A large number of ETF redemptions may exert selling pressure on the underlying market.

Authors: Dessislava Aubert, Clara Medalie

Translation: Block unicorn

Since the collapse of FTX, we have been closely monitoring the liquidity of cryptocurrencies. There is no hiding the fact: whether it is all assets or all exchanges, trading volume and order book depth have generally decreased, and even the latest market rebound has not been able to restore depth or trading volume to the levels before FTX.

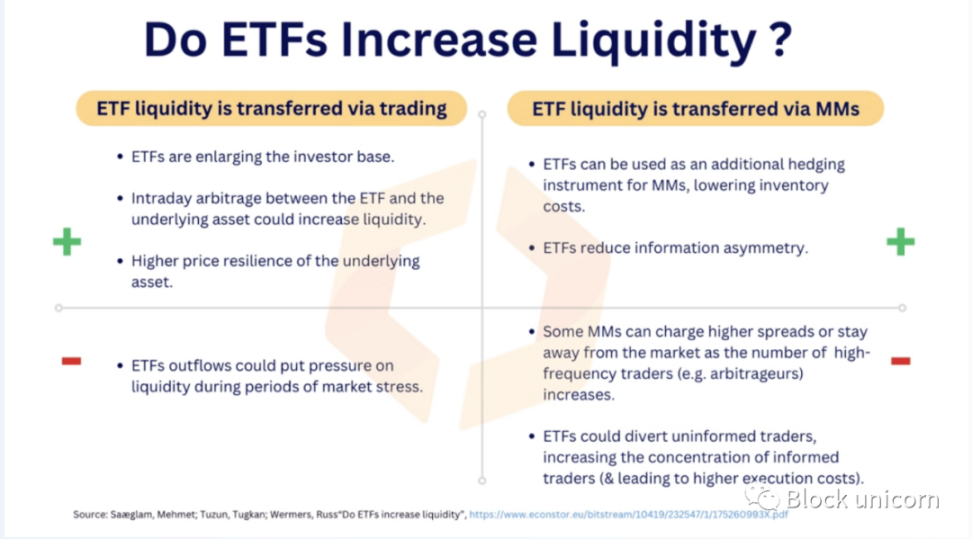

However, with the hope of obtaining approval for spot exchange-traded funds (ETFs) in January, it is expected that liquidity will truly recover quickly (although there are risks of negative impacts). This can be achieved in two ways:

Liquidity through trading transfer

Liquidity through market makers (MM) transfer

On the "ETF will enhance liquidity" side, there is a convincing argument that ETFs will expand the number of cryptocurrency traders, leading to larger trading volumes and a more efficient market. Market makers will also benefit from ETFs, as they may expand their activities while hedging.

On the "ETF will harm liquidity" side, the real concern is that a large number of ETF redemptions may exert selling pressure on the underlying market. As for market makers, they may charge higher spreads due to more informed traders. Let's take a look at the current state of Bitcoin liquidity to understand its impact.

Bitcoin Order Book

The collapse of FTX has led to a significant decrease in Bitcoin market depth. Not only did the sudden disappearance of FTX essentially reduce liquidity, but market makers also closed positions on many exchanges due to massive losses and a difficult market environment. The 1% market depth, i.e., the buy and sell quantities within a 1% price range in the order book, has decreased from approximately $58 billion across all exchanges and trading pairs to only about $23 billion.

The recent market rebound has had minimal impact on liquidity, and the observed slight increase is mainly due to price effects.

In the context of ETFs, why is market depth important? ETF issuers will need to buy and sell underlying assets. Although it is not yet clear where they will conduct these transactions—whether on spot exchanges, over-the-counter, or purchasing from miners—it is possible that liquidity on centralized spot exchanges will increase at some point, especially as many ETFs are expected to be approved at once.

From the perspective of arbitrageurs, liquidity is also important. ETF prices will need to track the underlying assets, and arbitrageurs will trade when premiums or discounts appear. Inadequate liquidity makes the work of arbitrageurs more complex through more frequent price discrepancies, so liquidity is crucial for market efficiency.

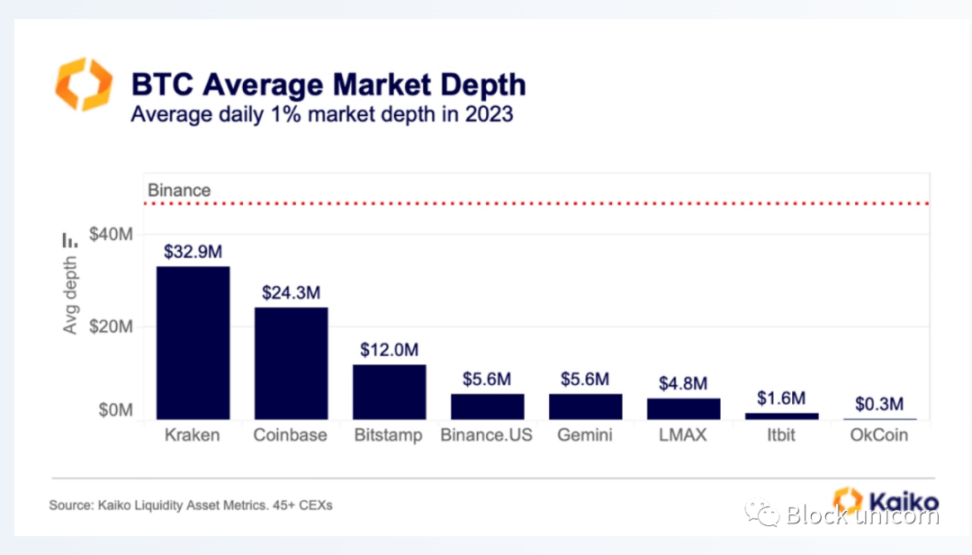

In particular, available cryptocurrency exchanges in the United States may play an important role in spot ETFs, currently accounting for approximately 45% of the global Bitcoin market depth.

In 2023, Kraken had the largest average Bitcoin order book depth at $32.9 million, followed closely by Coinbase at $24.3 million. For context, Binance's average daily market depth is indicated in red.

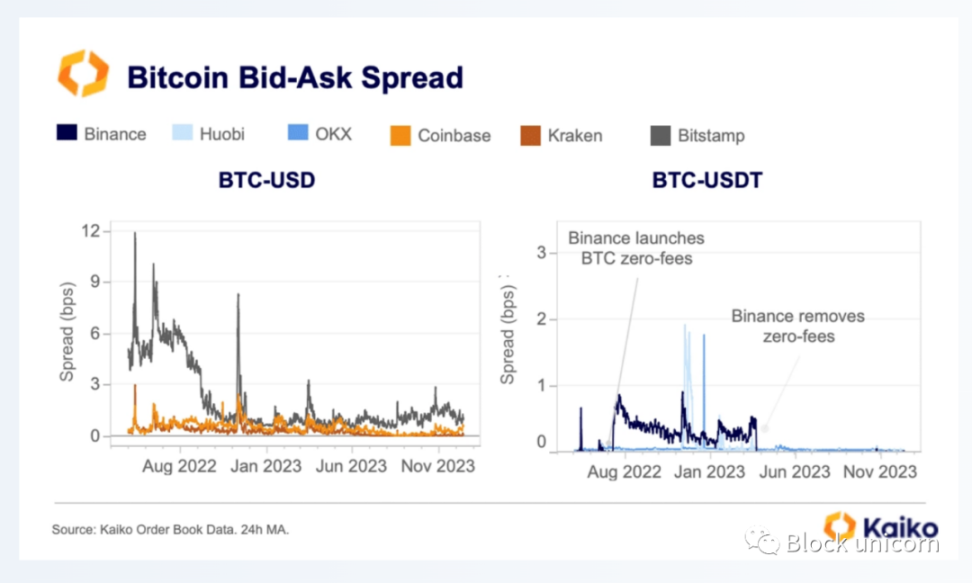

The approval of ETFs may also affect trading costs, as more informed investors enter the Bitcoin market. Over the past year, traders' costs, in the form of spreads, have mostly improved since last year, possibly due to lower price volatility.

In summary, Bitcoin market depth has remained stable for most of the time (with no change in liquidity), and spreads have mostly narrowed (lower trader costs), but the approval of ETFs may change this situation.

Bitcoin Trading Volume

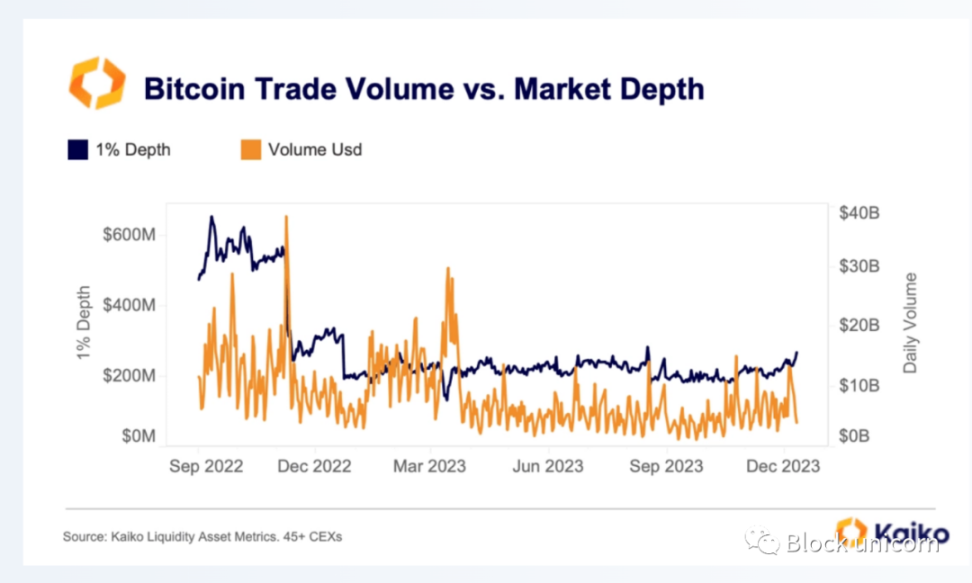

Compared to market depth, FTX's impact on trading volume is much smaller, accounting for less than 7% of global trading volume. Since November last year, there has been quite a large fluctuation in trading volume. In the first three months of 2023, trading volume remained at a relatively high level, then plummeted after the banking crisis in March, reaching multi-year lows in the summer.

We have seen some slight recovery in the past few months, especially in the recent market rebound, but overall, trading volume is still far below the levels before FTX.

Therefore, when comparing trading volume with market depth, we can observe that since November 2022, the decrease in depth has been more extreme, but much smaller than the fluctuations in trading volume throughout the year. This indicates that market-making activity levels have remained unchanged, with no new participants (or exits).

Bitcoin Dominance

Bitcoin remains the most liquid cryptocurrency asset to date and has shown the strongest resilience in difficult market conditions. ETFs are likely to further strengthen its dominance.

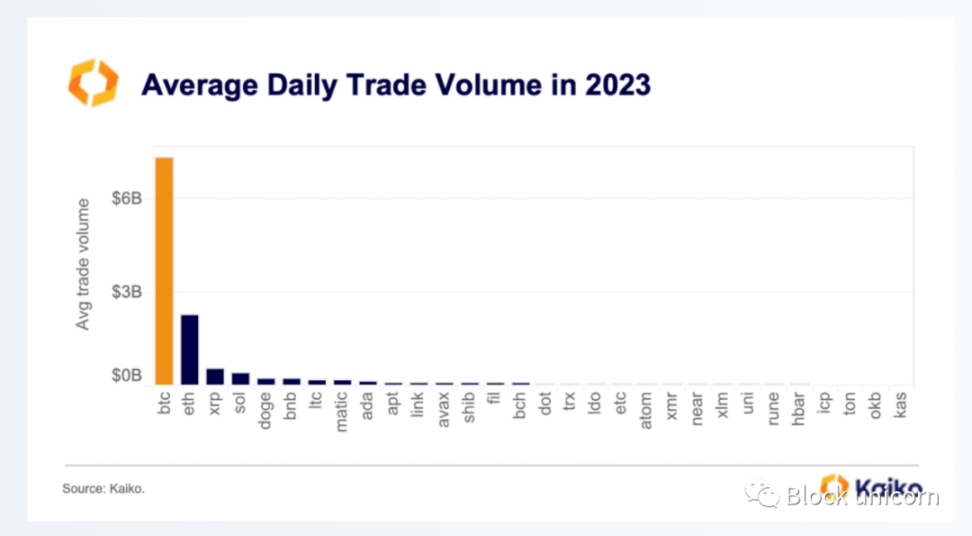

In the distribution of trading volume over the past year, we can see that the average daily trading volume of Bitcoin is roughly three times that of Ethereum and more than 10 times that of the top 10 alternative coins. It is worth noting that this trend was exacerbated by the Binance zero-fee Bitcoin trading promotion that ended in the spring.

The average daily market depth of Bitcoin is more similar to Ethereum, although it is still much larger than most alternative coins.

Conclusion

Bitcoin remains the most liquid cryptocurrency asset. However, since the collapse of FTX, both measures of liquidity have sharply decreased, with only slight recovery in the past few months. Therefore, the approval of ETFs is currently the biggest catalyst in the cryptocurrency market, promising significant potential upside and limited downside risks. Despite some liquidity risks, if investor demand increases significantly, ETFs are expected to improve market conditions overall.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。