the first batch of Ethereum futures ETFs in the United States. Futures products typically require investors to have more understanding and may incur additional fees, as well as the risk of tracking errors and performance declines due to frequent rebalancing. In fact, the underlying futures contracts are traded on the Chicago Mercantile Exchange (CME) and are regulated by commodity exchanges. This is a popular explanation for why futures ETFs were approved before spot products.

The first application for a spot Bitcoin ETF in the United States was submitted by the Winklevoss brothers in July 2013 and was subsequently submitted multiple times over the following years, ultimately being rejected. Ten years later, on June 15, 2023, the world's largest asset management company, BlackRock, submitted an application for the iShares Bitcoin Trust. The influence of the BlackRock brand and its outstanding track record (according to Eric Balchunas, Senior ETF Analyst at Bloomberg, BlackRock has been rejected only once out of 575 ETF products) changed the game and helped make the U.S. Bitcoin spot ETF one of the most anticipated products ever.

On August 29, 2023, the tide further turned as the U.S. Court of Appeals for the District of Columbia Circuit made a favorable ruling for Grayscale in the Grayscale v. SEC case, stating that the SEC's decision to block Grayscale's proposed Bitcoin ETF was "arbitrary and capricious."

Fast forward to today, 11 issuers have submitted applications for spot Bitcoin ETFs, which are currently under SEC review in S-1 filings: BlackRock, Grayscale, 21Shares & ARK Invest, Bitwise, VanEck, WisdomTree, Invesco Galaxy, Fidelity, Valkyrie, Hashdex, and Franklin Templeton. In recent weeks, there has been an increase in meetings between the SEC and issuers, and the SEC has requested all issuers to switch to a cash creation mode, meaning that the asset exchange for the creation and redemption of ETF shares must be in cash, not in exchange for Bitcoin. Typically, for efficiency reasons, the asset exchange between Authorized Participants and ETF issuers in creations and redemptions is done in-kind. While the SEC has not publicly stated the reason for its requirement to be in cash, it is likely that the SEC does not want to be seen as approving Authorized Participants (usually large banks and brokers) to engage in cryptocurrency trading.

As of January 5, 2024, all 11 applicants have submitted amended 19b-4s, which propose changes to the rules under which exchanges can trade the products. These changes must be approved by the SEC.

The final step is for the SEC to sign the final S-1 form. The market currently expects this to happen around January 10, with the listing and trading potentially completed within the next 24 to 48 hours.

We will closely monitor the fund flows and trading volumes in the first week to assess the competitive dynamics among the 11 issuers. Larger ETFs are favored by investors for various reasons, including cost efficiency and liquidity. Therefore, the seed capital amount for an ETF can provide a competitive advantage. Bitwise's S-1 filing submitted on December 29 indicated an initial seed capital amount of up to $200 million, while BlackRock showed a seed sale amount of $10 million. It is worth noting that there were rumors on January 5 that BlackRock may have prepared $2 billion for the first week of trading. Eric Balchunas, Senior ETF Analyst at Bloomberg, pointed out that given the seed investments in other funds, this fund size aligns with BlackRock's brand image, although it would far exceed any ETF previously launched.

BlackRock, VanEck, Ark & 21Shares, Fidelity, Hashdex, Invesco & Galaxy, and Grayscale have also submitted applications for spot Ethereum ETFs, with the first SEC response deadline set for May 23, 2024.

Hong Kong

Following the approval by the U.S. SEC, the Securities and Futures Commission (SFC) of Hong Kong approved cryptocurrency futures ETFs in October 2022. Southern Eastern Asset Management launched two funds, one for Bitcoin and one for Ethereum, on December 16, 2022. In December 2023, the Securities and Futures Commission and the Hong Kong Monetary Authority issued a joint announcement listing guidelines for cryptocurrency investment products, stating that "in view of the latest market developments," the Securities and Futures Commission will now accept applications for cryptocurrency spot ETFs. The updated SFC guidelines indicate that both physical and cash creation and redemption modes are permitted. Overseas-issued cryptocurrency ETPs that have not been specifically approved by the SFC will only be open to professional investors.

What's Next for Cryptocurrency ETPs

More and more investors are looking to include cryptocurrencies in their portfolios, and ETPs provide a familiar, convenient, and regulated way to access this investment. Driven by this demand, both native cryptocurrency asset management companies and traditional asset management companies are continuously participating in these products and innovating. By 2024, the expected approval of spot ETFs in the United States could become a catalyst for their growth globally.

As this field continues to evolve, we will focus on key areas including:

- The impact of intensified issuer competition on fees and ETP flows in other regions, and the potential consolidation or exit of smaller participants in the long run

- The shift in consumer and institutional understanding and acceptance of cryptocurrencies, supported by the marketing power of global leading asset management companies like BlackRock

- The increasing number of exchanges, asset management companies, distributors, and other institutional participants and service providers willing to engage in cryptocurrencies

- The timeline for accepting these products and integrating them into advisory models

- The development of institutional staking, including the growth of staking products available to investors and issuers developing liquidity solutions

- The growth of on-chain structured products: we believe the future is on-chain, and a recent collaboration between 21.co, the parent company of 21Shares, and Index Coop shows how ETP issuers are beginning to move in this direction

Note: Over-the-counter (OTC) closed-end cryptocurrency funds (such as those offered by Grayscale) are not included in this study.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。